Saw this one twitter , so most of the capacity expansion is already priced in ?

1 Like

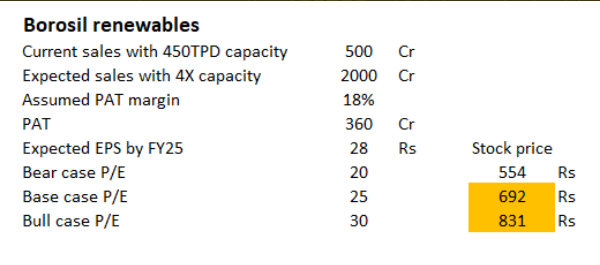

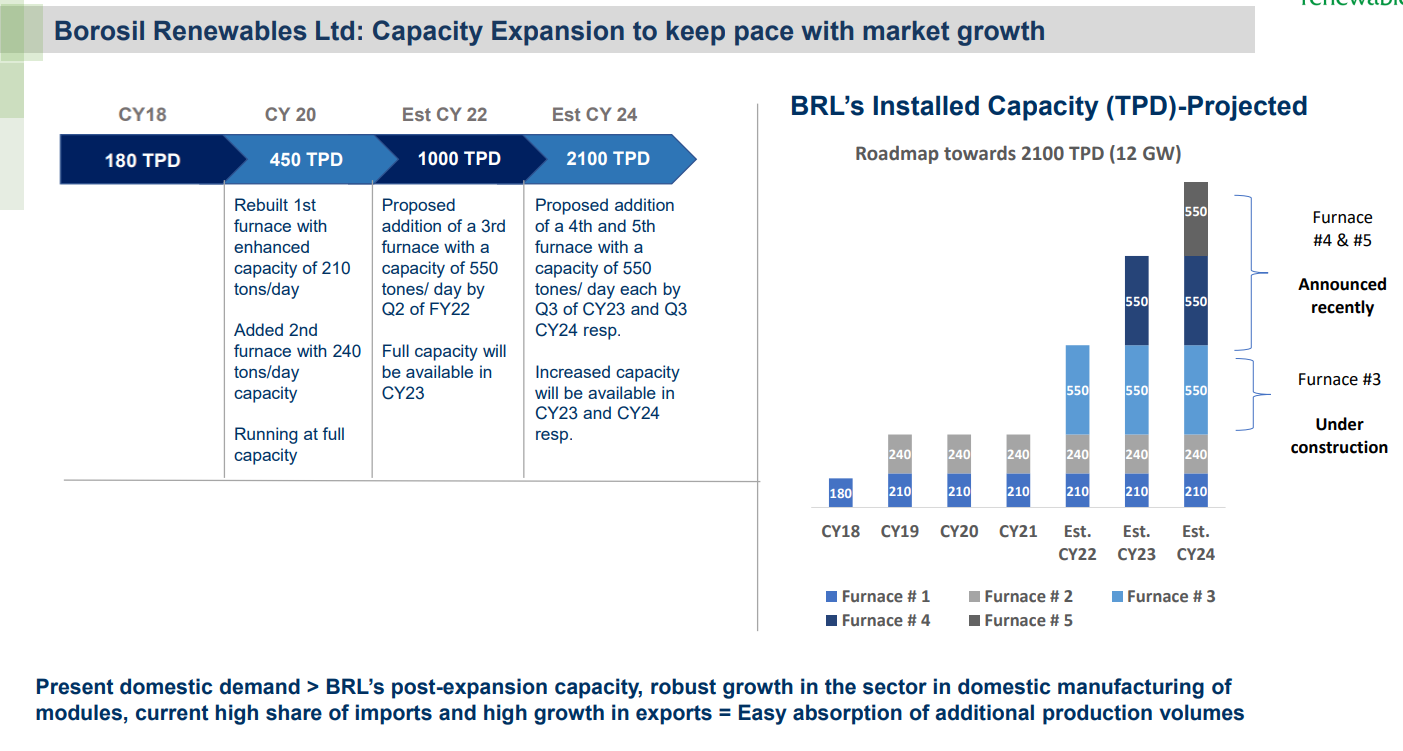

Well FY22 sales are likely to be in the vicinity of 550crs. Current capacity is 450 TPD and by FY25, the co plans to have 2000TPD. That is 4.4x the current capacity. Conservative revenue = 2420 crs. EBITDA % (conservative) = 30%. So annualised EBITDA = 726crs.

EV / EBITDA of Flat Glass = 40

Assume conservative number of 25.

EV at 25 multiple = 726*25 = 18150crs

Current mcap = 9024crs

Also. Valuations are very subjective. It’s an art and not a science. The multiples hide many qualitative factors.

D - Invested from 400 levels.

2 Likes

Only hitch in the calculation is assumed PE . For a high growth (30%+), highly profitable company, market can assign PE anywhere from 30 to 80. Once company starts showing consistent performance , market can rerate any stock with much higher PE than its contemporaries. Once you assume higher PE for this business, current stock price looks undervalued… So its in the eye of the beholder.

2 Likes

Have been wondering on valuations too, few questions that may help are

-

Can growth continue beyond med term +, we all know 4X type from FY 21 to FY25, I.e. 2025. Given solar ambitions, longevity and push in industry there is no reason to believe another 2-3X from base of FY25 to FY 30 journey. This dramatically changes terminal value and that too with solid demand visibility. It’s a different thing as to how Borosil secures market share to deliver on that growth with quality of margins, which at this point till next year or so a monopoly.

-

My take( and many be wrong here) is that as long as demand visibility builds ON with passing of time and margins are in acceptable range, valuations will stay elevated being forward looking ( and volatile based on news flow) ,given protection of ADD coninues, a quarter by quarter view will be key to watch trend of margins

4X by FY 25 is BTW 40% CAGR and probably devent growth thereafter too, and even at normalized 30% margins - valuations are not out of whack IMO,- given an evolving nature. But needs a close watch on margins and supply side dynamics.

Invested

1 Like

If in FY22 they do Rs142crs profits why would profits only double when capacity is going up 4x?

1 Like

My take on revenues & valuations

Doubling capacity which will get commercialised by Q2 FY’23

So, Q2 FY’ 23 revenues should be 320 crore

35% EBITDA margin – 110 crore

Likely case for FY’ 23

Annual revenue run rate – 1400 crore

EBITDA Margin 35% - 500crores

Depreciation : 140 crores

Interest: 30 crores

PBT: 330 crores

Tax:25%

PAT : 250 crore

Likely case for FY’ 24

Annual revenues : 2100 crores

EBITDA Margin 30% - 630 crores

Depreciation : 160 crores

Interest: 60 crores

PBT: 410 crores

Tax:25%

PAT : 310 crores

By end of FY 25

Annual revenues– 2800 crores

EBITDA Margin 30% - 840crores

Depreciation : 225 crores

Interest: 65 crores

PBT: 550 crores

Tax:25%

PAT : 410 crore

Current MCAP : 9000 crores

Available at 22 times FY’25 earnings.

As per COP 26 target by 2030, the total installed capacity from renewable sources should be 500 GW out of which 300 GW should be from solar. India’s current installed capacity from solar stands at 46 GW. This means another 25 GW per year just from solar. The runway for growth is huge and hence market may assign a higher terminal value for Borosil Renewables.

Discl: Invested.

9 Likes

Does the latest import ban from US on imports from Chinese province (Xinxiang, heard they deal with solar components too) anyway help this company?

Not really. Supply constraints are already there. Maybe the only way it helps BR and others is that they can think of further capex given that the potential TAM may have increased.

1 Like

Came across this video on You tube…launched on independence day… well made

4 Likes

2 Likes

Above video 9:45 timestamp onwards on being asked finance plans for expansion

- Expect significant operations efficiency once new capacities come online in July 22.

- 200 cr term loan for current ongoing expnasion( he said 650 Ton, though most releases said 550 ton).

- Expecting significant cashflows from Q2 23 ONWARDS hence difficult to say next leg finance plans now.

Reading between lines - At 450 ton, recent Qtr realization basis EBDITA is approx 60 cr, at 1000 ton, number goes up to 130 cr-140 Cr, higher with operating leverage called out by Mr Khureka. They can pump out a good cash flow of 450-500cr on annualized basis(80%), cost of next round of expansion if similar to current would be 600 cr( same would be 900 cr for greenfield for any new competitors), could be entirely funded by internal accruals of 1.5 years, maybe small debt.

Very smart capital allocation and thinking on spacing out each expansion round by 1-1.5 years.

Invested

2 Likes

As per the deep dive above, i noticed he mentioned about 60% rise in Soda ash prices and significant rise in power & Freight costs in last quarter. Are they able to pass on this spike in expense to end customer? Also did anyone track the spike in solar glass price during the quarter?

Yes exactly he has clearly mentioned that rising RM cost will negatively impact the margins and current margins will not be sustainable going forward. I expect q3 results will be poor vs h1 while RM cost absorption continues.

1 Like

Awesome thread by Mohit Jangir https://twitter.com/investor_mohit/status/1484174582236184578?s=21

6 Likes

Brillian thread… All bases covered and explained so amazingly

1 Like

Have a question about repeat revenue for Borosil Renewables.

Since solar cell/module life is said to be around 20-25 years, is repeat revenue potential for Borosil in the range of 5% only?

What happens when India reaches its 300 GW solar installation capacity by say 2030? Growth after that is likely to be less steep, so Borosil reneables revenue growth rates also moderate accordingly?

Intent of the questions is to try to understand what kind of terminal valuation a solar glass manufacturer can command.

3 Likes

Wondering how Borosil was able to passon higher input cost even achieved higher realisation… Is it a function of Better brand/ strong distribution?

Or anything else which is not repeatable every time?

If former is true then amazing result.

Also I assume lot of operating levers are at play as well.

1 Like

On last concall, Mr. Kheruka mentioned that he had long term contract for soda ash till Dec end so main commodity impact will be seen in this quarter. Also he mentioned on CNBC interview few minutes back that due to increased ocean freight cost, landed cost of imported solar glass has gone up which helped Borosil to increase prices in domestic market, thereby reducing impact of higher energy cost

1 Like

But, isn’t it that soda ash prices have considerably cooled off from November onwards?