This is another reason why India is pushing for domestic manufacturing. The moment someone starts looking at solar sector from the prism of energy independence, everything starts making sense.

Solar is the new oil. India was never able to become energy independent as long as oil was the chief energy fuel in the world. With solar this is changing. The only way we can get rid of huge oil import bills is by becoming independent in producing our own energy via solar. At 750 GW of solar energy capacity in India, it’s just a matter of time and execution for us to achieve that independence and get rid of huge oil import bills.

No country in the world can succeed without becoming energy independent first.

When such a huge once in a lifetime shift happens, companies participating in that shift tend to benefit one way or another.

If anyone wants to learn more about the future of solar and what’s possible, study some rich European countries and how they are now producing so much energy just by renewables that they export it. Oil in these economies is just non existent, only used for a few industrial purpose. Germany is a prime example, exports 11% of their electricity.

Investing in solar is like investing in Standard oil during the Roosevelt era. Oil was then mostly used for kerosene, very few imagined oil to dominate the energy sector for the coming century.

1.Polysilicon price flat wow - Mono-grade poly prices were flat wow at Rmb137.0/kg this week

2.Wafer price up wow - Mono wafer prices were up 1.0-6.6% wow to Rmb3.90-6.33/pc this week.

3.Cell prices up wow, module prices flat wow - Mono cell prices were up 2.2-2.3% wow to Rmb0.88-0.94/W this week. Mono module prices were flat wow at Rmb1.60-1.69/W this week.

4. Solar glass prices flat wow - The market prices of 3.2mm and 2.0mm solar glass were flat wow at Rmb28.0/m2 and Rmb22.0/m2 respectively this week.

On one hand, this news shows tremendous potential for solar glass in India and more solar glass production in India (if cost effective) will reduce dependence on chinese solar glass. Also healthy local competition will keep Borosil on its toes, which is not bad. Also no profitable sector can remain local monopoly so this was expected. On the other hand, once established it takes away monopoly status of Borosil which can be treated as long term negative.

But it will take around 2.5 years for any greenfield expansion of this size, to establish its credibility in the market. It would be interesting to see Borosil’s response as I expect them to accelerate their plans to capture bigger market share before local competition comes in.

Gold Plus Glass used to a be dealer of Borosil Glass. They have ramped up well in float glass. The solar venture is greenfield so they will not be as cost competitive as Borosil.

Today Borosil has 35% market share of India solar glass, 65% is China. With duties, basic custom duties on modules and cells and ADD and CVD on solar glass, China share will come down. So even if 1 or 2 other guys join the fray, there is enough room to grow for Borosil.

We have lost 4 employees to this dreadful pandemic. Their names are Santosh Chalke, Vijay Shirsath, Tushar Panchal and Shiv Shankar Bisht. The sadness for these losses is indescribable.

In order to reassure our employees, we have announced that the family of any employee of Borosil Ltd. and Borosil Renewable Ltd. and their subsidiaries will be given 2 years of salary in the event of an unfortunate demise owing to Covid 19. In addition to this, the education of the children of the employee will be paid till graduation in India.

The above is no comparison to the scale of the loss, but hopefully will allow the family enough time to process the bereavement and reorient.

I strongly believe that the real assets of Borosil are not reflected on our Balance Sheet at all. We need to protect these assets in whatever way we can. I hope this move is a step in that direction.

This too shall pass and we will emerge into a better tomorrow!

From Sreevar Kheruka MD @Borosil.

Looks like very ethical and employee conscious management. Please flag If inappropriate.

I do not understand why you thought this message is inappropriate! In fact, how the promoter and senior management of a company generally behave (crisis or no-crisis) is extremely important to long term sustainability of the company. So this kind of “inside news” is very much appreciated to gauge what is actually happening in a company and how promoters are behaving and spending money. Watch out for promoters who spend lavishly on fancy bungalows, yachts, private jets, islands etc…

Now coming to Borosil, the gesture of MD is highly commendable and praiseworthy. Such an action engenders employee loyalty. May the company prosper!

Actually, on the contrary, I would take this news with a large dose of salt. Any management which tom-toms their employee sensitivity in a pandemic puts a question mark in my mind of their actual credibility. A lot of companies are taking employee-friendly actions but their MDs are not going out on social media to blow their own trumpet.

I found the reasoning a little too harsh or pessimistic. They might be trying to send a message to their employees and investors that they “care”, and there is nothing evil about sharing that

As an employee (not with borosil), I would say it will help to set benchmark for others to follow. I do not think they are doing it on BSE/NSE, then it will be PR. But on a professional network is a great thing. I would be happy to work in an org which thinks for employees like this, not many do. Maybe Tata, and they are a great employer.

Besides I know few companies who are doings lots for corporate offices and are not really concerned about front line staff/ feet on the ground. Who will face the max impact.

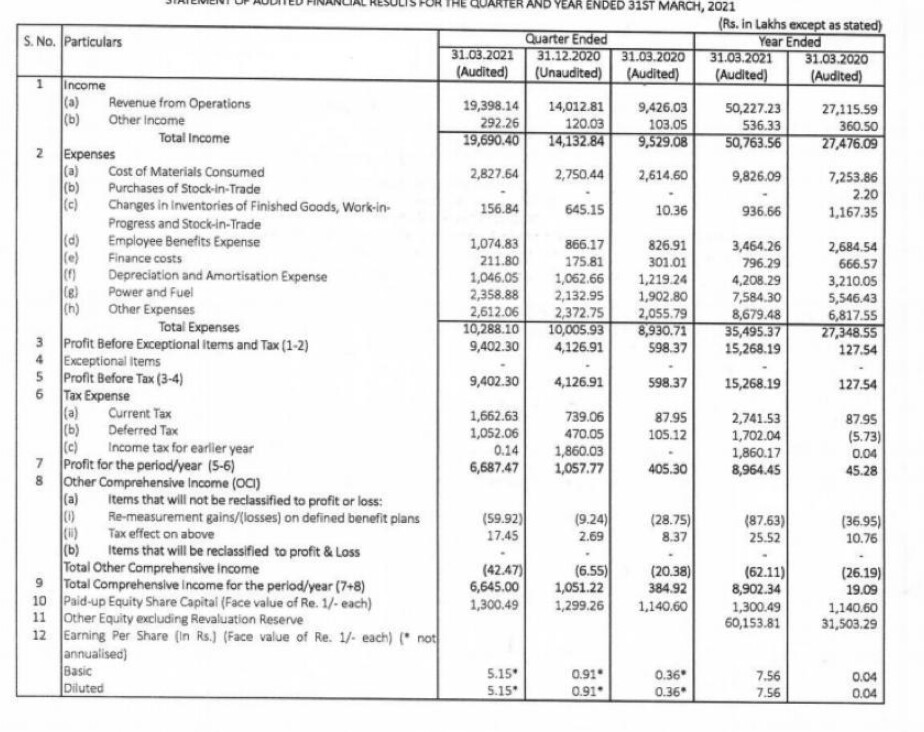

Results released, summarizing all developments below.

All comparisons are QoQ instead of YoY as production related tailwinds have kicked in only since Q3 when import duties kicked in.

Income from Operations grew by ~40% since previous quarter (Q3 140cr vs Q4 193cr)

Total Expenses for QoQ grew by just ~2.8% (Q3 100cr vs Q4 102cr)

This is how operating leverage functions, same plant, 100% utilization, stable prices, earnings increase multi fold

The increase in expense was mostly due to increase in Employee Benefit Expense which increase by over 24%. This may be due to their Covid related compensations etc., which is really impeccable that company is doing that.

Everything else under expenses, were minor increases.

Q4 EBITDA of the company stands at 104cr vs 51.89cr for previous quarter, so EBITDA increased by over 100% QoQ

Q4 EBIT of the company stands at 94cr vs 41.3cr for the previous quarter, an increase of 127%

EPS for the Year stands at 7.56 vs 0.04 for the previous year, I won’t even bother listing how much % increase that is. Expect Quarterly EPS of around 6 to 7 Rs for each quarter going forward until a) new capacity kicks in b) new rights / shares get issued which may lead to a minor dilution

From the Balance Sheet

Few things I like to monitor from the Balance Sheet are

Receivables : This has jumped slightly on a YoY basis, 72.5cr for FY21 compared to 40.6cr for FY20. Can be attributed to increased sales.

Borrowings : Total debt for FY21 now stands at 61.43cr compared to 83.5cr. A reduction of about 26% . Everything else on the liabilities side also shows a reduction apart from a minor increase in Trade Payables.

Provisions have almost doubles from 89 Lakhs in FY20 to 1.65cr in FY21, still miniscule compared to sales and profit of the company.

From the Cash Flow Statement

CFO increase by over 515% !! FY 21 CFO is 161.03cr compared to FY20 at 26.2cr

FCF also doubled from 57.03 Lakhs in FY20 to 1.36cr in FY21. As expected most of the CFO is being routed towards CAPEX and increasing capacities.

Other Developments Announced

No Dividend : Expected, they need to reinvest as much as they can. This made me happy as this shows management value money and are prudent allocators of cash. They could have given a dividend to please everyone and raised more debt or diluted more equity, but they instead decided to be prudent and reinvest back into the business.

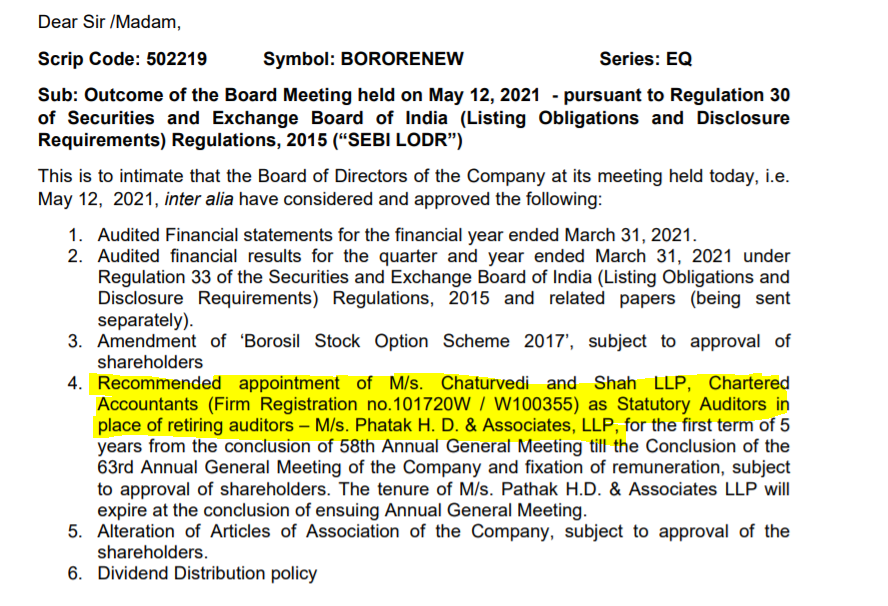

Auditors of the company are finally changed from the current Phatak H. D. & Associates, LLP to Chaturvedi and Shah LLP. The new auditors are well respected. Hopefully this will quash any ‘bad auditors’ accusations on the company.

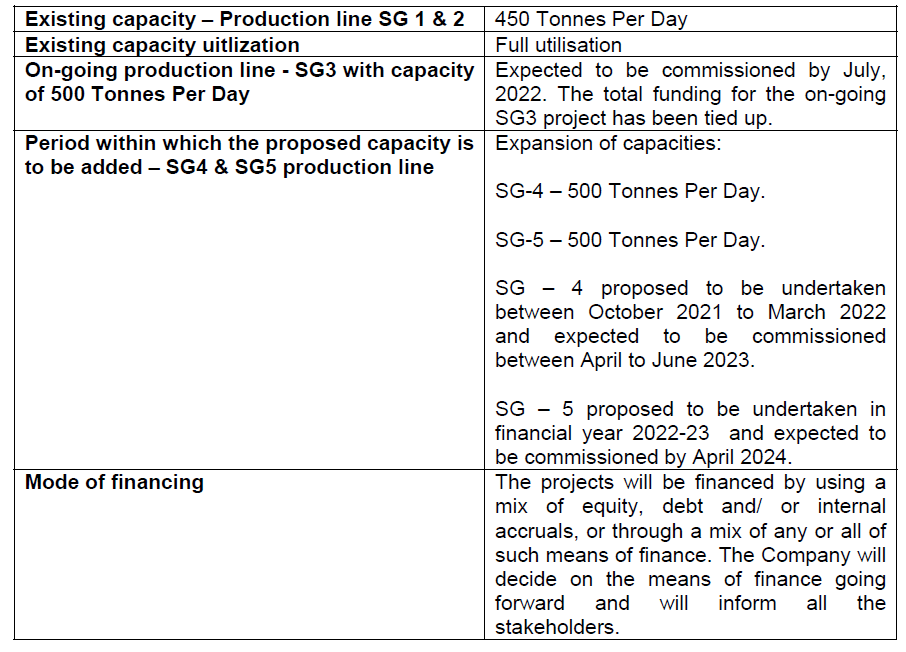

The company will be issuing 100cr as a rights issue to finance the new 500 TPD capacity addition they made a couple of weeks back.

Also, I wish to share this with folks following this company.

If you haven’t already, start reading Renewable Energy Market Update Reports by International Energy Association. I came across them last year when researching into renewable sector as a theme for investing. They are just pure gold filled with amazing insights that make you wonder how in the world is this report free.

The Agency publishes it mostly cause they want to fast track renewables deployment and help with climate change but you can get a ton of free amazing insights into what is happening around the world when it comes to renewables.

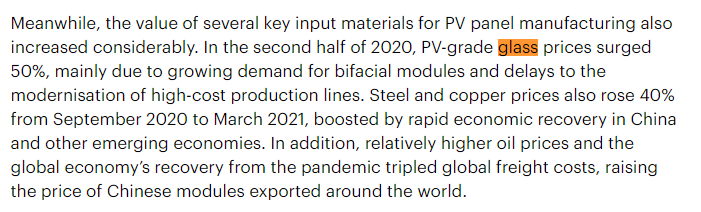

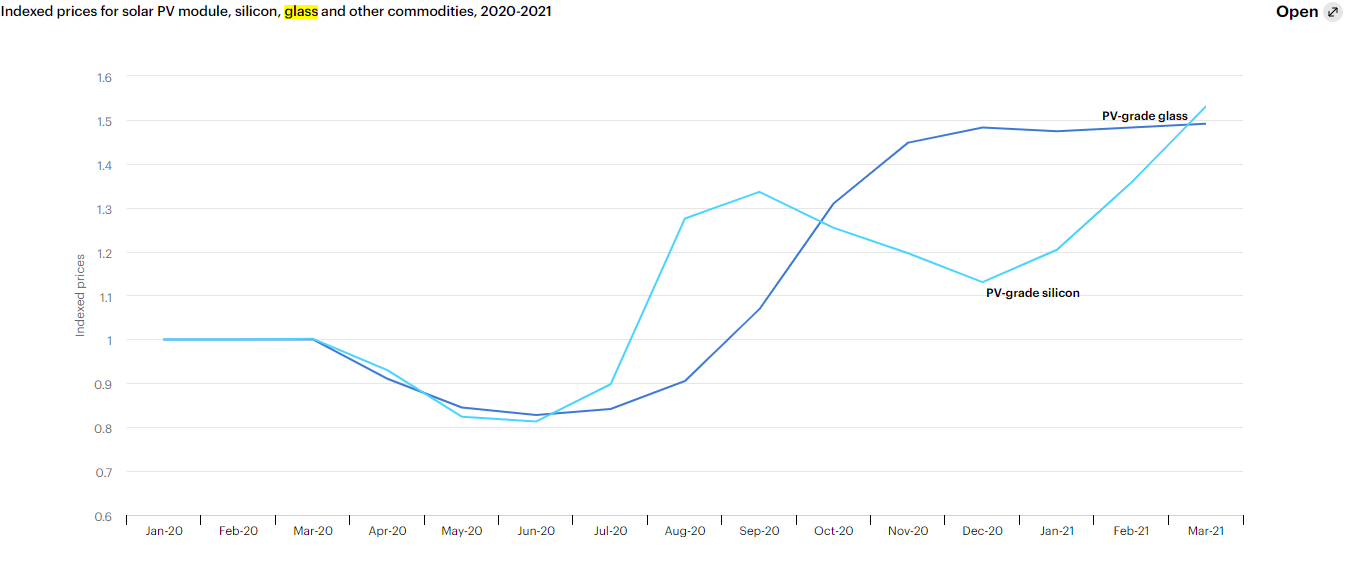

For example, I knew this quarter was going to be extraordinary for Borosil Renewable as the report told me that solar glass prices have pretty much remained stable throughout last few months after increasing. Here is an extract from the report below.

The report further mentions that glass prices may come down a teeny tiny bit or will remain stable from here on as suppliers across the world have scaled up production. We are essentially in a race of existing suppliers, whoever scales up will keep winning. This explains why BR announced back to back capacity increases.

Why are suppliers scaling up?

Because of a huge demand from Europe and Latin America.

There are many other great insights in the report, I plan to do a post here on Value Pickr just on these trends and the entire renewable sector as a theme, hopefully sometime this weekend. Will add more details there.

PS: I know this post has nothing to do with Borosil Renewables, but just wanted to share with everyone here. Reports and data like these helps one become a better investor. I personally follow data driven investing and for me to invest in something I need to find data (outside of financial reports) that can guide me and help build conviction.

Right are first issued to existing shareholders at a premium. This helps in less equity dilution. So 100cr right issue should ideally come to existing shareholders for a first right of refusal. In case existing shareholders refuse to subscribe, it will open up in secondary market for anyone to buy.

Shareholders can buy ‘rights’ to lock in a price of a share. For example, you can buy a ‘right’ to buy BR’s share at some future date at price X. For that right you need to pay some premium today which maybe Rs Y. Rights like options have an expiry date on them and need to be exercise on or before the expiry date.

The company is yet to announce all details related to rights issue.

The Board at the moment has only ‘approved’ the route of raising cash via rights issue. The actual rights issue will be decided by CFO and his team and filed with SEBI once done.

They are mainly going via rights issue as they do not want to dilute existing equity share further.

BR results are way above expectations with almost 53% OPM margin and the Q4 itself has achieved an EPS of 5 which is quite phenomenal. This kind of margin surely would be difficult going forward as the prices of Solar glass has come down plus due to lock down many Solar power projects is delayed and that will have an impact in the Q1 quarter sales figures.

You seem to have missed the detailed report shared a couple of posts above. The idea that glass prices will come down cause projects are delayed or duties are removed are without any base. If you read the report, you will understand the scale of PV plant deployment globally. China itself has so much demand that even when the Govt has removed subsidies, there is no change in the rate of increase in solar projects.

Further you have new demand coming up from Europe and Latin America this year. Next year US is getting ready with its renewable infra plan as part of the larger infra plan being championed by Biden.

I am just highlighting this because, many here make this assumption without really any substantiating data. Without data backing your theory, its just a theory, and in this case without any ground for the theory to stand on.

The same point has been debated several times since last Q result. If you understand the scale, you will stop guessing the demand.

The bottom line is even with plant delays and price increases, there is more demand than ever. I will even go to the length of stating I will be surprised if BR runs its plants at less than 100% utilization for any Qs for the next several years.