Hi Power tariff for solar is already going down day by day. I think the latest is Rs 2/- Do you have any idea about the BER for solar power producing companies. If things are not going to be rosy, it can pull down the demand. I am trying to link the last mile data to glass. Can you pl guide

Concall Transcription: https://www.bseindia.com/xml-data/corpfiling/AttachLive/19a4ccc5-40e1-4c19-888a-a74c52ff513a.pdf

At least one bottom line is clear at cursory glance: Demand will be on the rise for foreseeable future, and BR is sure they will be able to sell all their inventory even if other competitors come in.

I guess we are looking at competition from Adani and Asahi.

1 Like

Haven’t followed the industry news lately… Has Adani ventured into solar glass production?

According to BR’s concall, most likely next year.

According to the management,

this new capacity (i think ~500TPD) will be in Mundra, is a collaboration between Asahi India and Visaka Industries (associate co. of Adani) and will be operational sometime Q1 next year. This will be largely used for Adani’s captive consumption and fraction of it will be sold in the open market. However, the demand of solar glass is so huge - not only within India, but also from EU - that Borosil will have no problem selling its glass and that there is place for other players to enter the market.

There is also a chance that RIL, who has plans to setup 10GW module capacity, might also backward integrate to make its own solar glass, as it will be profitable for them given the volume they need.

2 Likes

Board meeting on 25th August to consider fund raise

4 Likes

From the ESG Report:

The company is looking to get into glass for high performance greenhouses and building integrated photovoltaics. Both are emerging sectors.

Link to ESG Report: http://borosilrenewables.com/pdf/ESG/BRL%20ESG%20Report%202021.pdf

11 Likes

Some interesting snippets from ESG report shared by @Tar above

This provides peek into margin expansion possibility, albeit small % to start with.

7 Likes

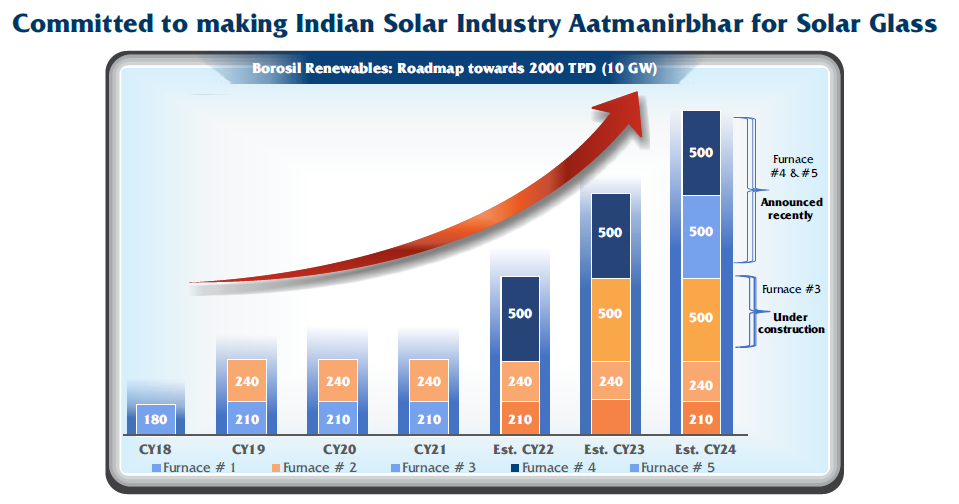

Capacity addition snapshot from annual report 2020-21

Interestingly on page 42, company talks about rights issue of Rs 100 Crores for SG4/5 funding.

12 Likes

4 Likes

3 Likes

Unable to read it, Paid article, could you explain in brief how this rate hike cause any changes to the proposed plan(announced by GOI) to add new solar capacity & how would it impact the margins of Borosil Renewables?

1 Like

EPC (engineering, procurement, construction) firms will bear the worst brunt of this decision.

It will also affect upcoming Projects

Except this not much explained

1 Like

Will impact Boro Renew very indirectly. If the margins of EPC firms get squeezed, they’ll tighten the screws on all vendors. But given the monopoly and supply constraint situation for solar glass, I guess Boro Renew would be low in the pecking order of EPC firms.

Will also raise tariff costs for solar plants though not by much. Cheap financing makes everything possible.

1 Like

Monopoly not anymore

1 Like

This plant’s production will be mostly be used for the internal consumption of Adani.

While Asahi has a minority stake, the majority stakeholder Vishakha Group’s Co. -

“Vishakha Renewables” is into some partnership with Adani Solar.

Found this on LinkedIn-

From TradeIndia Portal-

So Borosil Renewables will still maintain its Monopoly .

1 Like

In the previous con-call Borosil management confirmed this and also said that it is not a matter of concern for them. The solar pie is very big and they are not still catering to the whole market, so they won’t be losing market share per se, just gain with time.

3 Likes

“At present, domestic manufacturers lack orders and are running below optimal capacity. And, customers (project developers) were eagerly waiting for expiry of SGD to place orders from foreign players at a cheaper rate. This will make sustenance for local manufacturers extremely difficult as they will be left with almost nil orders to continue production,” said the executive quoted above.

Imports of solar modules with pre-fit glass will be rampant till March 2022. Borosil is likely to see reduction in margins till the end of this FY. Only hope is significant increase in exports by Borosil.

[Expiry of safeguard duty: Boon for solar developers, bane for manufacturers | Business Standard News]

5 Likes

Was curious to understand China’s current power shortage situations and impact for solar glass industry- Given it has high power consumption requirements

http://taiyangnews.info/business/xinyi-solars-h12021-revenues-grow-over-74-yoy/

Per above article for Xinyi glass

Major customers for the company’s solar glass products during H1/2021 were in China – revenues for this segment comprised 68.1% business from Mainland China, while 31.9% came from rest of the world. Its Guangxi production site is now catering to customers from Southeast Asia and India.

Power situations in Guangxi region

NEAR TERM EFFECT- Although not called out explicitly, solar glass production will see curbs in China in line with other industries.This may also mean that new capacities aggression will have to pause.

Possible mid term implications- as China recovers from power curb issues post winters( beyond next 2 quarters), by that time there will be policy push backed backlog for higher local renewable targets in China, thus CY 22 in one possible scenario- most of Chinese output will be focused on local solar glass supply backlog fulfillment. Knowing that Chinese capacities will eventually come online at some point, a serious capacities expansion is ruled out either in other geographies beside small ones like BR in India.

Summary - BR will likely have a relatively smoother run over next 1-2 years and overall demand will stay ahead of supply, thus a sustainable financial performance continues and get more predictable. Highly optimistic case would be strong exports as well. Yes there is Adani venture coming online as well by end of 22, need to see capacities outside captive consumption.

Market being smart, will sense it much ahead.

Above is a possibility and I can be wrong here, Q2 commentary key monitorable.

Invested

9 Likes