Biocon Biologics launches Semglee, drug to control high blood sugar, in US

Download Economic Times App to stay updated with Business News - https://etapp.onelink.me/tOvY/135dde21

Very Aggressive pricing,

Biocon Biologics launches Semglee, drug to control high blood sugar, in US

Download Economic Times App to stay updated with Business News - https://etapp.onelink.me/tOvY/135dde21

Very Aggressive pricing,

Latest Interview (link). Insulin glargine biosimilar market size is $2.2bn. They launched at a 65% discounted listed price. Does this mean that they launched at $65 for a listing price of $100 or did they launch it at $35? Can someone clarify this?

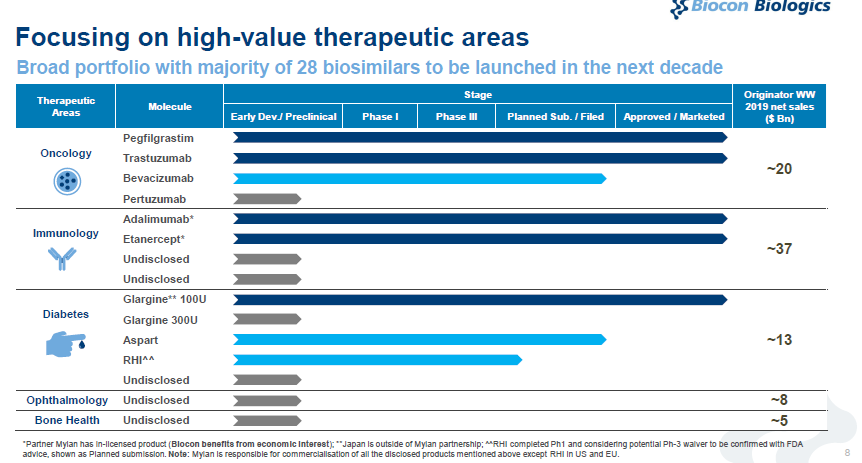

Expect FDA approval for bevacizumab in FY21.

5 pens on cvs pharmacy are available at discounted price for 328 dollars. Mylan has priced 5 pens for 148 dollars and obviously discount shall follow

https://www.healthline.com/diabetesmine/new-low-cost-semglee-insulin-now-in-us#How-cheap-is-it?

Semglee is almost one third of lantus, Sanofi product and almost half of basaglar, lilly product.

42nd AGM proceedings

Any information on how is this beneficial to us who are holding stock of Biocon Ltd from last many years (since 2017) and haven’t had much capital appreciaton? Please experts throw some light on this aspect.

Thanks

If you scroll up, there is discussion on IPO versus demerger of Biologics. The question you asked is also in top of many who invested in Biocon for a long time now.

If I consider around first Jan 2017 to today

roughly 160 to 450 in four years is 29.5%CAGR

If I consider my rough CAGR in five years is 41%

Frankly speaking never expected this much initially

By any standard it’s good return (in between line probably one can say some pharma stock are 2.5 times in 3 months , good luck to them)

Now come to total gross block and capital work in progress

In 2017 it was 6270 CR

In 2020 it’s 11343 CR

(Kindly compare this data with other pharma companies)

Biosimilars business require lot’s of investment and luckily market participants are forward looking for this business so hopefully our investment will be appreciated in future also

And like to add that This is not just like few ANDA opportunity it’s multi-year (chronic disease) large opportunity with good margin

Even in AGM also questions asked about BioconBiologic listings but it’s atleast 2 years away and management given assurance that they will do what is best for future business and shareholders

Thanks

Thanks for putting up this information. I feel missed out on pharma rally since march-20 as Biocon has been lagging in upmove. In any case I am now going to hold on to my position and see what’s in store until Biologics is listed.

KR

Biocon has been part of portfolio for 10 years now. I have held on because they have walked the talk. I believe they have huge opportunity and runway ahead.

Shareholders got fairly rewarded in syngene ipo as not many applied.

Both Biocon and syngene I believe have done well till now and hopefully shall deliver in future too.

Key summary of Q2 results of Biocon - Soucre: IndiaInfoline

Biocon reported an increase of 11.33% in top line sales for the Sep-20 quarter at Rs1744.80 Cr on a yoy basis. The operating profits for the quarter ended Sep-20 were down by 21.2% at Rs 213.70 Cr while the net profits were down by 23.8% at Rs 200.40 Cr.

This had a logical impact on the margins of the company. For the Sep-20 quarter, the operating profit margins or OPM was sharply lower by over 500 bps at 12.25% while the net profit margins or NPM for the quarter was down at 11.49% due to sharply higher raw material cost in the Sep-20 quarter due to supply chain disruptions.

Financial highlights for Sep-20 compared yoy and sequentially

| Particulars | Sep-20 Quarter | Growth (yoy) | Growth (qoq) |

|---|---|---|---|

| Total Revenues | Rs1,744.80cr | +11.33% | +4.40% |

| Operating Profit | Rs213.70cr | -21.20% | -13.31% |

| Net Profits | Rs200.40cr | -23.86% | +16.92% |

| Key Ratios | Sep-20 Quarter | Sep-19 Quarter | Jun-20 Quarter |

| Diluted EPS | Rs1.41 | Rs0.84 | Rs1.25 |

| Operating Margins | 12.25% | 12.56% | 14.75% |

| Net Profit Margin | 11.49% | 19.09% | 10.26% |

Key takeaways from the Sep-20 quarter results

The net cash generated from operations nearly halved to Rs209cr for the first half of the fiscal year ended on 30 September 2020. This was due to unfavourable movements in the trade receivables and the inventories in the first half of this year.

Biosimilars are the single biggest revenue source for the company in the Sep-20 quarter followed by generics and research services. Bio similars account for 38% of the total revenues, Generics accounted for 33% of the revenues.

The company is in the forefront of research into a possible COVID vaccine as also it has tied up for manufacture and distribution of Remdesivir. This could present a big opportunity for Biocon in the coming quarters.

Here are my notes from the conference call

Disclosure: Invested (position size here)

While most of data points are covered by fellow VPers, Some additional inferences from quarterly call

Most of Questions centered around biosimilar performance in short term( slow revenue growth, margins being bit low and bit lumpy,competitive landscape and pricing pressure, Capex and so on).

Very few long term and strategy related questions.

Growing concerns around performance consistency and predictability, and mgmt responses being not very reassuring & more subjective

At current valuations, neither revenue or bottomline are catching up. Capex heaviness.

Mgmt ommentary optimist as usual, good part logistics challenges acknowledged being worked on to address top line issues, admitted demand and supply both intact.

Capex heavy future outlook - counting on PE money, IPO proceeds and cash generated - first two doing hevaylifting

All three biz lines ( Syngene, generic and formulations, biosimilar) at give or take $100m qtrly run rate in near future( missed how soon part) , appears best case in next few qtrs to get market reassured. Heard one response on those lines.

Further acknowledged that first movers in biosimilar tend to get advantages and future will see lot more new entrants getting in - is the best phase on pricing power and quick mkt share gains getting over soon?

Unless they are always ahead of market curve by investing heavily on future pipelines etc. I.e. volume will drive value and competitive intensity will drive price( far from generic type pricing destruction but there were already questions on 60-70% type discount from innovator pricing for biosimilar)

Management acknowledged on working on equitable treatment for biocon shareholders on Biocon biological listing.

Summary

Invested, top 5 in PF

The company announced their third fund raise in biologics division.

| - | Fundraising sequencing |

|---|---|

| o | 06-01-2020: $75 mn for 2.44% equity stake with True North fund (valuation: $3.07 bn) |

| o | 31-07-2020: $30 mn for 0.85% equity stake with Tata Capital Growth Fund (valuation: $3.53 bn); For $30mn (at exchange rate: 75), they were allotted 88’30’456 shares of Biocon Biologics at price of 254.8 (Biocon holds 95.25% stake) |

| o | 07-11-2020: $150 mn (1125 cr.) for 3.8% equity stake with Goldman Sachs India AIF Scheme-1 (valuation: $3.94 bn); Exchange rate: 75; |

Trailing twelve month sales for their biologics division is ~2389 cr.; Goldman valued them at 29’550 cr. (EV/sales ~ 12.36). Post this transaction, Biocon will hold 95.25-3.8% ~ 91.45% of stake in Biocon Biologics (EV ~ 27’000 cr.). This makes the EV of rest of business (Syngene + Generics) ~ 24’000 cr. Removing syngene’s valuation (~15’173 cr.), the generics business is valued at ~8’800 cr. (close to 4x EV/sales).

Disclosure: Invested (position size mentioned above)

Good development and timing, if memory serves right they sort of indicated $300m type fund raising before IPO, Above 3 rounds takes it closer to that mark. Given sector tailwind, avoid any Policy setbacks by new US government, it makes sense to not to delay beyond H1 21.

Syngene being richly valued and for right reasons , wonder what is the upside left for current investors by the time of listing or there about, even if we take a 25% growth at consol level over year - that much incremental value would be balancing out holding company discount for Biocon.

Would be interesting to see minority shareholders treatment.

Biocon Biologics signs MoU with CSSC in Tanzania for Mission 10 Cents

Biocon Biologics, an integrated ‘pure play’ biosimilar company and a subsidiary of Biocon, in continuation of its Mission 10 cents affordable insulins program for low- and middle-income countries (LMICs), has signed a Memorandum of Understanding (MoU) with the Christian Social Services Commission (CSSC), a faith-based organization active in Africa. CSSC works closely with the government as well as international and national partners to facilitate health and education

services. Tanzania will be the first country in Africa that will benefit from this collaboration between Biocon Biologics and CSSC. Biocon Biologics is helping unlock universal access to quality insulins in low- and middle income countries(LMICs) by making recombinant human insulin (rh-insulin) available for less than 10 US cents per day as a part of its ‘Mission 10 cents’ program. Besides improving access to insulin treatment by making affordable yet high quality insulin available, Biocon Biologics is working with local partners to help strengthen overall healthcare capacity with the aim of supporting all people with diabetes in LMICs, where diabetes prevalence has been rising more rapidly than in high income countries.

Inspection of Bevacizumab manufacturing facility is delayed.

An Indian company, Biocon, is also working on oral insulin, but unlike Oramed it has not started advanced trials with the FDA, which is seen as the main path to the international market.