Please let us know if you can find the EB purchase by KMS in her personal capacity , soon after the bribery case where their staff had bribed or was black mailed by the Drug admin dept. for clearing their files. More like black mail as they already had approvals from all global regulators

I am not very ambitious on returns. My buy price (after accounting for splits/bonuses…) is about Rs. 17. Does 20X in 15 years count for a return?

Biocon tries too many things, it appears to be aggressive at times and very defensive at times.

Aggressive: developing new drugs (though with partnerships, licensing…), trying to be an innovator

Defensive: When they enter service space (with assured margins) that affects their product business

Too active: Buys a business from its customer, sells something else…

Pretty complex to analyse. Only concern is “outsized influence of the promoter, who is past the prime, on the business”

If you read close;ly… there is a certain regularity which is getting into their business and they are more foussed on monetizing Bio similars … They also have API’s ( linked to their generics ) and some generics and small molecules. Gestation of their business is long. and can be cyclical . They also spend sizable amount on R & D and call it out. They claim to make 30 % margin ex R &D and once R & D pipeline generates sizeable revenue . Numbers will start showing up . They also are probably best CDMO player potentially with 100 % India presence … There are off and on events which impact the companys standing but really not so much to sleep over. There is also an optonality about Bicara which not many people know about.

To round it off about Madams larger than life image, she is what she is and nothing much you can do about it Suffice it to say that there is a capable team below at all levels …

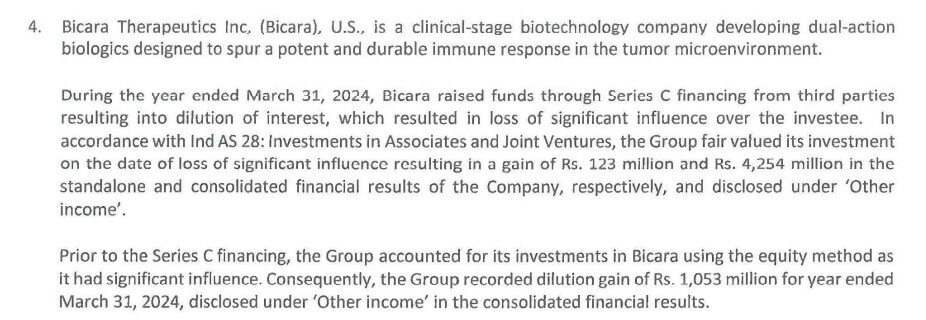

Bicara raised Seris C funding, which resulted Biocon Stake dilution, so there was a loss of significant influence over control by Biocon as there will be other funding parties on the board.

But that fund raise resulted into gain for Biocon agaisnt their stake sale.

Many positives in results. One of the good points is that finally management has made up their mind on no IPO for Biologics and will push equity raise in parent co to reduce debt. Bicara did an IPO and this was also a vindication of the companys earlier efforts

if my understanding is correct, they have not ruled out an IPO as yet. For now they are evaluating what is best option. Quoting her interview as reported in moneycontrol (source added):

“The IPO market is not very predictable right now,” Biocon and Biocon Biologics executive chairperson Kiran Mazumdar-Shaw told Moneycontrol in an interview on May 14 evening. “If we are not going to get value for an IPO, then why should we do it? If a merger is a better option, we will do a merger.”

“We are just being transparent,” she said. “If things suddenly change and it makes it very attractive to have an IPO, we will have an IPO. Otherwise, we will merge.”

The company has formed a board committee to evaluate all strategic options, including a merger, within a few months.