The stake is around 70%

3 Likes

Biocon investment thesis:

- Upcoming listing of Biocon Biologics in a couple of years or max 3 years could be a big valuation trigger

- Owns Syngene 70% stake and is a good way to play Syngene at a discount. Syngene is a CRO (akin to IT services industry) and does not have the upside that Biocon has

- First Indian company to have a biosimilar approved in US. 1-2 biosimilars approved can be a huge re-rating possibillty

- German CEO leaving and Biocon veteran taking over is also a plus. By doing scuttle-butt with Biocon employees & Syngene employees, it is clear that the new CEO is a much better bet

Overall, company stock has been a laggard. Could be a multi-bagger in 3 years.

3 Likes

Hi, could you please elaborate on this further. Why do they think he is better? Has he made any change to strategy. What was wrong with old CEO? etc.

Thanks

3 Likes

The abrupt departure of Biologics CEO when they were indicating an IPO soon was a real shock.

Also in biologics, the biggest valuation driver for global giants have been oncology drugs, but till now Biocon has mostly commented about some success in Diabetes drugs. So, a bit skeptical on how the valuations will play out.

I am eagerly waiting for Biocon’s rerating driven by approvals of existing biosimilars with Viatris but the potential is starting to look weak as competition is catching up.

At present Biocon/Mylan share in insulin is only 2.5% (roughly) this interchangeability may give real boost

2 Likes

Then it might make sense to buy biocon than in syngene.

Biocon looks undervalued from that perspective.

Sorry about the naive question… But can you throw some light there…

Biocon is the holding company for Syngene. Buying Biocon is like buying Syngene at a discount with the Biocon Biologics IPO upside. It is all a matter of time. Every good company goes up and Biocon too will get favour some time.

As investors, we have to have the right hypothesis, buy the right companies and hold tight till market recognizes the value of our companies

3 Likes

Biocon is up around 5% now. We cannot predict when companies will move up. See Hikal went up 3.5 X in 2 months.

As investors, we have to buy and hold good quality stocks and wait for markets to recognize the value. The value unlocking in Biocon can happen in so many ways:

- Biocon Biologics Approval

- Syngene push out holding company stake in some manner and remove holding co discount

- New molecule discovery similar to their insulin one

- From my scuttlebutt, employees are very happy that their beloved leader Arun Chandravarkar is back at the helm as MD.

3 Likes

Covid did affect biocon - manufacturing got affected, usage of their products were also lower due to covid postponing many cancer treatments all over the world, esp in the developed world.

Covid is settling in the developed world and things are getting back to normal. Biocon should do very well in the next 2-3 years. Insulin glargine usage in the USA should increase considerably as the pharmacies start to stock insulin glargine…

Discl - holding and adding since 2016

4 Likes

Biocon Q1 2022

Disc: small quatity holding

Biocon Q1 2022

Generics

Profit and loss impact on bicara subsidary may last to another two more quarter and investment value at the end of this quarter is 15 million USD, also this issue won’t last more than this fiscal year.

Generics business impacted of approx 75 cr due to covid ,especially in banagalore, fermentation not happeened due to lack of oxygen avaialabilty and Pricing presure from US .

New launches are blood pressure control tab labetalol and proton pump inhibitor of cap esmaprazole ( as per report USD 63 million and USD 233 million market share respectively)

Regarding interchanagabilty for insulin glargine would finalaised at the end of july.if that approves by US FDA,this would be the first insulin got status of interchangeability.Along with this insulin aspart also applied for interchanagability.

Biosimilar share of sale in ROW is very positive .also expect robust growth of 25%

Disc: holding small quantity

Would like to know from participants regarding more insights

2 Likes

Q1 con call

-

Syngene has done well woth 40%+ growth on YoY - some due to low base and part due to covid one offs- guidance conservative though of mid teen - high expectations and valuations, 5 yr for achieving 1X asset turnover in relation to Mangalore facility is also going to test patience, excellent execution on recent deal wins, leadership in new capabilities and aggression in investments continues

-

Biosimilar seems to be bouncing back with both YoY and QoQ, good commentary on demand being healthy/ mkt share gains/ July end interchangeability approvals/ over due FDA visits for pending inspection, key takeaway was RoW leading with 65% share in this qtr and acknowledgement by mgmt that RoW will be higher share in longer term as well- This IMO is better control of Biocon ( ownership of sales and mfg vs developed mkt where Biocon is more of Mfg focus with little or no control on demand dynamics in control of partners) - min 20-25% type growth required to support valuations

-

Generics has been a drag and margins have suffered as well - many reasons such as oxygen shortages affected fermentation drive APIs/ larger base last yr- low operating leverage quite visible and hopefully one off and should bounce back Atleast to past trajectory of single digit growth

-

Bicara clearly hitting bottomline, fund raising need acknowledged

All in all a great science and bio tech prowess, quality Corp governance, high valuations demands better performance, goal post moves further

Dilemma for investors in raging bull markets

Invested

13 Likes

Press Release titled “Biocon Biologics Partners with Adagio Therapeutics to Advance Antibody for the Prevention and Treatment of COVID-19

1 Like

Good news for biocon

This is a momentous day for people who rely daily on insulin for treatment of diabetes, as biosimilar and interchangeable biosimilar products have the potential to greatly reduce health care costs,” said Acting FDA Commissioner Janet Woodcock, M.D.

5 Likes

Lantus was Sanofi’s second best selling pharmaceutical product in 2020 and generated $2.7 billion in worldwide revenue.

“Biosimilars marketed in the United States typically have launched with initial list prices 15% to 35% lower than comparative list prices of the reference products,” the FDA wrote.

Per press release Biocon-Viatris will have one year exclusivity from commercial Launch , which is Q3 22, even at 15% market share in first year( mid teen pattern of other biosimilar) there is potential to do $200M-$300M from US in CY23 for both companies combined.

Biocon currently does approx $100M from biologics per quarter.

Invested

12 Likes

After the positive news of USFDA approval of Biocon’s long-acting insulin Semglee as first interchangeable biosimilar product, it is little shocking to see around 8% fall today

Tried to read up multiple sources but not seeing any red flags anywhere. Am I missing something?

Disclosure: invested

2 Likes

I’m sharing some anti thesis points. (I’m not justifying the fall in share price)

Regulated markets are witnessing higher competition, margin contraction, pricing pressure and higher freight charges & supply chain disruptions.

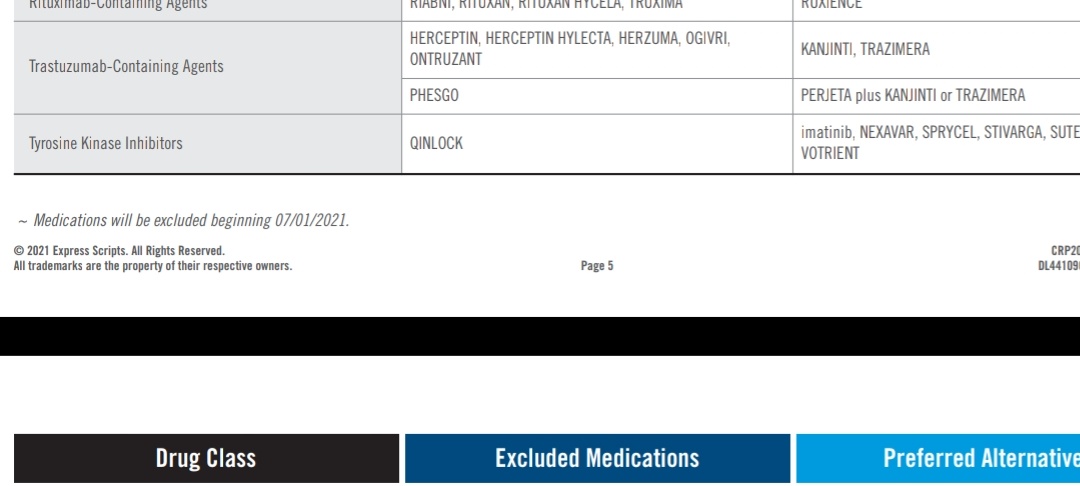

Biocon’s OGIVRI (trastuzumab biosimilar) is dropped from the preferred formulary list and substituted with Pfizer’s TRAZIMERA and Amgen’s KANJINTI. This can cause loss of market share.

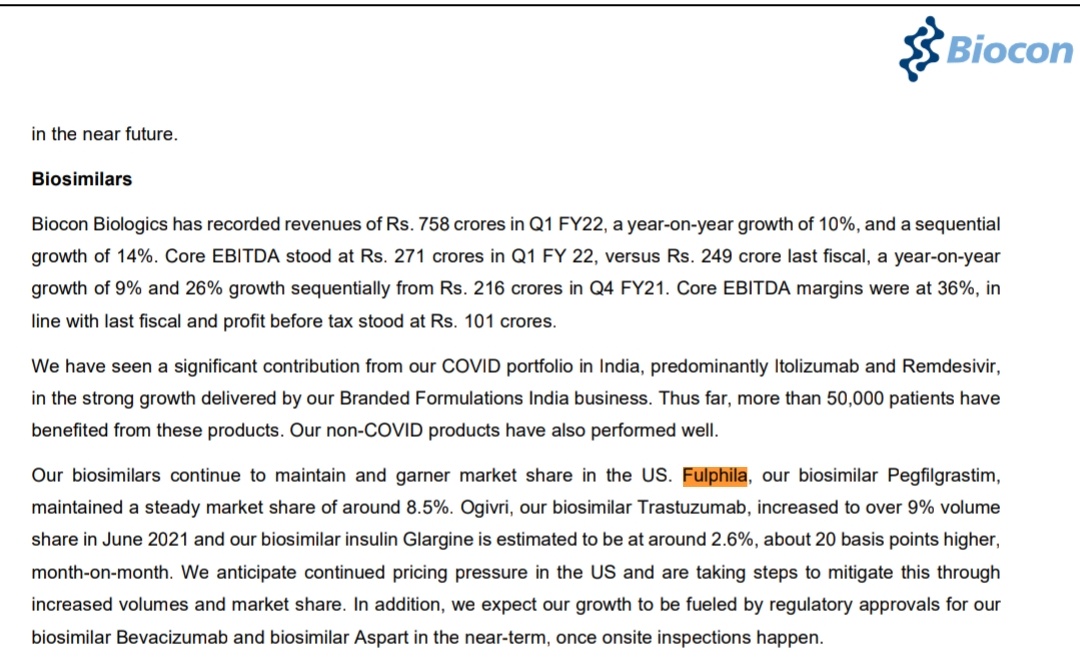

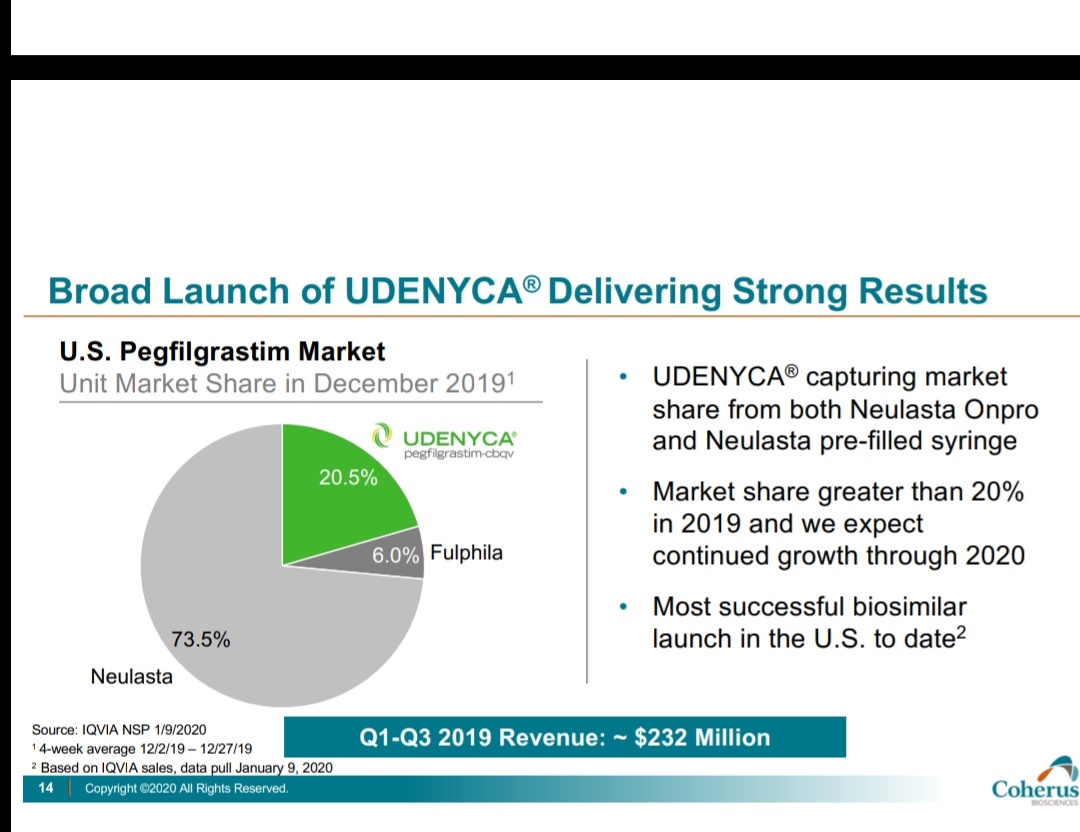

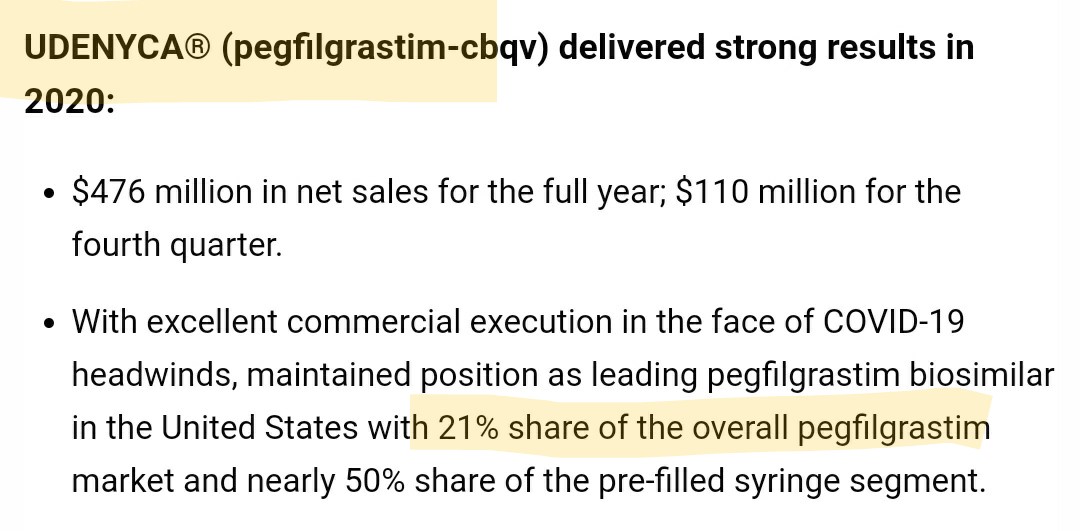

Earlier they had lost market share of Fulphila to Coherus’s Udenyca (23% to 6% in 2019 to 8% now)

Although Fulphila had first mover advantage, Udenyca later gained significant market share. On latest concall, Biocon’s fulphila market share was mentioned as 8.5%. This is the level of competition we are seeing in biosimilars space. With the drop of OGIVRI from the preferred formulary list, we may witness reduction in market share.

22 Likes

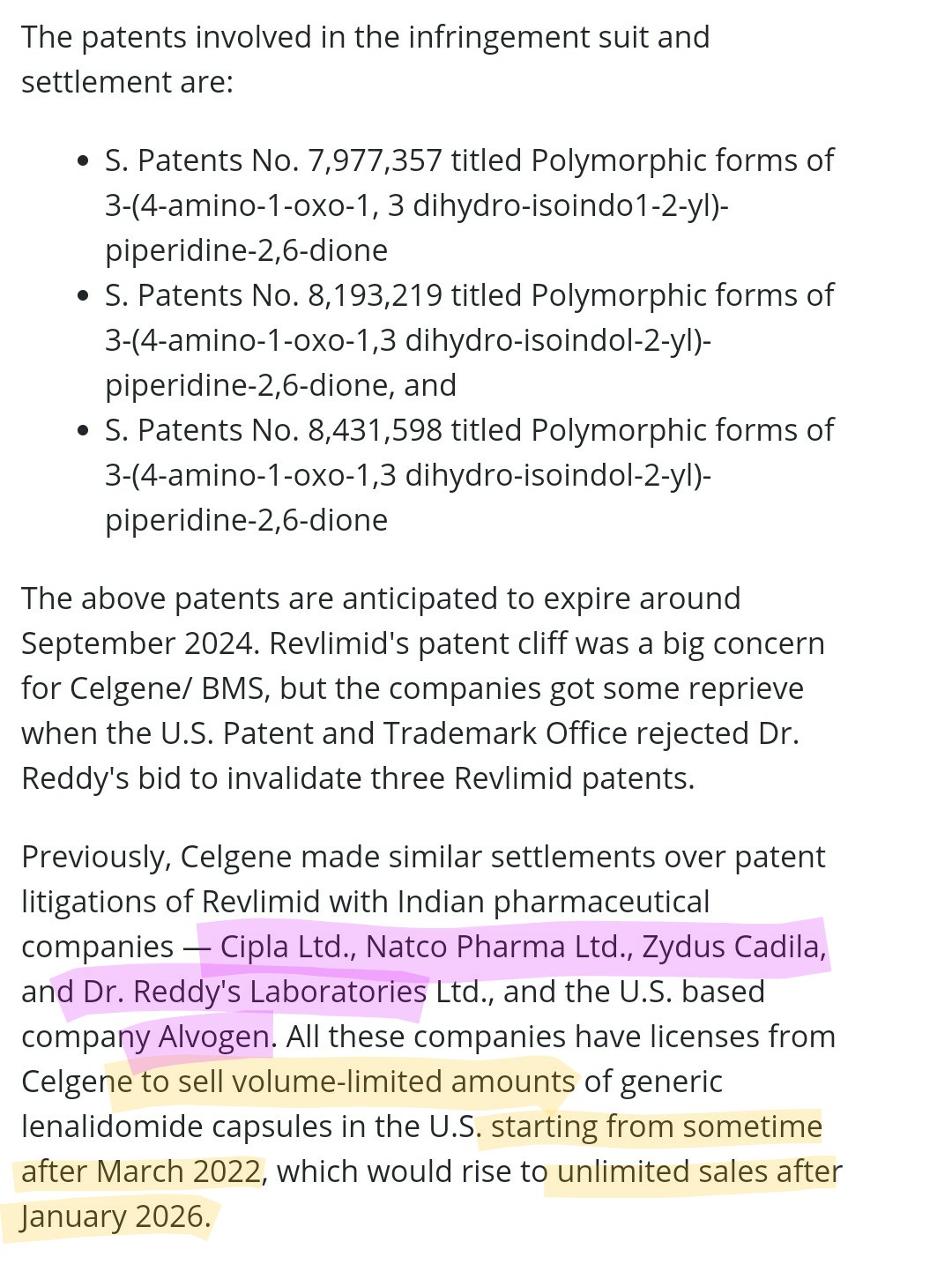

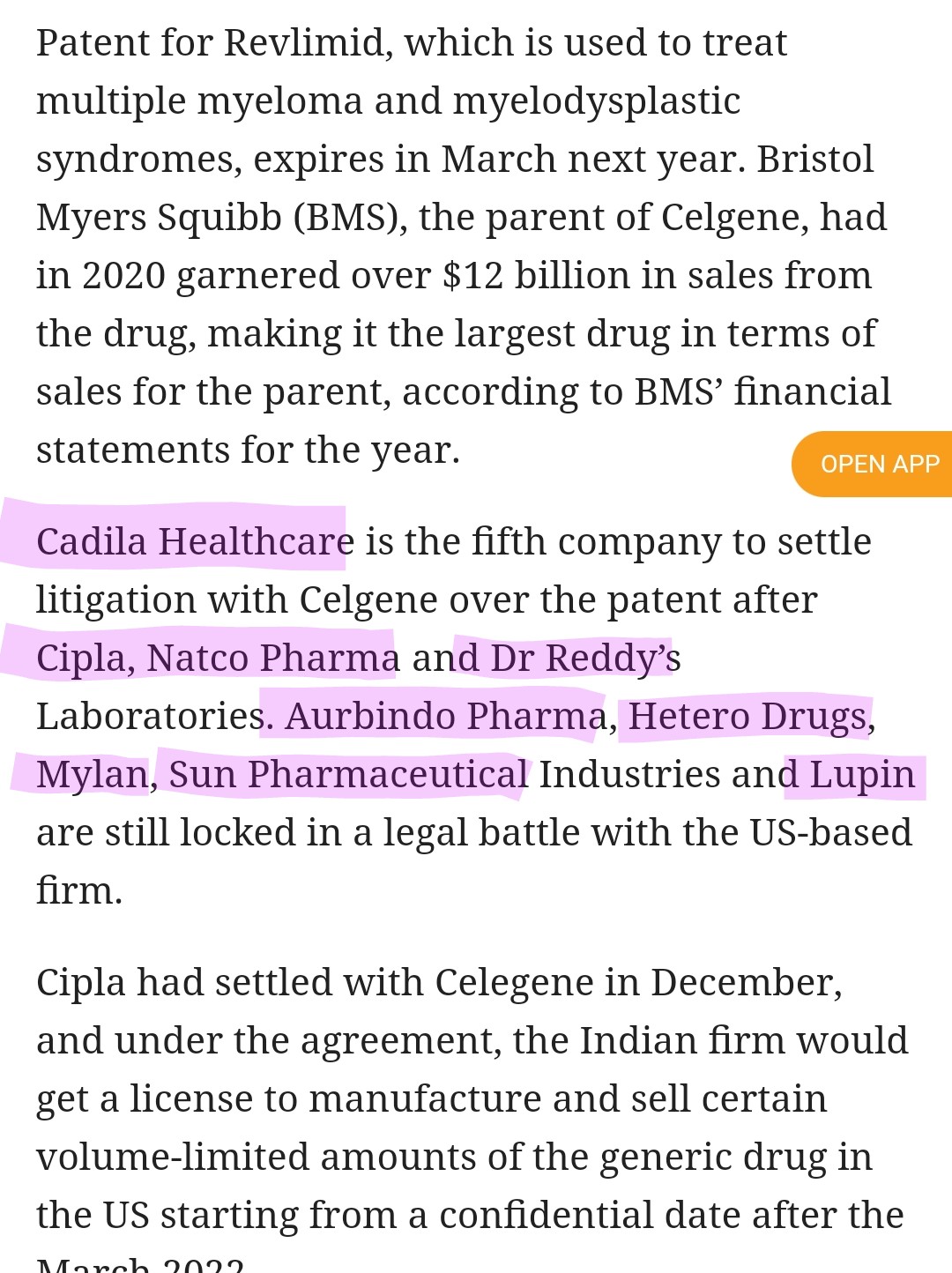

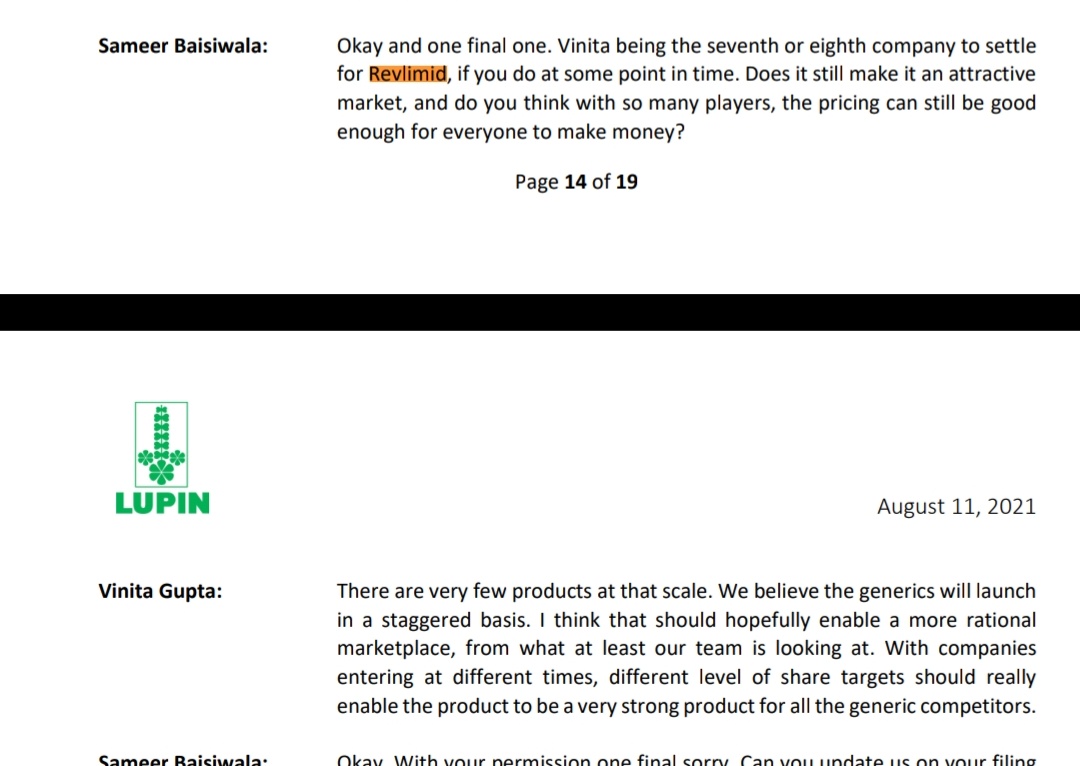

“Biocon Limited enters into a settlement agreement with

Celgene Corp.

Could some explain the impact of the above?

Biocon is around 7th company to get license from Celgene to sell Lenalidomide in US with such settlements over potential patent litigation. (Aurobindo, Mylan, Lupin, Hetero drugs are still in the battle I suppose. I don’t know the current status). From what I’ve understood, all these licenses are for selling volume limited amounts until January 2026.

This what Lupin management has told in the recent con call.

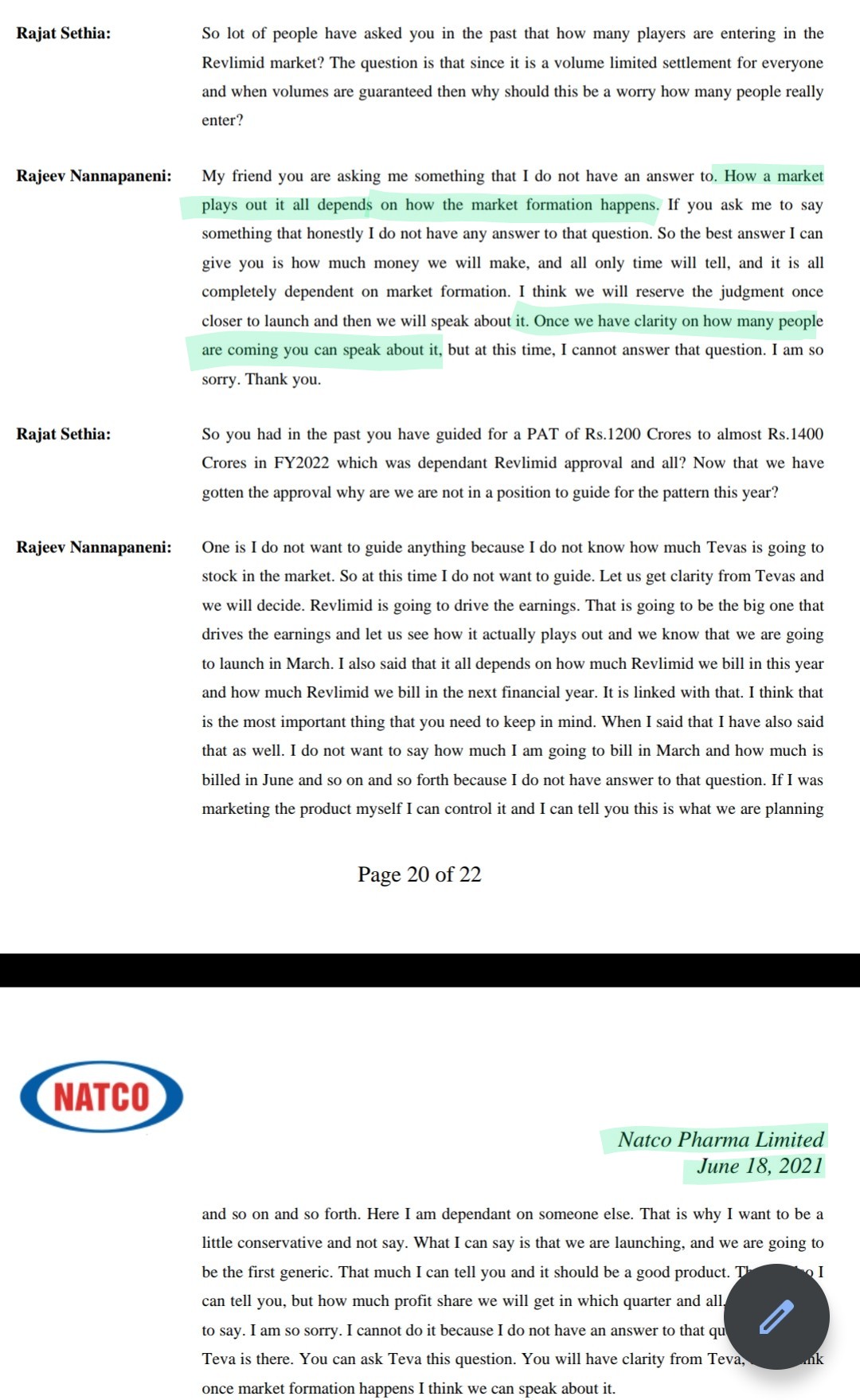

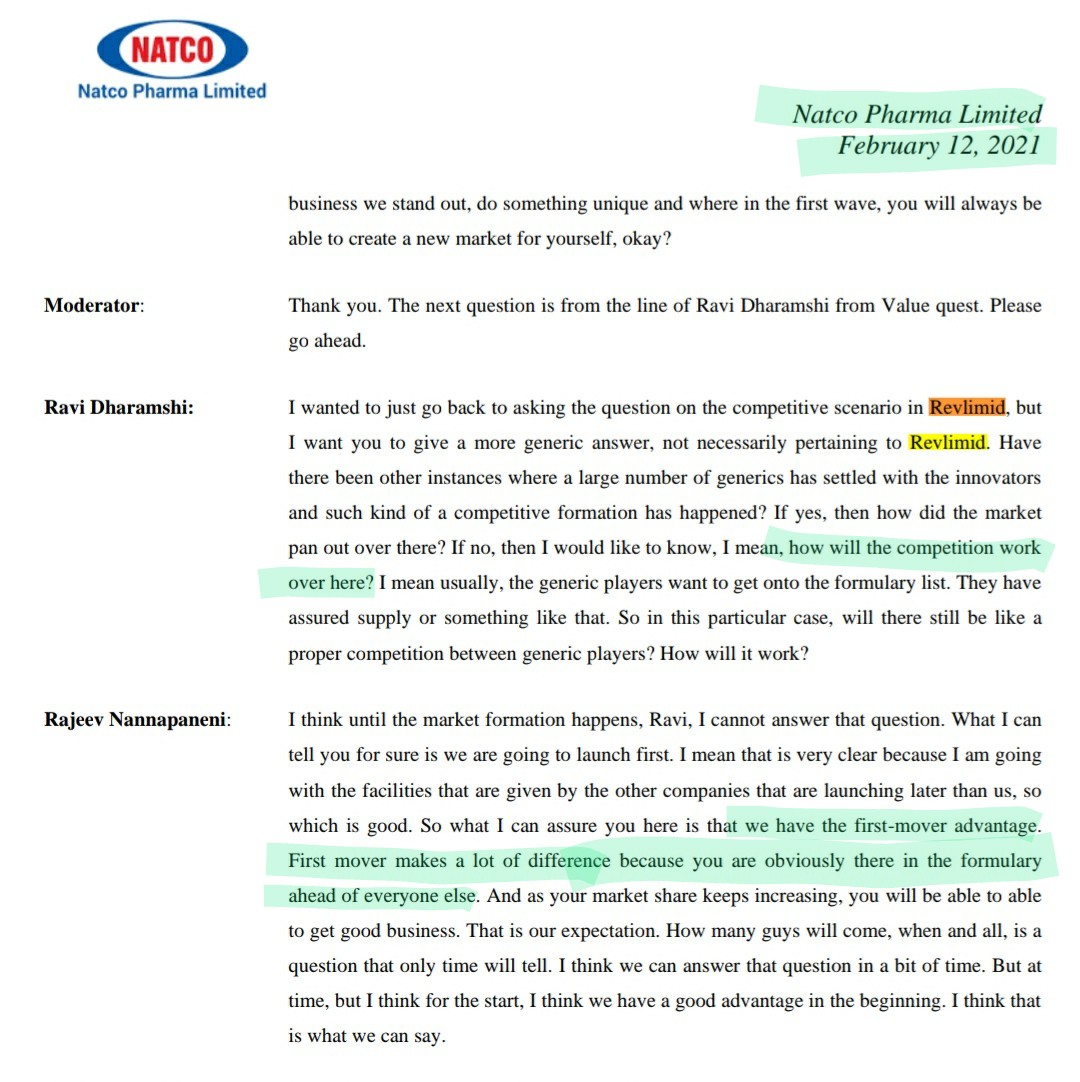

From the recent concalls of Natco pharma, what i understood is, the competition for Revlimid (Lenalidomide) would be high. Natco has first mover advantage. Several other players are lined up and are already ahead of Biocon.

.

14 Likes

Biocon - Notes from AR 2020-21 -

- Total sales - 7360 cr, up 14 pc.

Break up -

Generics - 2335 cr - grew by 6 pc

Biosimilars - 2800 cr - grew by 21 pc

Research services - 2184 cr - grew by 9 pc

Domestic sales of total - 19 pc

Intl Sales of total - 81 pc

R&D spending at 627 cr, up 19 pc ( at 13 pc of revenues Ex - Syngene ie Research services ). This is expected to remain in the 12-15 pc band in near future

EBITDA at 1907 cr, up 8 pc

EBITDA margins at 26 pc

PAT - 740 cr, down 3 pc

Adjusted for exceptional items ( a gain of Rs 159 cr on account of ceding control in Bicara ), NP would have been at 594 cr

- Biosimilars - One of the select few companies globally to have co-developed 05 biosimilars. These are -

bTrastuzumab ( used to treat breast cancer ) - named Ogivri

bPegfilgrastim ( to reduce infections in patients receiving chemotherapy ) - named Fulphila

bBevacizumab ( used to treat a number of Cancers ) - named Abevmy

bGlargine ( long acting manmade version of human insulin ) - named Semglee

bAspart ( short acting manmade version of human insulin )

Company has also commercialised rh-Insulin ( recombinant human insulin ) in many developing markets

Company commercialised third Biosimilar in US - Insulin Glargine. Only company from India to have 3 commercial biosimilars in US markets

Obtained regulatory approvals for Biosimilars - Bevacizumab and Insulin Aspart in EU Biocon is among a select few companies to have 5 biosimialrs approved in EU

Commercialised Pegfilgrastim ( Fulphila ) in Australia and Canada.

Company saw fund infusion totalling $ 330 million by funds such as - Tata Capital, Glodman Sachs and Abu Dabhi based ADQ - valuing Biocon Biologics at $ 4.2 billion. Funds being used for Capex, R&D and Opex and to redeem Biocon ltd’s preference shares in Biocon Biologics which will further be used for Capex in generics business. For now, company is adequately funded for near term capex requirements

Mkt opportunity in biosimilars remains strong as biosimialrs worth $ 90 billion are set to lose exclusivity over the next decade

Total capex for the FY in the Biologics business - $ 125 million primarily for expansion of production capacity for monoclonal anti bodies. Additional capex lined up for FY 22 at $ 100 million. Company’s new facility for monoclonal antibodies, largest in India is awaiting commercialisation

Company continuously investing in R&D in biologics space. Will continue to do the same to commercialise second wave to Biosimilars in second half of the decade

- Generics - Company supplies Statins ( family of drugs used to lower cholesterol ), immunosuppressants, narrow spectrum antibiotics and other APIs to over 100 countries. **Company is one of the largest manufacturer of Statins and Immunosuppressants globally.**Company is a late entrant in formulations business and aims to replicate the success of its API growth story into formulations by successfully forward integrating in nice , difficult to make APIs. APIs continue to remain biggest contributors in the company’s generics business. Key highlights in generics business include - launch of Tacrolimus capsules ( used as an immunosuppressant during organ transplants ) in US , approval for Everolimus ( generic to Afinitor - immunosuppressant used to treat cancer ) , DMF approval for Sitagliptin API in China and company’s new tie ups in Brazil, Singapore and Thailand. Company aims to enter Japan and Russian markets in FY 22

Statin formulations continue to hold mid teens mkt share in US

Continue to witness intense pricing pressures in APIs and formulations particularly in competitive markets like US. Stockpiling of medicines in the first half led to demand slowdown in the second half.

Filed for 33 APIs globally and got approvals for 14 APIs during the year

Also filed for 09 formulations - globally

API capex projects are in various stages of execution. Experiencing some delays in Greenfield capex at Vizag ( immunosuppressants APIs facility ) due COVID. This facility is expected to go commercial in FY 22. Various cost saving programs are also under implementation. Company working towards reducing single vendor / single geography dependence for key materials for API manufacturing - Novel Biologics business - Company’s portfolio of novel biological assets comprise therapeutics for diabetes, autoimmune disease and cancer. Itolizumab - initially launched in India for treatment of plaque psoriasis in 2013. In Sep 20, Itolizumab approved by DGCI for treatment of Cytokine release syndrome in moderate to severe ARDS ( acute respiratory distress syndrome )

Also out licensed Itolizumab to their US biotech partner - Equillium Inc in 2017. Equillium is developing Itolizumab for multiple severe immune-inflammatory disease including acute graft vs host disease, lupus and lupus nephritis and uncontrolled asthma. Company is expecting clinical data from these studies in 2021

Insulin - Tregopil ( a first in class oral insulin molecule ) - Phase 2 studies have been submitted to DCGI and USFDA. Data from type - 2 diabetes studies has been encouraging, marketing authorisation applications were delayed in wake of the pandemic. In FY 20, company had also commenced studies for Type 1 Diabetes in Germany. Expected to be completed by FY 22

Bicara - Its lead program - BCA 101 entered phase -1/2 studies at leading US and Canadian cancer centres in Jul 20. Biocon ceded control over the board of Bicara. Biocon now classifies Bicara as an associate company now from being a subsidiary - **Total Capex guidance - For FY 22, expected to be in the range of $ 300-320 million. $ 100 million each for Biosimilars, Generics and $ 120 million for contract research.**Funds already raised via PE placement in FY 21 and the rest would be made up via internal accruals

I ve deliberately not covered the CRO business here. One can get notes on the same from the thread on Syngene International as the same is separately listed

Disc : Invested, Biased

14 Likes