Looks good decision by Govt

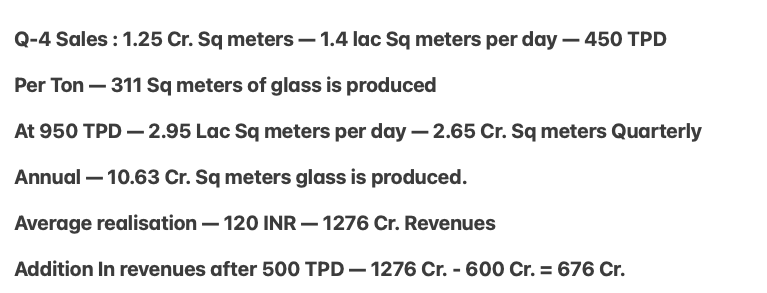

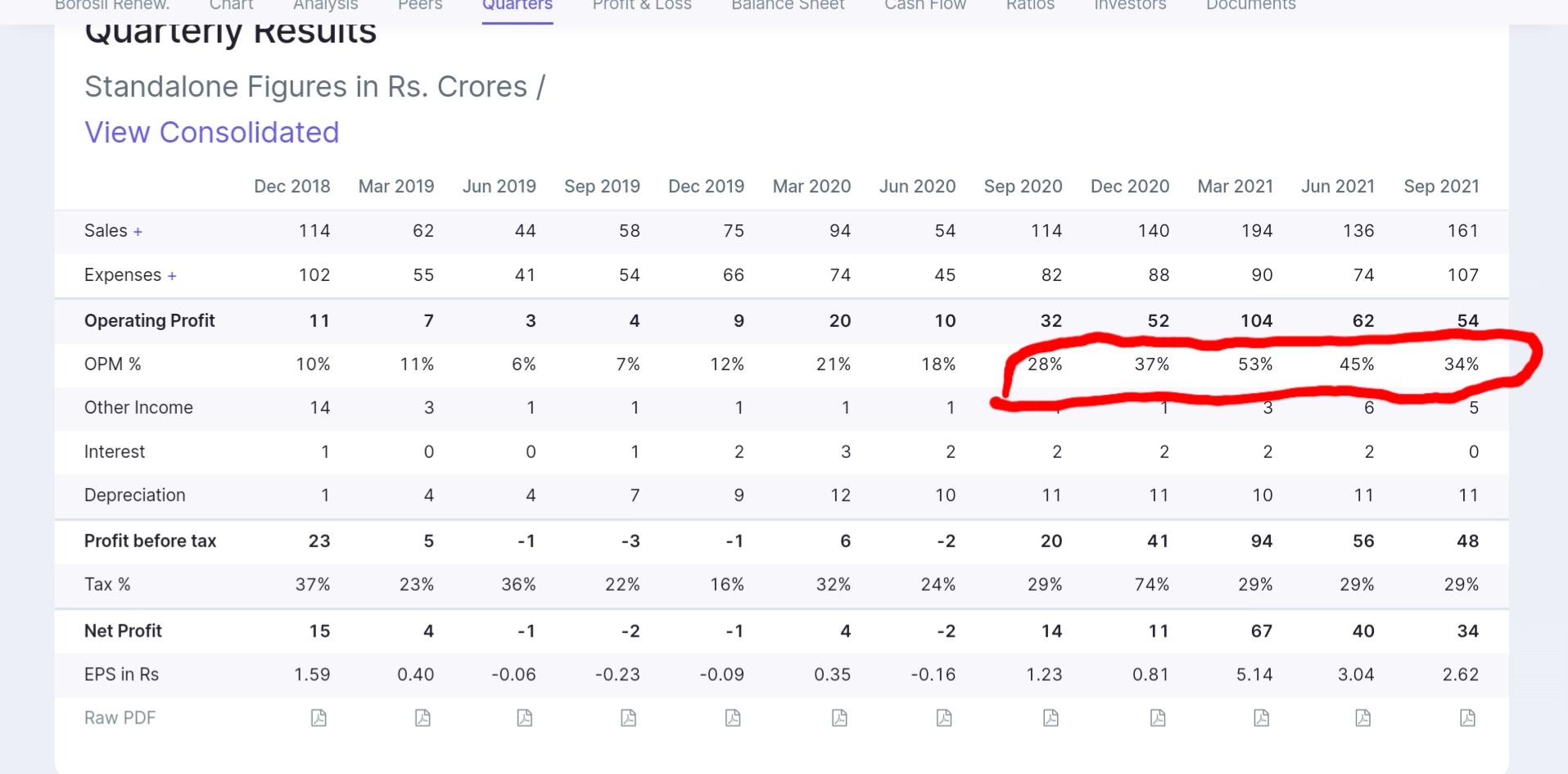

I was doing calculation for the BRL revenue for Q2FY22.

- Current capacity : 450 Ton per Day.

- 1 ton produces 200 sqmtr of solar glaas.

- Avg. realization taken = Rs. 118 per sqmtr (as per latest concall).

- Assume plant operated for 90 days.

- 70% final product obtained i.e. tempered glass.

if we multiply all these

= 67 crores

but q2 revenue was 160 crs.

what am i missing? kindly someone correct me

3 Likes

This calculation is based on their Q-4 numbers of last financial year.

I hope it will help you in calculating correct numbers.

@Investor_Mohit

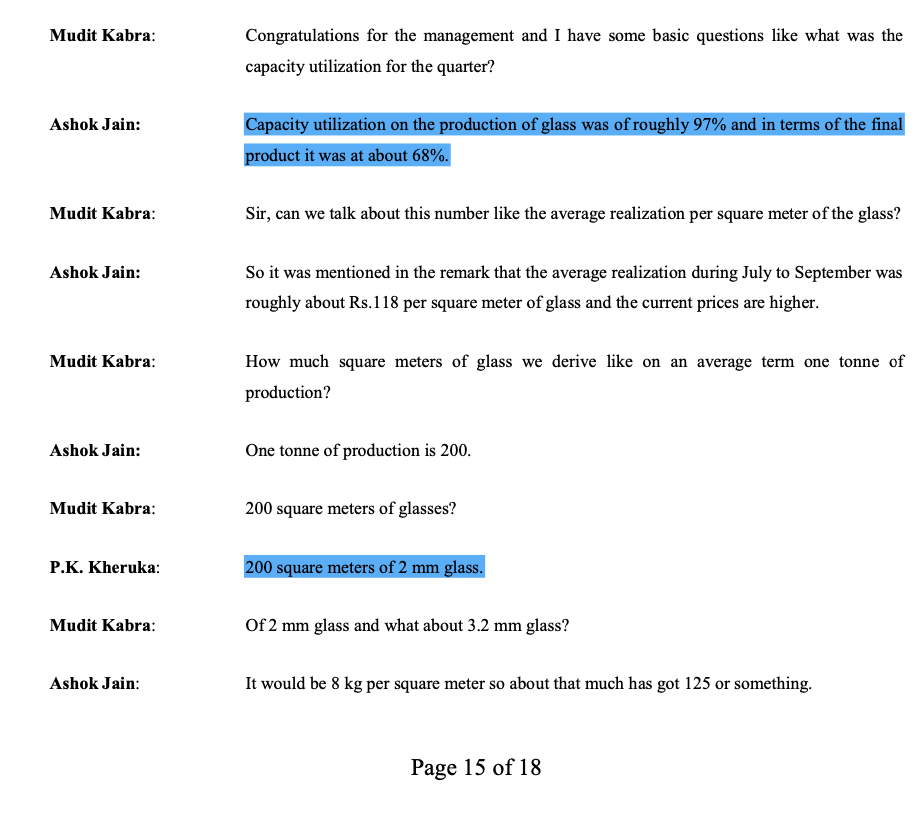

But as per their q2fy22 concall, management said that 1 ton produces 200 sqmtr of solar glass. is that correct?

Yes, We will have to get more clarity on that in the next concall.

As the final product was 68% of total capacity / production.

1 Like

As per Tata power MD, 8:00 onwards, solar glass factory fire in china caused solar input cost increase for them in last few months hence pressures on EPC margins, and expect to normalize going over next few months. Didn’t hear this in Borosil renw Q2 call.

3 Likes

Renewable growth trajectory keeps getting better, solar will be lion share of this growth at multifold ftom current yearly runrate(5X+)- to put it in perspective,

Internal government assessments indicate that achieving the same would require India to up its RE capacity by near 40 GW per annum over the next eight years. As of now, India has on an average added 8GW of RE per annum except for 2020 when we added 12GW. Hence, a 40 GW addition per annum is tall order.

Sector Tailwinds are getting stronger…China capacities playing catch up in their own backyard- supply for glass likely to lag demand. Borosilrenwable has delivered 4 consecutive Quarters of growth with stable margin range, with no wild swings in between.

3 Likes

Given the announcements at COP26, i’m just wondering why isn’t BR announcing another capex? It isn’t that already announced capex would fulfil all the demand or even a significant portion of it. Financing would be available in plenty for further capacities.

What is stopping BR?

2 Likes

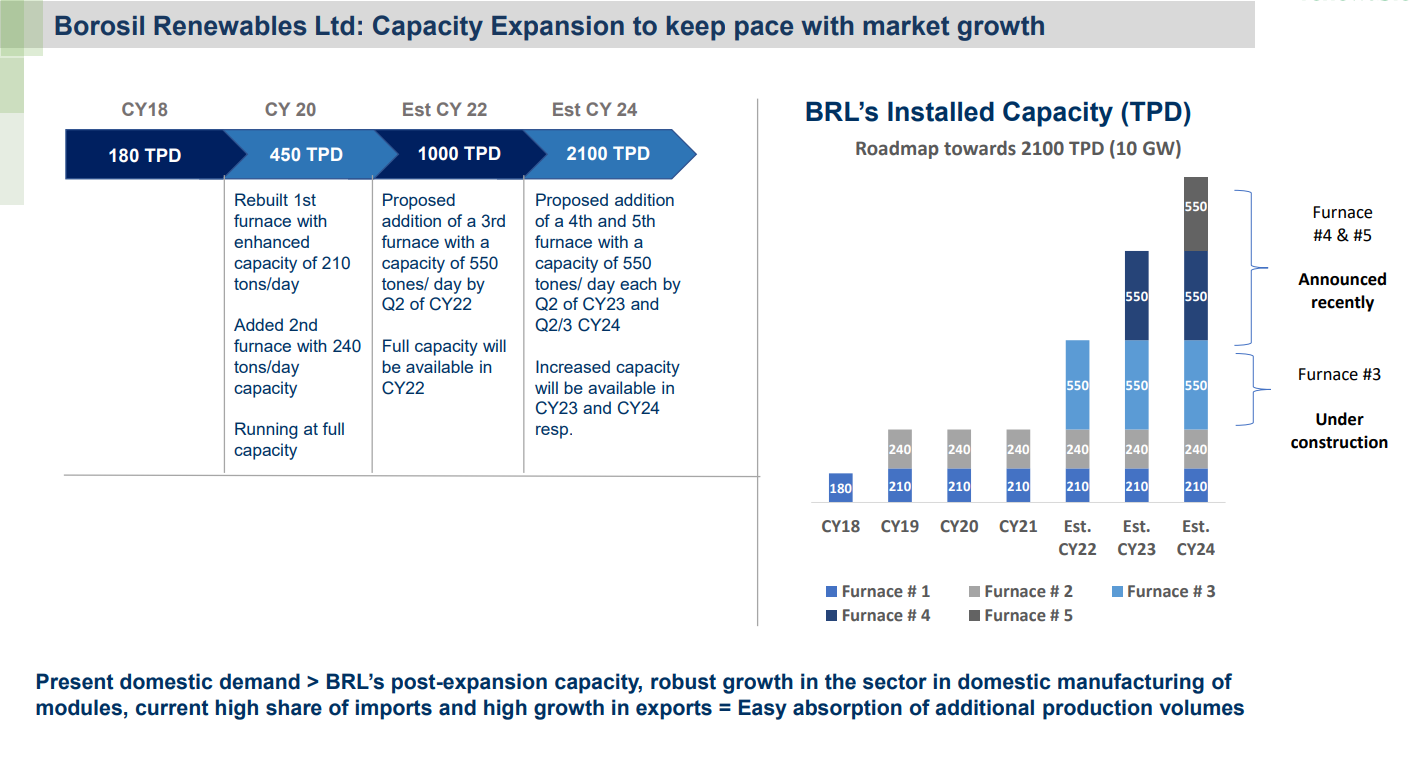

They have already planned to 4x the capacity over the next 3 years or so, that seems aggressive enough especially considering the fact that other players will look to enter the market over the course of time.

1 Like

4x capacity would still be around 20/30% of what India needs. Leave alone the export opportunities. I am aware that 4x is ambitious but the TAM here is equally large. Surely BR must think of adding more capacities.

From what we know, currently the co is pretty much debt free (LT loans perspective atleast)? SG3 and SG4 are being funded from internal accruals. SG5 is via QIP, internal accruals and debt.

1 Like

Ken’s article on borosil summary, refraining from posting the article here since it is a paid article (to comply with the ethics of forum) :

China accounts for 97% of Solar Glass production.

Borosil in India has 40% share and largest non Chinese producer in world. Rest Indian market is catered by China and Malaysia.

India by 2030, wants to fulfill 50% of energy demands by 2030.

Gold plus directors were approached by government to enter solar glass due to lack of domestic supply. By September 2023, will make 300 TPD.

Realiance : Reliance plans to build Solar GigaFactory, 100GW capacity by 2030, it will be in entire solar chain from silica to cell to module.

Adani : 45GW by 2030.

India, there are 40 module makers and 10 solar cell makers, Glass was monopolized by borosilicate renewables. As per Kheruka, no one entered Solar glass was because of margins and returns. It is highly capex intensive business, The learning curve is also longer.

Xinyi and Flat Glass account for 50% of market.

Glass accounts for 7-8% of Total Solar module while solar cells make up 50%, hence most players focussed on cells in order to lower their cost of production.

Assembling module is easy, hence waree and Vikram solar chose to source RM and compile them to create a module.

Governments PLI : For cells and modules close to 4500 crores, plans to raise to 24000 crores.

Asahi India partnered with vishaka group.Capacity : 3Gw in 18-20 months.

Competitors will have to spends years in learning the thing like borosil did it.

Given competition from China at lower price, plus high capex, St. Gobin had to shut down glass business but borosilicate held on.

Borosi patent the antimony glass. It is world’s 1st manufacturer to do the production of 2mm glass.

When one exports to china Solar glass has 30% duty, when china exports, they get subsidy of 17%, there is no level playing field.

March, 2021, 9.71% import duty from Malaysia, will remain in force for 5 years.

ADD on China is valid till Aug, 2022. Company has filed to extend.

Xinyi Solar says, price difference between theirs and borosil’s product is 5.5%.

As per local customers, Before Duties, there was 5-6% difference, now the price for both of them Is same.

BOROSIL IS IN SWEET SPOT FOR 2-3 YEARS, THEN NEED TO INNOVATE AND DIFFERENTIATE TO SURVIVE.

Switching suppliers require testing and research, it will be difficult to break-in borosils market since they will be in learning phase.

Kheruka’s comment on competition : Without Nadal and Novok, I dont think Federer would have been as good.

26 Likes

Run up has been quite steep, valuations are now over $1B, it is at 5.5X FY23 sales, 16X EBDITA ( I.e. including capacities that will come online in Q3 22). 1+ year Near future seems fully priced in at current valuations.

Next round of capacities increase beyond 1000TPD is yet to get actionized, Balance sheet likely to get heavy. Med to long term is Bit tricky business given history of price volatility and semi commodity perception.

Question is does risk reward favors from here on? Let the winners ride or take some part profit off the table? Technicals might offer a cue.

Invested

Why do you need to do sales and EBITDA multiples, when company is decently profitable?

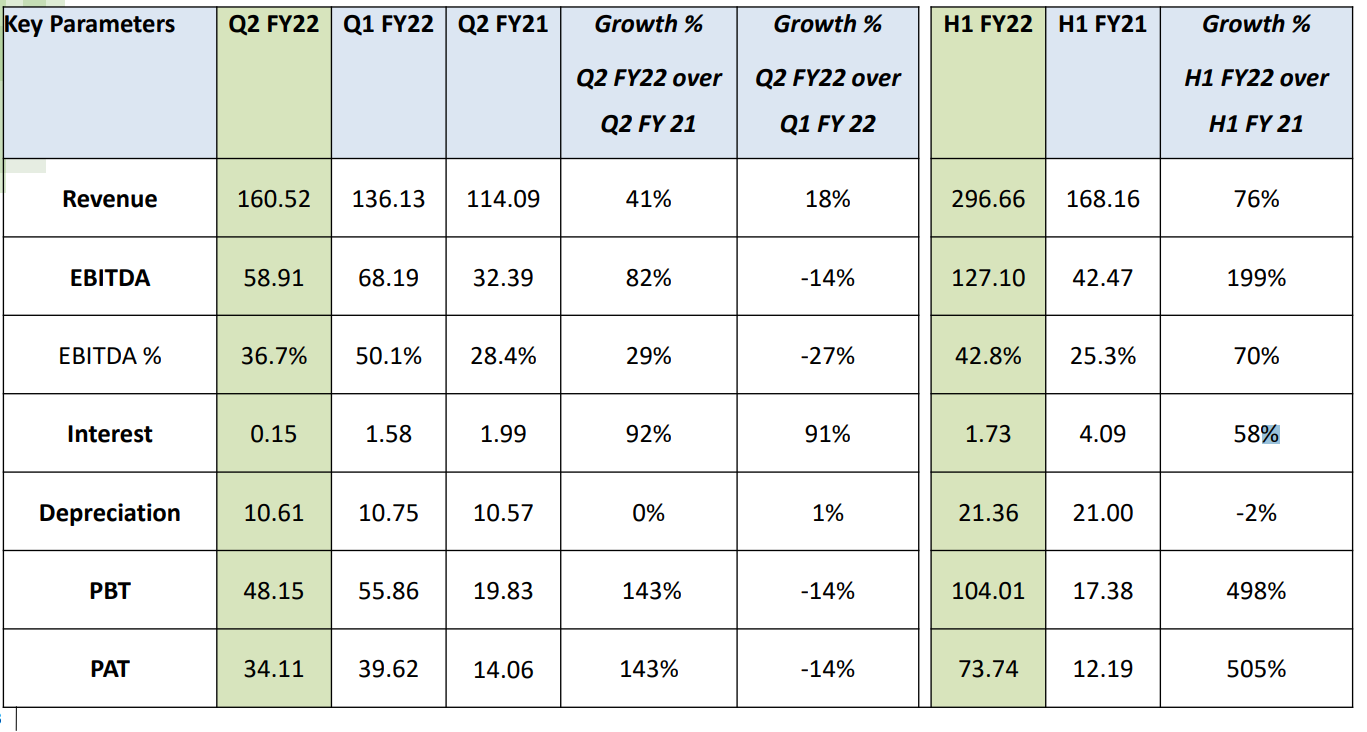

With 450 tpd company has delivered Rs74crs profits in 1HFY22. Selling price has gone up 18% post end of 2Q. For the time being ignore that. Lets extrapolate Rs34crs (2QFY22) profits for next 2 quarters you get Rs68crs. So conservatively company will do Rs142crs profit in FY22. Current market cap Rs7686crs. So stock trading at 54.1x FY22 P/E on conservative estimates

Capacity is going up 4.7x by CY24/ FY25 with great demand both in India and exports.

8 Likes

Article is behind paywall but I found explanation about exports most interesting. As per the article, Q2 FY22 exports of 55.1 Cr which comes to 34.3% (exports -20%, SEZ - 14%) of the gross revenue and goes to mention that it believes that world is looking for alternate source to Chinese solar glass. Also article mentions that other manufactures are not able to deliver fully tempered 2mm glass. In China, they Heat Strengthened (HS) glass is used as 2mm glass. So Borosil clearly has an edge over its competition as HS glass is less strong than fully tempered 2mm glass. Currently 20% of revenue comes from export which can go up 25% on the expanded capacity, which can help de-risk the business model.

Rest of the points are discussed on this forum as well as in the concalls.

13 Likes

I think it was last concall or prolly the one before in which Mr Kheruka had clarified that exports don’t really give them a higher realisation and the exports were mainly to derisk themselves.

As of now and even when the expanded capacity comes up, Borosil is unlikely to cater to exports since the domestic demand will outstrip supply.

So while the quality edge remains a good news, capacity constraints will always be an issue, which is in a way good thing as BR investor but also leaves you feeling that the Company could do a lot more.

In many ways, the Company does need a big strategic investment from a player like RIL / Tatas if it has to come close to matching the overall demand for its glass.

1 Like

Capacities expansion is given and even ful utilization is given, question is can they sustain current EBDITA margins at 40%+( linked with glass prices) once supplies( Chinese and India) catch up over next year, point was to call out risk reward keeping that in mind on current valuations. Add to that depreciation will accelerate with every round of expansion, thus bottomline decelerate faster in case of EBDITA compression.

Great sector, superb quality mgmt and execution - no second thoughts there. Joyride may last till supply deficit lasts and it can not be forever. Again valuations are individual aspect.

Invested

6 Likes

Borosil Renewables announces the demise of Chairman Emeritus On 12 December 2021

Isn’t his son part of the business from very long time? I beleive succession plan has always been in place

1 Like

Oh yes, i thought it was shreevars dad. However it is Pradeep’s dad

Given that Borosil Renewables caters to only 35% of the country’s solar glass requirements and even with increased capacities, they will be at 50-55%, I think there may be plenty of room for growth.

Also, this may prove to be an additional trigger

" In March 2021, the Ministry of New and Renewable Energy (MNRE) announced that BCD on solar cells (25%) and modules (40%) will

be levied wef April 1, 2022 and this has been agreed to by the Ministry of Finance and have also advised that the customs notificationin this regard shall be issued at an appropriate time"

6 Likes