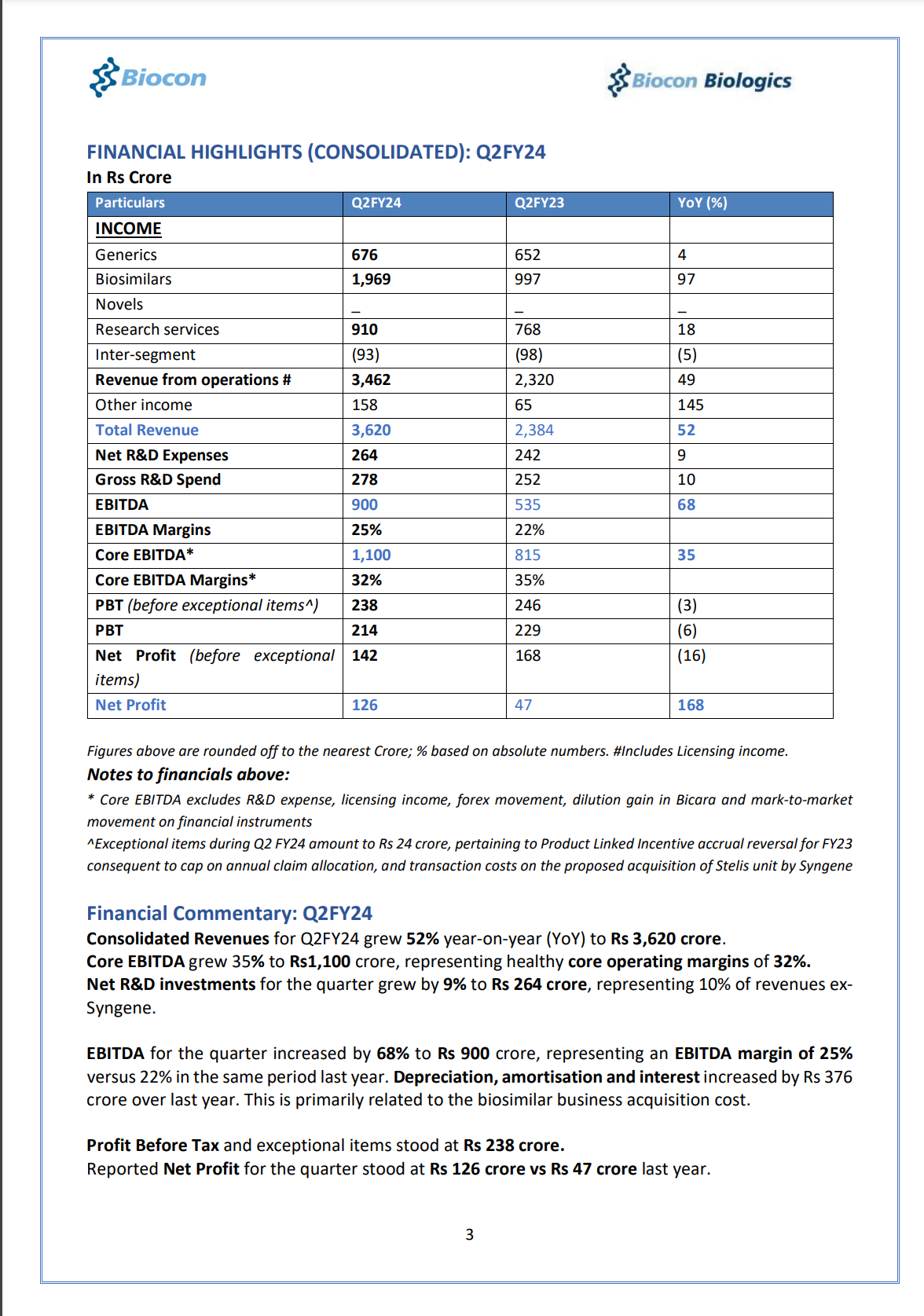

Biocon released its consolidated financial results for the fiscal second quarter ending on September 30, 2023:

-

Revenue: The company reported consolidated revenue of Rs 3,620 Crore, which represents a substantial increase of 52% compared to the same quarter in the previous year.

-

Core EBITDA: The Core EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization) stood at Rs 1,100 Crore, marking a significant rise of 35% year-on-year (YoY).

-

EBITDA: The overall EBITDA for the quarter was Rs 900 Crore, indicating a robust 68% YoY growth.

-

Net Profit: Biocon reported a net profit of Rs 126 Crore for the quarter, reflecting an impressive surge of 168% compared to the same period in the previous year.

-

Core EBITDA Margin: The Core EBITDA margin was at 32%, while the EBITDA margin stood at 25%.

These financial results are categorized into different business segments for Q2FY24:

-

Generics: APIs & Generic Formulations: The revenue in this segment was Rs 676 Crore, which represented a 4% increase compared to the same quarter in the previous year.

-

Biosimilars: Biocon Biologics Limited: This segment showed remarkable growth with a revenue of Rs 1,969 Crore, which is a substantial 97% increase YoY.

-

Research Services: Syngene: Revenue in this segment amounted to Rs 910 Crore, demonstrating an 18% growth YoY.

Income: Biocon made money from different parts of its business.

-

Generics: This part of the business made Rs 676 Crore in revenue, which is 4% more than last year.

-

Biosimilars: The biosimilars part did exceptionally well, earning Rs 1,969 Crore, which is a huge 97% increase from last year.

-

Research Services: The research services part made Rs 910 Crore in revenue, showing an 18% growth from the previous year.

-

Inter-segment: There was a 5% decrease in revenue from activities between different parts of the business.

Total Revenue from Operations: Biocon made a total of Rs 3,462 Crore from its various activities, which is a big 49% increase from last year.

Other Income: Biocon also made Rs 158 Crore from other sources, which is a big 145% increase from last year.

Total Revenue: In total, Biocon’s earnings for the quarter were Rs 3,620 Crore, which is an impressive 52% increase from last year.

R&D Expenses: Biocon invests in research and development.

-

Net R&D Expenses: The expenses for research were Rs 264 Crore, which is 9% more than last year.

-

Gross R&D Spend: The total money spent on research was Rs 278 Crore, which is 10% more than last year.

EBITDA: Biocon’s EBITDA, a measure of profitability, was Rs 900 Crore for the quarter, which is a 68% increase from last year. The EBITDA margin, a profitability ratio, was 25%, up from 22% last year.

Core EBITDA: This is EBITDA excluding certain expenses. It was Rs 1,100 Crore, which is a 35% growth, and it had a good operating margin of 32%.

Profit Before Tax: The profit before tax was Rs 238 Crore (excluding exceptional items), which is a 3% decrease from last year. The total profit before tax was Rs 214 Crore, which is a 6% decrease from last year.

Net Profit: The profit that Biocon made after all expenses was Rs 126 Crore, a big 168% increase from last year.