Biocon Q3 show was strong on all fronts, 2nd consecutive quarter of strong performance by Biologics and signs of generic turnaround, outlook commentary good as well,

Q3 concall a must listen for understanding direction better

Key highlights from concall

- Q3 21 2200 cr revenue, pbt reported at 269 cr = 350 cr excluding mtm losses for Adagio - annualized 8-9K cr revenue, 1400 to 1500 cr pbt. PAT in range of 1200cr+ range

- per mgmt estimations Serum deal to contribute $400 M revenue at full utilization with margin profile similar to core EBDITA- ramp up from H2 23, mgmt says aggressive in commercialization- that is as big as current whole Biologics division - need to be conservative in estimation here give past track record

- Biologics firing on all fronts- mkt share gain, Interchangeable status boosting performance and best is yet to play out, Sandoz pipeline to be announced soon as next phase of growth , Serum deal to contribute in H2 - con call has finer details

- Grnerics new launches doing well, Vizag facility coming online and contribute from FY 23, still seeing cost pressures but sequential improvements visible

- Syngene on its own doing well, raised guidance a bit

- Opportunity size was never issue, biologics /biosimilar as well as CRAMS are a theme for deacde + , long runway but uneven stock performance driven by mkt expectation mismatch

- Biosimilar price erosion is sane in developed mkt and holding better than expectations in emerging mkt

- New leadership appointment are in right direction with signs of better control on mkt facing/commercial destiny( e.g. Head of BB commercial- DM, India branded Head etc)

All in all, mgmt sounded at offense than defense in past many Qtrs, technicals supporting turnaround after near 1-2 years of underperformance, valuations look decent considering future triggers, breakout on weekly and daily charts with volume.

Valuations

- Biologics- Q 3 at 981 cr, EBIDTA at 313 cr, 28% YoY and 30% QoQ on topline, primarily driven by following

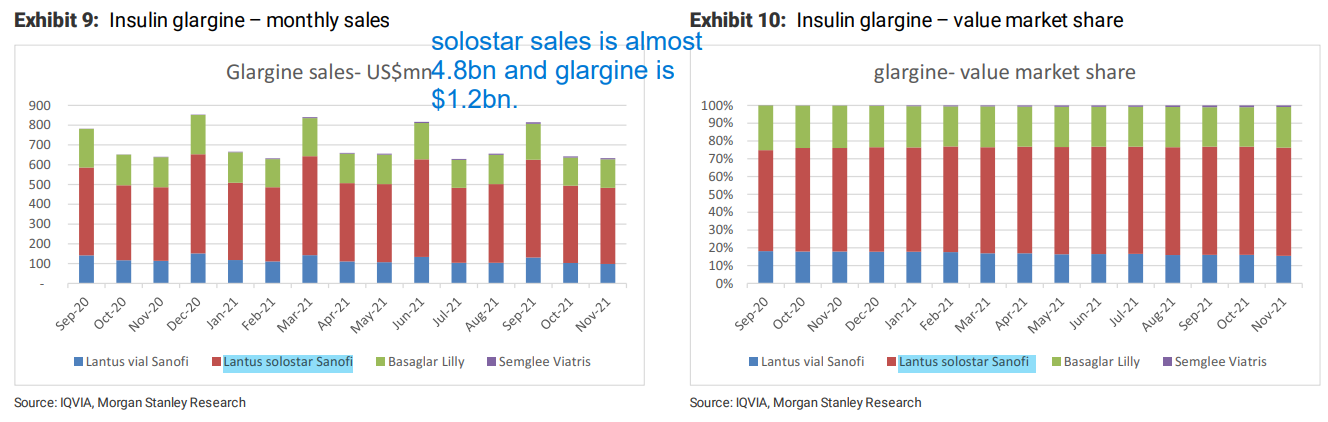

- Glargine supply to Viatris contributed this Qtr, trigger of profit share is yet to play out when Viatris supplies in end markets. Glargine has two launches - Branded as Samaglee and unbranded as Insulin Glargine. Branded profile bound to have higher margins, Interchangeable benefits and preferred status over Lantus to also reflect in numbers.

- Continued to maintain a steady market share for bTrastuzumab (Ogivri*) in the U.S. and

bPegfilgrastim (Fulphila**) in the U.S. and key EU countries

-

Ogivri mkt share gains in EU helped them in this Qtr

- Fuphilla approval in Canada to help in coming Qtrs

While they do not give guidance we know that biosimilar grows healthy as mid teen, new launches and preferred status, Profit share gains and better than expected pricing in emerging mkts - they can continue to deliver similar growth as last two qtrs for 1-2 years. Pending approvals of Aspart and other upcoming ones ( with Sandoz) to keep pipeline healthy.

At Q3 annualized, biologics biz is 4000 cr topline 1250 cr EBDITA, 25% growth, let’s add Serum( H2 23 onwards) $400M and $120 M numbers - 3000cr revenue and 1000cr EBDITA.

How much one pays for an innovative biotech with revenue 7K cr+ 2250 cr+ EBDITA - Serum merger happened at $5B valuations but with future potential this biz could be way higher - samsung biologics at $1B+ sales is valued at $45 B ( of course much higher growth metrics)- on continued performance delivery Biocon biologics on its own have significant room for rerating here on. Even at 25X EBDITA 60k cr type number - ofcourse Pre conditions being ability to commercialization of Vaccine capacity ( serum) and steady growth from BB. Market being forward looking some rerating should play out in next 2-3 qtrs.

- Syngene is listed at 25K cr, at holding co discounts(40%) one can factor in say 16K cr- it’s in middle of sizable Capex and results to show in FY 24 onwards including Mangalore facility.

- Generics is a crowded space and will get standard peer based valuations- at annualized 2500 cr revenue at 8 - 10K cr range. New API facility trigger and Tabuk pharama tie up to help in ME.

- High risk reward of novel molecules not added as buffer

All in all 25K cr( Syngene + Generics), Biologics at last round was $5B - likely to get rerated based on execution to 60Kcr by end on FY23 based on success in core biosimilar + Serum vaccine capacity commercialized at healthy Financials

Posiibility of 80-100K cr mkt cap against 45K cr now. This is back of envelope and could be wrong. Mgmt has missed guidance etc in past and things usually take longer to materialize in this industry compared to others, entry price and MoS is key.

Risks

- Recent past underperformance of business post corona, though all facts suggest worst is behind

- Capital intensive business, compliance risks of pharma

- Investment for those okay with industry nature and sizable period of flat/underperformance , these are not secular compounders( key learning)

- Pharma Sector not in favor currently ( more of a factor of mkt momentum than biz)

Invested and added recently