I am not comfortable with the figures of the Company. On standalone basis more than 95% revenue is from trading activity. On a consolidated basis also around 35% is trading revenue.

Company dedicated to R&D should not have higher trading revenue.

Disclosure: Not invested but tracking for academic purpose.

Trading volume is reducing. Good sign. FY24 would be superb for this Company when other Agro company are struggling with old Inventory and China dumping issues.

Not sure if this is confirmed news–search found only one tweet on this, and in this tweet the source is not specific. If this is confirmed, why hasn’t this been notified to the exchanges yet?

(Not invested. I have only theoretical interest in this stock; not considering for investment. For reasons, check my earlier comments in this thread.)

Let’s wait for a day or 2. Neither there is exchange filing nor media reports. If it turns out fake, we will know RedBoxIndia is not reliable source of info.

And there are people who make money, if it’s fake news

Great work done by @Anand6 and others about Raj Kumar.

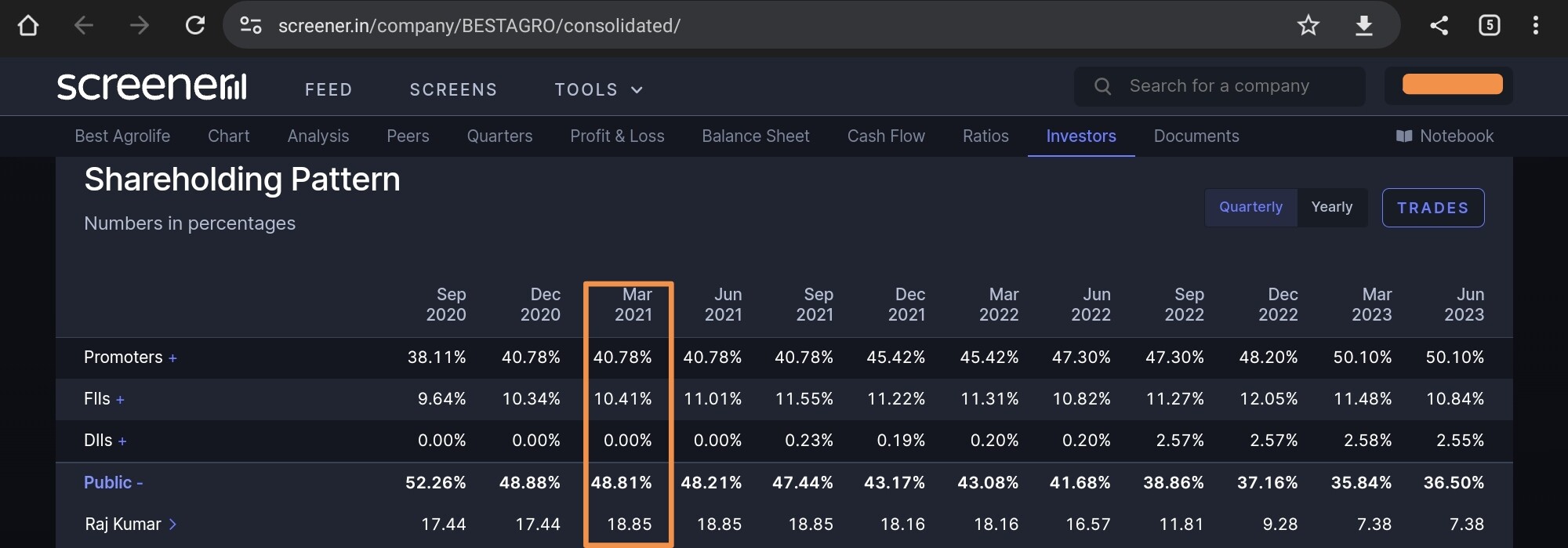

Raj Kumar, large public shareholder who has been continuously selling, has DIN 02793669 and PAN ABCPK4370L. This PAN can be verified from the latest Shareholding Pattern page 16 available on the company website.

Now, as per the link below, Raj Kumar was a director of Best Crop appointed way back in 2010. So, clearly Mr Vimal Kumar, promoter and MD, knows him. Yet, he has claimed in interview to CNBC that Raj Kumar is unknown to him.

Some people are pumping this stock but many seem to be in for a rude shock.

Can someone please explain the reason a company would not list on NSE in first place? Also how much time.does it take for approval of listing? I’m of the view that once it lists on NSE volumes will increase dramatically

Very irresponsible from the company to not inform the exchange when an IT raid has taken place.

Seems a bit fishy especially when they claim they have nothing to hide.

Raj Kumar is a director in BEST BUILDCON PRIVATE LIMITED and BEST CROP SCIENCE PRIVATE LIMITED

Raj Kumar was allotted 17% of the company in FY21 under the scheme of amalgamation. This means he had a large shareholding in the previous/amalgamated company along with the promoters.

Now, Raj Kumar is selling his holdings in Best Agrolife. Not a small percentage of his holdings but more than majority of his holdings.

A word to the wise is enough. Samajhar ko ishara kafi hai.

Interesting. Digging more using this information, I found BEST BUILDCON PRIVATE LIMITED currently having 3 promoters, RAJ KUMAR, ANKIT BHUTANI & SAKSHI RAJPAL.

Would it perhaps not be more relevant to look at total share holding change in the promoter + Raj Kumar group since the issue is Raj Kumar is defacto one.

Since peak holding of end March 2021 of the grouping considered, the total fall till date is by 2.15%. This may look serious, though depending on your risk appetite.

Since peak holding of end March 2021 of the grouping considered, the total fall till date is by 2.15%.

This would have more weight if the shared were acquired using cash in the open market. In reality, “off-market by way of gift” (God knows what this means; who gifted and why?), “inter-se transfer” (between the old promoters and the new promoters) and “preferential allotment” (during acquisition of companies) are some of the ways in which these shares have been acquired by the promoters (and Mr Raj Kumar). Hardly any shares have been acquired in cash.

In contrast, the sale of shares by Mr Raj Kumar, who mysteriously is not in the promoter group even as prominent director in the group companies and designated partner in one, has probably been in the open market for cash.

What I read is that the promoter is not really the promoter?

Tanla had been universally labelled big fraud by this forum. I don’t really understand if the business is money spinning then what use of virtue signalling?

If the business is money spinning, why is it trading at 11 PE?

Can it get to 40 PE like PI Industries?

Should it be taken as an investment position or a trading position?

How is it that they are projecting a much more rosy picture when compared to the rest of the industry? Are their projections believable?

These are some questions an investor may be interested in. I thought the purpose of these forums is to discuss such questions. That’s what I am doing. Who is doing virtue or vice signalling is for the readers to decide.

I think the major problem with them is cash conversion.

On this cfo says will look after a year to get in shape currently rev grwth is focus.

Sale is credit hmmmm