already borosil has 2 mm thin glass

I think the fundamentals are strong. The story is good for atleast 2 years.

Disclosure: Invested

(39) DHANDHA: BOROSIL RENEWABLES - YouTube

The interview is from feb 21 so a bit old but still found it very useful to judge the promoter’s prospects.

They explained each aspect of the industry and related industries.

Another older one is Borosil Renewables Says Capacity Running “Flat Out”, Margins Could Improve (bloombergquint.com)

He said that the chinese giants operate in the EBITDA margin space of around 50%, which is why they have been able to relentlessly plough money back into the business. Similar levels of margins can be achieved.

1 Like

Hi will Reliance investment of 75,000CR into clean energy have any impact on BOR-RENEW? On CNBC when they were discussing Latha mentioned it would address the entire supply chain from Raw Silica to batteries. Any idea if reliance might enter the Solar glass game? If\ not could these investments and the increase of domestic solar module manufacturing further benefit BOR-RENEW?

4 Likes

I think Boro Renewables will be a good future bet as even if Rel Inds does 100 Giga all inhs out of the 300 Giga target of the GOI the game is still big.

1 Like

FII/FPI and institutional investors have further decreased their share holding in June 21 quarter. Does anybody has any views on it?

1 Like

This is the reason why even after BR’s 4x increase in capacity, the supply wouldn’t be enough to meet the demand.

100s of solar module manufacturers, only one solar glass manufacturer.

10 Likes

The question really is that what makes Borosil the preferred partner for domestic module manufacturers and how does the equation change in case ADD is removed?

1 Like

Why would domestic module manufacturers prefer Borosil Renewables?

- Thinks from a perspective of s module manufacturer. If you are a module manufacturer what are the main reasons you would prefer any glass manufacturer?

Mainly two things (keeping quality of glass is standard across companies)

- Price: whoever gives you for less price you will select them.

- Availability: How soon you can get the glass panels required for your work. You may be compromise little on price if glass is urgent. But again not much.

Now come to Borosil. On price regard, we know that BR is price takers rather than price makers. So whatever the price Chinese guys set, BR just follows that. Management also spoke about this many times. So price side not much difference for you to select whether it’s BR or Chinese import. You are fine with either of them.

Now availability part, If you are importing it takes time to get the product delivered. Here BR can be a preferred glass manufacturer. They can deliver much earlier than import companies.

Most important part, glass demand is greater than supply. As long as that stays like that, no worries for BR. For me it looks like even if BR’s new plants are operational, still demand will be higher for at least next few years.

@luckbychance please read the thread. All of this information, and more, is there - views and counterviews.

1 Like

Chinese companies did flush out most of the glass manufactures. BR was not the first company to make solar glass. There were American, European and Turkish companies. However BR was on among top 5 or 6 companies. Chinese came to the flat glass manufacturing in 2011. BR started in 2010. Then the Chinese dropped the price so dramatically and all other guys went out of business. However BR survived it. This is a good video to watch if you haven’t seen DHANDHA: BOROSIL RENEWABLES - YouTube

1 Like

There is a very simple answer to why local manufacturers prefer domestic solar glass over imported.

-

Domestic solar glass is available on 60 Days credit facility. For imported solar glass you have to pay upfront in advance and receive shipment only after 30 days of order placement. This effectively blocks 60 days of working capital.

-

Do not have to pay shipping fee on imports. This is minor advantage when shipping isn’t in turmoil. For the last 6 months it is though, so expect even this quarter BR to run on 100% utilisation capacity.

Chinese do not have some heavenly advantage with them. They are only able to cut down prices because a) cheap electricity available b) scale.

BR is achieving scale and thus able to compete better. Achieving scale is the only way to compete in this industry.

Electricity costs can become competitive by a) using other forms of energy like gas, renewables etc (BR has a captive solar plant) b) duties to help

The moment you start looking at this sector as strategic and a energy sector, the thought process will become much clearer.

India wants to be a world leader in renewables and domestic manufacturing is priority. As solar panel manufacturing increases in India, BR will keep benefitting.

90% of the global renewables markets is controlled by China, the democratic world doesn’t like that. Imagine if 90% of world’s oil supply was controlled by a communist nation. Wars have been fought for much less. The next rational option to establish renewables manufacturing is India. Google recent news and you will see global giants ready to invest billions of dollars to set up solar wafer and module manufacturing in India. How many of these companies from democratic nations have set up shop in China? Zero.

This can be a cyclical industry too eventually (Post 2035) but for now it’s a structural mega trend.

The last such mega trend was the oil boom and steel boom when both those commodities started witnessing wide adoption. The companies of those era were darlings of the market and bigger than any giant. US Steel, Chevron, BP etc.

Also, a request to members to please read the thread before asking same questions again. You’re not adding any value and cluttering the thread. There are both believers and skeptics on this thread and both sides have repeatedly laid out their points in detail. Thanks.

24 Likes

Guys, the idea wasn’t to circumvent what has already been posted. I did read up prior posts to a fair degree but couldn’t find the answers (maybe brainfade moment!) but on that note, if the original topic could perhaps be edited by mods with a FAQ, it would help a new investor who’s just started tracking.

Secondly, thanks for all the moments. China+1 makes sense now in this space especially from a geopolitical pov.

1 Like

I reached out to a friend who’s an expert on PV module manufacturing, and currently works in a foreign EPC company. I wanted to understand the role solar glass plays, and how much of a commodity it is.

Sharing my notes from the conversation.

Is the kind of glass important in a PV module?

Quality glass is definitely important in module manufacturing. I’m not a solar glass expert, but I can tell you the basics:

- You want a glass that doesn’t reflect the light away from a module, allows a lot of light through, and is durable.

- Light varies quite a lot in a day. You want to test the module profiles across varying light conditions, especially during diffused sunlight and low light conditions, and the glass plays a part in this. (EPC providers will usually deal with all control variables like angle on the roof, direction, etc.)

- Your module should last twenty years or more. While there is some basic cleaning that’s needed, poor quality glass will be spotty / cloudy over time.

- Coating on top of this is important and varies by application.

What do you think of glass manufacturers and the industry?

So the question you have to ask is in the supply chain of module manufacturers, where do they cut costs?

- You know poly silicon price is rising, the real effects of this rise in poly silicon prices is felt by EPC companies, as they have razor thin margins.

It’s not obvious that in cutting costs, glass is the first to go, because there are various things to think about first as a module supplier.

-

Panels have different peaks/power, you get them in 200W, 300W, 400W and so on. So if I were supplying modules and say the customer needs 3000W of energy, I would try to see if I can cut costs by changing how many of each I make: 5x400W + 5x200W versus 2x600W + 4x400W + 1x200W for example. Maybe I’d optimise my supply chain for the period as a whole by thinking how many of each to produce, before thinking about cutting other costs. It varies from company to company.

-

Remember glass has to be cut in different shapes and sizes, so this works into the optimization I just told you about.

-

With solar power goals, the person that makes the commodity will make the most money. Read about Jinko, or Ambani’s ambition to buy out REC (Norway). These are your panel manufacturers, and glass too falls into this category. These are the primary beneficiaries, not the EPC companies.

-

Markets are highly concentrated globally - most panels come from China. If you want a residential PV module for your roof, you contact your EPC company. We design the roof, purchase from China, buy the inverters and necessary supplements and put them together.

-

EPC companies will have the lowest margins in the industry. If panel prices go up, these are the companies that will suffer. Procurement costs increase, sales get affected as customers already have to pay a lot up front. A successful EPC company is one that is an economy of scale; you make money on volumes. It is a completely cut-throat market.

Questions from @Tar:

What kind of advancements are being made in PV/Solar glass, will technology transition into main markets?

- So for PV developments, we’re already there. Just like the Carnot’s thermodynamic limit to mechanical efficiency, there is a theoretical limit on efficiency from a solar PV cell. It’s called the Shockley Queisser Limit. I’ve worked with people on this, and we’re fractions away, maybe some 0.04% or something like that. So incremental gains going forward will be of a similar small order of ~0.01% efficiency.

- In terms of climate change, we’ve reached the efficiency we need to in order to make a difference. The goal is just to roll it out as fast as possible.

- Developments in solar glass is outside my area of expertise, sorry.

What do you think of the Antimony free glass made by Borosil?

- I know antimony has some use in the manufacture of solar glass, but I think this product has more to do with the environment, as antimony may cause problems with disposal.

If anyone has other questions, please let me know. He’s kindly agreed to read through Borosil’s technical specifications.

Disclosure: invested.

25 Likes

Just a observation…

as and when solar energy picks up…may be 20yrs + ? there will also be a need to dispose them safely.

Govts will then need to come up with regulations for safe disposal of antimony glass or mandate use of antimony-free glass.

…something similar which has happened in asbestos, CFC etc !

2 Likes

5 Likes

One may want to attend

1 Like

Asahi India Glass and Vishakha Group announces partnership and investment for setting up 500 TPD Solar Glass manufacturing plant at Mundra.

2 Likes

-

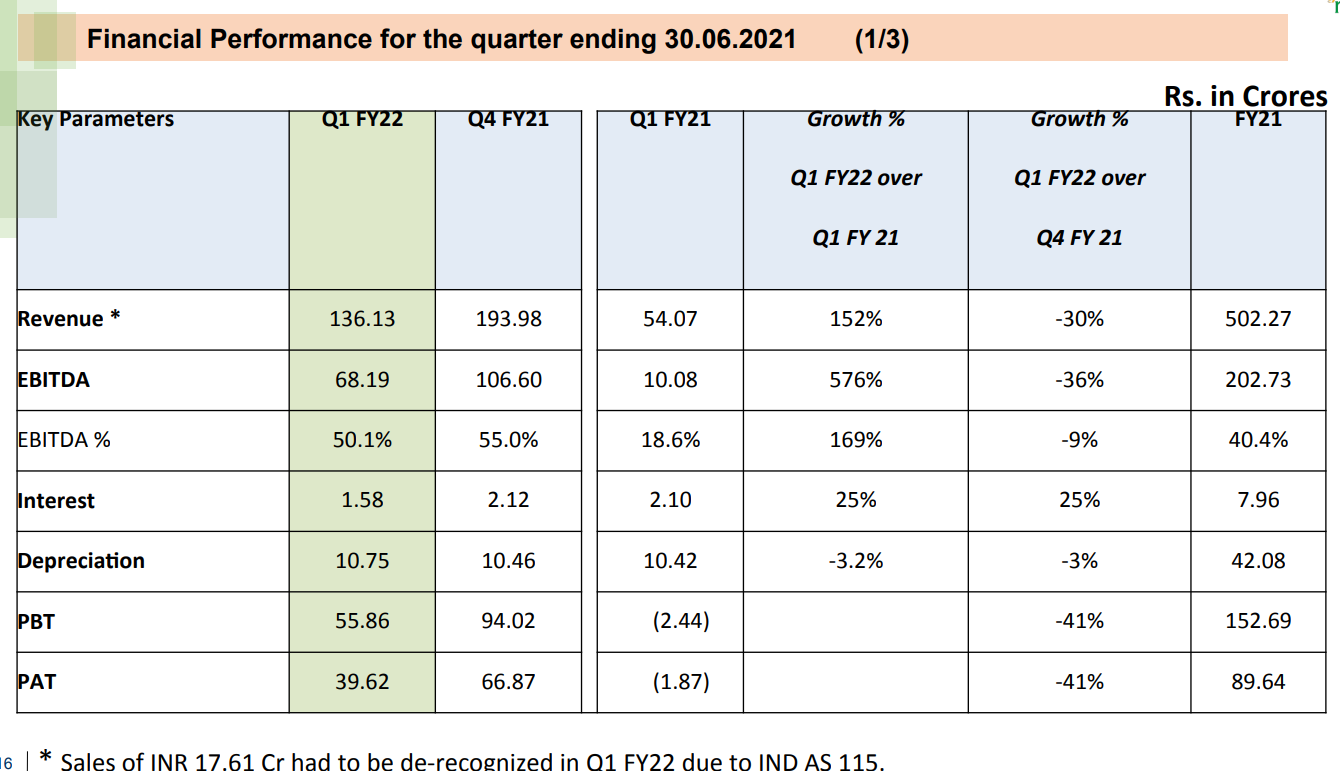

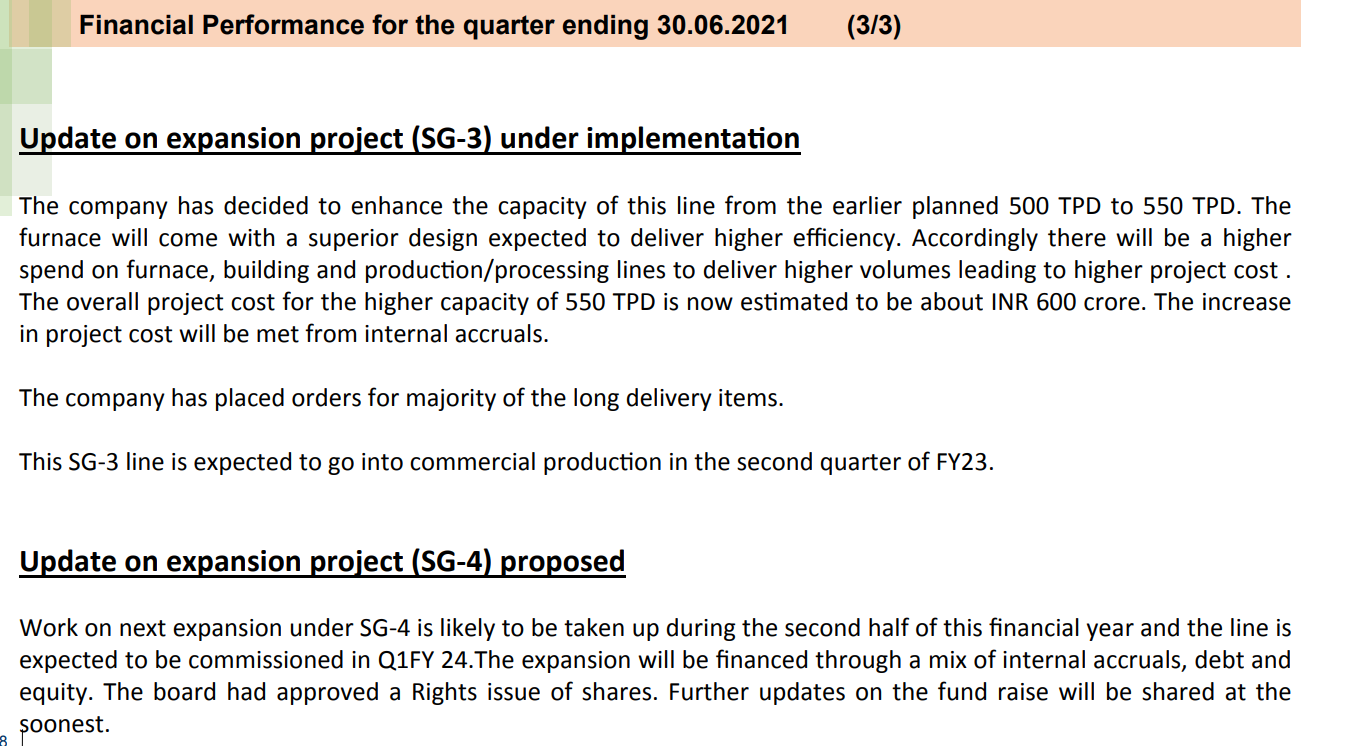

3rd Furnace capacity plan increase from 500 to 550 TPD - revised Capex to 600 cr from 518 cr - diff to be funded by internal accruals

-

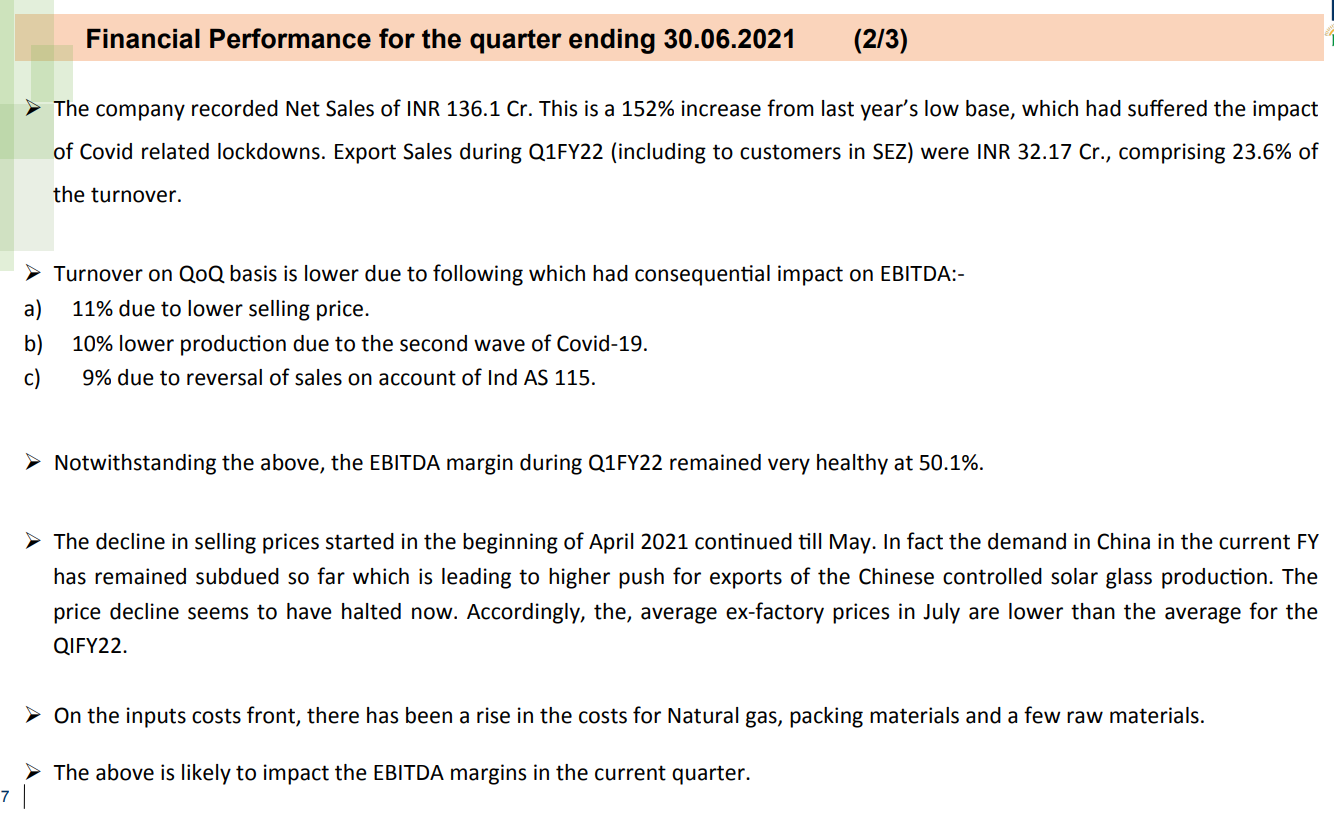

Quarterly performance is reassuring on sustainability of industry and numbers ( which is further supported by competetion setting up plants ) - Good performance inspite of challenging Qtr

-

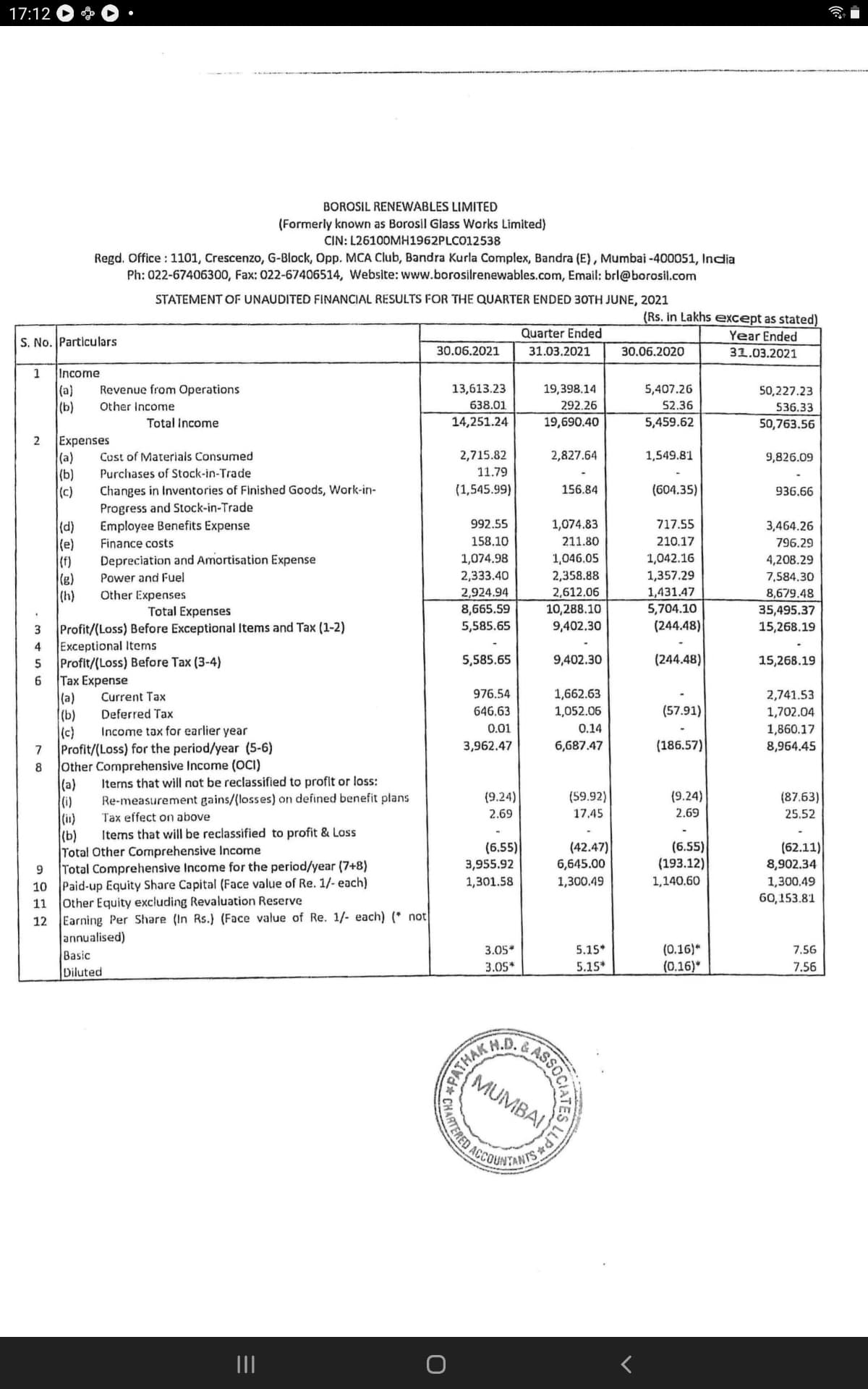

Q1 FY 22 142 cr revenue and 56 cr PBT

-

Q4 FY 21 197 cr revenue and 94 cr PBT

-

Q3 FY 21 140 cr revenue and 41 cr PBT

Can Sustainable Op margin probably settle between Q3 21 and Q1 22 op margin numbers, more to hear on concall

Invested

6 Likes