ADQ invests 550cr for 1.80% stake in Biocon biologics. Valuing biologics segment at $4.17B.

In November 2020, Goldman sachs valued biologics division at $3.94B

Biocon launched tacrolimus capsules in US.

Press release on Bicon Q3FY21 Results

Biosimilar segment witnessing improved interest from investors. It is valued at Rs 30420 cr and Investment on Syngene with holding co discount of 50% valued at 8400 cr (Mkt Cap). Balance segment (API & Formulations) with the revenue of 4400+ crores is available at the market cap of 14000 crores.

Disc: Invested

Here are my takeaways from the last conference call.

- Biosimilar business

o Insulin glargine (semglee) market share in US is still below 1%: It’s a formulary driven business and Biocon is trying to get its drug on the formulary list; Ramp up will happen next fiscal onwards

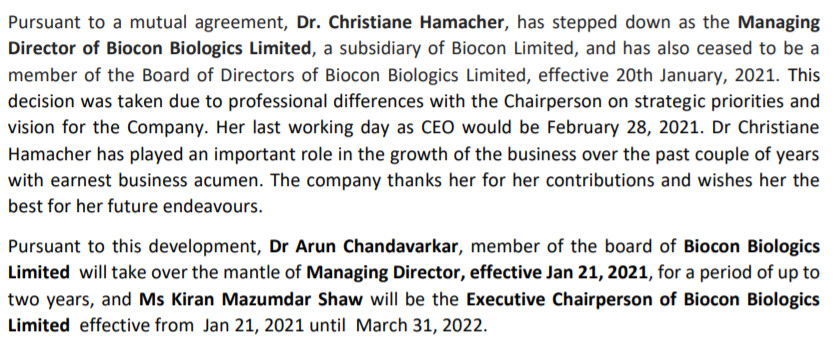

o Muted performance because of operational issues; CEO of biologics unit removed probably because of muted performance of biologics division; hospital patient visitation has gone down because of COVID

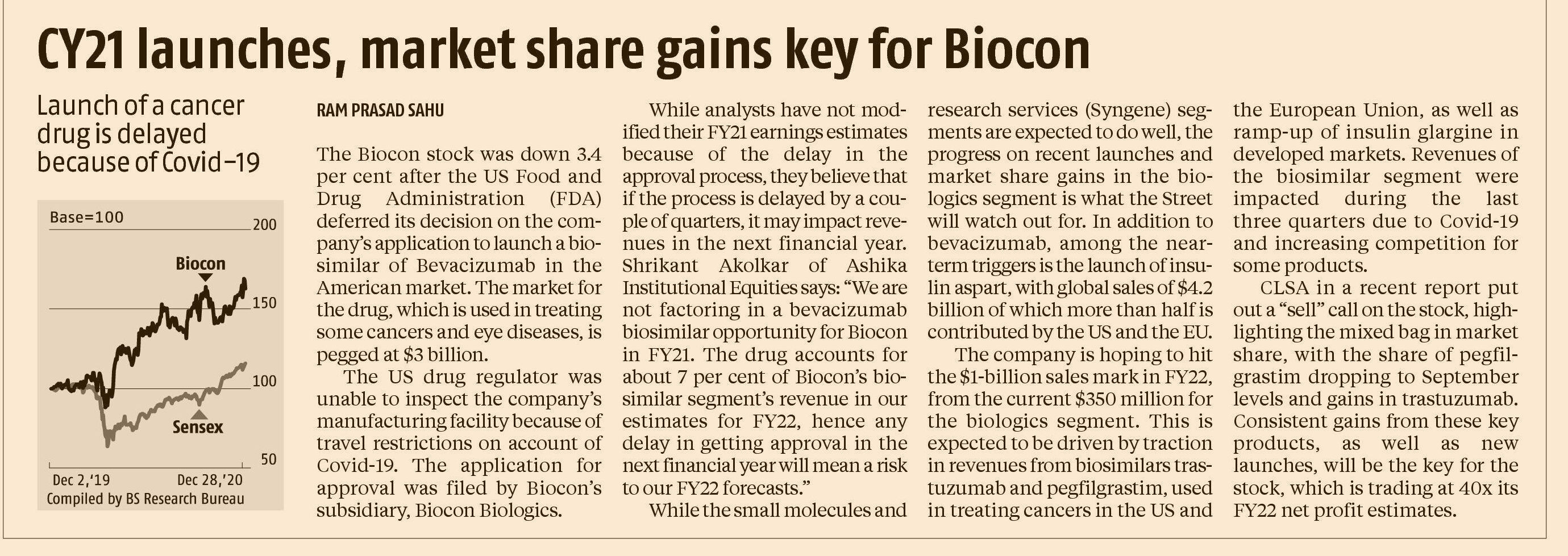

o Approval of Bevacizumab delayed because of FDA’s inability to travel to their site

o $1bn revenue target for biologics by FY22 will be revised not because of regulatory (US + EU) market growth but because of lackluster performance in developing markets where strategy needs to be revised; hints that the revenue target maybe delayed by 1 year

o Lot of emerging markets are tender driven which were adversely affected by COVID; Instead of new tenders being floated, a lot of older tender contracts were extended

o Price erosion in biosimilars is close to 10% every quarter in US (according to Nitya Balasubramanian; IMS data): Biocon has already accounted for these in their projections

o 3 of their biosimilars is close to entering clinical trials

o Dilution in biologics unit will go down to ~75% during IPO; will be similar to how Syngene was handled - Generics business

o gCopaxone: Will respond to the CRL in the next few months

o For the 3 statin products, market share is between 20-50% in US

Disclosure: Invested (position size here)

Q3 call - key take aways around misses.

Biosimilar

-

1Bn rev target had meaningful dependency in developing countries contributions( 60:40 for developed vs RoW), that part is lagging and a key strategic approach difference leading to exit of current CEO.( my inferences)

-

Risk due to sudden exit of CEO on strategy and org design as well as execution risks - Arun and Kiran being seasoned, there is no transition risk and continuity is assured.

-

How will growth strategy work- It sounded like between both of them ( Arun and Kiran) rest of world will get higher focus which was not happening till now and gap for aspirations of 1B rev targets - this makes sense as Mylan and Sandoz are driving Developed mkt growth, that means real heavy lifting from Biocon needed on RoW.

-

Biosimilar margin should show uptick as Most of Capex for medium term us over, only Malaysia plant ph2 expansion was called out for. This IMO is something that will partly give mkt what they are nervous about.

-

Although they missed 1B Target and IPO timeliness are also pushed - they were not in denial and attributed execution( RM, transport, RoW focus) issues as well mkt dynamics challenges ( tender delays in RoW mkt, FDA delays in inspection for Bevacizumab) - what is assuring is that now Kiran has put her neck on line to make it happen rather than hiring - there is always difference in promoter driving operations vs hired folks - they have called out 2YRS for new leadership - which would be where both 1B and IPO will converge - again a hypothesis.

Not much to Say about Syngene - firing on all cylinders and delivering,

-

90 new employees added in Hyd facility - at $60K/ yr - revenue to follow

-

Mangalore facility operating leverage to playout over next 10+ yrs

Generics -

-

Api vs formulations, 80 pc from API, 20 from formulations.

-

H1 was good as customers piled up, API rev came down in line now

*formulations some launch delays on FDA visit, formulations key growth driver for this group going forward,

-

API growth from immune capacity in vizag to come in once ready

-

mgmt focus has been Biosimilar, going forward this segment to get some more focus - this was not clear - maybe they meant increasing formulations contributions in mix

All in all - Lot of expectations were baked in high prices- short term there is pain - choice is to either trust mgmt and give few more quarters or log out and come back in on signs of green shots. Call was reassuring to some extent but on thin rope now.

Invested as part of core PF( biocon and syngene), for Biocon there is technical support around 370- 390 range, need to watch out. Syngene story intact.

Arun Chandavarkar was the earlier CEO of Biocon for many years. From my discussions with those that work at Biocon, Christiane was not a popular CEO. So this is not a major factor

If Biologics IPO gets same treatment as Syngene, then it means Biocon shareholders who have incubated the business all this while, will lose out…no proportionate shares like in a demerger + Biocon becomes holding co. only solace - IPO pushed out

Whether the existing shareholders will be getting shares in new entity ?

Covid is having an impact on all aspects of Biocon business, there is no doubt about that. I am surprised that Biologics have managed to grow at 11%. Most cancer treatments are postponed if the treatment is not urgent/lifesaving and this is having an impact on biocon, that is for sure

Share price has corrected by 20%. Market is overreacting to a temporary covid-related slow down, it is not going to last forever…

Discl - very biased, bought more today

Isn’t Biocon a massively undervalued business just on the basis of relative valuations.

The company owns above 70% of Syngene and above 90% of Biologics business. Just the sum of valuations of those two is more than its entire current market cap.

Why is it that the market has discounted the business to this extent?

First Salvo fired after Mgmt changes, this partnership gives biocon a preferred access and act as an influencer channel for MoW goals( Primarily Aftica and Asia). Biocon biologics $1B ambition has 40% coming from MoW countries.

Biocon Biologics to offer its Oncology Biosimilars through Cancer Access Partnership in over 30 countries, Will enable access to T

Simple SOTP valuation won’t apply here due to holding company discount applicable for Syngene & BBIL ownership in Biocon. Sometimes the discount can be huge & sometimes it can be less but generally 50-60 % is fair to assume. This holding company discount also came up in the L&T thread earlier.

Holding company discount is not purely applicable for Biocon as Biocon will have substantial core business even after divesting Biologics… Even Kiran Shaw talked about this too in her interviews… its like L&T, M&M, SBI, HDFC… which have valuable subsidiaries while having their own strong core businesses…

Exactly, holding company discount is applicable for firms like Berkshire and Tata Sons. These firms are just holding companies. Also, holding company discounts are usually applied to conglomerates with businesses in diverse sectors (like Tata Sons) and the discount stems from the logic that conglomerates are poor allocators of capital as they have business interests in many different sectors.

None of the above play out in case of Biocon. Biocon’s holding in Syngene and Biologics is still focused on pharma industry and Biocon still has substantial business of its own generating postive cash flows even if you take out Syngene and Biologics.

As Syngene starts making money, the flows will translate to Biocon’s EPS and that should significantly re rate the stocks PE.

I agree with the views @Tar but in this case I also feel that Syngene will grow better in view of the operationalisation of Mangalore unit.

Syngene definitely will grow faster but it’s revenues should translate towards consolidated balance sheet and PnL for Biocon since it holds a majority stake in Synegne.

My reason for investing in Biocon was mainly for their Biologics portfolio. The moment Biologics is listed I will sell Biocon and move my investment into that.

This is going to be a common action by many investors, which will increase the discount as we approach the IPO. Also, directly owning Syngene & Biocon Biologics has advantages as you can allocate weights to both these companies based on your conviction. In the holdco there will be a fixed proportion of both companies.