There are two close Large Players where we can take inspiration : Xinyi Solar Holdings Limited and Flat Glass

If we look at Xinyi, the stock currently trades at 10 times Price to Sales and at 25 times PE.

If we look at Borosil, the TTM Revenue Stands close to 400 Cr which with the new capacity coming should increase inspite of drop in prices

So how should I value this company , with Margins looking to be in upwards of 20%+ can we value the company at 4 - 5 times Sales as I can see 30% Sales growth easily… My rationale, is that BR being the only Indian company in this space and a lead time of 2 years to setup new capacity & with ADD. I am inclined towards valuing on P/S but happy to understand alternate viewpoints

I have read through the postings on BR and have been going through their data.

Recently i came to know that they have hired Pathak HD audit firms that are supposed to have audited firms like Rel power and satyam. Looks like the auditors are known for fudging and stuff.

I am invested and am not sure how to take this news.

Sorry, I have no views on the auditors. Name any auditor in the world, including the Big 4, and I will show you the scams they were involved in.

The best way to stay on top of all this is to learn a few simple forensic accounting techniques. With the help of any screener you can easily catch companies that are a) aggressively showing profit without any cash flow b) taking money out of the company

Few examples are, low cash flow conversion to profit without any or limited Capex, management salary as a % of sales. If you google forensic accounting screeners you will even find a few ready made formulas to apply.

Further, no company in the world is safe from audit risk. The likes of Enron and Wirecard were darlings of their respective markets and comparable to Reliances of India. An auditor can only do so much if management itself doesn’t have good intentions.

@Marathondreams can give you more views as he has been following the company for far longer than I have.

Depends on your outlook and investment horizon. Valuing a company for 1 year investment horizon vs 10 year investment horizon are two different things.

To give you some context, India just crossed 40 GW in solar electricity capacity. Our target is 175 GW by 2022 and 450 GW by 2030.

So we are only done with about ~9% of our journey. This should help you value the company and sector and the target market.

Actually I was very very gung ho on this company. I did not panic sell. And I am definitely adding for the long term 2 years for now and with confidence more as I get to know the company.

Saw news on their expansion plans to 10gw and India’s power needs. Above all I have used their pdts and know how good they are… We know them for their glass but I bought their oven and boy!, It was best in class at a good price to boot.

Plus mgmt looked very very genuine and not the type to go into blind expansion on debt nor did they rush to dilute equity. Plus I see excellent govt support now. Thanks to China.

Above everything else their persistence in the face of all the odds btwn 2010 till 2018.

But still don’t want to be caught unawaress and wanted the long term investors opinion.

I was thinking of PWC and KPMG and all that they were involved in too. Thanks a ton Tar… That info you shared helped.

I have raised the issue with company by email. Although I did not receive any response from them, I am sure they will consider it at the right time if more investors provide feedback to them (including institutional ones). Company promoters are open and transparent (within business constraints). Whole restructuring exercise ( between Gujarat Borosil and Borosil Glass) was done by the company based on investor feedback to eliminate any cross holdings /related party transactions and provide clear options to its investors to either own solar glass business or consumer/scientific glass business.

So ideally I would love to see big known auditor for the company (as it will add more credibility to their numbers), I am ok with their current auditors as for me, promoters integrity matters more than their auditors.

I have been attending their concalls for last 2+ years , mostly as a passive investor. I did ask few specific questions in the past ,which were not asked by others.

Isnt this issue of ‘not having a big auditor’ a trivial one ?

especially when historically we know that the so called big auditors have never been able to catch the bluff of promoters and many times have been caught napping while the promoters continued to lie all the way ?

During recent TV interview the management spoke about the possibility of doubling capacity immediately again. However we needed 500CR for the Brownfield capacity expansion at the moment, would the additional 500tonne expansion be a brownfield or greenfield expansion? And if it is greenfield then what would the required capex be?

1. What are the data points around sustainable prices that we can expect from this industry in light of global supplies ramping up.

Ans - Past is a good place to look at trends - per below article it has hovered between 23 -26 rmb/m2 over last few years - not very far from current. It would be rational to assume these as base case scenario for global prices( for BR some premium given ADD and DCR support)- with renewable as Megatrend , all the reasons to be optimistic going ahead. Remember they export close to 20% as well.

2. How would BR play in light of price/ realization as well as global supplies going up.

Ans - As a sensible mgmt team, let’s see how they behaved - Conservative capacity expansion till 200 ton, once they had confidence about their own capabilities and Industry tailwind they announced 250 ton brownfield ( live by mid 22) - this was Q3 20 when glass prices shot up, media lime light, QIP and what not…

Now that in Q1 22 glass prices have softened from spikes and cautiousness prevails - they are hinting another 500 ton expansion possibilities by sept- of course with backdrop of Duty and DCR visibility. All signs of visibility and sustainability.

Is there a reason to think otherwise when bet on BR is practically bet on mgmt. ( they are the industry itself for India as of now and with wild price movement of glass and China capacity addition - don’t see anyone rushing to set it up in India yet, even if it happens - that will further validate industry viability and will take few years)

3. What are fair valuations and growth run rate?

Ans - very subjective for each but with some base price for glass as in #1, Q3 and Q2 results available, Q4 numbers and commentary to be out soon, We have a reasonable base set. India ambitions on renewables and govt policies support is quite visible to all. BR capacities be twice by mid 22( done deal) and possibly 4 times by early 23 (likely) - mkt is forward looking and further rerating will happen much sooner - as story unfolds.

My bets are with them as of now, of course technicals are there to keep any eye on which seems to be indicating a base building for 12+ weeks.

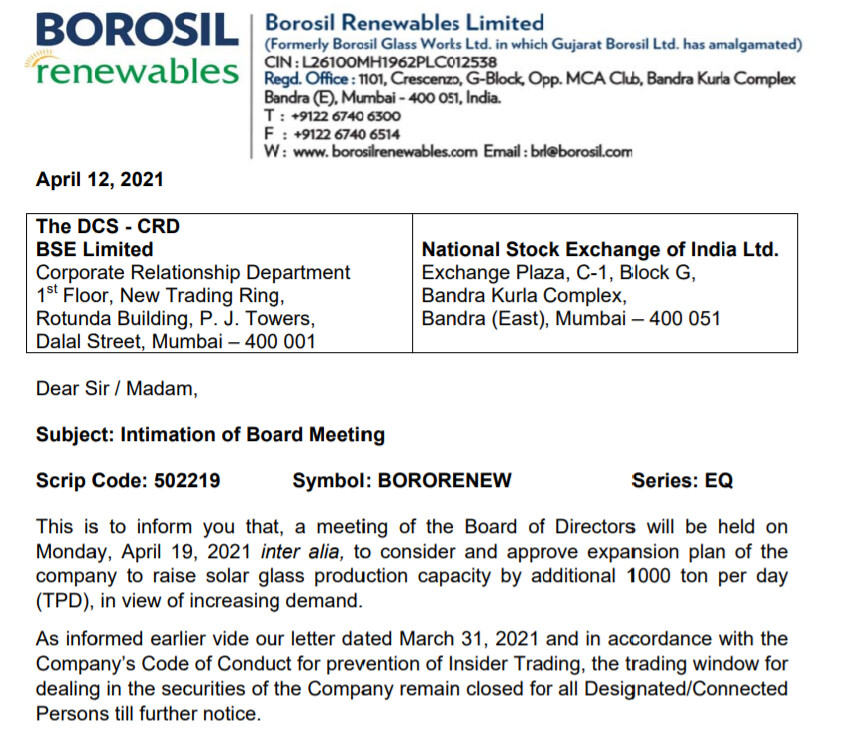

Translation

Board is meeting on April 19,2021 to approve another capacity expansion of 1000 TPD.

Post this BR will become the third largest and the largest non China based solar glass producer in the world.

The question I have regarding this expansion is where the funds will come from? For the last expansion they did QIP + internal accruals. Would be interesting to see where they decide to fund this expansion from.

When conservative management like Borosil starts thinking big, its time to take notice. Its never happened in 50+ years of the history of this group. Good thing is that they are sticking to the knitting and trying to up the game by bringing in economies of scale aggressively. This also creates challenge to any potential domestic competition.

About funding, I am sure it would have substantial equity portion (as the outlay could be around 1000 Cr) which can be funded either by rights issue or by getting either big bulge PE player or any big solar player like Adani as financial investor.

Company is getting ready to enter in the big league and it augurs well for long term investors considering huge growing global demand for solar power and push for localization by Indian govt.

If you have not studied the stock it is not correct to give any advice or suggestions on any stock.

This is the forum only where one can give suggestions based on their own study.

Please avoid any baseless suggestions without studying properly.

A few thoughts from interviews and what they shared in the last AR

They are very risk averse and careful in expansion. China’s top 2 glass company caters to 90% of the global solar glass market. Even with the 950 capacity BR will be the 3rd largest player in the world in a funny way. Their market share though will be very low.

They have kind of pioneered the bifacial glass 2mm and Antimony glass. Their biggest customers are from India. Margins though are from exports but that market is going to take a while to develop and cost pressures and competition with china will be high.

There is always the risk of Chinese players offering the same products at a lower price. Patents take a long time and I am not sure if it can be effective.

Their biggest support should come from the GOI and from Athmanirbhar Bharath and with that the govts implicit guaranty that they will get the Indian market share and they expect the price of solar power to go up by say 10 paise and that will result in a bigger margins for the manufacturers locally.

The concern would be how the debt would be structured and what would be the equity dilution.

The second one will be competition. I read an article on Vedanta getting into fabrication glass or some sorts in a very large scale… wonder if they can eventually enter into solar glass. That sort of thing would be a threat.

Also these expansions take anywhere between 15 to 18 months. Wonder how they will be phasing the expansions.

Disclosure: I am invested.

Edit:. If company is going into expansion I have a strong feeling they have a big push from the govt. They did mention in one of the concall that govt has promised them in duty support as needed.

Just to give an example in last decade or so many companies tried to establish solar glass including reliance but no one could withstand the rough weather except this company.

By your own admission solar glass is a commodity

a difficult to produce commodity, but a commodity

If one really wants to play the commodity cycle, there might be much more favorable risk reward equations available. A commodity producer quoting at 5-6 times sales is a risky proposition imo. SAIL or IFGL or one of the second rung cement producers might be a much better risk reward proposition rather than a commodity producer quoting at 5x sales. Commodity Prices can often surprise on the downside, specially when buying the company at high valuations.