The share price fall in Viatris is because of disastrous financial result … and If not for this deal the fall would have been higher according to Motley Fool

View of Seeking Alpha is as follows

The share price fall in Viatris is because of disastrous financial result … and If not for this deal the fall would have been higher according to Motley Fool

View of Seeking Alpha is as follows

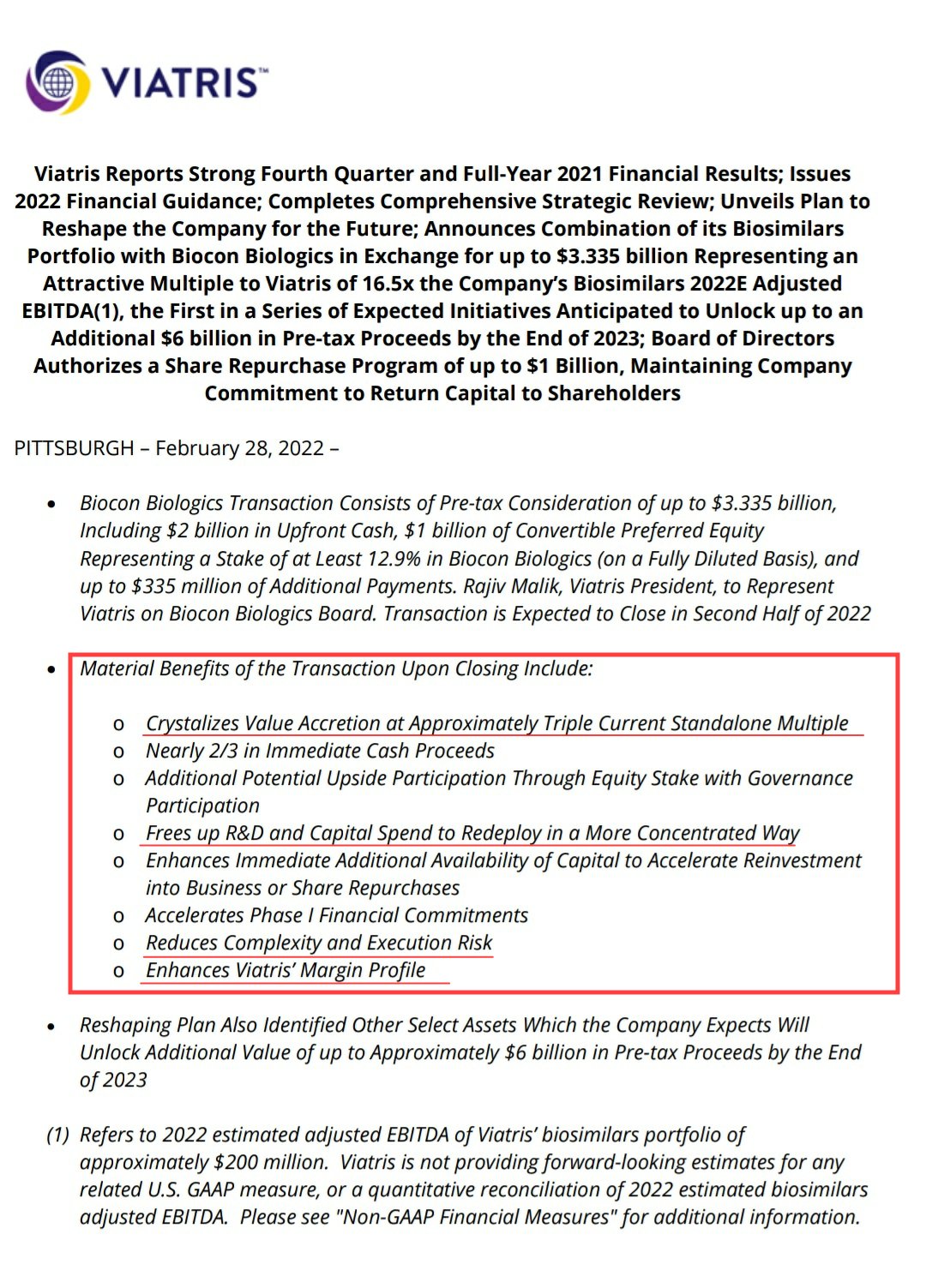

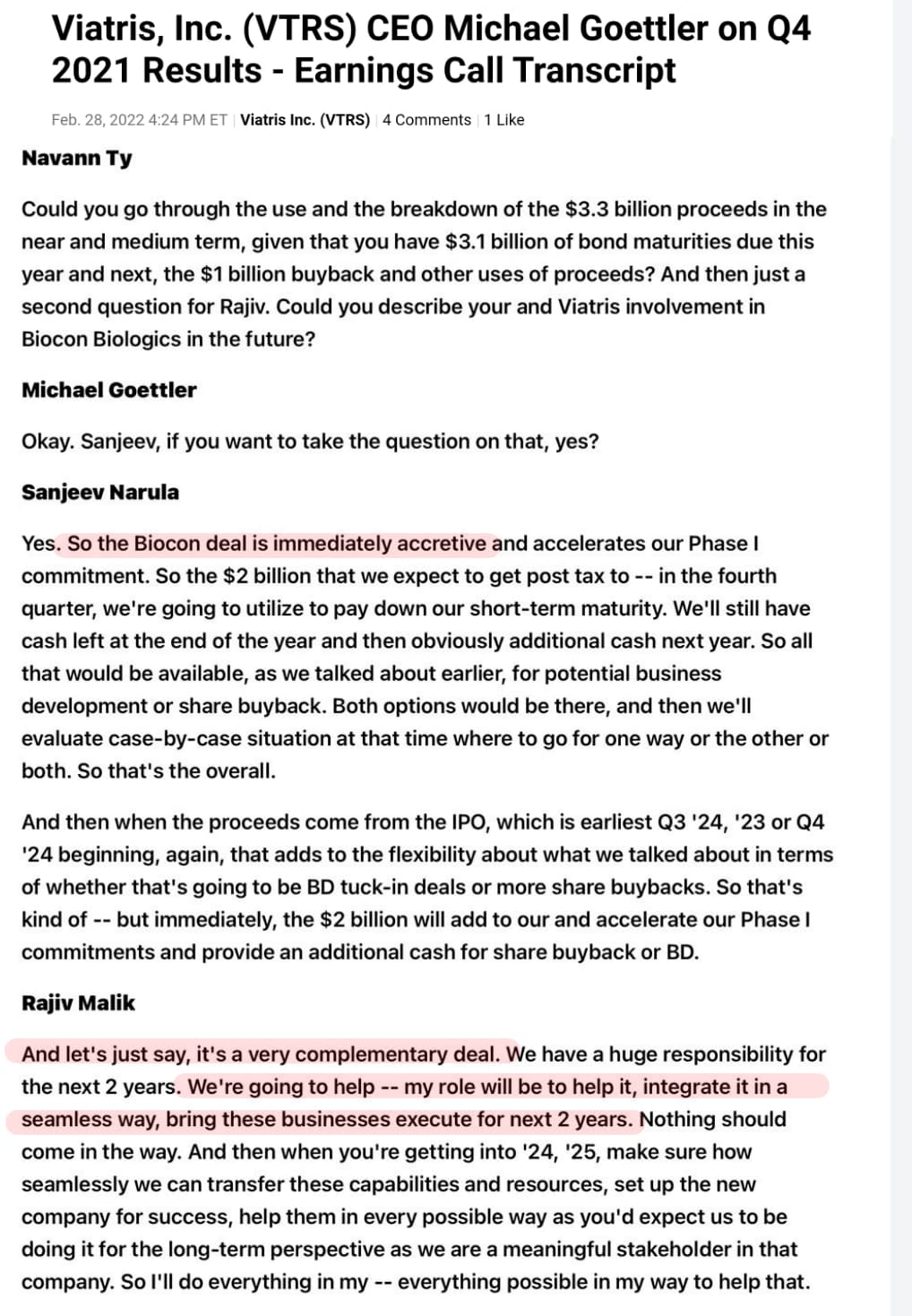

For Viatris the deal is immediately accretive & they have got a very attractive valuation.

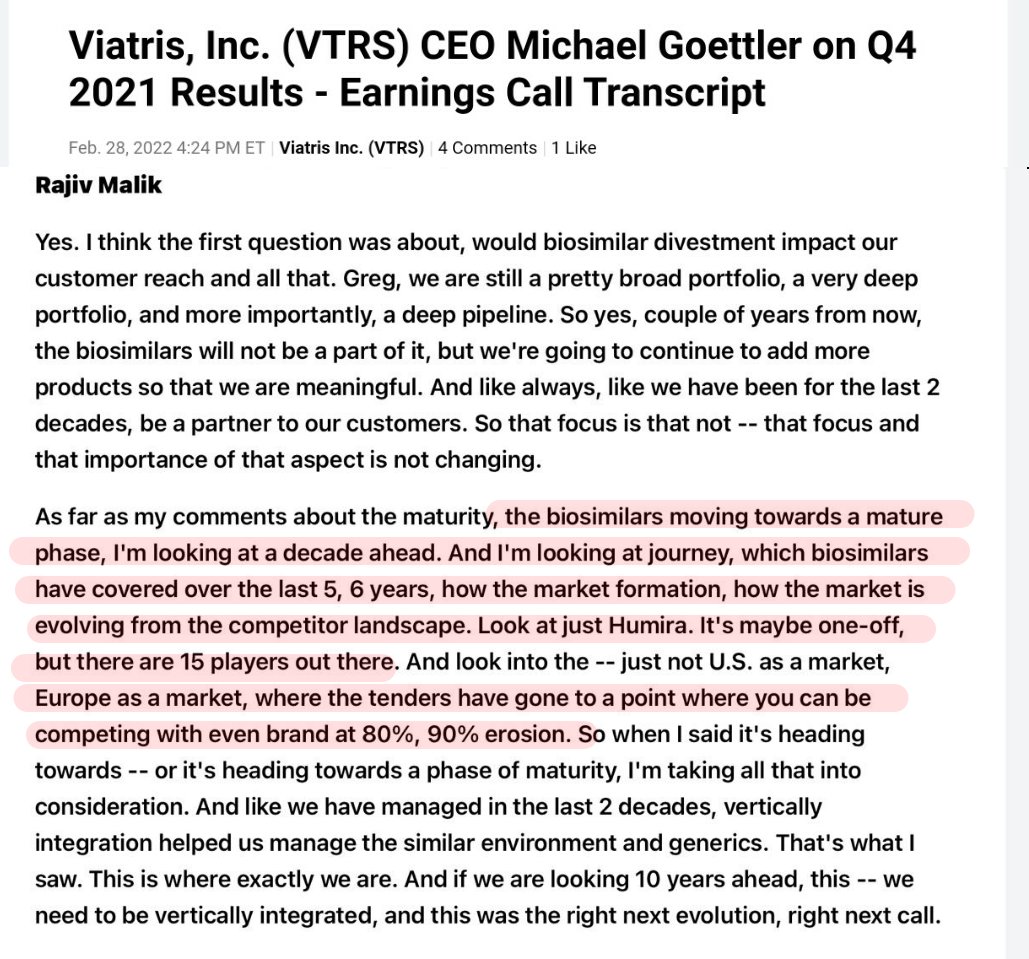

EBITDA margin of biosimilar business was lower than the company average for Viatris. It makes sense to sell the business at a very attractive 16.5x EBITDA multiple.

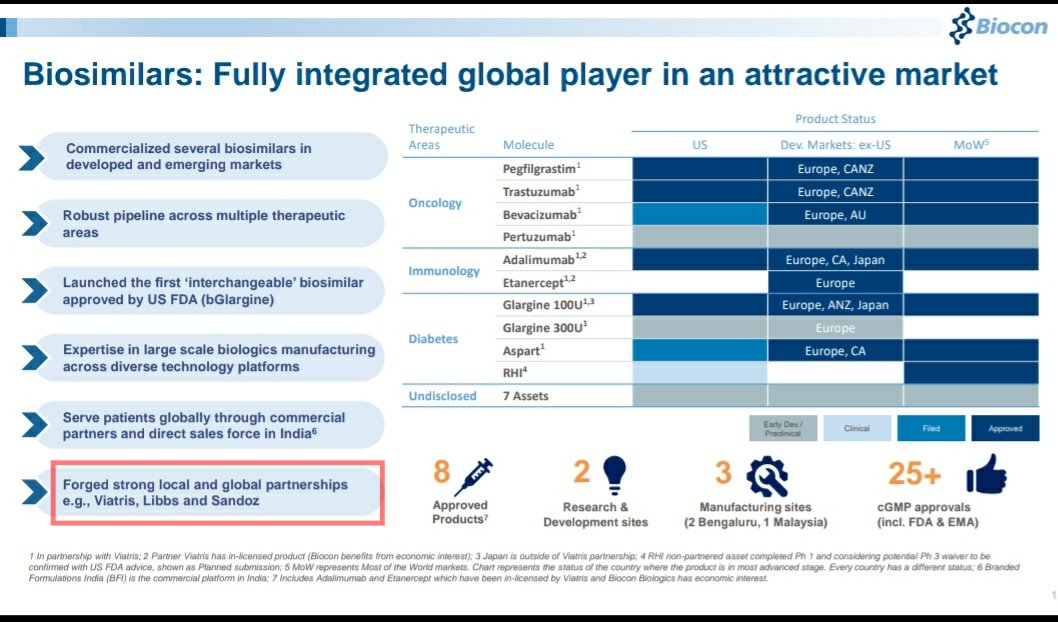

It seems like this deal is not the entire biosimilars portfolio. It does include all biosimilars developed alongside Biocon as well as a few others (biosimilars for humira, Enbrel, Eyelea)

But No mentioning of Abatacept (Orencia), Onabotulinum toxin A.

There is an option to buy Aflibercept at $175M payment due in FY25.

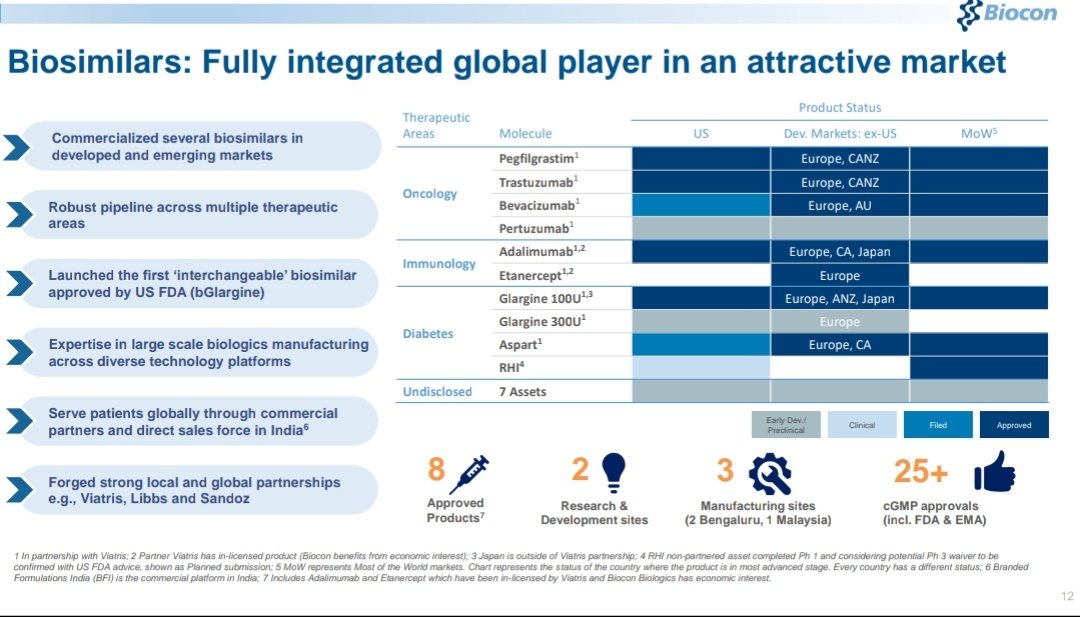

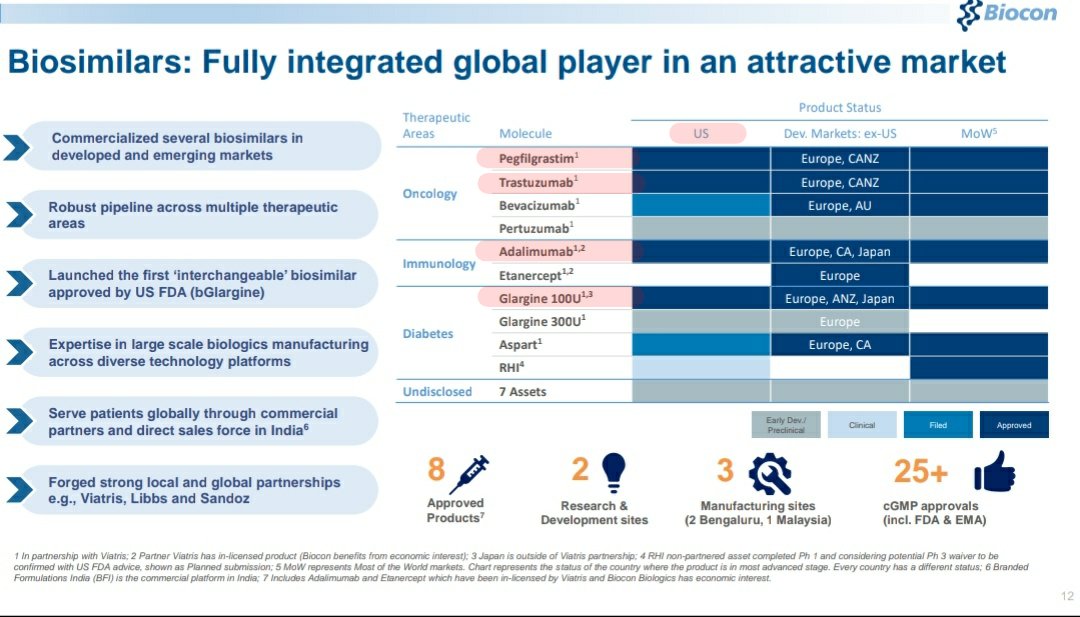

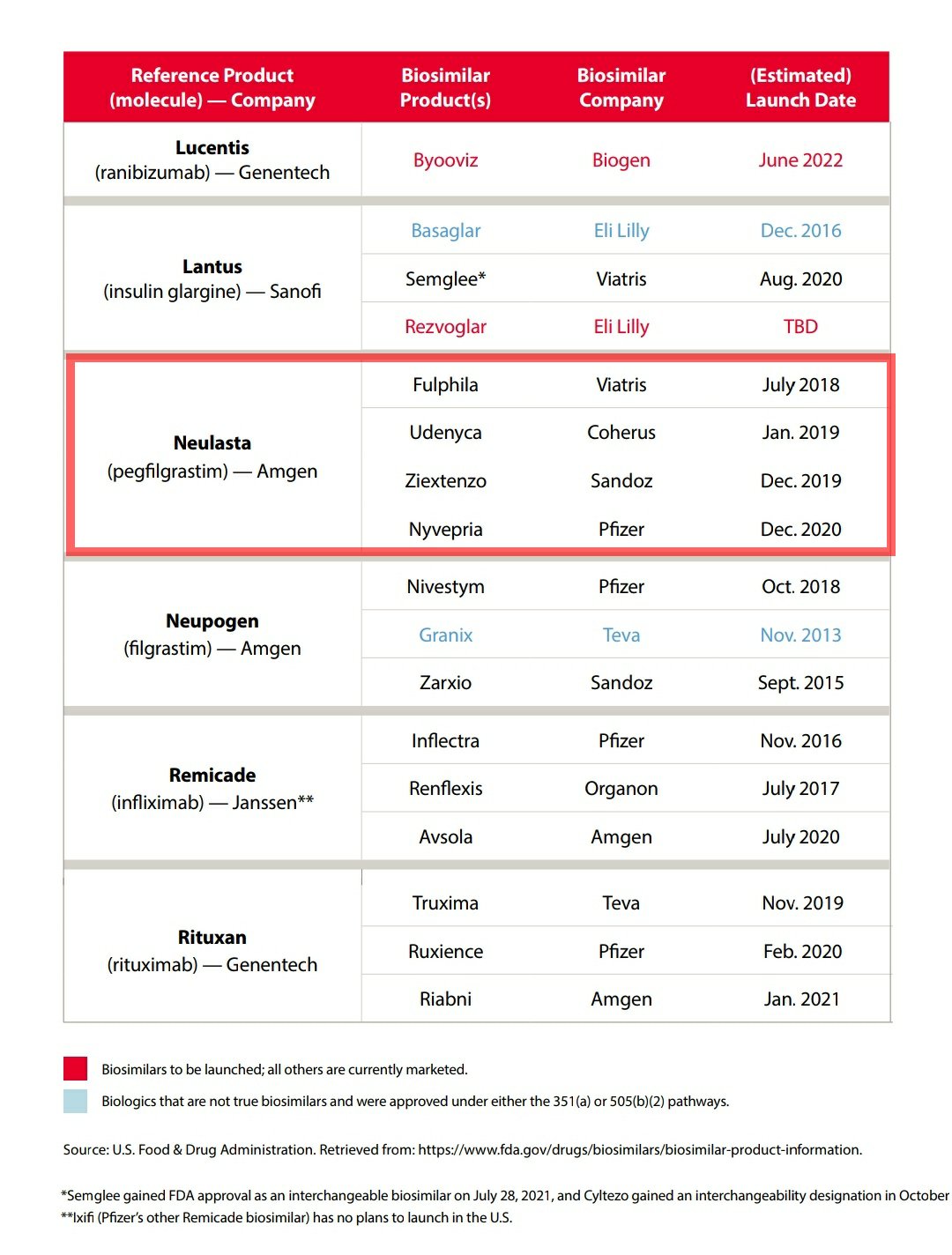

Right now they have only 4 Biosimilars approved in US and 3 of those were first to get approval

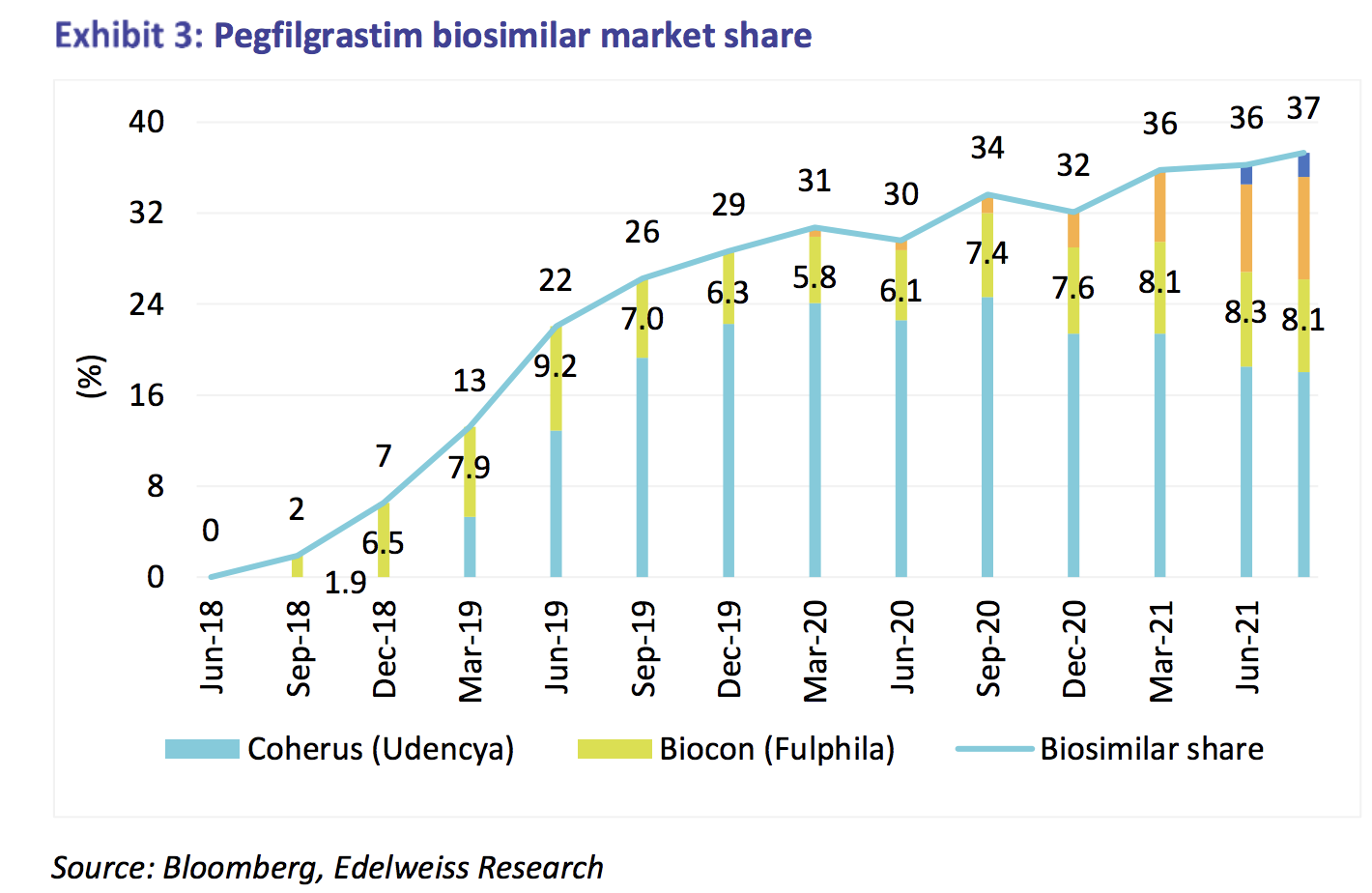

Fulphila(Pegfilgrastim)

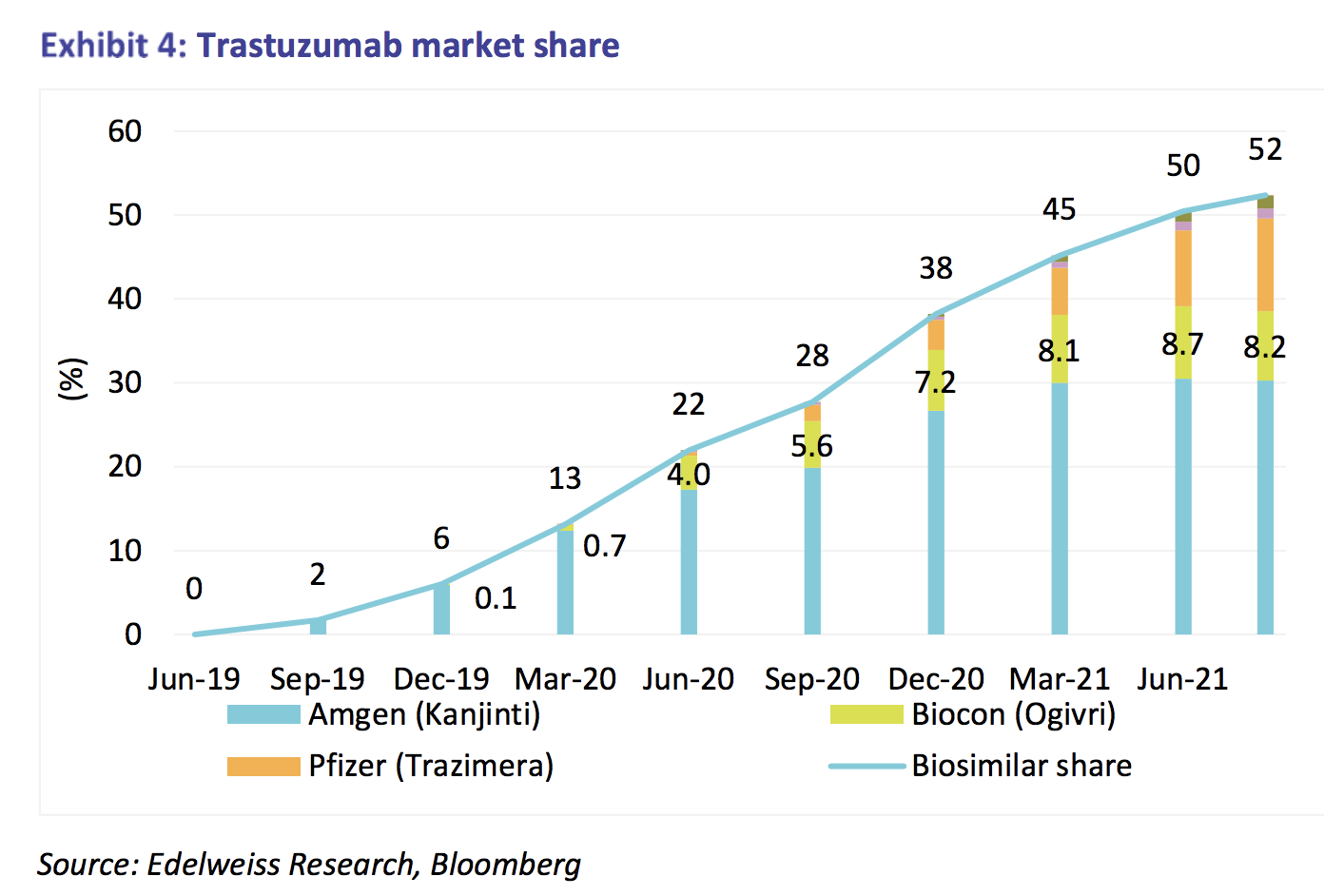

Ogivri (Trastuzumab)

Insulin glargine with interchangeability (Semglee)

Adalimumab(Hulio) will commercialize in US only on 2023 as there is patent protection.

Viatris (Biocon) was the first one to get approval for Pegfilgrastim biosimilar back in 2018.

They had launched Fulphila on July 2018.

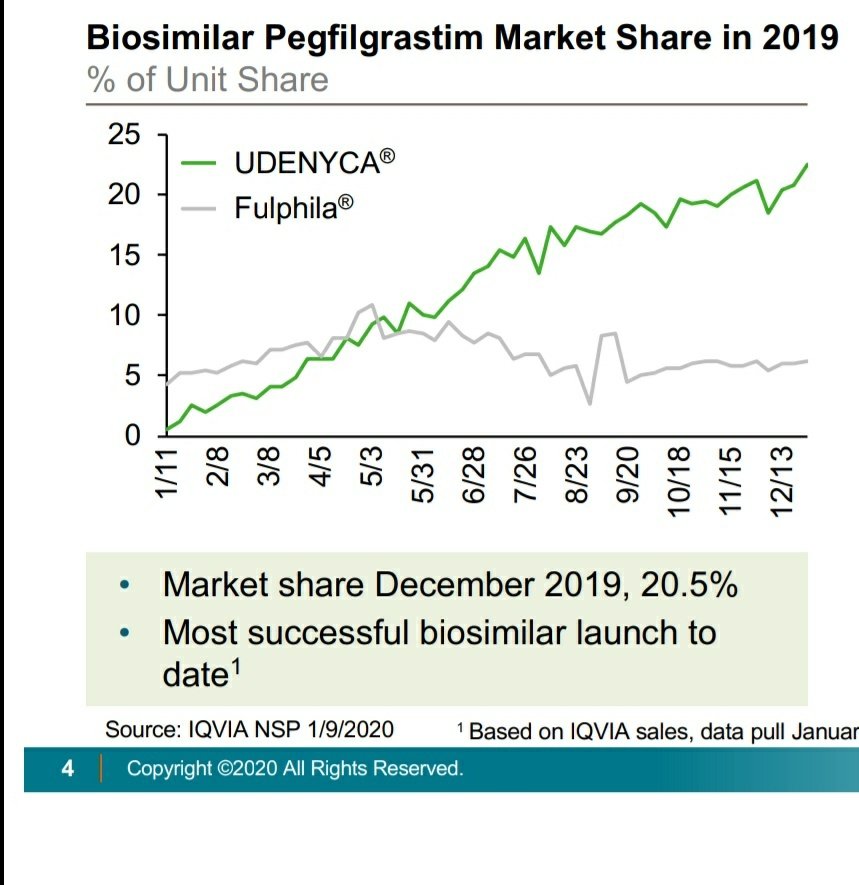

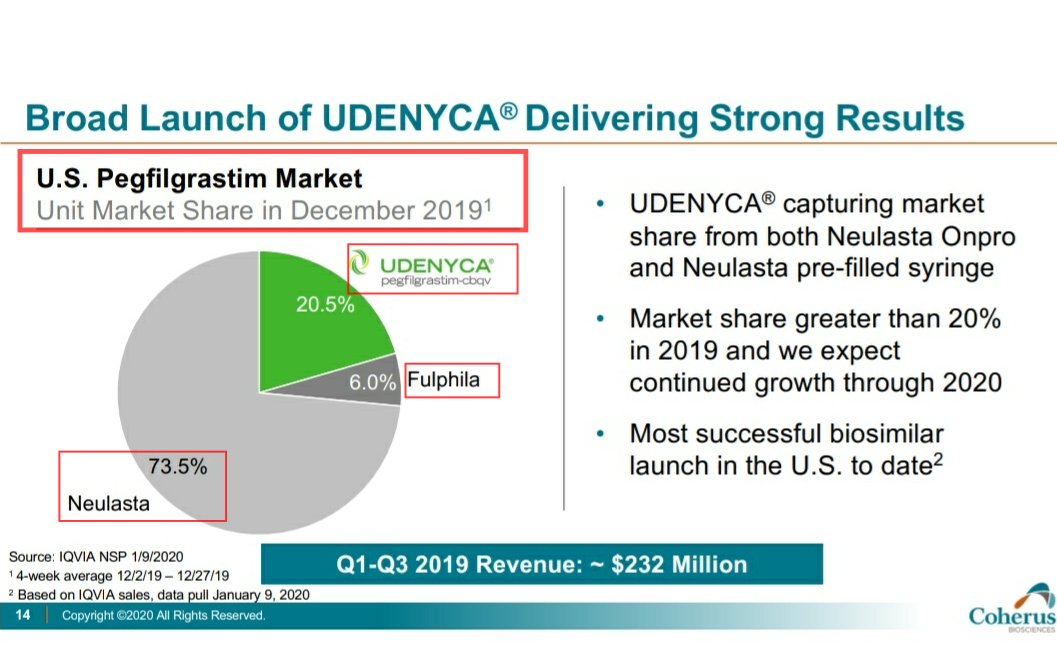

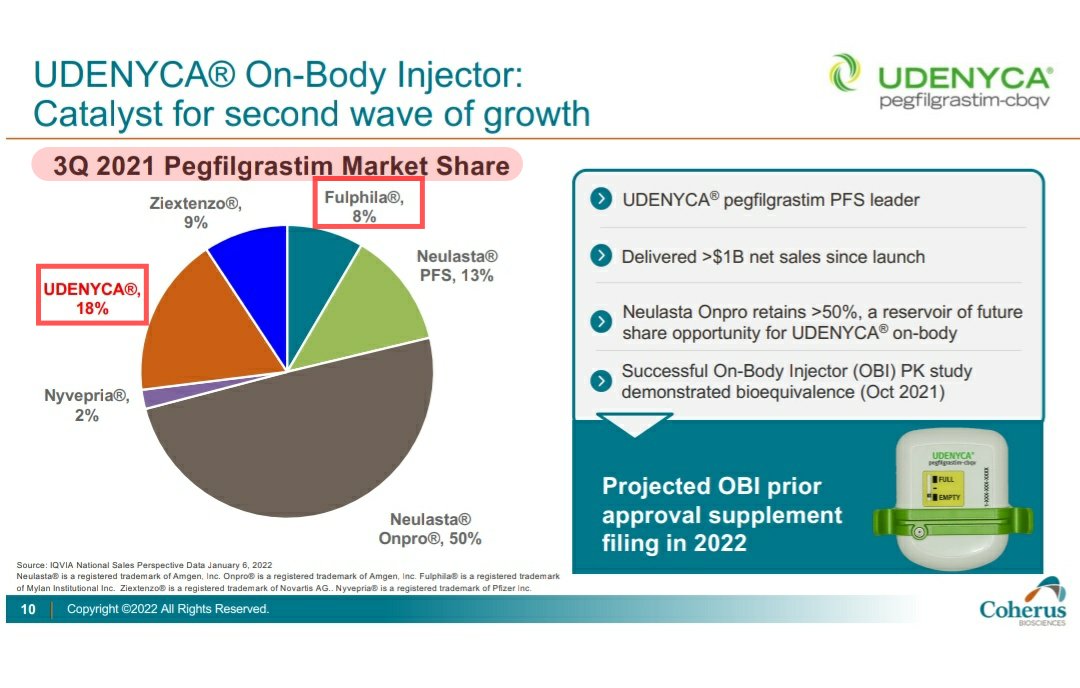

Despite being the first one to launch & having early mover advantage, they had lost market share to Udenyca by Coherus.

Coherus launched their product Udenyca on Jan 2019.

By December 2019, Udenyca had gained 20.5% market share, while Fulphila (Biocon’s product) had shrinked it’s market share to 6%

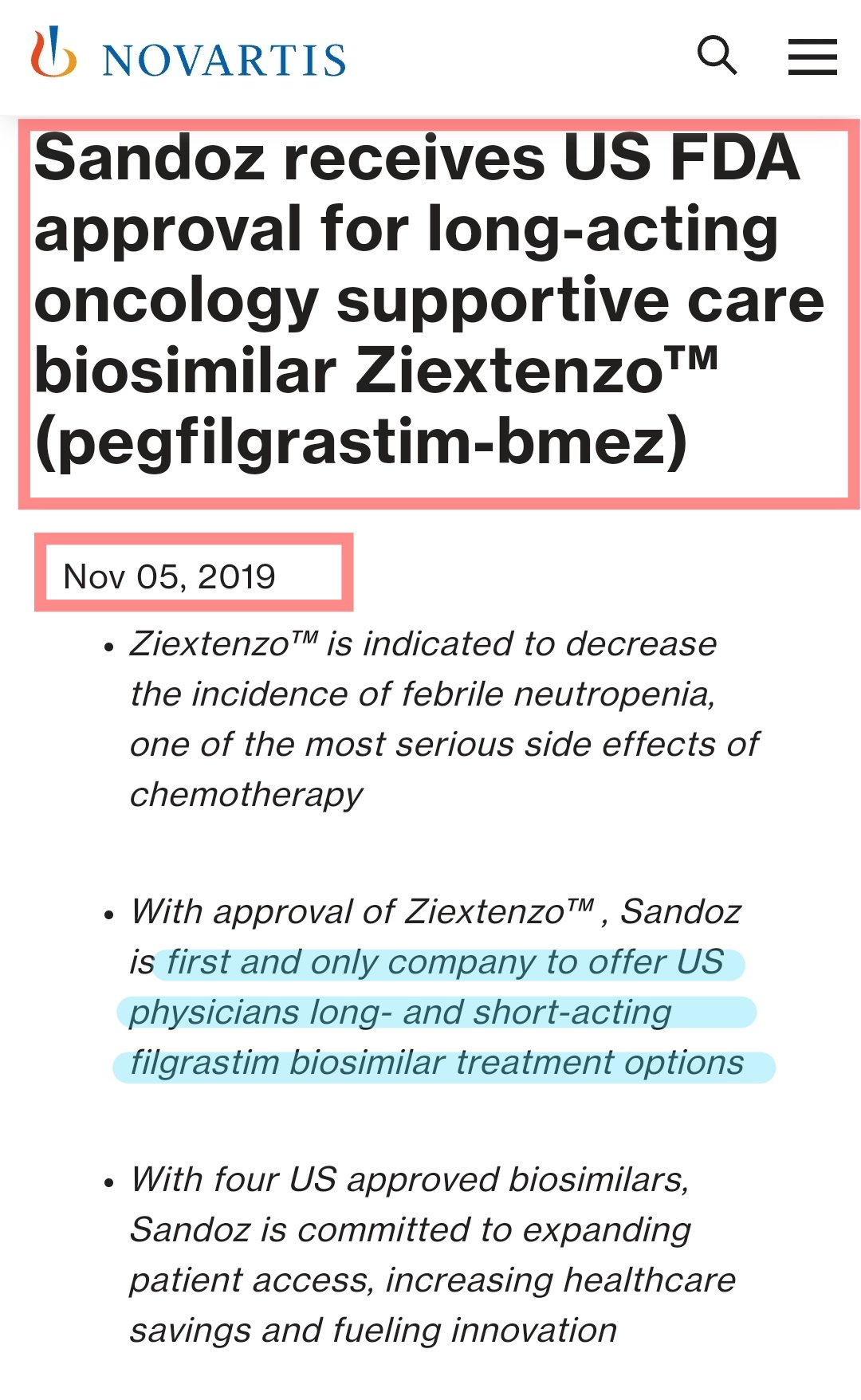

Another biosimilar of Pegfilgrastim had launched on Dec 2019, Ziextenzo by Sandoz.

Right now, even Ziextenzo has more market share than Biocon’s Fulphila.

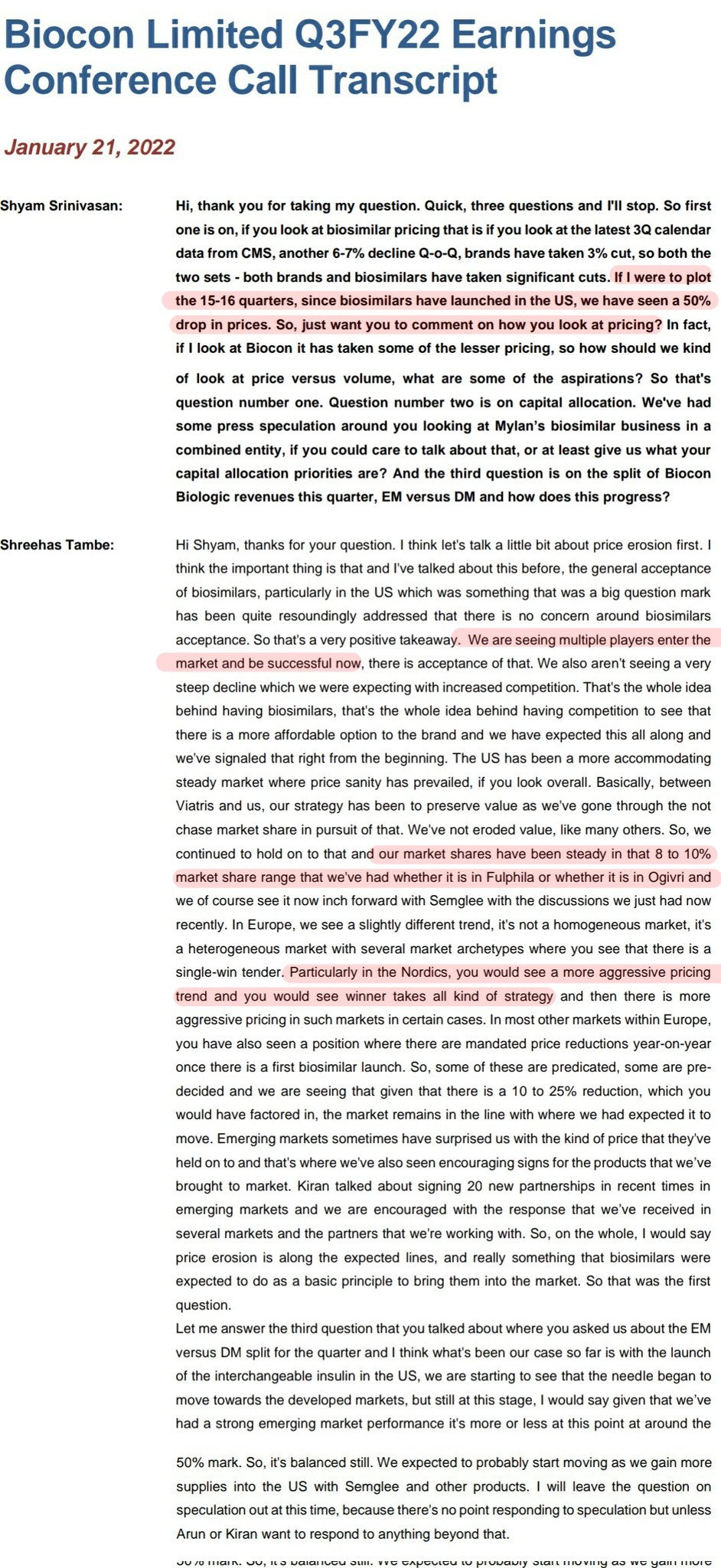

There is intense competition in Biosimilars.More players are coming in & it is not easy to maintain market share.

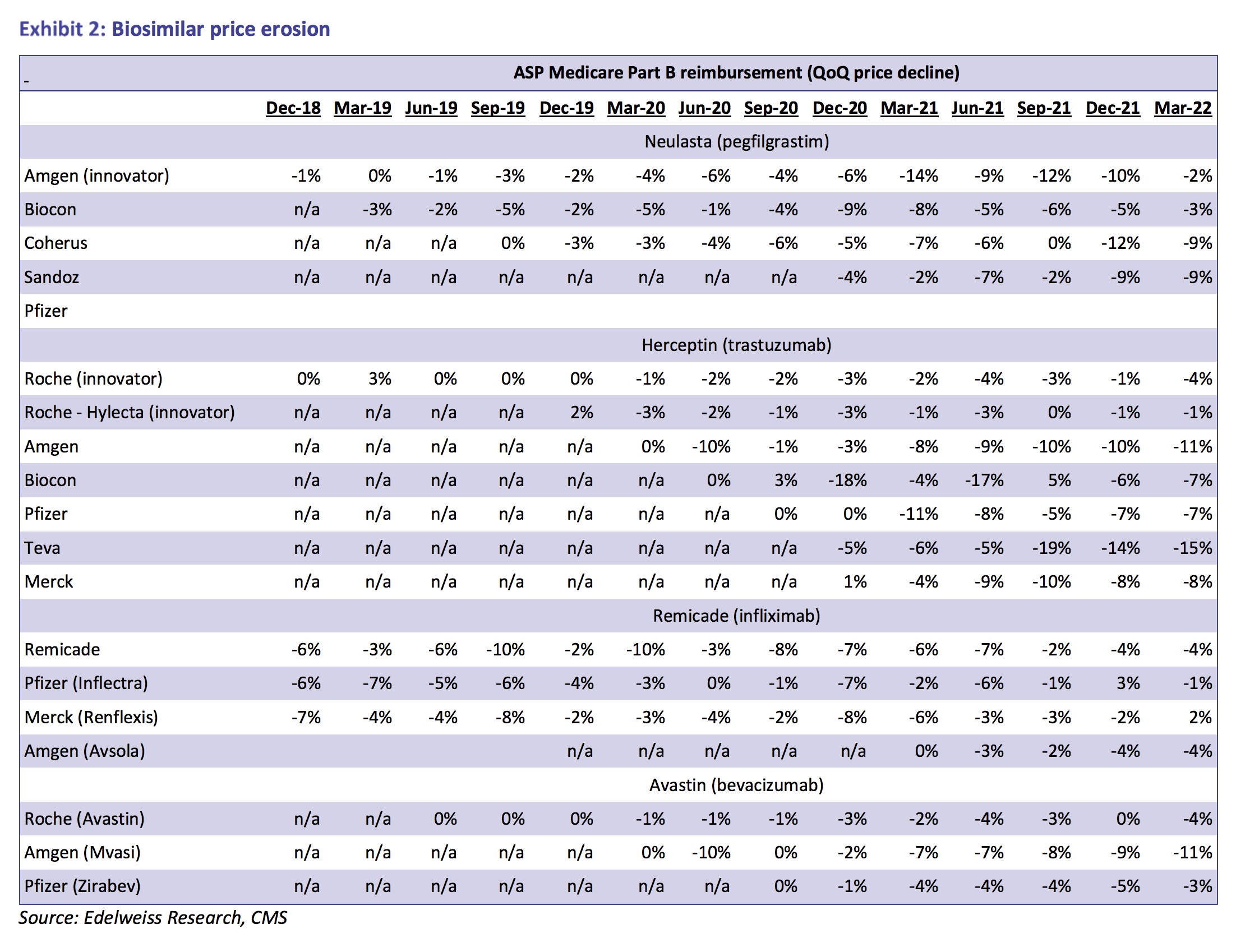

This leads to average selling price (ASP) erosion and margin decline as seen in generics.

In certain areas of Europe, there is tender,where winner takes all.

How did Coherus & Sandoz gain market share in Pegfilgrastim so fast while Viatris struggled?

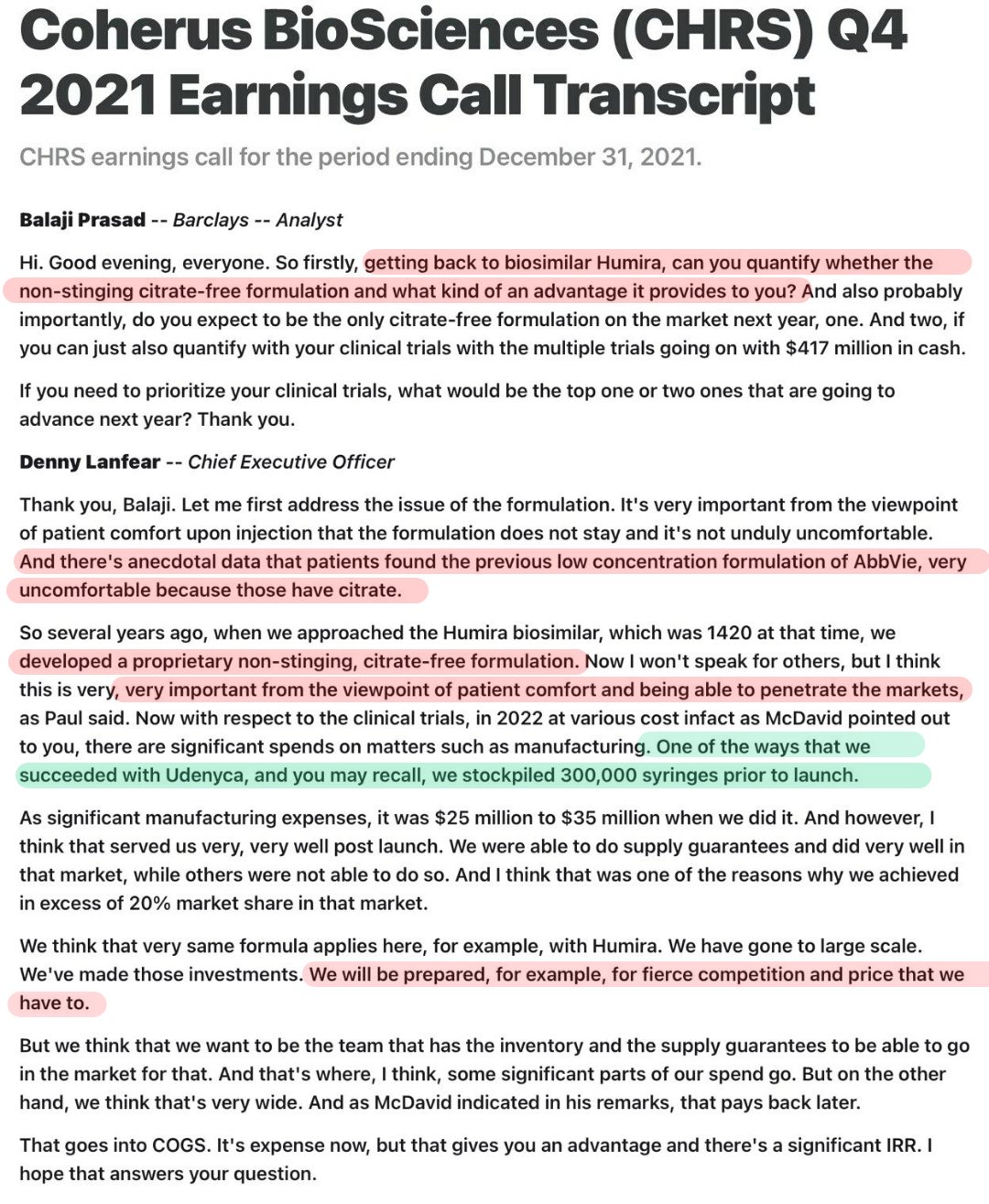

Coherus (Udenyca) - They stockpiled 3 lakhs syringes prior to launch & they were able to do supply guarantees & did very well in market where others couldn’t.

Sandoz (Ziextenzo)- They were the first & only company to launch both long & short acting treatment options.

Together with better marketing of Novartis they’ve also gained more market share than Fulphila.

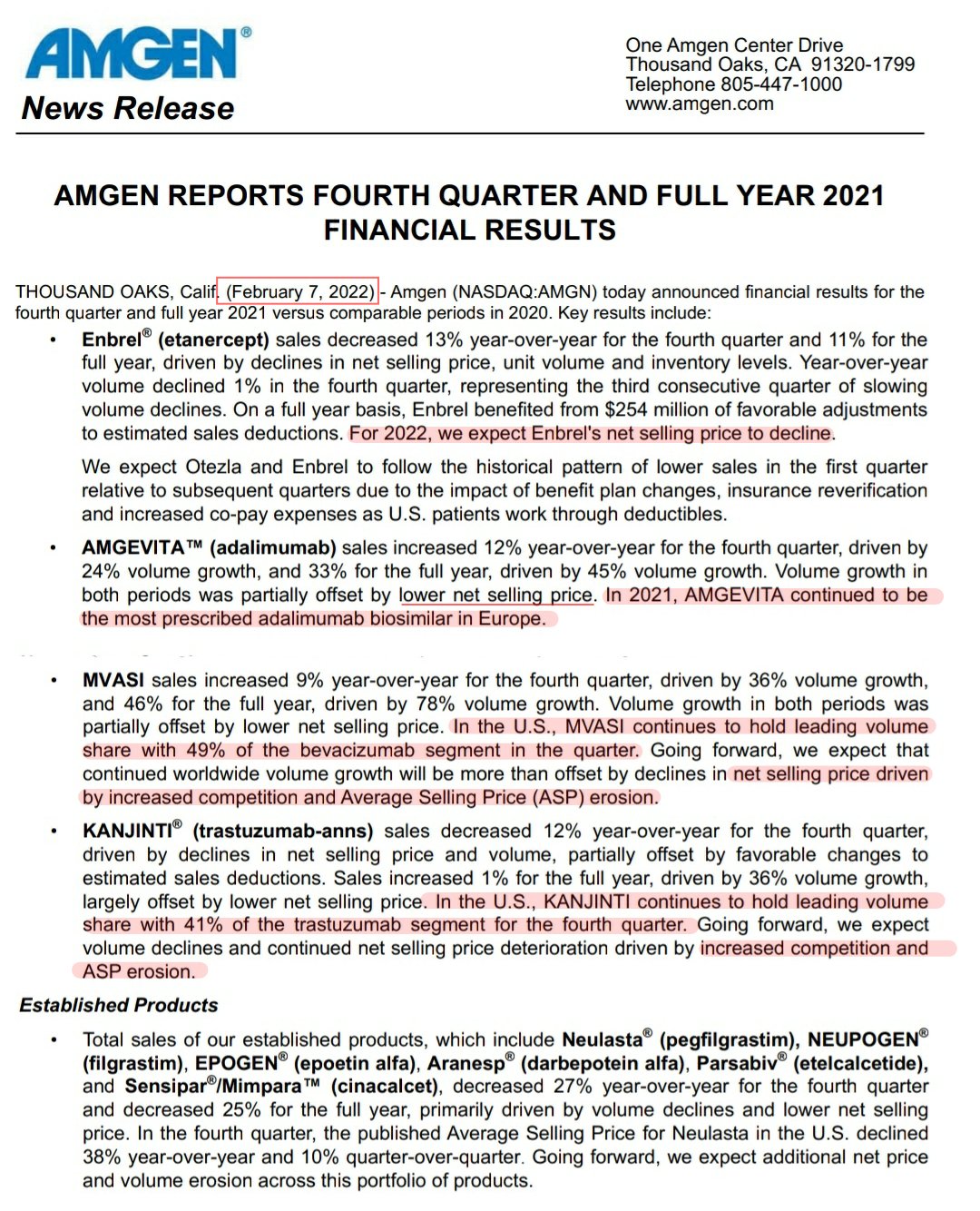

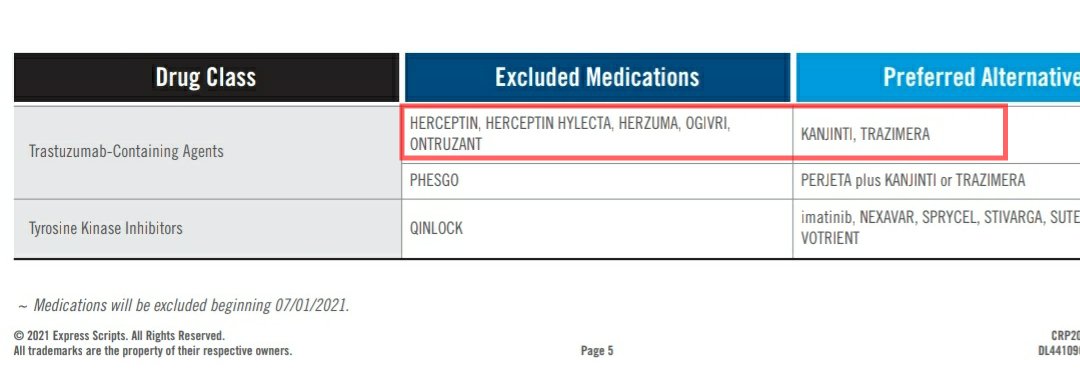

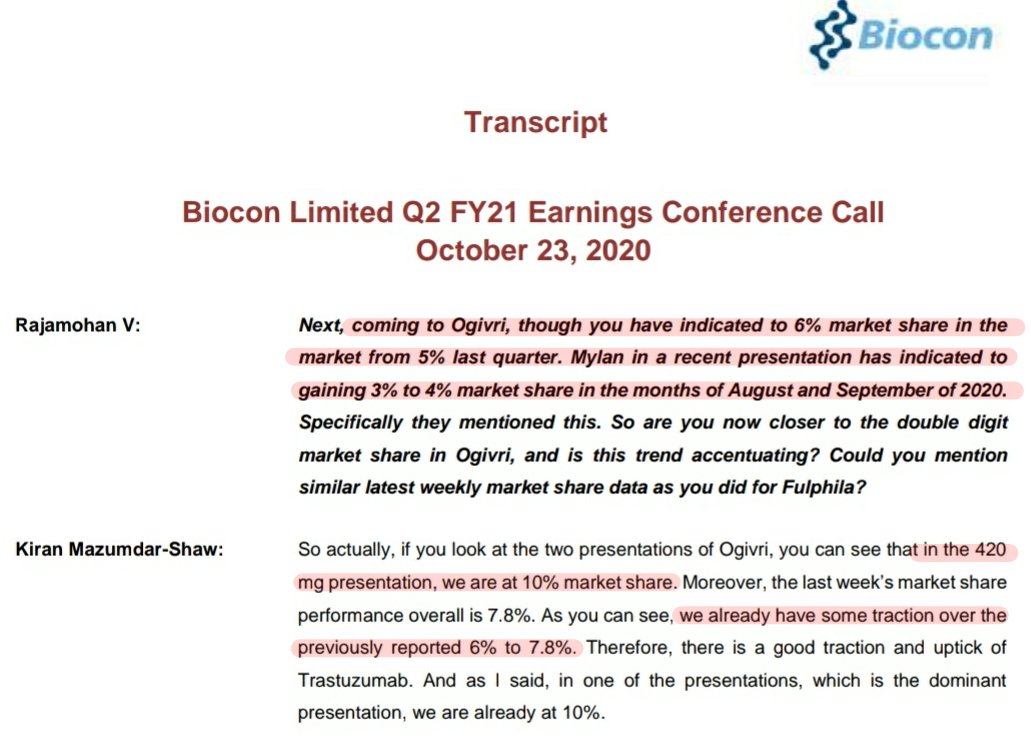

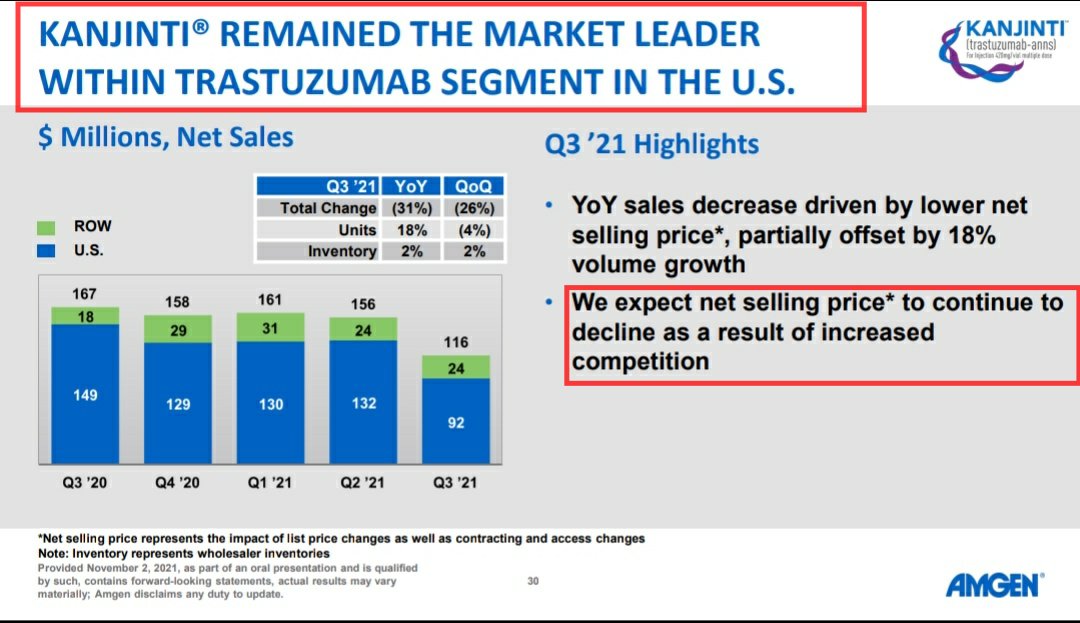

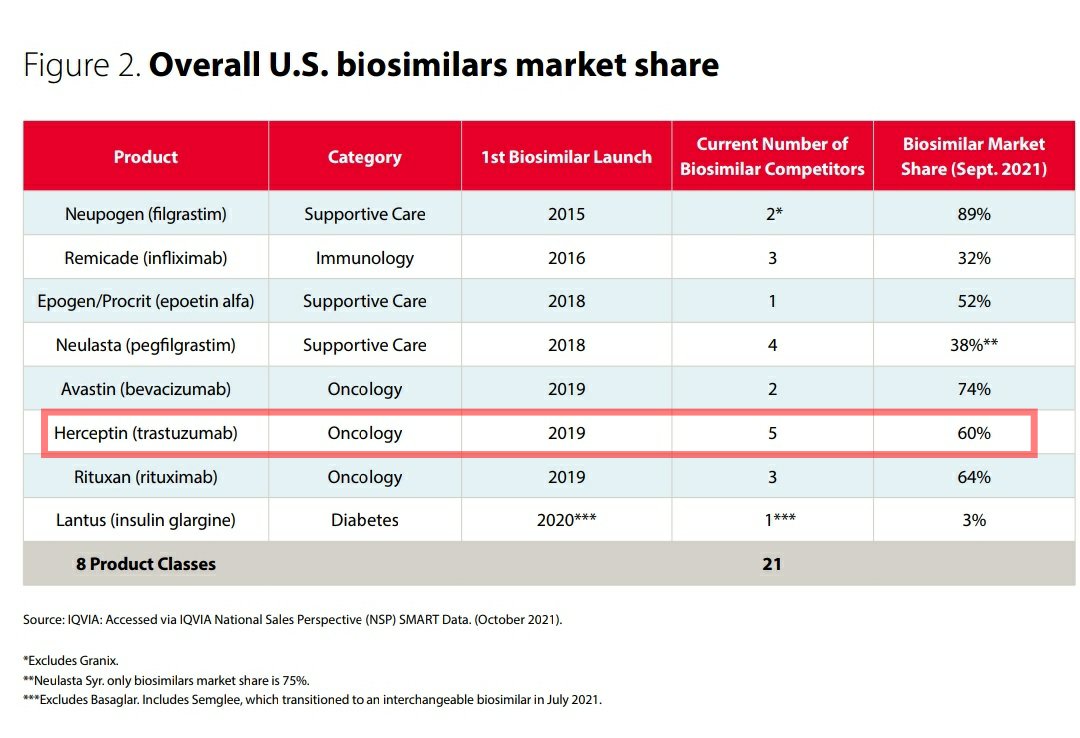

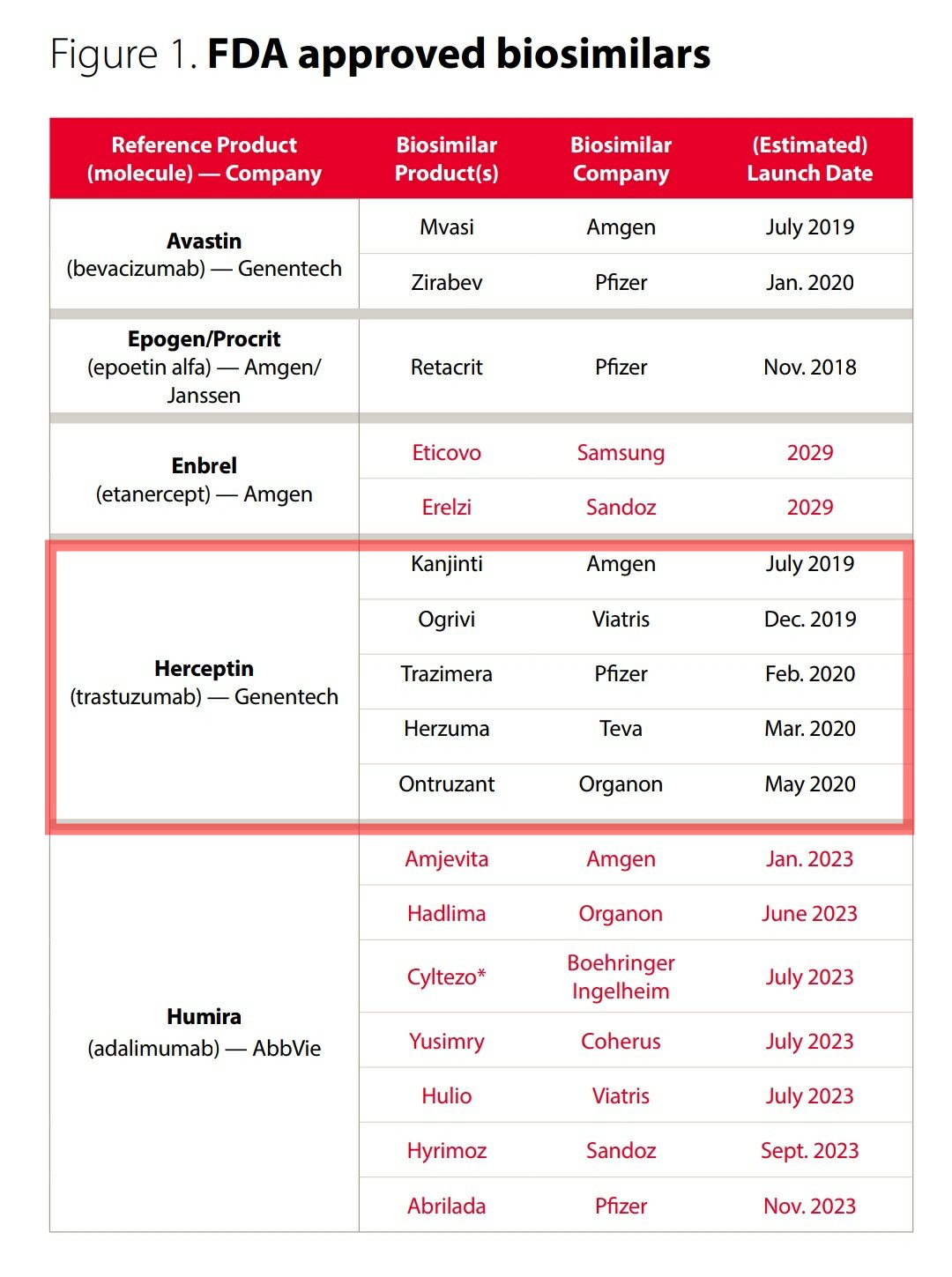

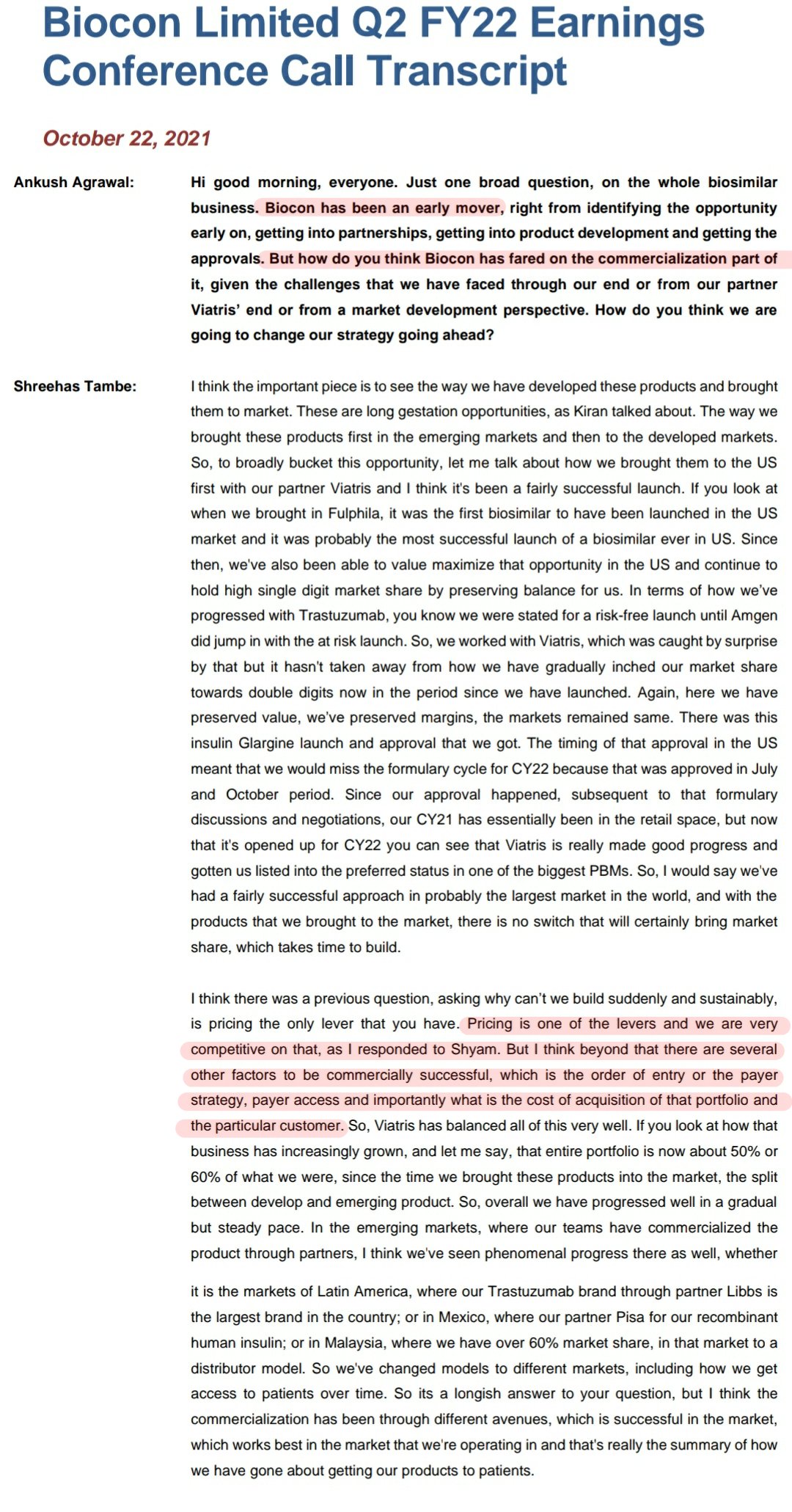

In case of Trastuzumab biosimilars, Ogivri of Viatris was dropped from preferred formulary list and substituted with Amgen’s Kanjinti & Pfizer’s Trazimera on Jan 2021.

Kanjinti is the market leader of Trastuzumab biosimilars now.

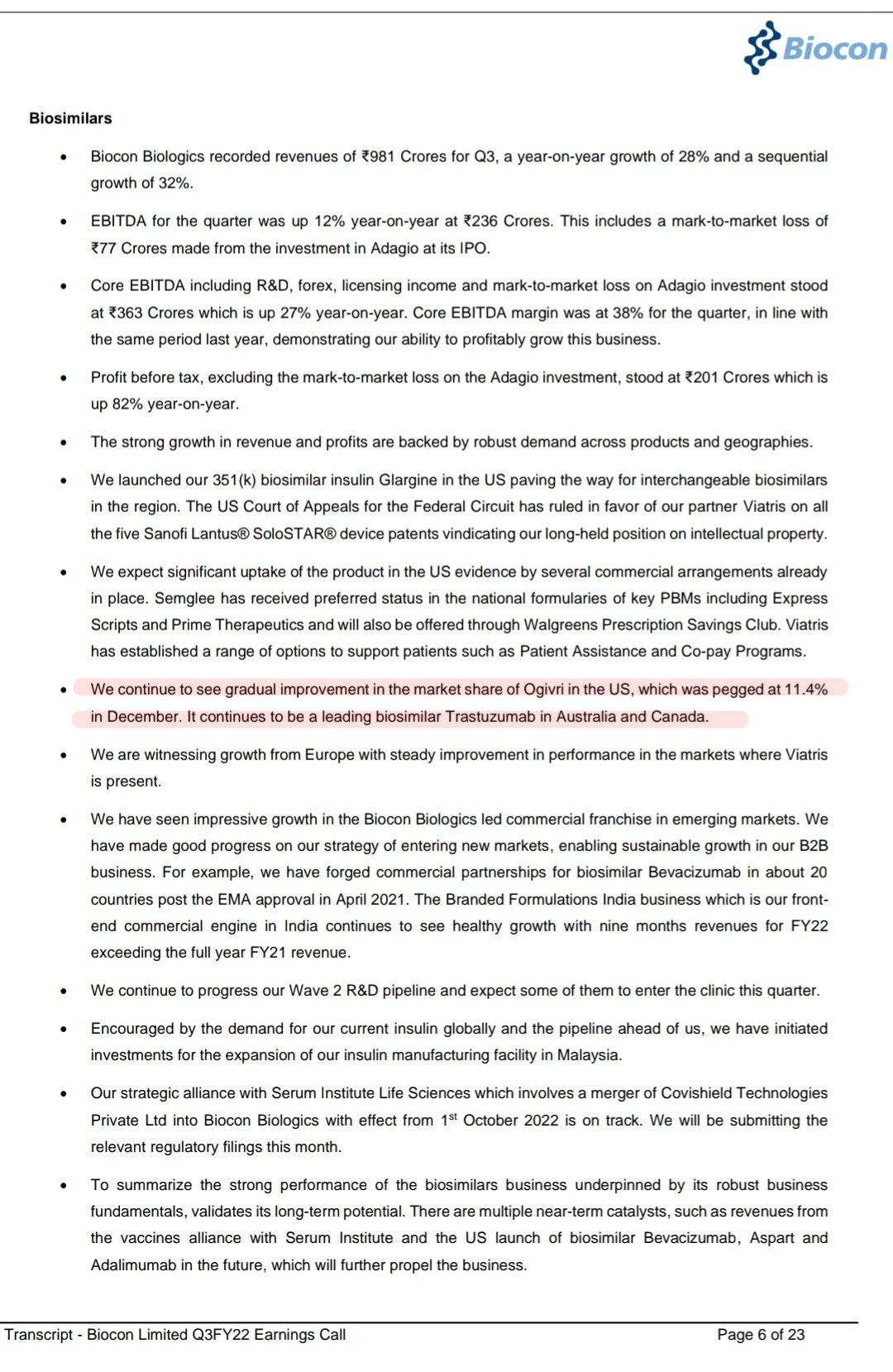

Ogivri of Viatris has a market share of 11.4% in US within a space of 5 biosimilars and total of 60% biosimilar market share.

Amgen’s Kanjinti is the market leader here.

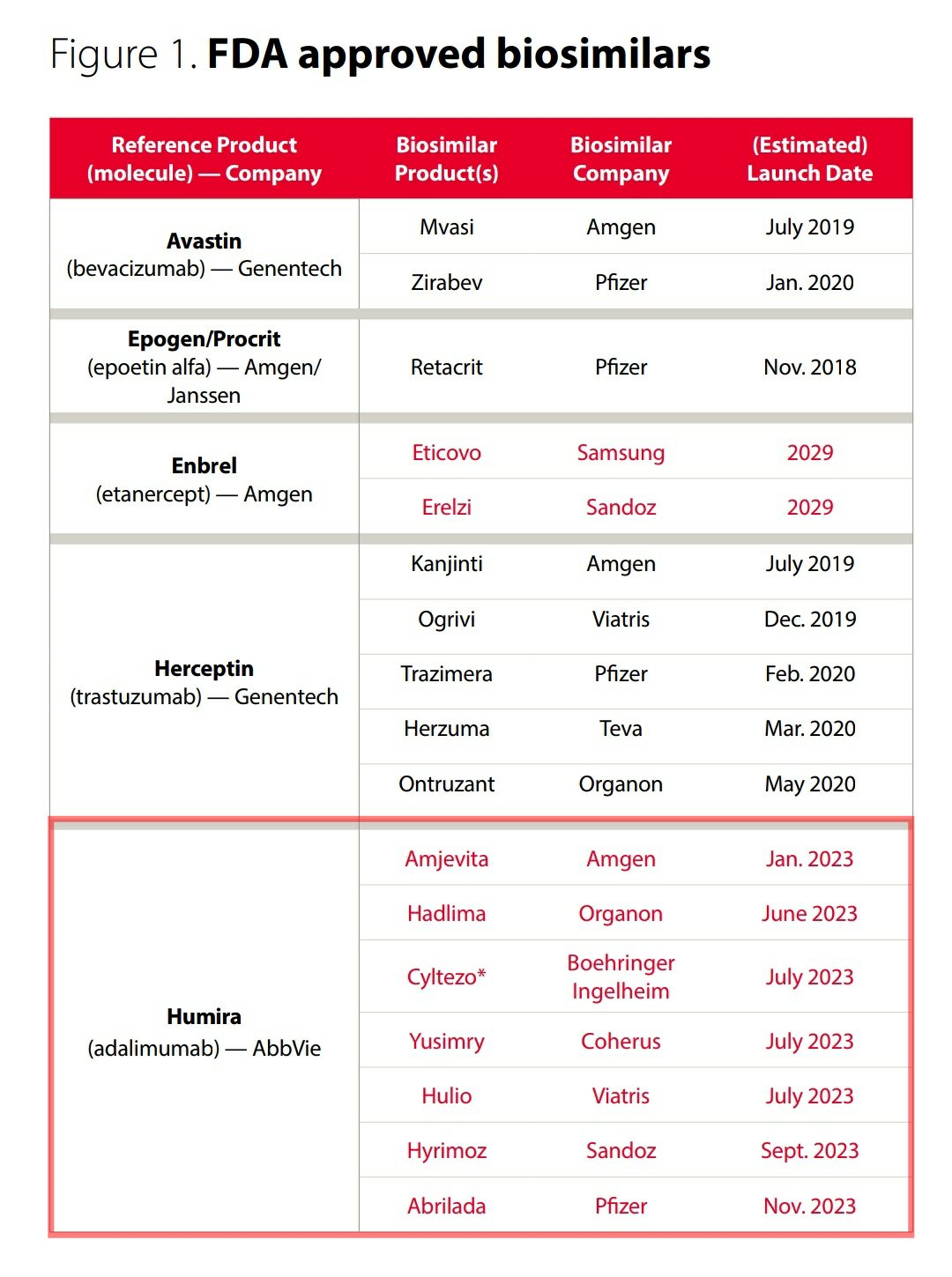

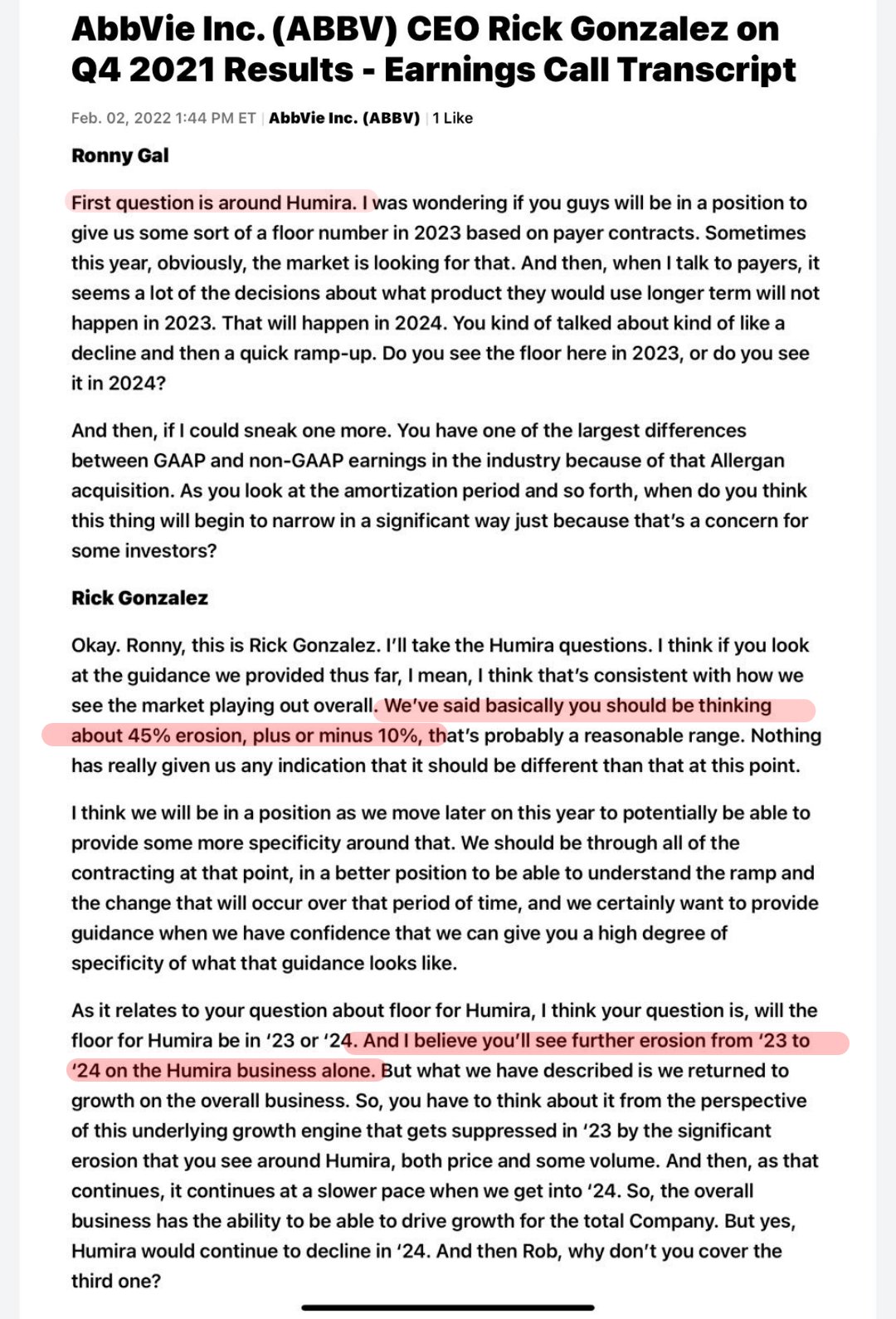

In Adalimumab (Humira) biosimilar space, 7 players have got approval and all of them will get commercialised on 2023 when patent expires for Humira.

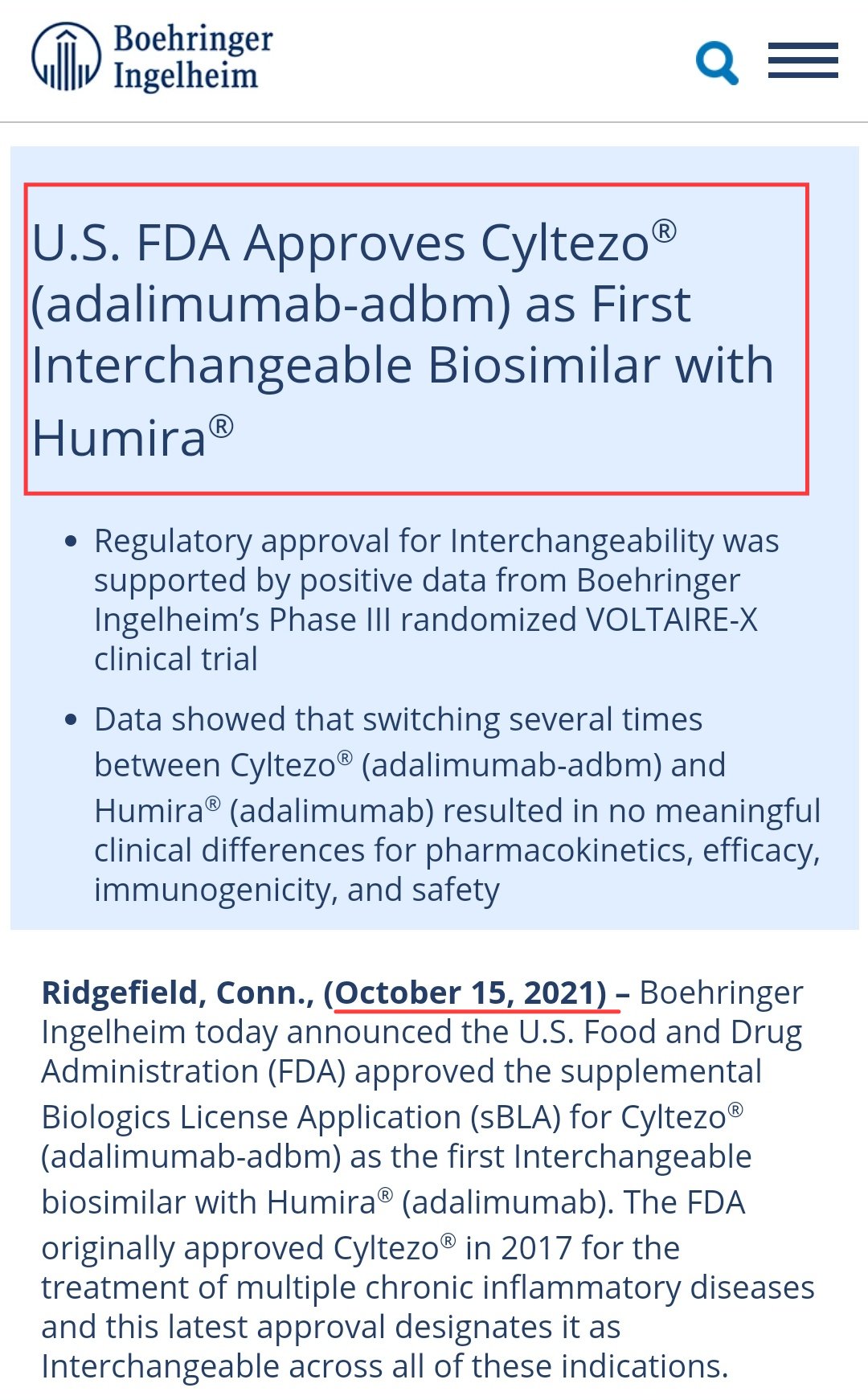

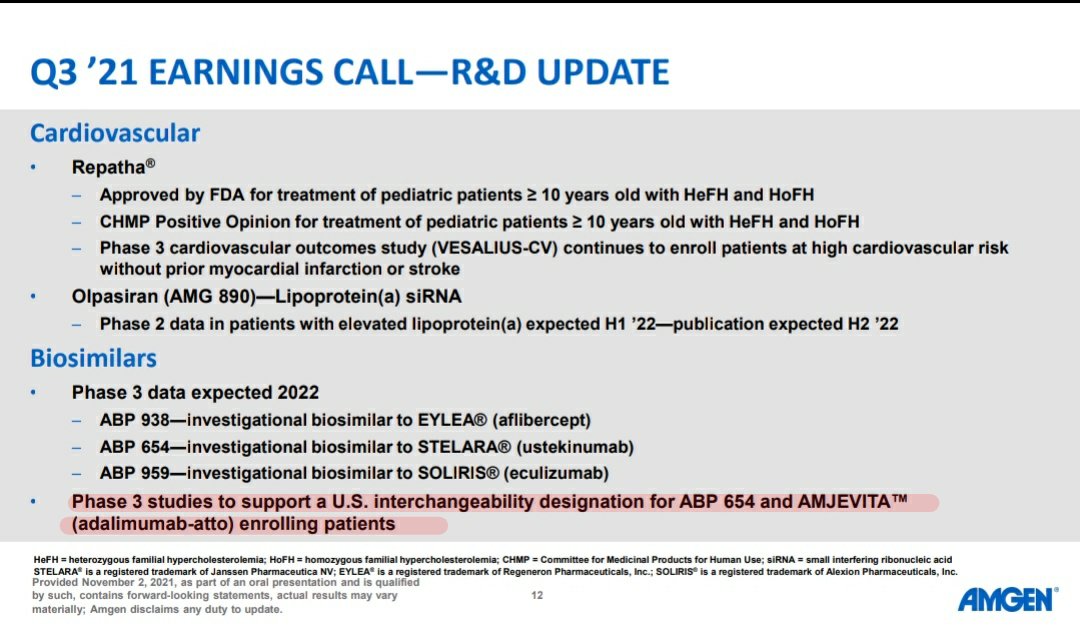

Among those players, Cyltezo has got interchangeability approval on 2021 and Amgen is near to get that status.

Interchangeability status may help them to get good market share even during intense competition.

There will be intense competition among 7 biosimilars and Humira.

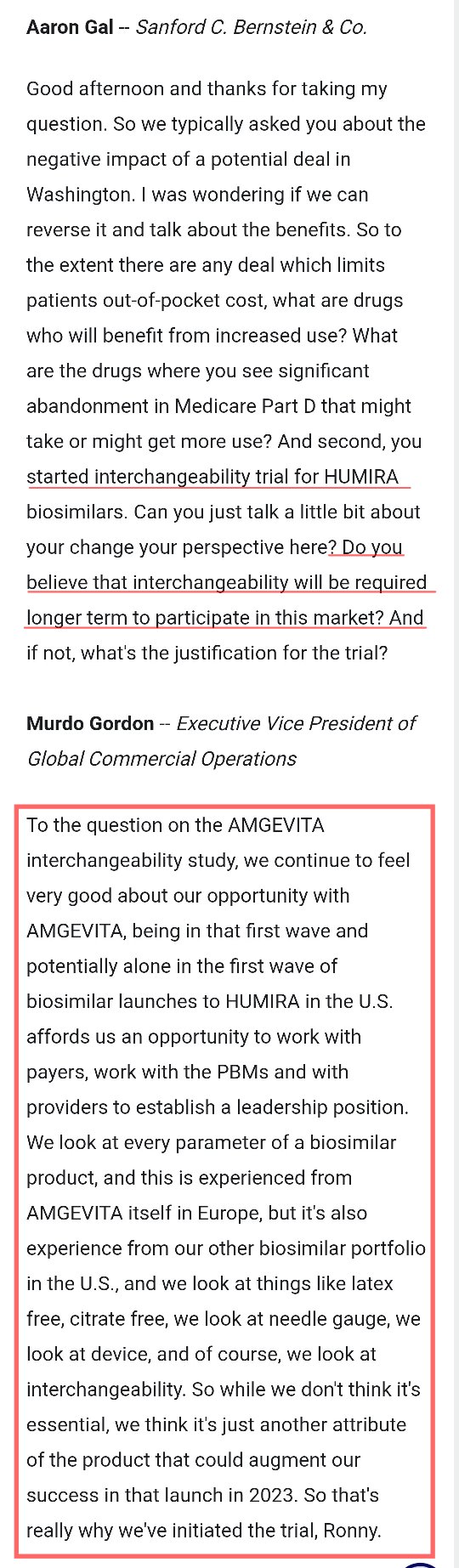

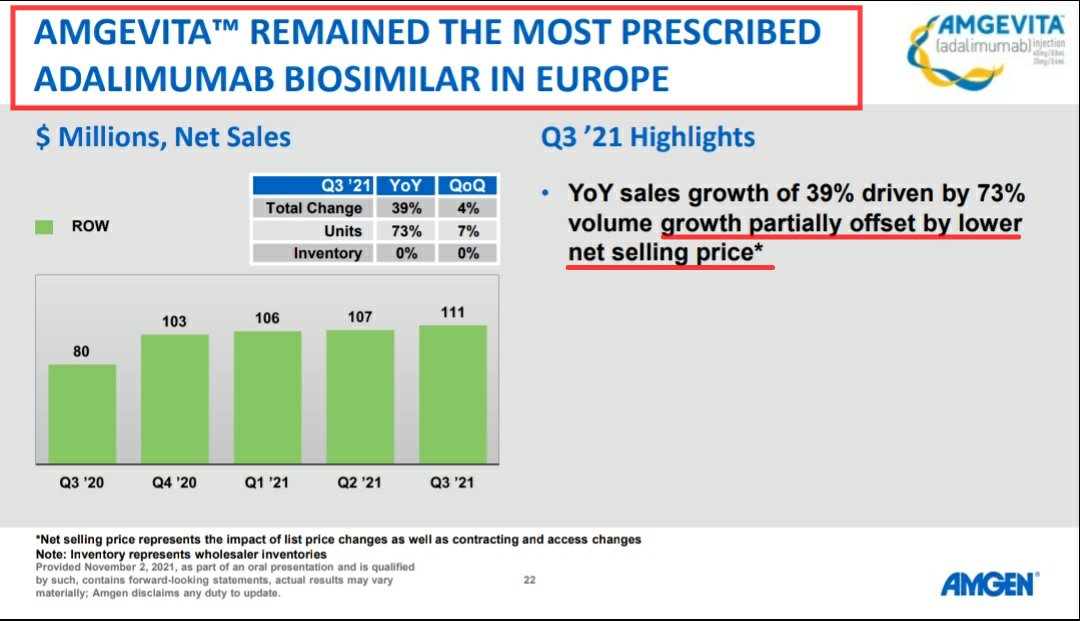

Amgen tries to differentiate their product Amgevita (Adalimumab biosimilar) with

Latex free, citrate free preperation

Finer needle gauge

Interchangeability status

Amgevita has got leadership position in Adalimumab biosimilar space in Europe. They might replicate that success in US also.

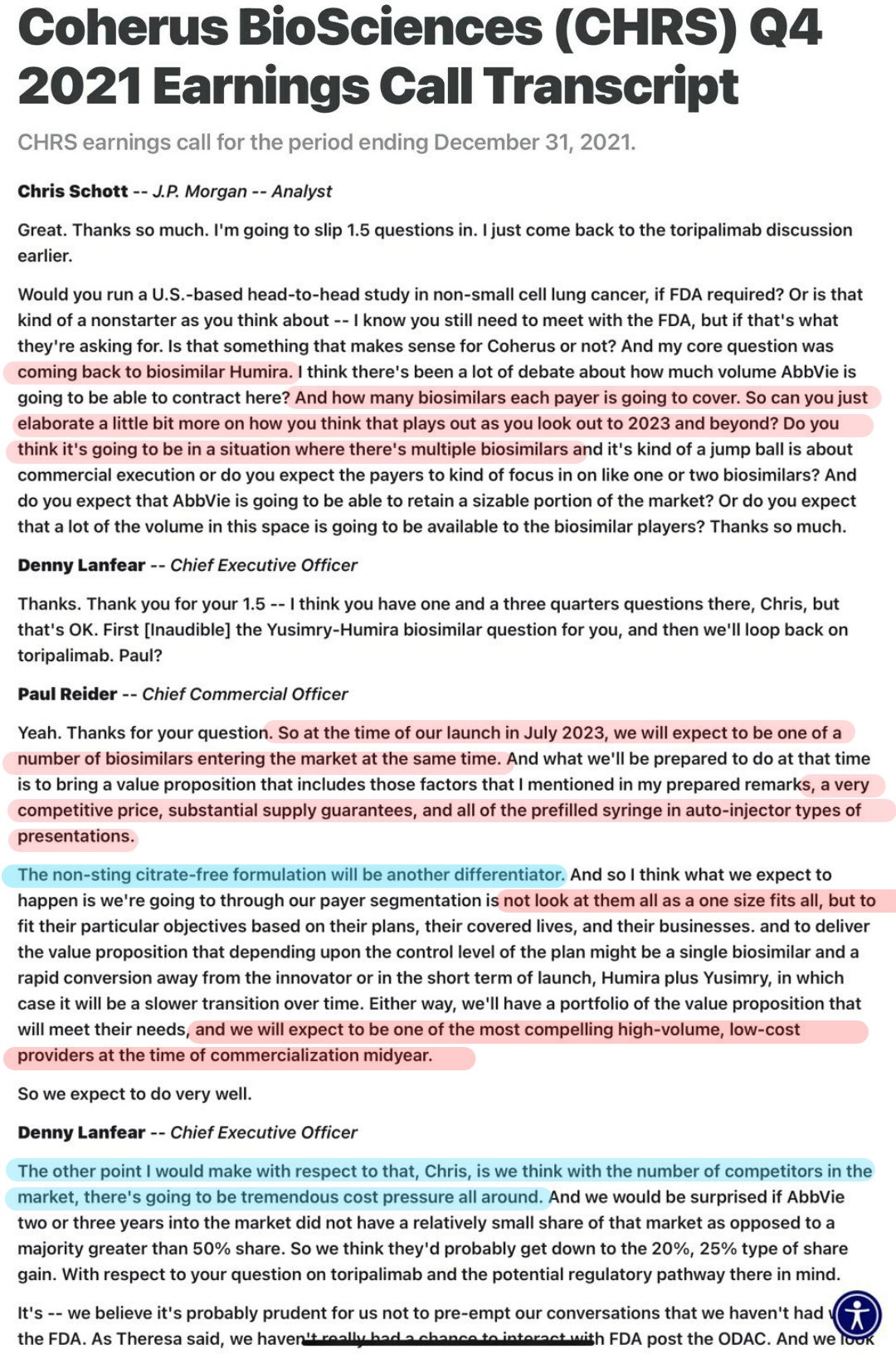

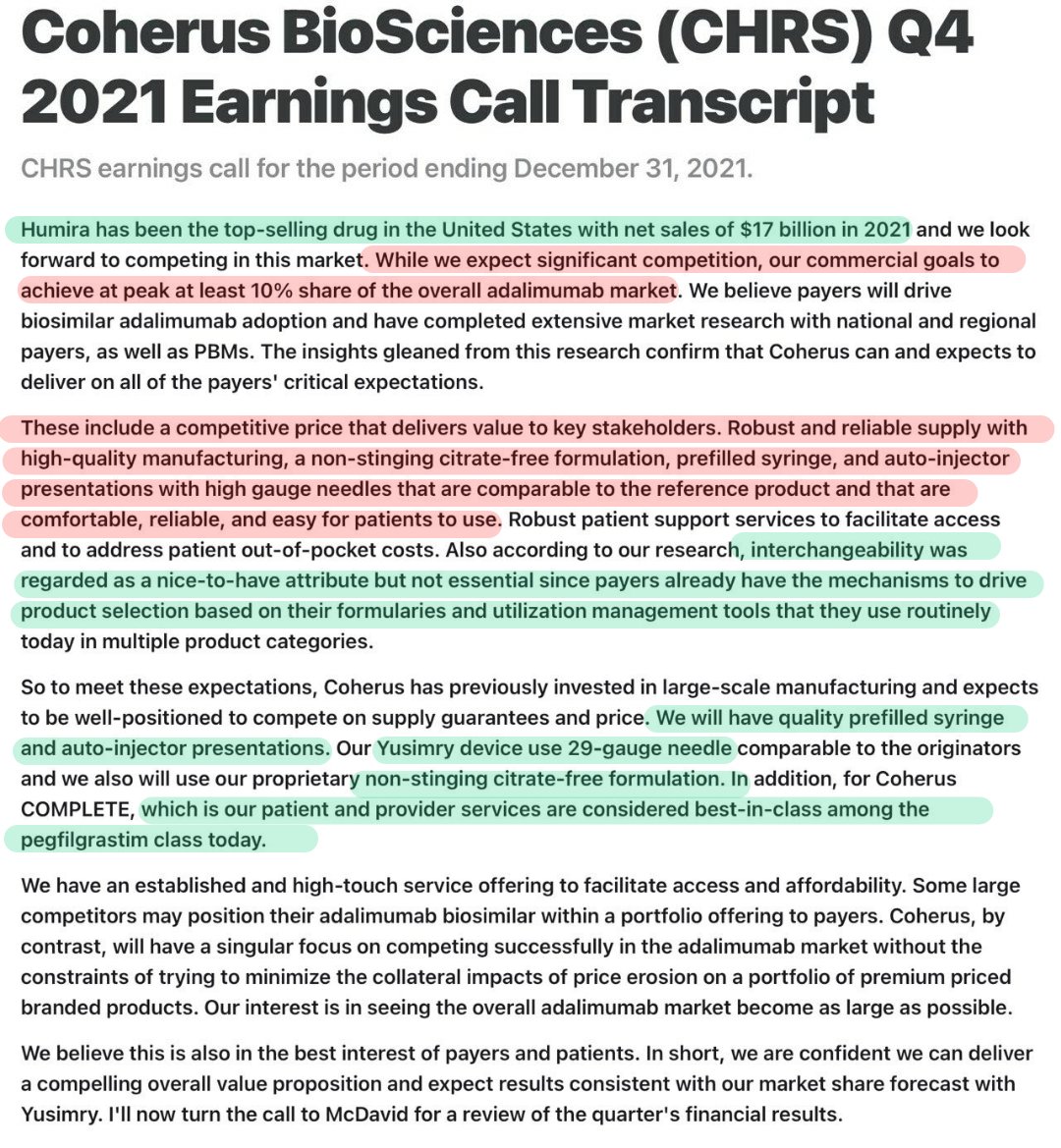

Coherus tries to bring value proposition with

Very competitive price

Substantial supply guarantees

Pre filled syringe (PFS) with auto-injector

Non stinging citrate free formulation

29gauge fine needles.

Humira had citrate in their formulation-injection was uncomfortable for the patient.

Coherus has developed proprietary non stinging citrate free formulation -greater comfort for patient.

29 gauge fine needle-less pain

Differentiating features helps to face fierce competition

In Humira (Adalimumab) biosimilar, there is total of 15 players preparing for that, 7 players already got approval and competition is expected to be fierce.

80-90% price erosion may happen.

Others are developing differentiating features to face competition.

What will be the differentiating feature for Viatris?

Where will it stand in this competitive space?

I couldn’t find any differentiating feature for Viatris in Adalimumab biosimilar space. (Can any of you point that out to me, if you find any details in past earnings call or presentations?)

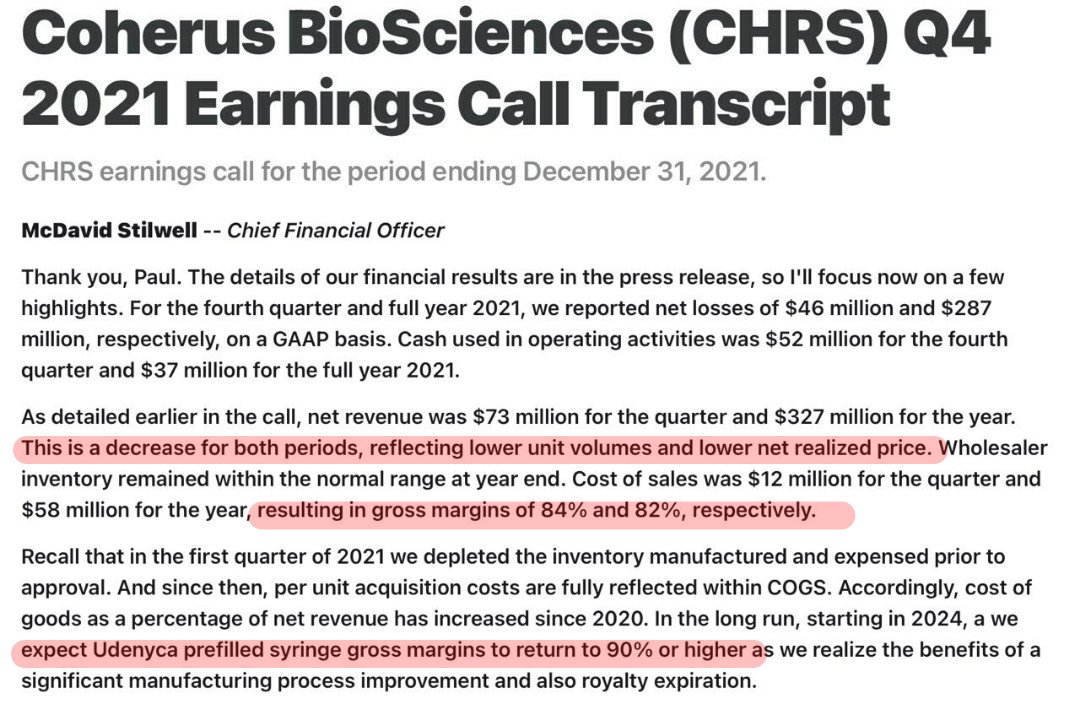

Coherus had gross margins of 84-82% in Udenyca (Pegfilgrastim biosimilar) with leadership position.

I don’t think even Biocon has this much gross margin. (Kindly share info if this is wrong)

And Coherus continue to be in leadership position in Pegfilgrastim biosimilars.

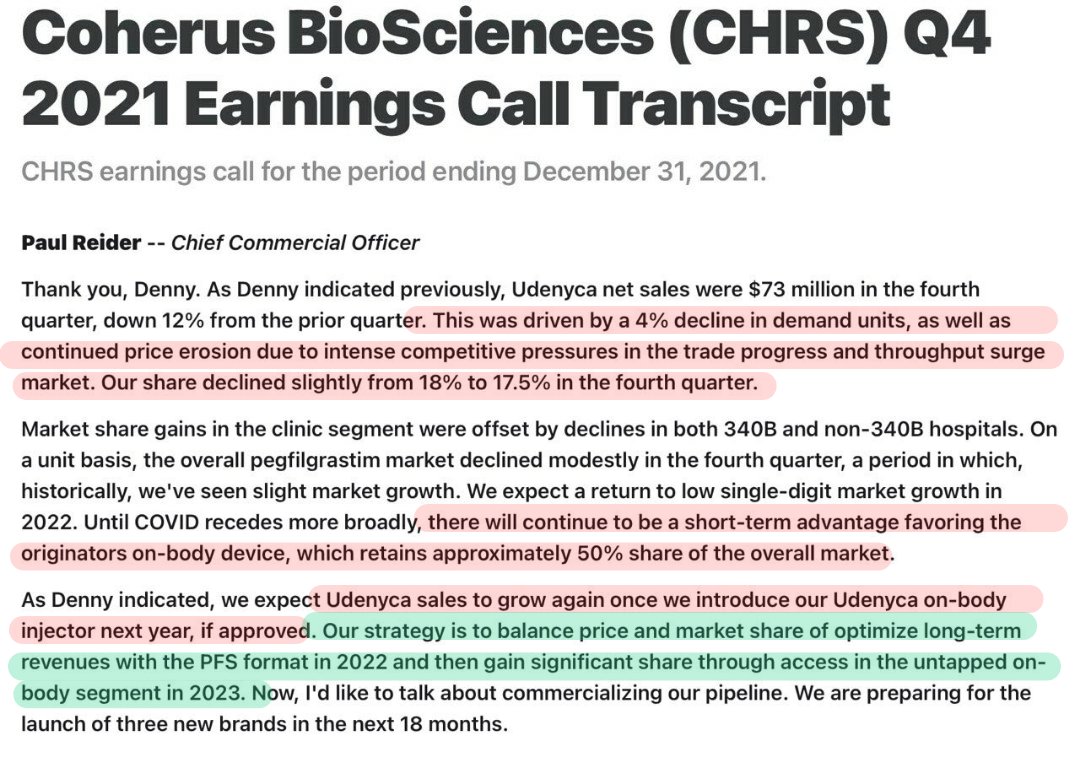

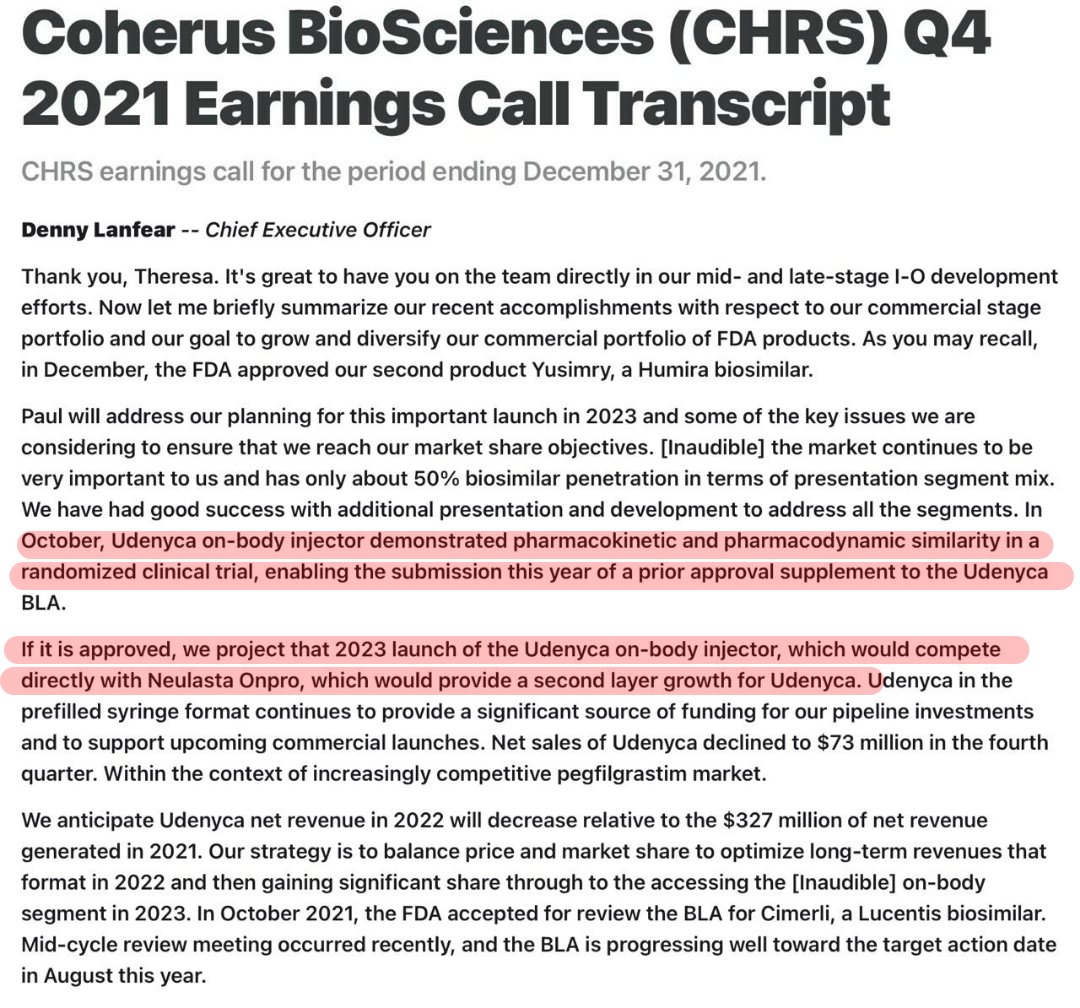

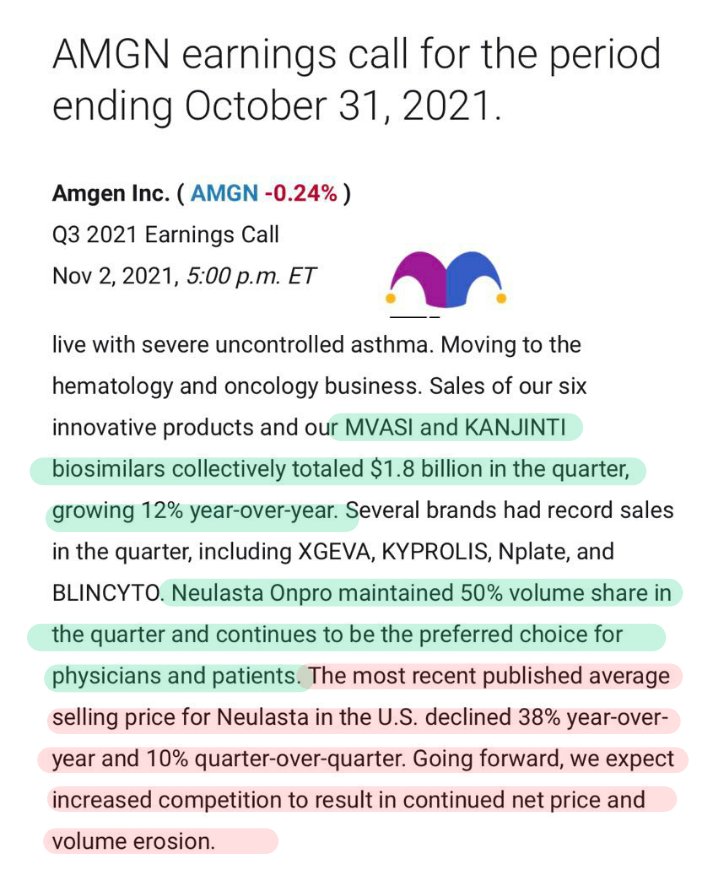

Coherus is planning to launch on-body-injector in 2023 which will compete directly with Neulasta Onpro(50% market share) to gain further market share.

Amgen expects severe competition against Neulasta and expects net price and volume erosion.

Despite having early mover advantage, Viatris (Biocon) have only 8-10% market share in both Ogivri and Fulphila.

As more players enter the market, competition will become much fierce, results in price erosion & decline in margins just like in generics.

Is Biocon the lowest cost producer? Their margins doesn’t say so.

Needs to be seen how this unfolds.

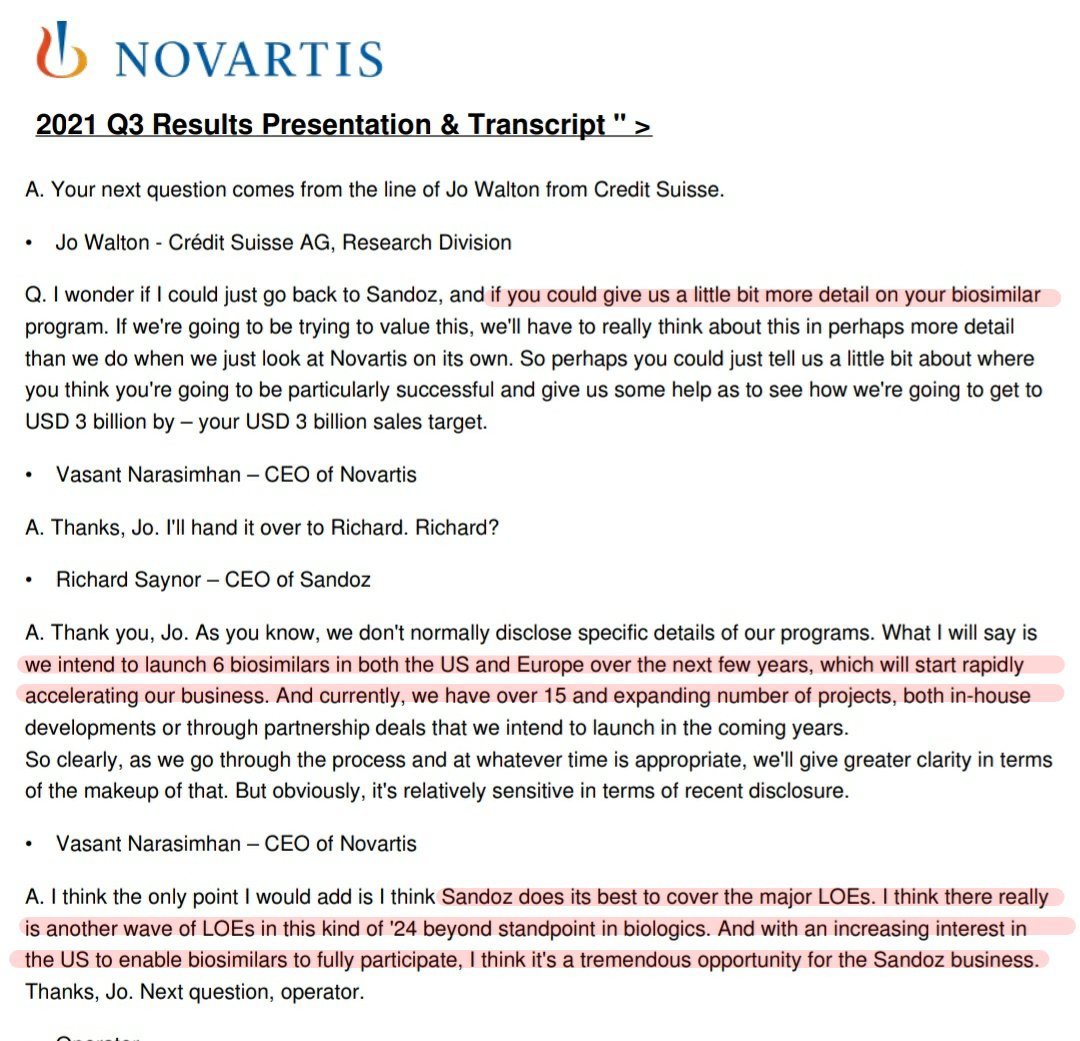

Earlier they had CDMO partnerships with players other than Viatris. (Libbs & Sandoz)

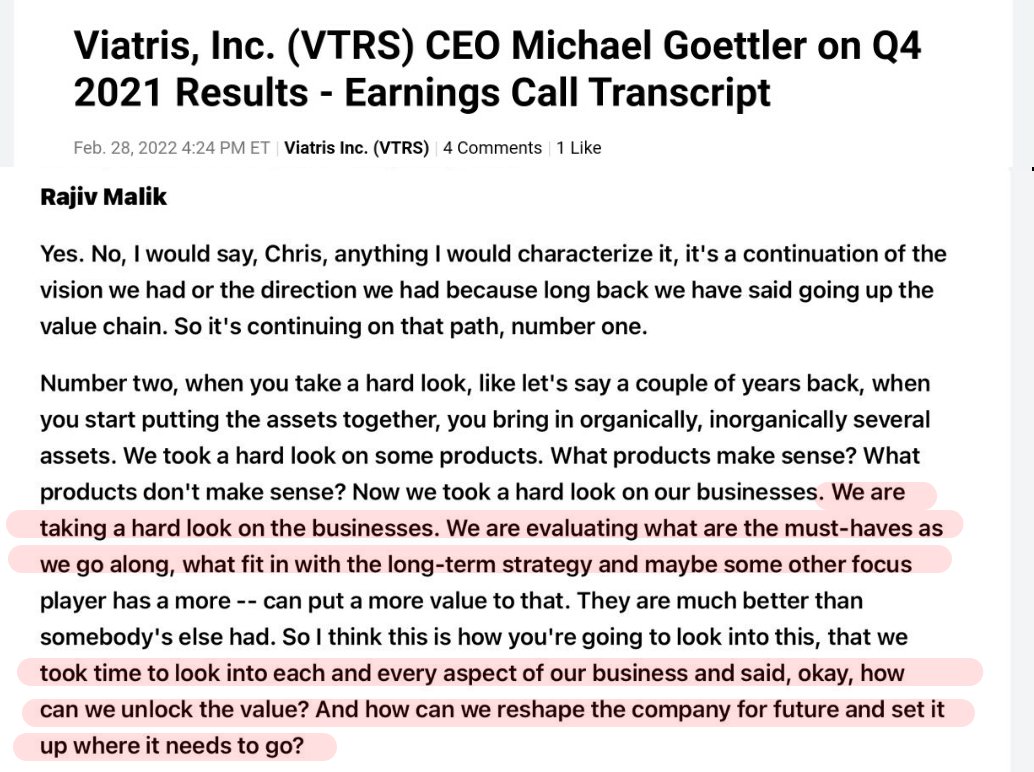

What will happen to their CDMO opportunities now as biocon has become a competitor to them as they have acquired Viatris & become a fully integrated player.

For the next 2 years they will get transitionary services from Viatris for a fee, Rajiv Malik will work for them for next 2 years.

What will happen after 2 years?

Will they have enough commercialisation marketing capabilities & leadership capabilities like competitors?

These questions need to be answered.

I think it was a very good deal for Viatris at 16.5X EBITDA multiple. Biosimilar space is getting very competitive and average selling price, market share and margins may decline with fierce competition.

What are your thoughts, senior members of this forum?

I have been tracking biosimilar developments in US for the last 2-3 years and can share my observations. In the beginning when there was no clear cut pathway for biosimilar marketing, selling a new biosimilar molecule was almost equivalent to a speciality generic molecule, where companies required doctors to directly prescribe their version of biosimilar. This was in stark contrast to marketing generics where interchangeability happens at pharmacy level, which means that gaining market share is relatively easy. With the recent interchangeability of insulin glargine, this might change and biosimilars are likely to go down the generic route, where gaining market share is directly a function of price and relationship with a PBM.

Now coming to Biocon, there has always been a lot promise due to their large pipeline and early mover advantage. However, they have almost made no usage of early mover advantage. In the beginning, Biocon struggled against the likes of amgen which had a better doctor connect. Then they have struggled in terms of pricing where competitors (including Amgen which is an innovator) have underpriced them. Lets look at it through market share of individual molecules.

Pegfilgrastim: Biocon got to 9% market share in June 2019 and since has been struggling. This is despite the fact that biosimilar market share has increased from 22% in June 2019 to 37% in June 2021. Over this time time period, all the gains have been made by newer players and Coherus.

Trastuzumab: Biocon got to 8% market share in a few month and has since been struggling. Amgen has been fiercely competitive and gained market share. The total biosimilar adoption has increased to 52% here.

Glargine: Biocon currently has 3% market share even after >1 year of launch. Their market share should increase as they have supplied and booked large revenues this quarter. However, given their past track record, I don’t know if they can get to a 20-25% kind of market share. Getting to a 20-25% market share is important to have optimum utilization of manufacturing capacity, also this kind of market share leads to better pricing with PBMs.

Pricing pressure trends: Biosimilar market has been a bit unusual in terms of pricing pressure where even when there is no new player, incumbants go for price cuts every quarter. The kind of pricing pressure seen in biosimilar in 3-6% on Q-o-Q basis which is even worse than generics. My own thought process is innovators want to capture the biosimilar market as they have been unable to bring new molecules in market, so they cannot simply let the biosimilar market go to manufacturers that operate out of a cheaper geography.

What I have struggled to grapple with is why Biocon is not more aggressive on pricing. Even in India, Biocon has struggled to gain market share against Cadila. I think they lack seriously in their marketing capabilities. Also, I don’t understand as to how taking over the marketing unit of Viatris leads to more synergy as this is the same marketing unit that couldn’t get double digit market share in trastuzumab and pegfilgrastim after 3-years of launch. Also the price paid is quite significant for a simple marketing entity (4x EV/sales vs 1-2x EV/sales paid by other generic companies recently).

All this said, I think strategically it might make sense for Biocon as they have bet almost everything on biosimilars. Its going to be a binary outcome for them as balance sheet will be very stretched now.

All the graphs are taken from an Edelweiss report, its a must read to get a good understanding of pricing pressure in US biosimilar market.

https://www.edelweissresearch.com/Research/Download/13828

Biocon has always been known as R&D led organisation and not Marketing led Organisation .

Customer orientation of right pack size , delivery mechanism , pricing and tactical sales promotion is required in competitive drugs.

Now Mylan was superior to Biocon in Marketing ( sales & distribution ) and hence Biocon tied up with them … But somehow it had not worked out …

The logic of buying same unit of MYLAN with all its people and culture and make them work under Biocon will be even more difficult . I see huge execution challenges in integration of two diverse cultures .

Any way at some time Biocon had to get its hand dirty in Sales and Marketing if it was play generic and biosimilar game … Biocon now will be very long term game > 8 years … as it is embarking on very new journey …

Yes Biologic IPO is game which Biocon wants to play but in current market environment it is some time way

Good insights on changing industry landscape driving consolidation and exits

My submission

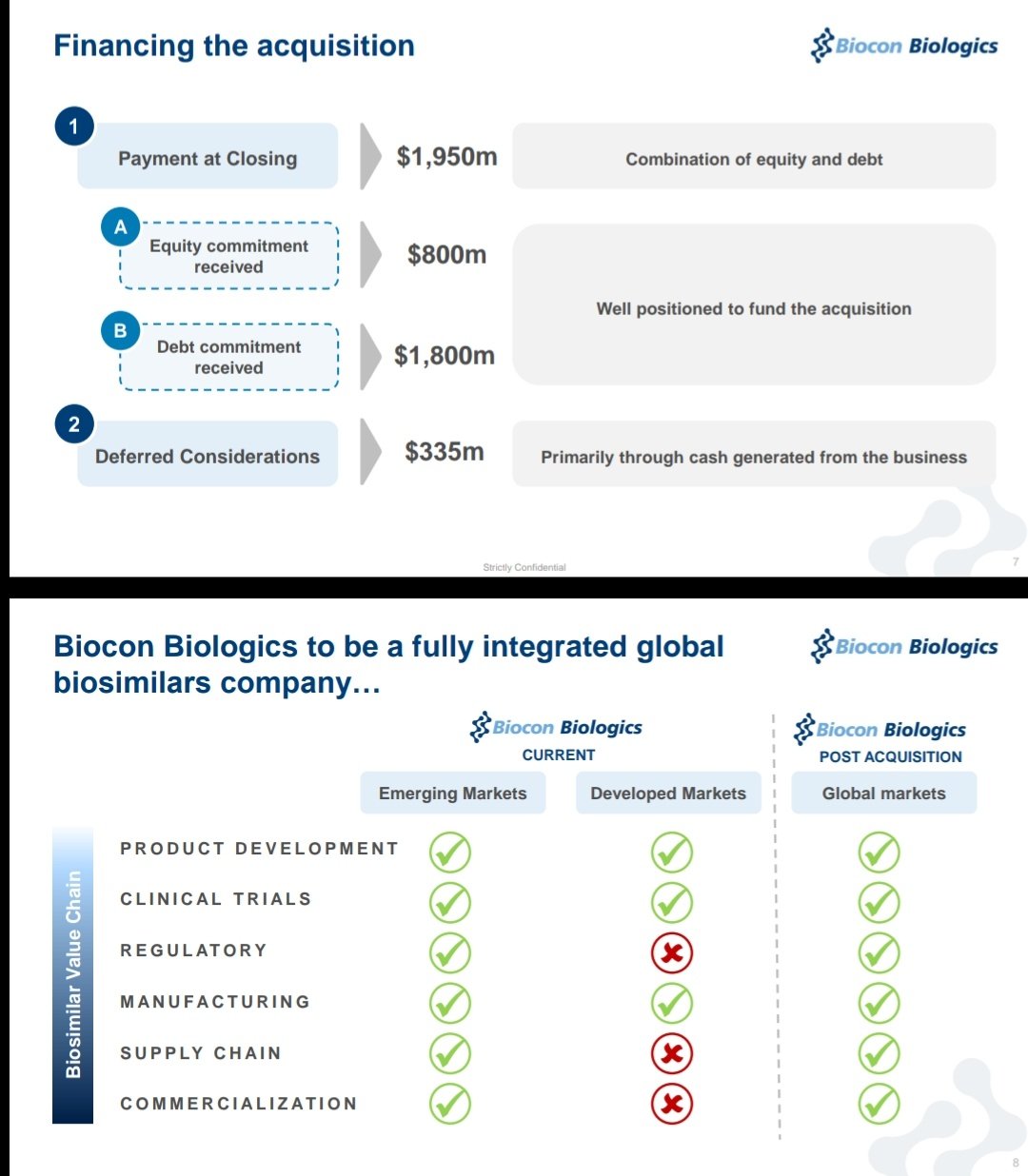

It’s a no choice scenario for Biocon to play binary game with deep skin in game, get IPO done at any cost, build scale to fight at cost basis and be last man standing, and they have taken a bold decision. Kiran has been vocal about ambitions on commercial capability building. What valuations they paid is different matter( in their minds they have already bumped up biologics at $8B valuations via this deal, and have funding committed from existing investors as well). If India mkt is not appreciating, they have options of global listing as well.

Valuations- beside debt profile perception( which will look like 5X EBDITA of combined entity), things for biosimilar unit may actually look very different in FY 24( Approx and basis mgmt commentary, rather than real execution)

4500-5000cr EBDITA is a possibility. Does $8B+ valuations justify it - very subjective. Doesn’t look out of line either for a sunrise sector.

Risks - Lot of uncertainty, excecution succes to be seen, multiple M&A to be digested, IPO still away, Consolidation and comptetion aggression visible.

Doubt if it’s the opportunity for retail folks given lots of other opportunities available in current mkt conditions, deep pocket guys probably like such cases -will be visible on how funding shapes up.

Edit - take on market share and lack of aggressive price by Biocon- think( pure hypothesis)answer lies in partnership construct so far, Bicon was working on cost+ basis with Viatris and some profit share, Viatris was also making margins on same inputs, thus end price always was function of two hops. In reality the sales culture end of day is commission driven, Viatris didn’t have free hand there given lack of control on landing cost which needed to have Bicon margins protected. Biocon on other hand needed volumes to deliver healthy performance, which was missing with Viatris aggression limited by construct. Q2 and Q3 Biocon biologics margin establishes volume success part, full control on sales engine to increase market share should reflect in upcoming quarters if acquisition is well though of and executed.

I for one have tracking positions with stop loss, would like to see how it plays out over next few qtrs, do believe that Pessimistic scenario is built in at current price.

Hi

Biocon is 5th largest holding in my PF.

Can someone help me understand that by listing Biocon Biologics how will value be unlocked for existing shareholders ?

I am looking forward to the results this year - Insulin glargine sales in the USA will be significant this year.

It will be interesting to see the contributions from the biologics business bought from viatris.

2022 will be a successful year for biocon in terms of financial performance of their business - that is my guestimate…

Discl - holding and adding since 2016

Topline/revenue was very good but PAT was negative due to exceptional items - their business has become complex, exceptional items should be normalised from now on.

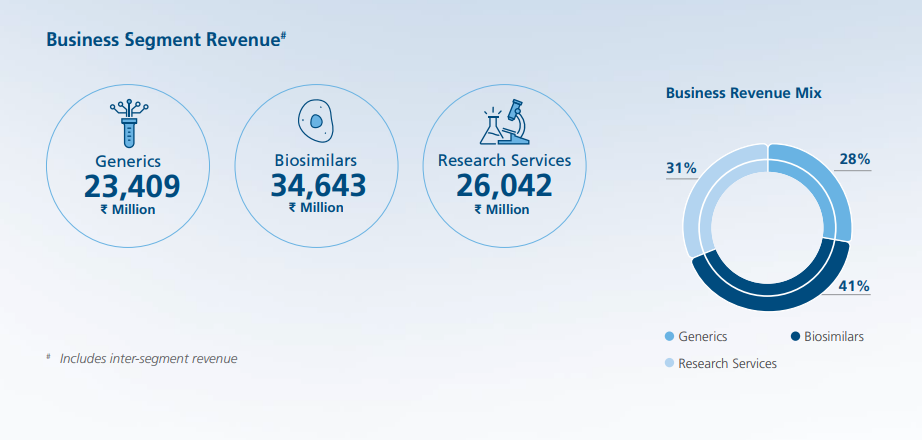

Q4 investor presentation.

Nice pick up in all three verticals - biosimilars, generics and research services. However, the valuations continue to be rich.

Disc : invested, biased.

I see that Biocon had non current borrowings of Rs.2961 crore at the end of FY21 and Rs. 3998 crore at the end of FY22. However, the financial cost for FY22 comes to only about Rs.67.6 in P&L. That seems very low for the quantum of borrowing they have done. Are they capitalising interest cost? If so how to figure out the exact interest outgo?

Latest interview of Ms Kiran Majumdar, post Biocon and Syngene’s Q4 results. Lots to take away.

She is guiding for double digit growth in generics, mid teens growth in research services and north of 30 pc growth in Biosimilars. Will be interesting to see if these numbers can be met.

Disc: holding both - Biocon and Syngene. Biased.

At Cusp of growth both biocon and Syngene

Serious allegations against Biocon Biologics. CBI accuses Biocon Biologics associate VP L Praveen Kumar of paying bribe to Joint Drug Controller CDSCO to waive phase 3 trial of insulin Aspart injection.

“The CBI has alleged that executives of Biocon Biologics were trying to exert undue influence on officers of CDSCO under the Directorate General of Health Services, Ministry of Health and Family Welfare, to waive the phase 3 trial of 'Insulin Aspart Injection”, officials said.

“It was alleged that they agreed to pay a bribe of Rs 9 lakh to Reddy for “favourably processing” three files related to Biocon Biologics and also to favourably recommend the file of “Insulin Aspart injection” to the Subject Expert Committee (SEC) meeting”, they said.

Response from biocon biologics.

Reply from Biocon on false allegations

Biocon notification to the stock exchange

“The U.S. Food and Drug Administration (US-FDA) conducted three on-site

inspections of Biocon Biologics’seven manufacturing facilities spanning two sites

in Bengaluru, India and one at Johor, Malaysia. These inspections started with the

Bengaluru site on August 11, 2022 and concluded with the Malaysia site on August

30, 2022.

Outcome: The agency issued form 483s with 11 observations each for the 2 sites in Bangalore and 6 observations for the site in Malaysia

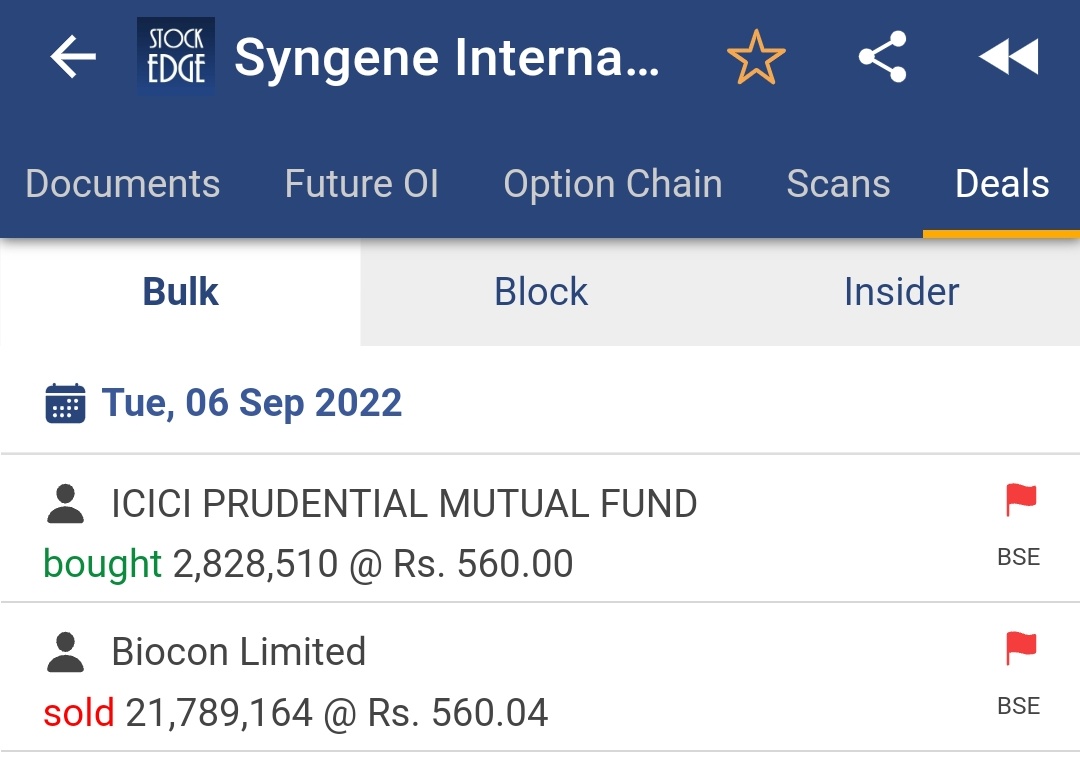

“Biocon is likely to sell a portion of its 69.99 percent stake in Syngene, sources have told CNBC-TV18.” Link

Biocon have mentioned in the past that, they would fund the Viatris deal with debt & equity commitments. Seems like, they are now forced to sell their better business (Syngene) to fund comparatively inferior, cash burning business. (Biosimilars)

What are your thoughts, fellow investors & veterans?

Update:

BIOCON notification to the exchange

“This is to inform you that the European Directorate for the Quality of Medicines & HealthCare

(EDQM) conducted a GMP inspection of an API manufacturing site of Biocon Limited in Bangalore

from the 12th to 14th of September 2022 and issued a list of deficiencies on 5

th October 2022. There

were no critical deficiencies and one deficiency cited under the category ‘Major’. We will be

responding to the agency with appropriate corrective and preventive actions within the stipulated

time. Biocon remains committed to the Quality, Safety & Efficacy of its products.”

Off late, we see many such repeated observations on their manufacturing facilities across various global locations. Is Biocon losing the sheen and not focusing on the quality aspects in chase of volumes?