Has any update been provided on the running of plants this quarter? Due to Oxygen being diverted for medical usage and local lockdowns im guessing Q1Fy22 will not see full utilization?

DISC- invested

Has any update been provided on the running of plants this quarter? Due to Oxygen being diverted for medical usage and local lockdowns im guessing Q1Fy22 will not see full utilization?

DISC- invested

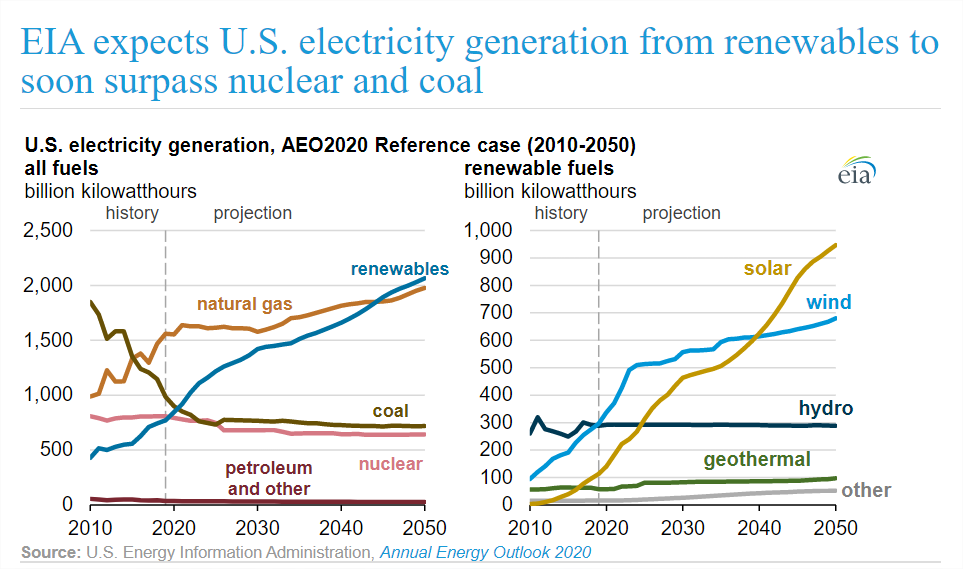

This is in support to previous comment about US plan for renewable energy mainly solar

I am working in power sector for the last 20 years and when i said about delays in projects, it was to signal not on margin but for sales target. With respect to margin it is based on the current prices of glass for modules which the developers are procuring. you may please check on the ground with solar module manufacturers. The post was meant to just signal only for few quarters and not on any structural demand change.

Along with outstanding financial results for the quarter, company has made few announcements which I feel are worth reflecting on -

Change of auditors - About few months back, this issue was raised on social media as well as on our forum. The issue was their current auditor M/s. Pathak HD & Associates is also auditor of many firms with not so good reputation. Hence many investors, including myself, had written to the company requesting them to change the auditor at the earliest to avoid credibility risk due to wrong association. This announcement shows company listens to the investor community and ready to mend their ways ( Their reorg plan was also driven by investor feedback)

Rights Issue - This is welcome step from the company as it shows they are willing to share the growth and wealth with their existing shareholders. Rights issue is an equitable way of diluting equity (or else they could have done QIP like last time or preference shares or underpriced warrants to raise their own stake etc)

Issuing shares under ESOP plan 2017 to 4 key employees of the company and its pricing - 1,28,000 shares are issued to 4 key employees with 10% discount to market price and will be vested over period of 5 years. (33% each at the end year 1 and so on). This clearly indicates that management is aware of possibility of poaching by competition and hence trying their best to retain the talent. This is addition of earlier announcement of 2 years salary + education expenses till graduation for the children, in case any Covid related employee fatality. Current quarter increase in employee expenses confirms this.

Aggressive expansion plans unveiled even before earlier expansion plan yet to come to fruition. This coming from extremely conservative promoters shows their confidence in the future growth for the sector.

If you step back and see all these actions and their timings, you will see a very thought through coordinated approach where the company is getting ready to play in the big league for the long run. The current plans would help the company to grow in solar glass till 2025 beyond which I expect (pure hunch) them to diversify into related business in solar sector as a first step and maybe beyond in other renewables. Company name defines their long term ambition , which otherwise they could have easily named as Borosil Solar glass or Borosil Solar etc etc

Disclosure - invested for last 4 years (and would like to keep it at least for next few years) and forms part of my core portfolio. This is not a buy /sell recommendation and I am not SEBI advisor. Please do your due diligence before taking decision.

Credit to you for your earlier thesis on the thread which got a lot of us interested and invested in this story!

The current results are great, and the story seem to be playing out, all looks fantastic!

But just to act as the devils advocate, let me present 2 contrarian points to the thesis as questions

But in cyclical businesses something always happens because of which the cycle peaks and the market knows it much before time. Could we be in the upper end of the solar glass price cycle globally as of now?

My view is still positive on Boro Renew as an investment but just to understand what your thoughts might be around 2 contrarian viewpoints that I have against a high performing business.

Discl : Invested

It’ll be great if someone can help me with the amount of Capex required for new capacity addition. Like what’s the amount per 500TPD capacity addition? I seem to have read it somewhere but unable to recall.

Capex for ongoing 500 TPD (SG - 3) capacity addition - 500 Cr

Capex for further 1000 TPD (SG - 4 & 5) capacity addition - Apprx. 1100 Cr (10% capex increased compared to prev due to increase in steel and other metal prices)

As above mentioned capacity expansion are brownfield and any capacity expansion after that will be mostly greenfield so capex for that will be on higher side.

Thank you so much for this info.

Anyone attended today’s conference call?

Any links to view a recording of the same?

@Tar you can use the following youtube link for concall recording

The International Energy Agency (IEA) has raised its forecast for the global growth of wind and solar by another 25% compared to figures it published just six months ago.

Explaining its new forecasts, the IEA points to a number of changes over the past year, as well as areas where its earlier expectations have proved too pessimistic.

The biggest changes in this year’s forecast are for China, the IEA notes, where more projects are going ahead without government subsidies than expected. The update says:

“The pipeline of solar PV and wind plant projects accepting provincial electricity prices without additional subsidies has increased since last year, resulting in a more optimistic forecast.”

The IEA has, therefore, increased its forecast for growth in China by 45%, boosting total additions in 2021 and 2022 from around 150GW to around 230GW, as shown in the chart below.

The Future of Renewable Energy by Arvind Kothari, Founder of Niveshaay:

@Malkd @sahil_vi @hitesh2710 @ayushmit @basumallick Would love to have your guys’ opinion on this.

What I like about Borosil Renewable is that it has got a huge huge tailwind. With the current 500-tonne per day solar panel glass capacity( 2.5 GW per annum), It can just meet 22% of Indian domestic demand and this demand is increasing year by year. Indian Govt wants to have 30 GW per annum domestic capacity(around 12x of current Borosil capacity).

So, any capacity addition is most probably going to be consumed instantly.

But what I don’t like about this business is huge Capex of 500 crores is required every time we need to increase the capacity by 500 ton. It’s not like those businesses where small Capex is enough to multiply capacity.

So the problem is not sales, but capex required to scale. The current 500 crores ongoing capex will be live after the 1st quarter of FY 22-23. If the company starts the upcoming 1000 crore capex from Sep 2022, It would finish by March 2023.

Can anyone help to quantify the approximate return we would be able to make in the next 5 years if we buy at the current price assuming No rerating happens?

@pankaj_xxxx Here’s my attempt at it.

Based on latest concall, realizations in apr-may have come down to 115 /sqmm. this is between 3rd (106) and 4th qtr (155) fy21 realizations. Management indicated that current realizations are more or less sustainable due to duty from malaysian imports and thus higher than the 3rd qtr numbers. Assuming the sustainable revenues to be 74% of q4 revenue based on above, i calculated a sustainable NOPAT of 133cr annually, going ahead with current capacity of 450 TPD running at same production efficiency.

Now, the 4x capex will come alive in 3 years. For simplicity, lets ignore operating leverage and assume this NOPAT also becomes 4x, i.e. 532cr annually after 3 years. Assuming 15% cost of capital, we get sustainable earnings power value of 532/15% = ~3500cr, which is close to current market cap. Hence, my view is that the 4x expansion growth is baked in the current market cap and growth after that is available for free.

Feel free to suggest improvements.

Disclaimer: invested. Please don’t assume a recommendation or buy advice based on above calculation. It is only meant for academic purposes

In a low interest environment where FDs are giving 5% returns using 15% cost of capital is trying to be super duper conservative.

equity is still risky i guess, esp. with small caps, and since BRL is not levered much, its mostly cost of equity

For an individual the risk free rate is FD interest of a safe bank like HDFC, SBI, ICICI etc.

You need to add a risk premium rm-rf and the use a beta to calculate cost of equity.

For you equity might seem risky, for someone else it might not seem that risky. Hence they might come up with a potential fair value of 7000crs also.

I think Operating profit will be 60Cr per Q with 115/- rate, 240Cr annualized.

Do you see company getting any PLI benefit? which will add another 6% margin.

Yes, operating profit will be ~240cr annually. For understanding sustainable and distributable earnings, I preferred NOPAT = EBIT(1-t) and included depreciation as expense to proxy replacement capex (capex reqd. annually to restore ops). Since company is going through growth, its difficult to segregate growth capex from replacement capex. In fy21 cash flow, net capex was ~20cr, even if we assume this is replacement capex and not growth capex, this number can go higher due to commodity inflation. Therefore, on the conservative side I used ~40cr annual replacement capex (same as depreciation) and deducted it from op profit to arrive at EBIT.

No idea on PLI front

Extract from update by Sterling & Wilson on 16-May-21.

The global Solar EPC industry has been impacted with several module manufacturers refusing to

honour past price contracts given the sharp increase in cost of modules. Some of the Company’s

module manufactures have also reneged on honouring their contractual commitments and have sought to substantially increase their module prices in two projects;

Continued increase in commodity prices and freight costs remaining at their all time high.