But its unique in a way that it is a commodity having single producer in India. None of the other commodities have that luxury. Also its different as its demand in India is going to grow by 25%+ CAGR for next few years. Hence one can call it a “super commodity”.

I am willing to bet on this “super commodity” with the inherent downside risk possibility. (which stock doesn’t have this )

I would say import duty,execution history and management is the key differential here. Without the import duty it will be tough for the company to compete with Chinese competitors

Discl: Not invested in either. Not yet able to build a conviction on borosil

My two cents.

Don’t think Copper and Solar glass can be compared. Some differences and similarities listed below.

End usage industry maturity: Copper is used in matured industrial as well as domestic uses. Building construction, wires & cables, machinery, transportation etc. We all know these are fairly matured industries growing at more or less in-line with GDP growth rate. Solar glass on the other hand is just used in solar panels which is a fairly early stage industry if we assume that future energy requirements won’t be fulfilled by fossil fuels anymore. According to projections, solar energy might already have a major share of our energy requirement in the next 10 years.

Measure of demand growth: Copper usage worldwide has increased by just 36% over the past decade (see screenshot attached). That’s a CAGR of ~3% p.a. I don’t think next 10 years will be any different in terms of growth. While on solar glass, I read somewhere that solar energy will increase by 20%+ CAGR by 2026 (https://www.google.co.in/amp/s/www.alliedmarketresearch.com/solar-energy-market/amp). That somewhat implies demand growth we can witness in solar glass.

Technology: Copper production technology is pretty much the same since long time, no particular producer manufactures superior quality copper. While solar glass technology is evolving. Borosil specifically mentions that it’s solar glass is of superior quality (antimony free etc.)

Ps: feel solar industry has long long way to go in the coming decade… heavily invested so views are bound to be biased.

Hi kushal, thanks for adding your views. This is going to be my last post on the topic because busting other people’s bubbles is not really much of a value add exercise imo.

Have you explored why the price of copper is through the roof recently? If not, please do. This is due to the demand for copper being used in EV. The primary driver of copper prices is due to shortage of copper compared to demand due to the new age technology which is EV. sounds similar to how the solar glass prices shot up recently?

If history was a perfect predictor of the future then historians would be the richest. Also you’re comparing the history of copper to the future of solar glass which is not the correct comparison. Copper demand is also through the roof and expected to be so for years because increasing copper production is difficult and demand for EV will only increase exponentially (does that sound similar to the story for solar glass?) with many

auto companies publically stating their desire to only sell EVs by 2030.

3.

This is like saying that Domino’s makes wheat thin crust pizzas. The question is : who’s eating it? They also make solar glass out of eggshells. But who is buying that? All of these are good for parlour tricks but their primary product is borosilicate glass which has import substitution risk from Vietnam, china, and other places that Chinese companies might manufacture out of. Only way one might make money is by hoping the government views solar glass as strategic and hence provides some r

Protection against dumping. Basing an investment thesis on hopes tied to whims and fancies of the Indian government is not something I am able to digest that easily. Of course some investors can probably do that better. I say all the best to them.

Most importantly if you go back and view the context, the question was of whether there are any lone producers of a commodity in india and to that my answer was yes there is: hindustan copper.

Another way in which these companies are very similar is the valuations which are out of whack. Borosil renewables is at 7.5x sales and hindustan copper at 10x sales. These are very high and unsustainable valuations. Even if by some chance operating margins might sustain to 25% in future (I doubt that because even the much larger industry leader has 15% operating margins after eating subsidies from Chinese government) the valuations themselves would kill the investment. Valuations could easily derate to 2x sales even if sales increase 4x with end result being loss of capital.

Disc: studied in some depth and decided not to invest.

Completely agreed. Topline is vanity bottomline is sanity and cash in the bank is reality. Would suggest checking out sterling wilson. Although this isn’t a great company either but many things going for it compared to borosil:

One of largest in world. Able to compete and win deals in Australia mena usa and of course in india.

Unit economics is beautiful. Asset light business. 50cr fixed asset base and 5000 cr sales and negative working capital. Talk about asset turns.

Some risks wrt the promoter group paying back ICD but imo this is going in right direction and expected to be resolved In 4/5 months.

Mouth watering valuations

Clear revenue and growth visibility

The thing about being asset light is that they throw out cash. It’s a cash guzzling machine .

Margins are a little volatile but the beautiful thing about having asset turns of 100 is that 100 times 1 is 100. (even 1% EBIT margins are great).

You may be right about Borosil Renewables. Only time will tell. But I am not in agreement with you that Sterling & Wilson is superior investing opportunity than BR. Its a project based company where lot of things can go wrong.

I am a researcher in areas allied with PV/ indirectly related to PV solar cell materials. Cutting-edge tech is evolving rapidly: double-perovskites, tandem cells, etc pushing the S-Q limit. Even though Indian research is late to the party, it is there. As far as this product is concerned, it is to solar panels as tempered glass screen protector is to our smartphone (important today, obsolete soon). As it happens, the developed world is moving away from flat-glass and actually towards transparent or near-transparent solar panels/cells, which means a variety of semiconducting materials to replace silicon. Silicon has its issues- single crystals are the ones providing respectable efficiency but extremely expensive and time-consuming to synthesise, which is why all practical solar panels use polycrystalline silicon which has abysmal efficiency. The tech to make high purity silicon wafers exists in few places globally and no, do not expect any single-crystal silicon miracle from Coal India!

Even solar concentrators and conical dishes are preferable to flat-glass panels!

I have personally experienced the intermediate gasoline-electric hybrid vehicle stage in the US, unlike in India where we are trying to make the leap from diesel-powered vehicles to solar/fossil-powered EVs! A similar analogy applies to this product, where I feel transparent solar cells, gallium arsenide, cadmium telluride, quantum dots, thin films, silicon-substitutes will be the way ahead, in which case this technology will be obsolete and it might very well occur sooner than expected.

Transparent solar cells might still use glass- but in a totally different manner. Here, glass (better alternatives exist) would be the substrate and that would require finer synthesis techniques as well as additional surface treatment steps to make for suitable substrates and I am skeptical about whether this company can successfully pivot towards that- for eg, ITo/FTO-coated glass substrates.

Another point- antimony-free glass is not an achievement to harp on; would you accept Asian Paints marketing their products USP as “lead-free paint”?

I would consider making my money work on disruptive tech/ cutting-edge research and innovation in mundane quotidian sectors like FMCG, etc. But I would not do the same on a business that makes mundane/ non-critical/ non-innovative/ non-strategic products in a continuously evolving sector with cutting-edge research and competitive tech which would work against it.

Disclosure- my opinion can turn out to be correct/incorrect and only meant to provide a different viewpoint, not buy/sell advice on this stock.

Hi @sahil_vi, I absolutely respect the takeaways in the above post and have liked your analysis else where on VP. I’ve not been very informed on what’s happening in metals space at all, hence have little to no idea about things you mentioned for copper, but definitely an interesting argument to make on copper. Also I agree to the point that there’s a commodity angle to the business as it’s ultimately a demand supply game primarily governed by what’s happening in China (and now US to an extent). But here I would like to point towards two important assumptions which you explained in your above post.

Margins: You need to see their margins before ADD came into existence and before solar prices shot up. They were already making 25% EBITDA margins (after their capacity expansion). I feel even after 5 years they can hover around these levels ± 5% depending on solar prices with atleast 4x sales.

Price to sales: Flat glass and Xinyi glass trade at 6.2x/5.6x price to sales (as per Bloomberg). I actually feel Borosil’s 7.5x valuation is very attractive (if not mouth watering) given we might see an almost 4x capacity expansion in 2 years. Anyways valuations are a function of expectations about the future of the sector. If solar future deteriorates even 2x price to sales cannot sustain.

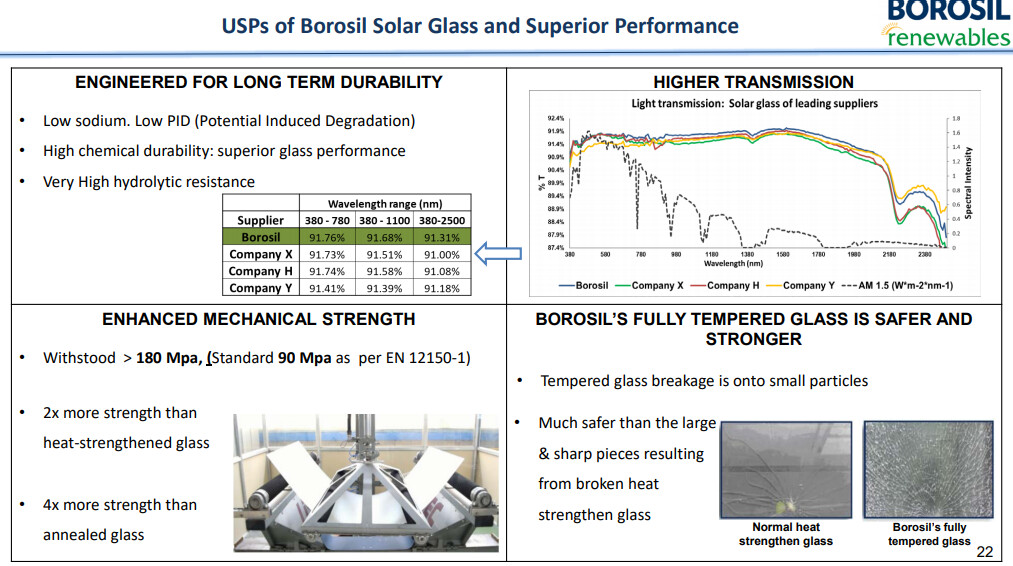

Ultimately, superior glass quality can help you deliver better unit economics. Attached below screenshot from their investor presentation. I am sure if you’re a solar park developer in India, you’d definitely like to bake in savings related to usage of a superior glass quality into your models and compare present value of those savings with the additional cost you’re paying today.

PS: I understand it ultimately boils down to one’s conviction, comfort level with the sector and govt. policies around it amongst other things. My conviction on Borosil is based primarily on the fact that solar is now one of the lowest cost ways of electricity production.

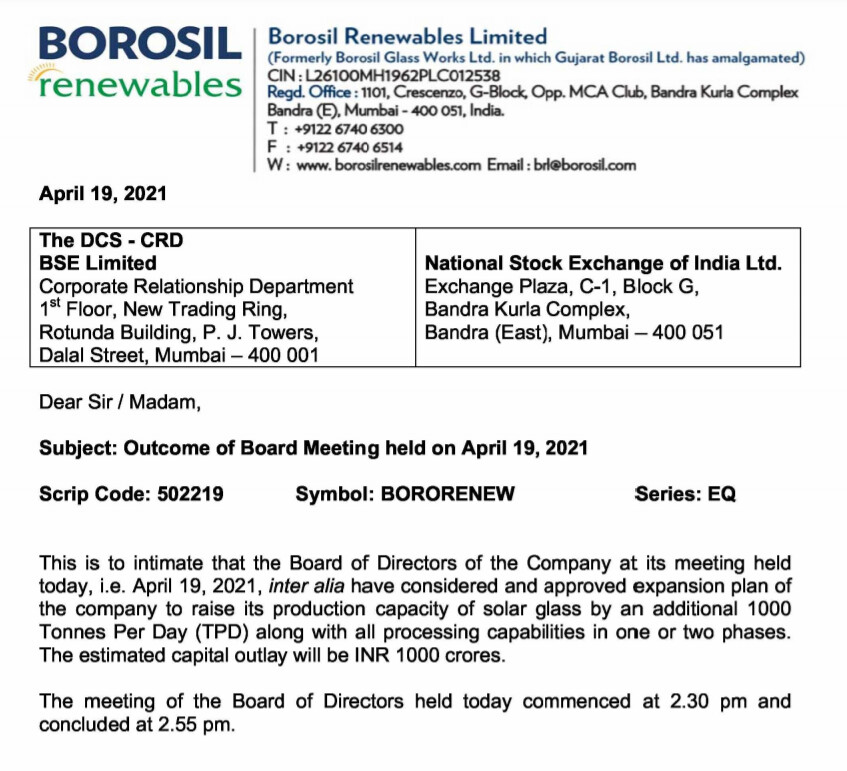

Formal announcement by the Board for increased capacity announced. 1000cr capex will be done either in one or two phases. No disclosure on how the 1000cr will be funded.

Hi, thanks for writing this eye opening comment for layman like us. I wanted to pick your brain on how soon you think solar glass can become obsolete - 5 years, 15 years, 50 years? Just want to be sure it is not one of those far fetched and debatable “AI will render humans jobless” sort of predictions. Also, can you please elaborate on why you think BRL is not equipped to pivot towards the new technology, ITo/FTO-coated glass substrates etc.?

Thanks again.

Solar cell technology may take a different shape, but all the capacity they put up for glass will not go waste. It can be used for many other applications. PLI scheme (hope it comes through) and initial higher margin should be good enough for recovering cost + RoCE in time.

Non-silicon panels such as cadmium telluride or gallium selenide based ones still use same solar glass. They are categorized as thin film based panels. Though they are cheaper, they are less efficient

The transparent solar glass panel as pioneered by the Michigan state university is still in its infancy. Efficiency achieved by this panel is at 5% in comparison to 15-20% from traditional panels

Well, agree on short term causes lots of pain, especially for those who expect those orders to come through for their projects and timelines, But in medium to long-term isn’t this good news for domestic manufacturers?

Additionally, shouldn’t this have a reputation cost for those suppliers, not just in India but globally?

)

)