Recent concall trasncript

2 Likes

I completely agree with your point. The market has gone into a euphoria when it comes to companies in the solar domain. I booked 50% of my holding after Mr. Kheruka said that they expect the demand-supply shortage to last till Q1FY22. The Chinese have been restarting their old capacities and have been tremendously increasing their capacities. However, I would wait till the US announces their solar plans as the company mentioned, since that would give some clarity regarding the glass prices for the medium term (2-4 years). The EBITDA margins without the increement in the glass price is pretty high for this business. If the prices stabilise even 15% above the usual rate of 96-98, I feel the margins would be excellent in the long term. Coming to the duty, I feel the rate is pretty less. Unless, the capacity of solar glass production increases by 3x and new players come in (doesn’t matter if it’s just one new player), I don’t think the government would have any motive to increase the duty since it would hamper their solar ambitions.

Things would be much clear in the next two quarters I believe. The management has always been transparent about all the developments so we can take a call based on their outlook.

2 Likes

2 Likes

One correction in this video

He says copper is not a beneficiary from renewable energy and it is only for EV.

I wish to correct here that the wind turbines and generator require copper.

Hindustan Copper is the beneficiary.

1 Like

This should allay fears regarding margins if it does indeed turn out to be true

Disc: Invested

2 Likes

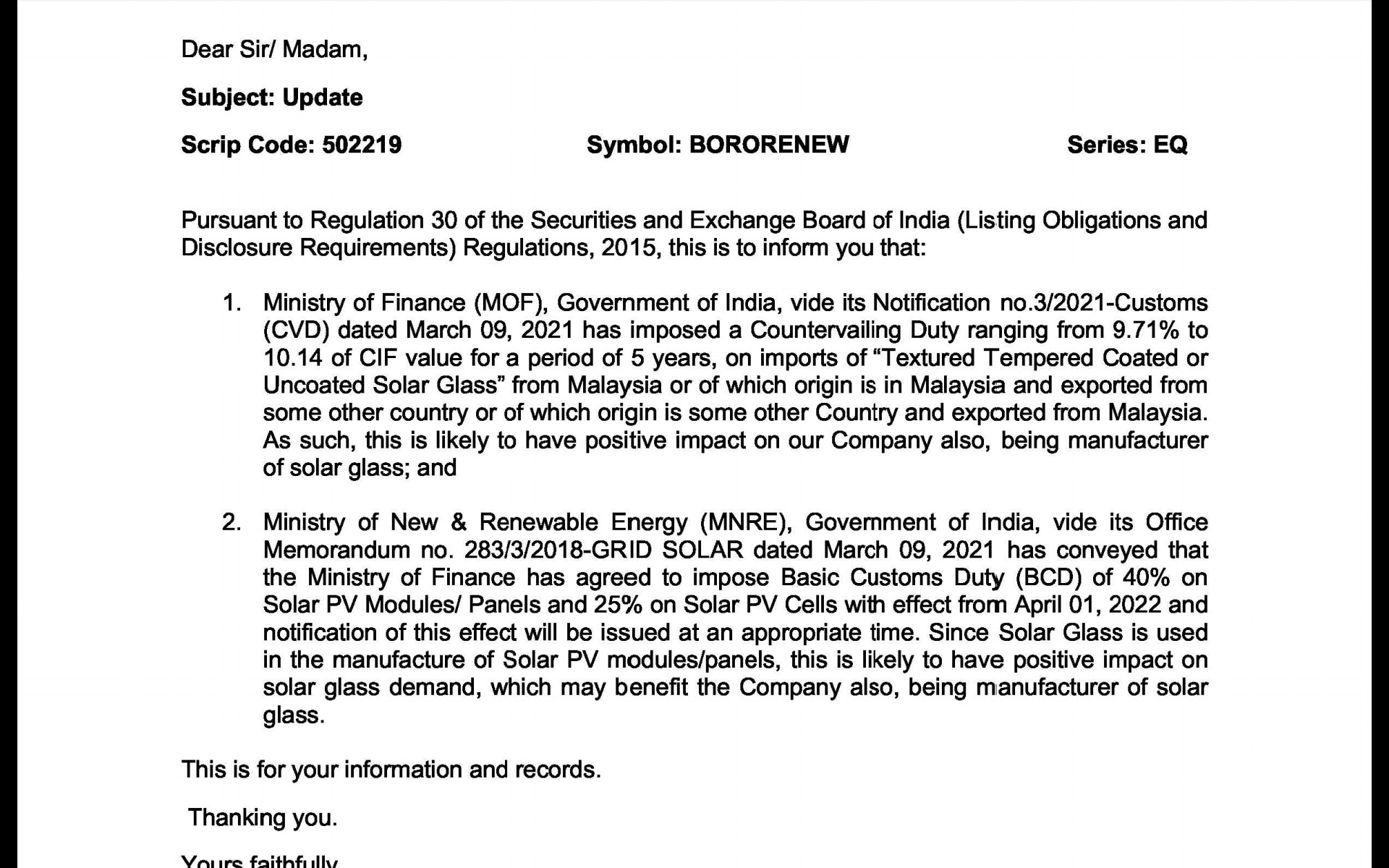

Dual positives

- Govt of india has notified for a 5 year duty specificallyfor solar glass from April 1st 2021

- in addition as well on solar panels from FY 22 onwards - thus positive for whole industry

mgmt can now be bit more aggressive on growth Capex with this protection shield, market will have better trust on margin visibility and consistency

4 Likes

5 Likes

I feel that CVD on solar modules may not really help Borosilicate Renewables.

A. The duty is proposed from Apr 1, 2022 i.e. one year away. This is to ensure that all successful bidders for solar power tenders have sufficient time to complete their imports before the duty comes into play. As such for next 1 year there will be no +ve impact on solar glass sales.

B. Indian mfrs of solar modules may still prefer to import solar glass if prices are favorable. Even a 10% CVD differential may not deter imports if prices go down which is likely to be the case if the capacity goes up multifold.

In short, short term outlook for the company is good but long term is a bit cloudy.

1 Like

Well, that may be true…but please note that imports have lot of additional costs apart from purchase price. I have noted few as below-

-

Working capital - in case of imports, its mostly LC payments so money gets blocked for around 3 months more than buying locally (BR gives credit of 30-45 days)

-

Planning and cost of delays - One has to plan atleast 3 months in advance, and more so now a days considering shortage of containers, port clearance issues etc

-

Cost of containers keeps fluctuating so one has to account for that

-

Since imports can be ordered in container loads only (whereas BR provides supply as per demand), one needs to have warehousing space and hence warehousing charges.

Considering all of the above, only large buyers who have long lead time order visibility, dedicated imports departments and large working capital pool would be better off in importing. Even they would be sourcing at least 10% or so from BR for urgent requirements and as a second source for supply assurance. Since BR’s capacity is not even 50% of the total domestic demand, it seems they are well protected against any global competition for next 2-3 years (unless local competition comes up)

12 Likes

The current market prices of BR glass is approx Rs 570 per sq.mtr. i understand the prices has reduced by 5-7% in the month of the April (what is being quoted). Taking Rs 570/m2 as the avg price for Q4 and with an approx capacity of 2 GW, it is expected that with back of the envelope calculation, they would have made ~ 1.43 Million glass pieces in this quarter. It translates to top line revenue of Rs 160-162 crores ( optimistic analysis with more than 90% plant utilization) and with 37% EBITDA margin, should give 60 crores of operational cash flow in Q4. The whole year EPS is expected to be in the range of 5 with the current price ~ P/E of 50-52 (seems reasonable seeing the demand and growth story). I feel eventhough the management keeps saying the price is not sustainable, still Rs 550 would be a realistic price as the price from China is ~ USD 8.3/sq mtr landed which is still higher than BR price. since the expansion capacity would be operational from '22, the full year revenue for 21-22 should be similar to what Q4 and Q3 has been.

request for your views please

Disc: Invested

5 Likes

I concur with your numbers. I think company management is very conservative and smart. By being conservative, they are keeping margin for themselves in case of any unknowns. By underplaying their domestic monopoly status and continue to harp on the fact that they are price takers and not price givers(and everyone knows large chinese capacities coming on line and will put pressure on prices in future) , they are discouraging any potential competition which is very smart strategy. I will repeat that Borosil’s bigger concern would be potential domestic competition. So fluctuating solar glass prices is a boon in disguise for them.

13 Likes

Slowly and Steadily we are transitioning to a solar first economy. 40 GW of solar capacity reached from single digits just a few years back.

5 Likes

Market prices of 2.0mm & 3.2mm solar glass down 30.0% & 32.3% in last week to Rmb28.0/m2 and Rmb22.0/m2 respectively, due to low operating rates of module manufacturers and increased solar glass capacity.

Xinyi Solar and Flat Glass forecast solar glass prices to drop below Rmb30/m2 and Rmb25-28/m2 respectively this year on more supply.

1 Like

This is being reflected in share price as well.

Assuming prices come to 30rmb/m2 as forecasted,

- Let’s add approx 10% import duty applied wef from April1

- Shipping and logistics cost is super high across world and to remain so in near visible future, that is likely to add to a net landed cost as well as time cost of money - say 10 to 20% ( more informed folks can help make it more real)

Actual landed cost would inflate anywhere between 20 to 30% I.e. 36 to 39 rmb/m2

I.e. INR 420 to 480/m2 on a sustainable basis - a base case scenario baseline for global competition

With DCR requirements, time critical projects, global shipping disruption, make in india push - BR will be able to charge equal or slight premium and thus seems well placed. These price drops will make it less attractive for local competitors to come in.

130 to 140Cr top line and 22 to 25Cr per Qtr is doable even after drop in prices of glass.

Approx 500 Cr annual rev and 100 Cr PAT with current mkt cap of 3250 Cr is quite reasonable, newer capacities when they come up will have Operating leverage as well, given brownfield expansions.

3 Likes

You have missed a very important key word, they are less than 2% of global capacity now .

As you pointed out they have to scale up, which they are doing. Present capacity double is already on the process and on the existing land they have they can double yet again on their capacity. So after the two doublings they should reach about ~10% of global capacity.

-

Currently Xinyi Solar is 30% of global capacity, Flat Glass is 20%, Louyang is 8%, IRICO is 7%, Jinxin Solar is 6%, CSG is 4%. So Borosil is not in top 5 also.

-

Chinese Government had lifted capacity expansion controls on solar glass in late 2020. A lot of capacity plans have been announced. It is expected industry capacity will grow 60% YoY by CY22. There will be more additions beyond 2022. 1st round of new capacity will kick in from 2H21, that is why solar glass prices have started correcting

-

Beyond tier-1 players smaller peers and new entrants also plan to add capacity like Xinfuxing Glass, Almaden Glass, Kibing Glass, Anhui Yanglongji, and Anhui Deli. Fuyao glass, the largest automotive glass maker in China, announced fund raising of in Dec 2020 for new expansion (Including Solar)

-

So competitors are not staying still, which mean even if they double capacity they are not going to become no. 3 in the world.

Not true, they are a price taker only to the extent of prices in China + import duties the govt has levied. So if the landed price of solar glass in India from China is Rs 100, BR can charge maximum of Rs 100. They cannot charge Rs 110. Even at current Rs 100 in my example, they have very good profit margins.

-

What makes you think landed price solar glass in India from China cannot fall another 30% or 50%?

-

Do you know Xinyi Solar makes 50% EBITDA margins and Flat Glass make 35-40% EBITDA margins. Why are you so sure they cant cut prices further to sell more when they ramp up capacity?

-

What happens to Borosil’s margins if prices fall another 30%? @learning was 100% right Borosil has “zero pricing power”

3 Likes

Thats hypothetical but Possible if world decides to drop green energy plans overnight, or China adds further multifold capacity with heavy subsidies or for any other reasons

Even if this is considered Commodity, it has cycles and enough data points in thread to prove demand supply mismatch to not go away anytime soon, new capacities takes time. Prices went up sharply and corrected to midway - healthy sign infact.

Let’s see what Q4 commentary holds. Investing in many ways is about being optimist, each business has risks and that’s where exit plan need to be in place.

Technicals - support in place at 235 -240, bounced back few times…resistance at 320…consolidation in range for good no of sessions, with reducing volumes and higher delivery, retesting lower ranges

4 Likes

Just add to this, management of Borosil Renewables already expressed in previous conference calls that price increases are not sustainable and they expect them to come down and stabilize. So nothing out of the ordinary is happening.

Coming to the commodity part that so many fellow investors seem to keep harping about and stuck to:

- A commodity company gets commodity valuations if there are many alternatives available in the market. Borosil doesn’t have any.

- When a commodity product making company is the only one left standing in the market, it no longer gets valued as a commodity company, simply cause there are no alternatives available for the market to choose from. Instead of commodity company valuations, I would value Borosil Renew as a monopoly company and assign valuations accordingly.

On questions around why cant someone else start making solar glass

They certainly can but they wont and here is why

- Commodity companies thrive on economies of scale, just like you do not see 100+ companies making steel in the world, you will not see many players for even solar glass

- Only the fittest survive in commodity companies - lean balance sheets, low leverage and high economies of scale are essential parameters for any commodity company to survive. During the steel bust cycle of last decade, many steel making companies disappeared solely cause they were niche players with high leverage on their balance sheet

- BR’s balance sheet has only 74 crores of debt with 327 crores in reserve cash. To put this into perspective, they are making an operating profit of 30+ crores every quarter (when prices weren’t elevated). So when push comes to shove, BR can pay off its entire outstanding debt with just one quarters operating profit.

Why solar glass isn’t a commodity

While glass maybe a commodity, solar glass certainly isn’t. And here a few reasons why

-

Solar Glass actually requires a lot of technical capability to produce. Its not easy producing glass of any kind, requires a lot of skill and experience. To add to this, solar glass needs to be precise, it needs to withstand high temperatures, be sturdy and allow as much sunlight to pass through as possible.

-

Anybody with enough money can set up a steel plant, but not everyone can set up a solar glass plant. Why? Economies of scale. There is a reason why the glass giants of the world have exited this business as they simply couldn’t match the economies of scale coming out of factories in China (Xinyi Solar and Flat Glass). If, there were no custom duty to help borosil renewable gain the ground, I wouldn’t have been a investor in BR either, simply cause you cannot beat the economies of scale of a plant that is 5 times the size of entire solar glass capacity of India and controls 70%+ of the worlds solar glass supply.

Why this segment will not see much competition

While anyone with enough money can set up a solar glass plant, many wouldn’t. Here is why

Its just not worth the effort. Adani is the biggest consumer of solar glass in India yet doesn’t plan to set up a solar glass factory. It has announced plants to make solar PV films and assemble entire modules but has stayed clear of the solar glass industry. Why? Simply cause its not worth the effort.

Just like formulation companies in Pharma do not make every single API, similarly, solar module and plant makers do not have any interest in making solar glass. They would rather focus on their core competency and stay away from this sector.

Vinati Organics became a several thousand crore company just by specializing into manufacturing of few chemicals. Anyone with enough money could have set up another ATBS and IBB chemical factory, but they didn’t cause Vinati evolved, made their process better and eventually became so good at what they do that a multinational giant had to exit the market cause they couldn’t beat Vinati on cost and quality.

I foresee a similar trend playing out with Borosil Renewable in the coming years.

Hope this helps.

Disclosure: Largest holding in my portfolio and I am very bullish on the entire solar sector. I believe this sector will generate the maximum wealth and value over the next decade and I am watching it very closely. So please take this review with a pinch of salt and do your own research. Not a recommendation.

24 Likes

While i would tend to agree with some of the points that you have mentioned, I would not agree with the conclusion that you have drawn, here is my take on the same:

- Monopoly : they are less than 2% of glboal supply chain, with or without duties, they are not big enough to command a monopoly position, its a tradeable commodity and unless they scale up i would stay short of calling them a monopoly.

- They have zero pricing power. They are a price taker, which mgmt has said again and again, if you don’t have pricing power, you are not a great business let alone being called a monopoly.

- Duties etc are fine, but in the larger ecosystem, they are a very very small fish. They might get away for sometime, but if the end industry i.e. solar prices are decreasing all the players will feel the impact. I don’t think A big player like Adani will be paying super normal price just because domestic player is selling stuff, Adani will look for profitability first and then anything else, atleast if i was a sharehodler of Adani i would expect the same. Eventually economics will take over.

- Competition is global. Sterlite tech is one example, where i burnt my hands, where mgmt kept on saying we have LT contract and pricing does not matter. But look at the kind of wealth destruction they had post OFC prices fell couple of years back. Ofcourse coming from AA stable did not help their cause much either.

- I agree that other players do not really enter into the market, but at the end of the day if the duty support continues, and end players find it costly, no one stops a china or other european companies with similar glass technology to set up shop in india. Every one wants to make profit and govt would be more than happy to push this agenda.

Disc : invested from little lower level. thesis is to see if they can scale up and get economies of scale benefit. ~2% allocation.

6 Likes

You have missed a very important key word, they are less than 2% of global capacity now.

As you pointed out they have to scale up, which they are doing. Present capacity double is already on the process and on the existing land they have they can double yet again on their capacity. So after the two doublings they should reach about ~10% of global capacity.

They are in India, when you are the only producer of a product and the buyers choice is either buy from you or import the product at the same price, but for imports the buyer has to pay upfront cash while the domestic manufacturer is giving a credit line of 45 days. Why would the domestic manufacturer not opt to source domestic as his first preference?

Not true, they are a price taker only to the extent of prices in China + import duties the govt has levied. So if the landed price of solar glass in India from China is Rs 100, BR can charge maximum of Rs 100. They cannot charge Rs 110. Even at current Rs 100 in my example, they have very good profit margins.

I am quoting the management from one of their interviews here

“We only ask the prices to be fair and upto the mark where its feasible doing business. Currently China is dumping solar glass in India at below cost price. Duties will help make the market a fair game. We do not want any special treatment, just a fair treatment.”

After two doublings, they will be the 3rd largest producer of solar glass in the world. First being Xinyi Solar and second being Flat Glass.

No body is charging super normal price, price ceiling is what China is selling at + the cost of import + import duties in India. BR wins as long as its selling price is at par or below this price.

I think you burnt your investment there cause of the management more than anything else. Everyone on the street stays away from Anil Agarwal’s companies. He is know to be the king of corporate governance issues and wants to only make wealth for himself without caring for the minority investor. BR’s management is opposite, they are a shareholder friendly company.

Same cost as import. BR doesn’t charge more than what it costs to import from China. Solar glass prices recently increased cause there was a) shortage of solar glass globally due to increased demand b) China made it mandatory for 50% of all new solar plants to have a double sided glass modules which doubled demand in China overnight. So what you’re witnessing in previous quarter and maybe even this quarter is due to increased demand in China. Nothing to do with Borosil’s price policy.

16 Likes

6 Likes