4 Likes

-

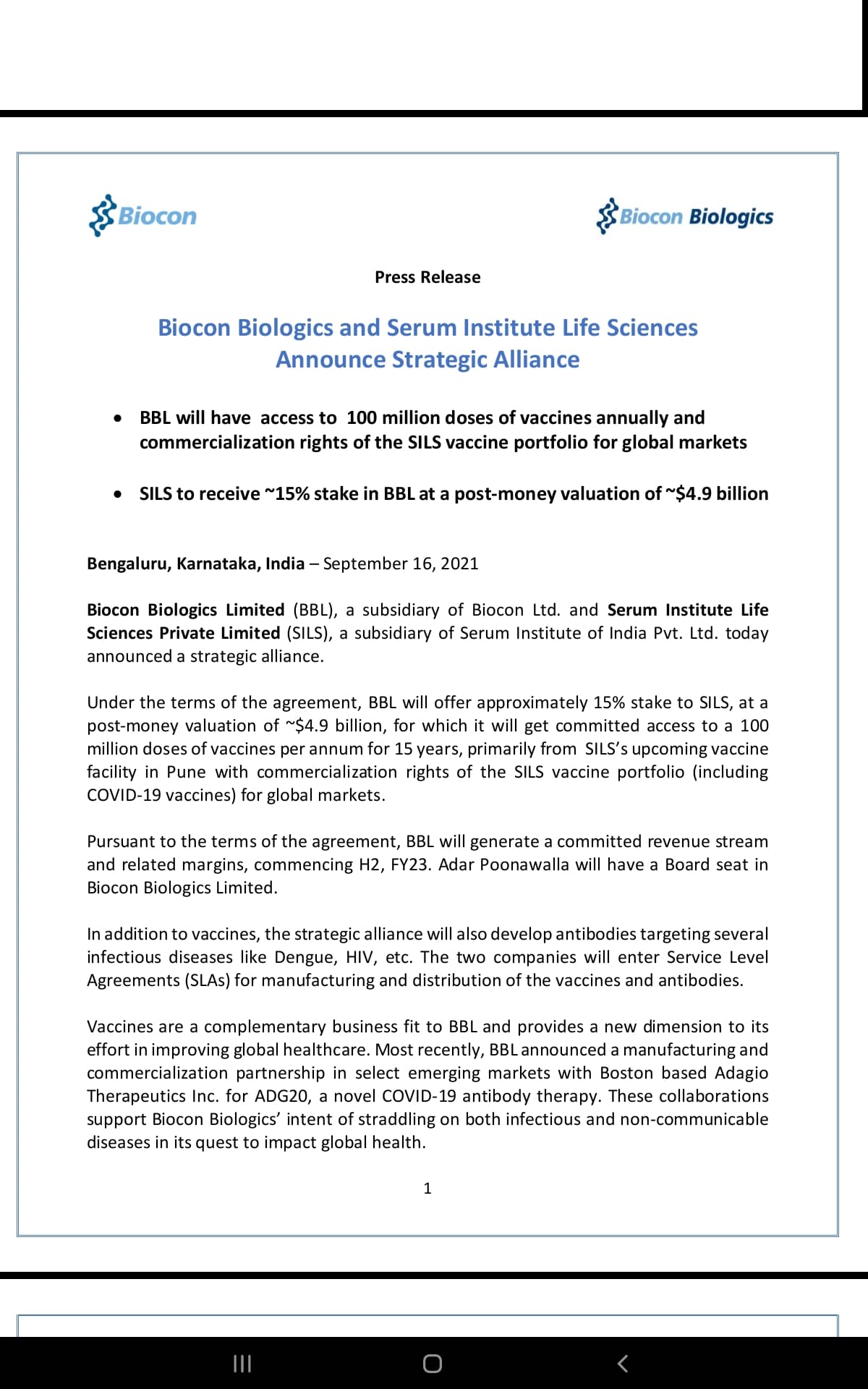

Two of finest biotech corporate houses coming together and complementary alliance

-

$4.9 B valuations for biocon biologics( last round at $4.1B), 100M vaccine capacity commitment/yr for 15 year(15% equity equity but quiker asset light expansion), a new product stream which is very relevant after Corona- all type Vaccine R&D, Antibodies to be driven by Bicon biologics with Serum - although not mentioned but 15% equity might vest 1% each year for 15 years - or something similar - just a guess

-

Serum gets R& D commitment and skills, go to market via BBL as a channel, pure play manufacturing to upstream market access with this alliance

-

India driven bio tech ecosystem gets a boost

Concall tomorrow 9AM for details in press release

9 Likes

SII AND BBL DEAL CONCAL

5 Likes

Latest Investors Presentation

1 Like

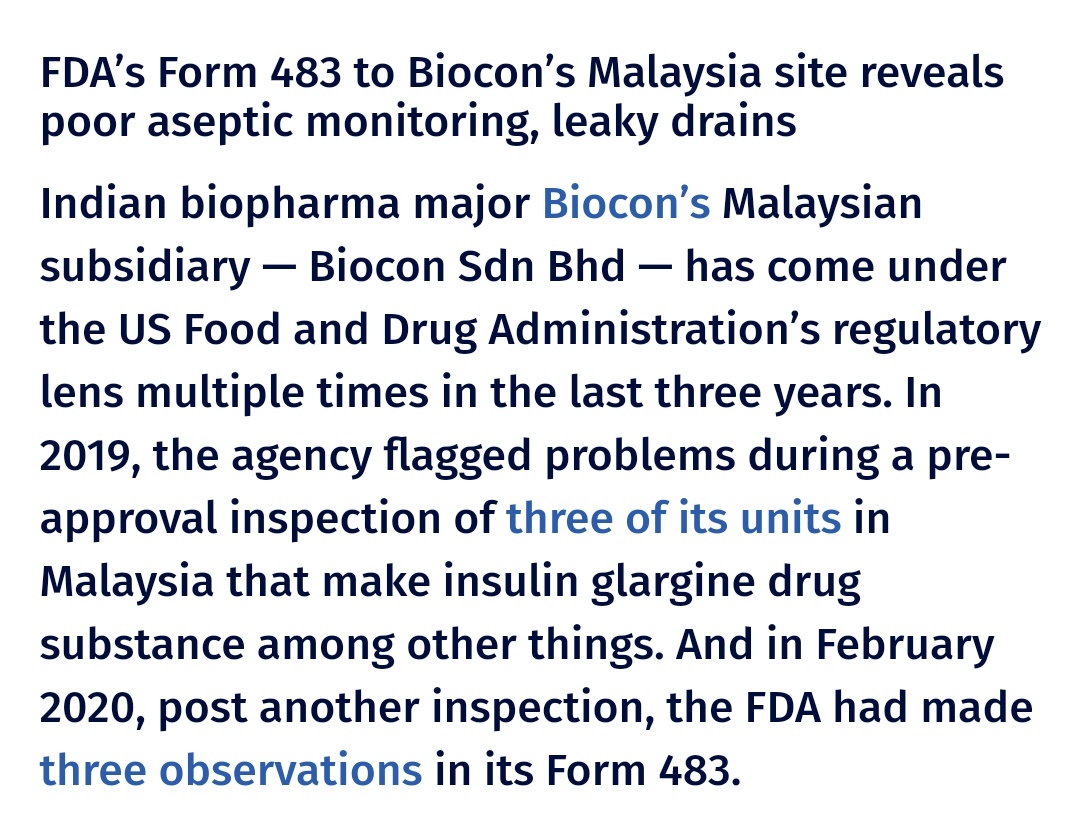

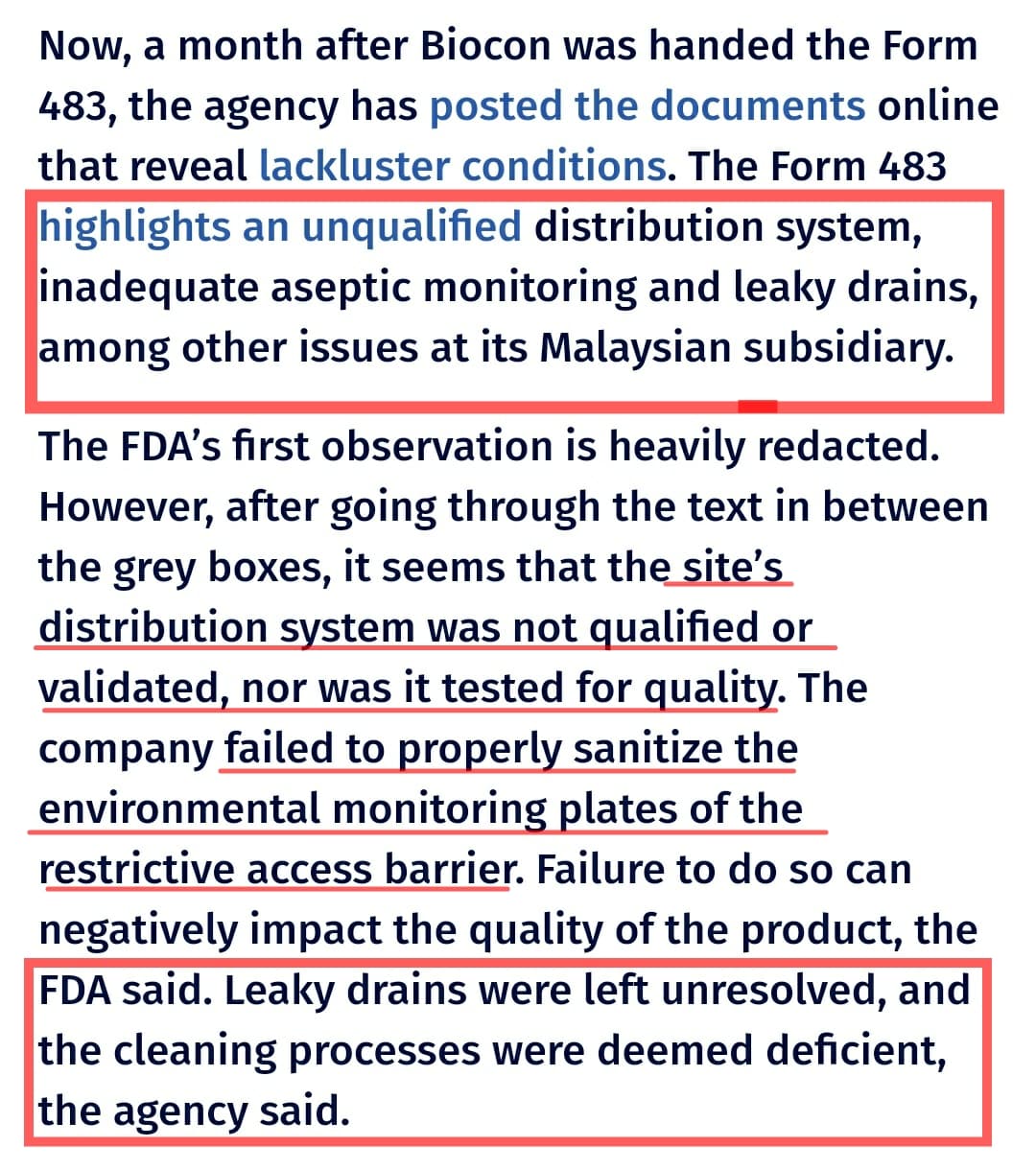

Biocon Biologics Insulin Manufacturing Facility in Malaysia Recd form 483 with 6 Observations

6 Likes

For kind attention of Biocon investors…

3 Likes

How should this clarifiaction be viewed?

As long as the business is alright, it may not affect the company in any major way, imho.

According to statement by Ms KMS, “Kunal Kashyap is an advisor to John Shaw and Glentec. In his capacity as an advisor, he is in no position nor has the legal authority to either control or influence the trust.”

An advisor, but can not influence? Very interesting…

BTW, you may want to look at this also.

SEBI order in respect of Mr. Kunal Kashyap and Allegro Capital Pvt. Ltd. in the matter of Biocon Ltd.

2 Likes

Power crisis in China is causing rise in price of key starting materials and intermediate chemicals. Those who are dependent on china for sourcing raw materials may witness higher input costs and margin contraction. One of the previous conference call mentions that, Biocon procures around 60% of it’s raw materials for generics from China.

8 Likes

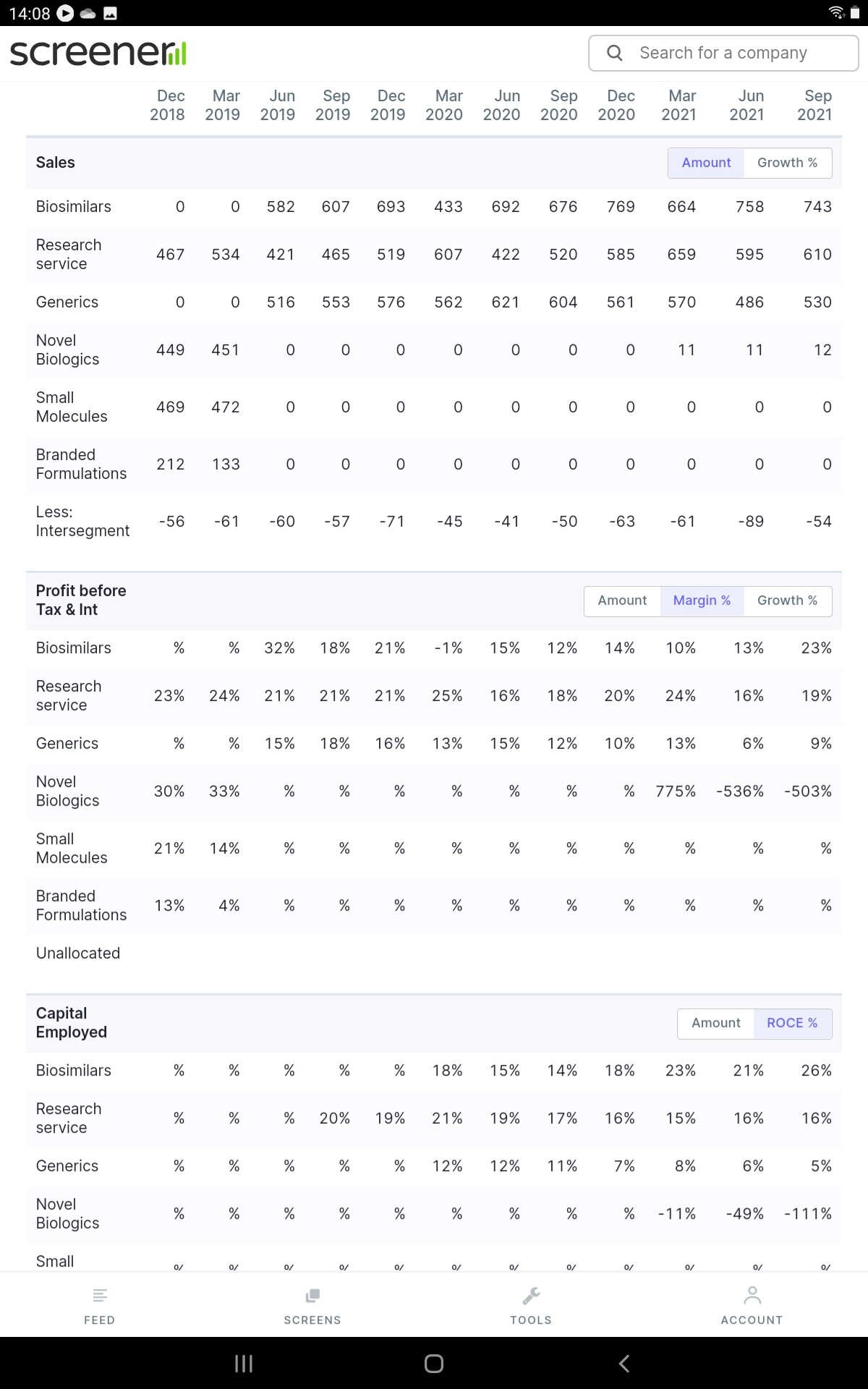

Q2F22 Results

The result is underwhelming - generics/formulations business did not do well.

My rough notes from the concall

Biologics revenue growth is 10% but profit growth is impressive at 47% (127 crores approx) reflecting capacity utilisation and increasing growth in the developed markets where margins are high.

Insulin glargine will be stocked in the leading USA pharmacy chain from January - this is excellent news indeed. Interchangeability status helped obviously. This will be the main driver in 2022. (Lantus market size was 7 billion in 2015 - it will be interesting to see how much market share biocon gains from the innovator)

Everolimus and esomeprazole launch in the US will help in the short term..

API manufacturing facility being built at Vishakapatanam - this will contribute from 2023. Capex 350 crores..

Partnership with serum institute will contribute from 2nd half of 2022

Covid affected biocon adversely - generics as well as biologics. Post-covid recovery will surely help biocon in a major way in my view. Share price has corrected 33% from the top.

Discl - accumulating since 2016

5 Likes

Biocon has been a underdog for quite some time now, to a point where pretty much folks have given up on them barring contra and high conviction folks with super long term views - silent thread is a good measure

Here is a 12 Qtr view

Some valuation takeaways and Q2 call highlights

- Though PE is not a right metric as they have E under pressure being in perpetual Capex phase, even after that they are below long term median PE range

- with Market cap of 40K cr, available at 5X sales and less than 23X EBDITA- that’s for a global scale Biotech and CRAMS player.

BelowTriggers for turn around in performance ( ignored by mkt for now)

- Biosimilar performance and margins improvement visible with back to back margins improvement - per call Geo mix helping with mkt share gains/steady

- Multiple Biosimilar positive trigers - post above by @stockcollector

- Syngene performance going steady- although hammered by mkt along with Biocon

- Generics can’t get any bad - cycle on pricing pressure to turn around next year as regular cyclical aspect and RM pressure to ease as well as covid stocking etc to normalize

- SII vaccine partnership, Adagio partnership appear to be smart win win proposition

- Good investors with successive raise in valuations for biologics

Monthly chart showing a lower channel bounce back, yet to see volume picking up

Invested , Re-entered recently

7 Likes

Positive Newflow + performance trajectory in Numbers = Narrative

Press release on Biocon Biosimilar Samglee and Glargine on National Formularies as preferred

Biocon Biologics and Viatris Announce Prime Therapeutics Prefers First-Ever Interchangeable Insulin Biosimilar Semglee® (insulin glargine-yfgn) Injection and Insulin Glargine (insulin glargine-yfgn) Injection on its National Formularies. This is for Prime Therapeutics- one of largest Pharamcy benefit manager

Few days back , similar approval on Express script, another largest Formulary in US - "Biocon Biologics’ First-Ever Interchangeable Biosimilar Insulin

Glargine, Co-Developed with Commercial Partner Viatris,Preferred on Express Scripts’ Largest Formulary in US

Now Q2 Biologics margin bump up and likely topline improvement in Q3( though launch are from 1st Jan 22, stocking will happen from Q3 onwards itself) is sustainable or not is anybody’s guess.

Given history of misses on performance, mkt may not fully believe until news follows with numbers, stock is in down trend+ consolidation from quite sometime. Risk reward may be favorable IMO for CY 22 - might be wrong in thesis.

Invested with small allocation

3 Likes

Excellent news indeed - interchangeability status for insulin glargine has helped of course…

I am very bullish on Biocon in 2022 and beyong - they will do exceedingly well, in my view, in the post covid world…

Insulin glargine sales in the USA will take the revenues and profit to the next level in my biased opinion…

Disc - holding and adding since 2016

1 Like

I do not track sequent scientific - I have no idea

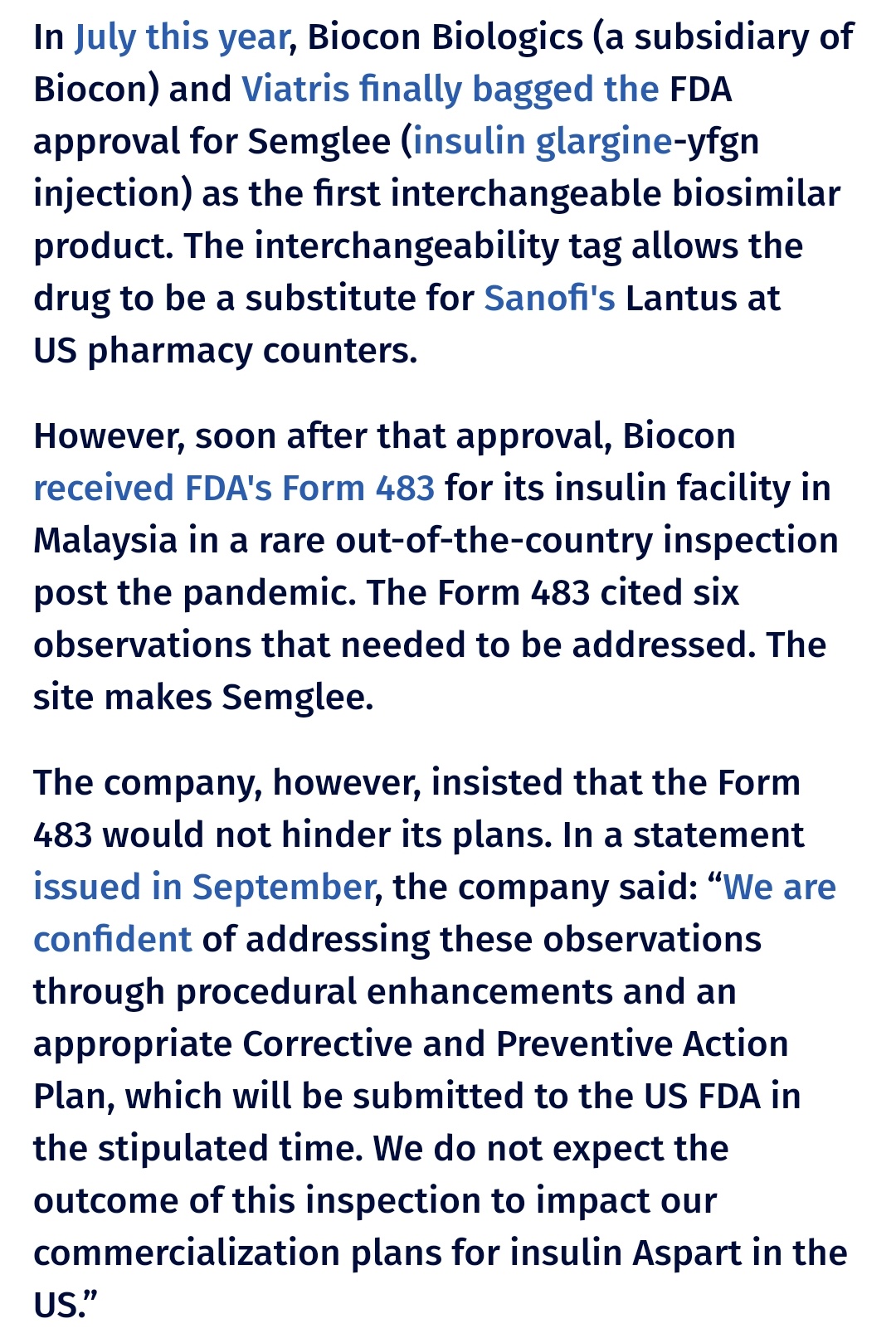

Won’t be surprised if western media is tilted against Indian bio pharma( has happened many times on Quality of deliverables from Indian IT as well, now that size and scale is with Indian players, such noises have relatively reduced). Worth a read to hear other side

in above article - Biocon has pushed back the writer/agency to factually report right content, below note was added and apparently its done - here it is

Editor’s Note: This story has been updated to correct an error. The Form 483 given to Biocon specified ‘raw material’ rather than drug substance. Biocon requested this letter be published alongside this story:

With reference to the above article dated Oct 28, 2021, published by Endpoints News on the nature of observations issued, at the conclusion of the USFDA inspection at Biocon Biologics Malaysia facility in Sep 2021, we would like to state that this article contains several inaccurate inferences drawn from a ‘heavily redacted’ Form 483 and is grossly misleading.

Furthermore, this article makes assumptions and extrapolations which are not just inaccurate but also exaggerated. “To cite one example, Josh Sullivan’s proclamation that “Biocon’s staff failed to properly identify each lot and shipment of drug received to ensure the adequacy of the Drug Substance” is inaccurate. The actual observation, as noted by the agency, but redacted in the published Form 483, is related to incoming Raw Material testing for a single inert component.”

Furthermore, the article in its opening para gives the impression that this was a ‘rare out of country inspection’ and talks about unqualified distribution system with leaky drains presenting a very gloomy picture. None of these words appear in this form in the redacted document.Statements such as these and others in the article, when taken out of context or extrapolated can be misleading and potentially cause concern to all stakeholders.

By way of background, this inspection was scheduled as a part of the FDA’s ‘Resiliency Roadmap for FDA Inspectional Oversight’ (published May 2021), wherein the agency laid out their roadmap towards prioritizing domestic and foreign inspections based on several factors including those tied to new product approvals.

In this instance, the on-site ‘Pre-Approval Inspection’ (PAI) was a part of the established PAI process for review of a Biologics License Application (BLA) for Insulin Aspart, for which there is currently no approved biosimilar available to US patients.Biocon Biologics had proactively released a public statement on Sep 25, 2021 on the completion of the US FDA inspection of the Malaysia site and disclosed the issuance of a Form 483 which had identified six observations spanning the Drug Substance, Drug Product and Devices facilities.

We had stated that we are confident of addressing these observations through procedural improvements expeditiously. We can confirm that our detailed Corrective and Preventive Action Plan (CAPA) has been submitted to the USFDA on Oct 15, 2021. Endpoints News is a widely read publication and we have great respect for its content hence it is important for your stories not to exaggerate, but provide a factual perspective.

As a company, we believe in open communication and would appreciate if your teams reach out to us in order to make an informed narrative. We therefore request you to either retract this article or publish this ‘Letter to the Editor’ and link it to our story.

6 Likes

Happy to hear other side of the story.

USFDA Inspection and issuance of form 483 with a total of 6 observations across drug substance, drug product and devices facilities is a fact.

Can’t tell more about the credibility of the article without reading the form 483 and those observations. I’ve tried to find the USFDA form 483 with observations on public domain, but I couldn’t find that one.