Borosil Renewables should stay in sweet spot as Indian Renewable Power Industry will have to depend on Indian Manufacturing rather than China for components to assemble solar panels.

(i) Rise in Soda Ash Prices : 1882 CNY/T at June end to 3100 CNY/T at the end of September

Though Mr. Pradip Kheruka has clarified that they have absorbed some costs and passing on the rest to consumers, impact on demand side will have to be watched out. Inability to pass on further increase in costs can be a risk. Price hike in Soda Ash seems to be temporary as it is available in bulk and GHCL is expanding their capacities as well.

Still Sillica Sand comprises of 75% composition of Glass so impact of hike in soda ash prices might not be very high.

(ii) Shortage of Raw Materials (Polysilicon / Wafers) :

Manufacturing process of Poly-Si and Wafers is an energy intensive process. Polysilicon is the key raw material in manufacturing wafers which is then used in solar cells. As China is having electricity shortage due to their decarbonisation plan and multiple other factors, Indian panel manufacturers might have a shortage of solar cell which is mostly imported from China as of now. It can have an adverse impact on Borosil as well. The only way we can mitigate this threat is to outsource Poly-Si / Wafers from Wacker, 2nd largest Poly-Si manufacturer globally (based out of Germany).

Supply Demand Mismatch :

Any new capacity will take at least 12-18 months and with electricity shortage persisting in China, Borosil will stay in sweet spot. Adani is coming with their own capacities but they won’t get the quality of glass which they need from the first day.

Along with Supply Demand mismatch, we will have to keep an eye on the capex plans whether they might be delayed as most of the machineries come from China and Europe.

While price of PV glass in August increased 18.2% YoY, that of adhesive film went up by 35% over the same period. Polysilicon prices have gone up to exceed $260 per kg, according to the companies.

Prices were up during Q-2 in China while the management of BR was expecting pressure on prices. Still we will have to see what will be the impact of rising gas and soda ash prices.

Soda Ash prices have gone up 110% since beginning of the year and has gone up 22% in last 4 weeks - as per the article dated 27th Sept 21. So this would surely have impact on company’s margins, not sure by how much.

As per the article , they say

" For us, the biggest bill of material component is float glass, something which is available in India. Its easier to localize"

Although it will take 2 years for them to start production, news like these shows glass demand will continue to go up, which will absorb all additional capacity to be added by Borosil.

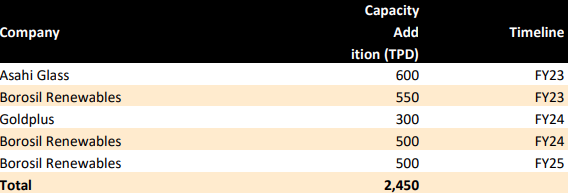

Lots is talked about how other competitors are entering this space and will take market share away from BR. Below is a snapshot of all solar glass manufacturing capacity that will be added till FY25. 60%+ of this is BR increasing its own capacity.

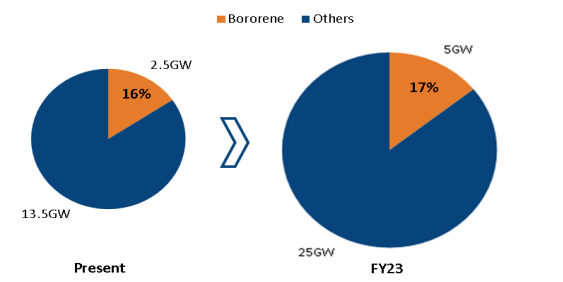

Further, BR doesn’t have a very large share of the market today anyways, imports still make a large chunk of this market. Growth and runway is long and plenty of room to grow for all scalable players in this market.

Prevailing prices higher than Q2 avg prices, ability to deliver higher EBDITA despite rising RM cost demonstrated, Export share picking up. Superb YoY and stable QoQ( some realization drops led profit moderation)

At 200 cr net profit ( annualized) , available at sub 6K cr mkt cap, opportunity size is huge and growing, capacity doubling from mid CY 22, excellent cash flows.

While concall details will have broader details, here are some qualitative inferences.

Exports picking up despite being slightly lower margin profile, why? - geo diversification leads to some risk management but at the same time Borosil wants to have relationships going with global markets - longer term this helps on multiple softer aspects - global credentials, quality improvements, BR while increasing capacities is assured of another channel of sales outside India - thus stronger business case of investments.

Forward integration - not interested !! - it’s easy to get carried away with Renewables being the buzz word - mgmt knows their Forte and wants to build scale here first.

Fast forward FY 24 - Can BR demonstrate operating leverage with 4X capacities- answer in today’s call was inconclusive - however in past mgmt has called out possibilities- shared administrative staff, shared utilities bring adjacent, new machinery likely delivers better throughput( atleast theoretical) - better to show numbers and tell later!!!

RM impact and next 2 Qtr story till big jump comes in capacities by Q2 22- whole narrative around margin impact going on - Gas+Soda together will impact at 8%, however realization being higher by 20% - net net beneficial as prices linked to China and energy situations ( read cost) to stay elevated for atleast winters- BR is winner among losing majority in manufacturing. Talk about luck!!!

Picture in Q2 23 - slightly more than Double capacities( from 450 TPD to 1000 TPD)

Base case - current Q2 realization rates and slightly elevated RM as current, EBIDTA 35%+ = Rev 350 cr, EBIDTA 130 cr

Optimist case - Higher realization as Q4, RM cost heads lower to normalcy, EBIDTA 50%+ = Revenue 400 cr, EBIDTA 225 cr

Pessimistic case - realization dips by 10% type( that puts to 100 Sq Mt range a long term case when demand wasn’t this great) from Q2 22, normalized RM, EBIDTA still at 30% = revenue 320 cr, EBIDTA 100 cr+

Now assigning probability to above is all it takes for investment case, if investing was that simple

Point is even at base case in FY 22 ( basis capacity fully online ) we are looking at annualized 1400 cr revenue and 500 cr + EBDITA- we are 3 quarters away so not a pipe dream - it’s available 4X sales and 11X EBDITA at current mkt cap. We can discount any operating efficiency gains from 2X capacities as buffer. Also where else we get sold out at full capacity scenarios, before capacities come in

Can’t think of better risk reward to play renewable theme, even though stock continued in lower circuit after results came out !!! , market has its own unique ways!!

If you hear mgmt in con call - they resort to distribute production carefully for e.g. Export vs Domestic question in Q2 22 concall. If you read thread and previous concalls this is a quite conservative mgmt, who plans additional capacities very carefully ( at calibrated pace wrt to demand), every quarter after quarter its full/near full capacity production.

Demand visibility so strong that short after 2X capacities announcement ( live in Q 2 23), further 2X were announced in short succession and they are only supplier in India in near future atleast till other capacities come online, however by that time demand will stay much ahead. Look at Glass capacities vs Solar mfg capacities- it’s a catch up game atleast for mid term.

If not done already, Suggest to listen last 4 quarters concalls and mgmt interviews, that’s where one can connect dots, again that’s my way of looking at things and can be wrong.

There is insane level of demand for this product. Chinese are consuming their own capacities. European and other regions want suppliers out of China (China +1). They told in the conference call that they can’t service many players since they sort of can’t fulfill their minimum capacity requirement. For eg: they have 450 TPD capacity, and if some big player comes in and says give me guaranteed 200 TPD, they can’t since they have to service existing customers such as Adani, Waaree and Tatas. With larger capacities, they can fulfill it easily with long-term contracts as soon as production starts. I don’t know of Reliance, but if they plan to not enter glass industry, they might strike a big contract with BR for their requirements. So, their new capacities will be sold out pretty easily.

Do we know for sure that Chinese don’t have any spare capacity? Even if such is the case Chinese are know to ramp-up their capacities pretty fast given demand for product.

As the demand of the product is even greater than the supply they will ramp-up & it won’t matter,

Because after years of initial pain,Now with economies of scale, Borosil has the ability to match the prices at which the Chinese sell.

So anyone will prefer to buy it from Borosil instead of importing it from China where delivery takes longer & Payment has to be upfront.

See the screenshot in this post, where Chairman of Waaree Energies mentioned about this.

I am still confused about this point.

I also heard management say that exports are less profitable. Does this make business sense to let go profitability for geographic diversification?? Lets discuss this point please.

Sometimes you have to let go short term profits for long term gains. Borosil always wants to develop long term relationships with important large customers, including overseas customers. It takes long time to develop any new export customer or new market. Borosil can not deny these customers ordered quantities just because they are getting higher prices domestically. Also supplying to demanding export customers help Borosil to improve their quality and benchmark themselves with the best in class competitors in the world. In nutshell, it is long term play and doing it right in my opinion.