QOQ growth seen, seems like the recovery in Agrochem sector is near

3 Likes

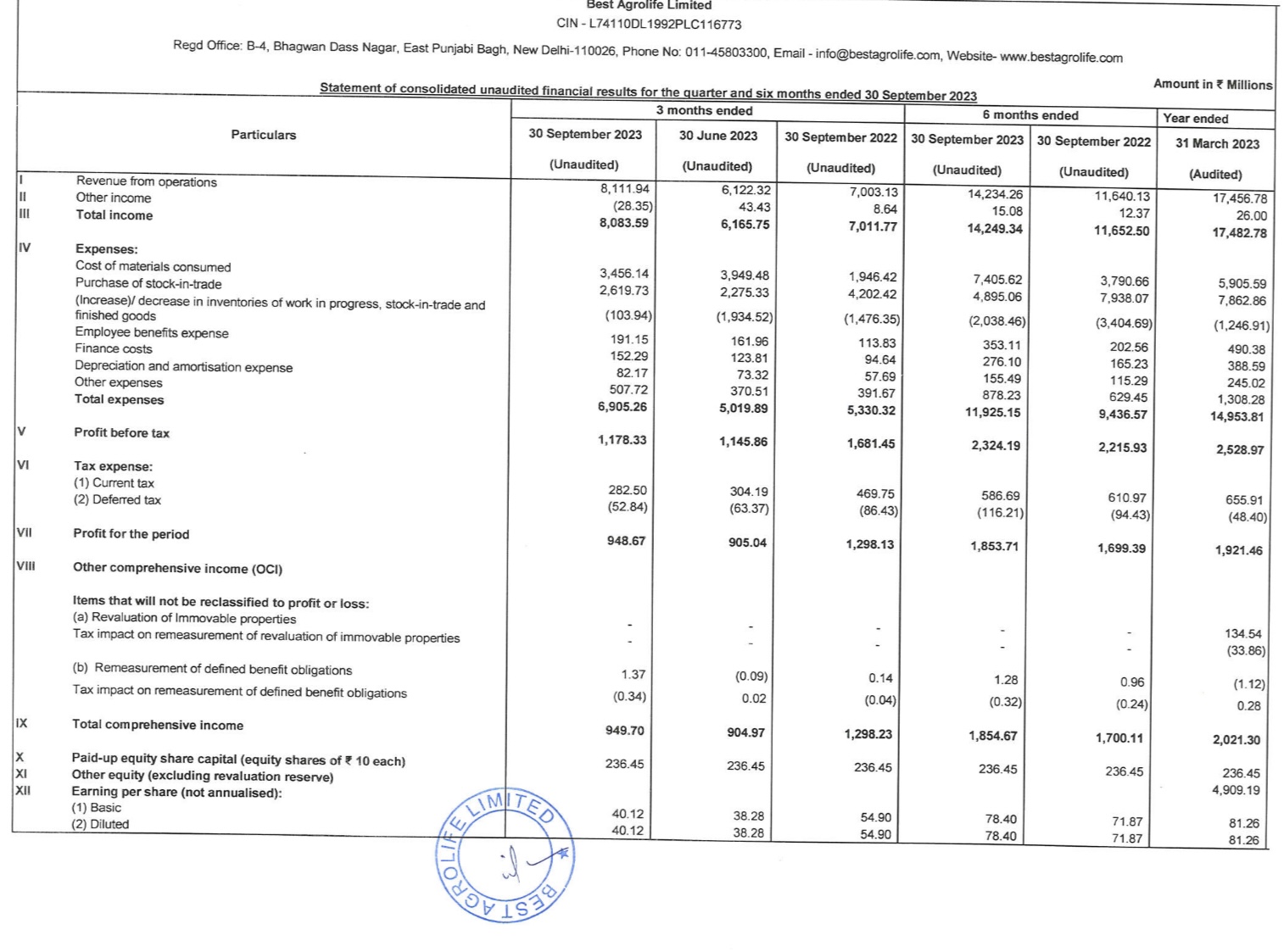

Why is stock 8% down ?

Margins dropping from 11 to 6% ?

margin have dropped and receivables have increased to 1011cr

1 Like

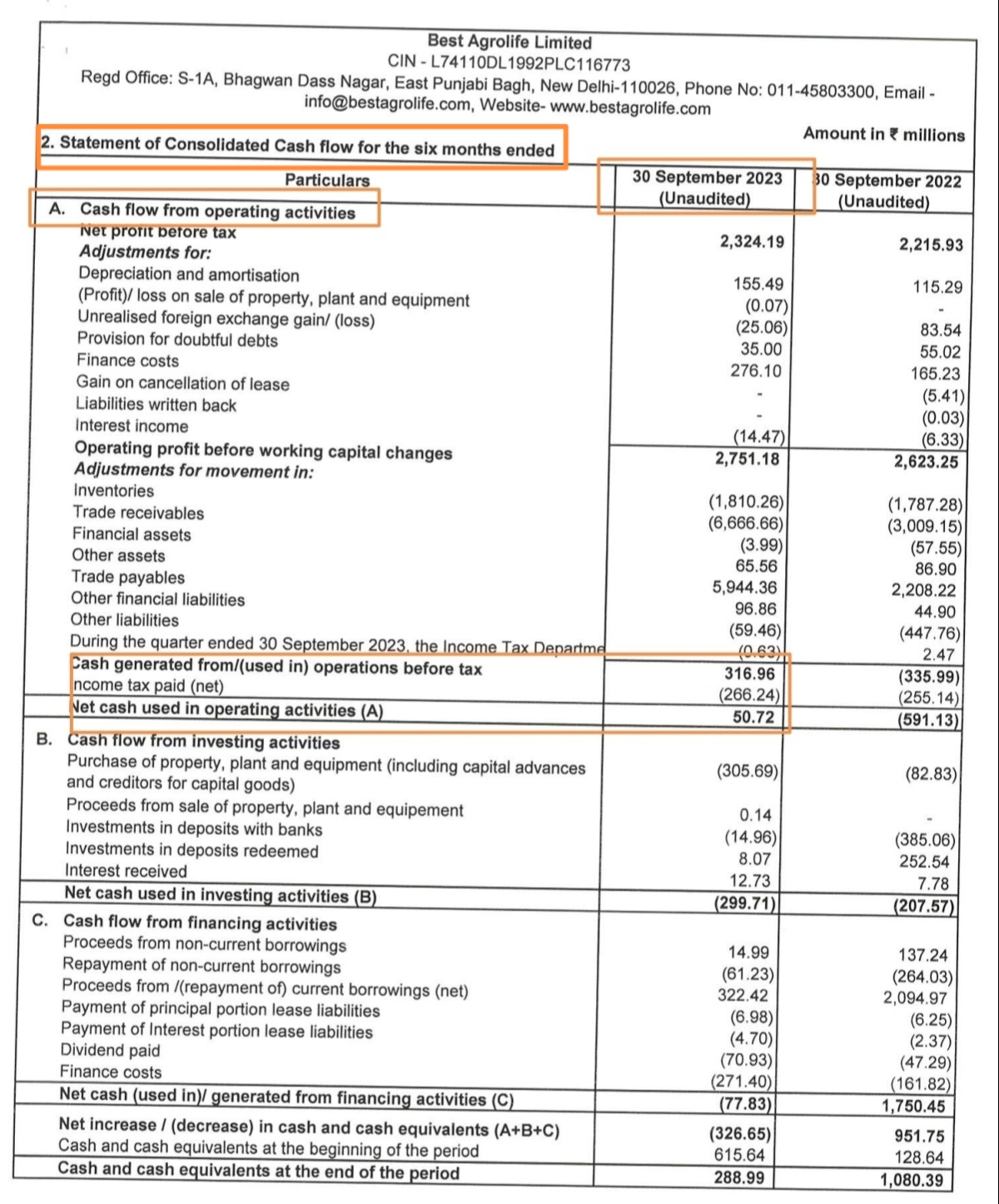

Inspite of profit of Rs 232.4 Cr during H1 ccash flow from operation is negaitve… Recievables have increased to Rs 1011 Cr…Trade revenue is around 32%.

All are red flags for me…

Disclosure : Already exited 1 year back due to lot of red flags.

There are so many investment opportunities and one can avoid investing in such kind of stocks and if invested it should be less than 1% of your portfolio

Stand alone Cash flow from operation is negative Rs 48.6 Cr and at Consolidated level also out of Net Profit before Tax of Rs 232 CR for H1, Cash flow from operation is merely 5 Cr. …

I would stay away from such Company and more than happy to loose 1 multibagger like Best Agro.

2 Likes

Ignoring the obvious red flags present, such as, aggressive accounting practices, increasing receivables, headwinds in the agrochemical industry, depleting margins, recent IT raids, I would still like to look at certain positives. All views and opinions welcome.

- Management confidence in achieving 20% Ebitda margins

- Continuous launch of new products that are expected to contribute to margins in H2FY24

- Plans to explore opportunities in SE Asia, Middle East and Africa

- Acquisition of Kashmir Chemicals (to meet growing demand)

- 20 years patent for its subsidiary

- Capex for backward integration

Also, reading the concall transcript has given me a little bit of confidence in the management and a belief that the company is possibly headed on the right path.

The stock is currently in a free fall and my thesis may be wrong but I feel the business model is strong and fundamentals are expected to improve next quarter or maybe 6 months onwards.

6 Likes

Yes you are right at this point.

I also have gained confidence after reading latest concall about improving the financial in next 6 months or in a year.

1 Like

Before q2 result stock was trading at Rs 1100 level now trading at Rs 785. As someone pointed out that receivables increased to 1012 cr and negative cash flow are red flags. Are these two factors so strong that stock will correct 30%? In last 2 months they acquire Kashmir Chemicals also which will increase top line by another 100 cr. I just want to know is there something else is cooking which a common investor is not aware?

A company with a ROCE of 34%, ROE of 45%, PE of 9, CAGR of 45% is beaten down so much that too in a mad bull run is unthinkable.

Appreciate any valuable input.

1 Like

The receivables is the problem here

Generally Agro Chem are sold through distributors. The Co pushes the distributors to buy and stock their product. What ever quantity supplied to the distributors is shown as sales and they show profit on it.

To increase the sales, the co sells the product without cash upfront. The distributor repays the amount later (this is shown as receivables in balance sheet).

The distributor will return the product he’s not able to sell. So, the Co needs to reverse the sales that means whatever sales they’ve shown earlier are reduced now.

This exactly is the problem here. As long as the co doesn’t get back the receivables, there is a chance of reversal of sales and profit.

So, we can’t judge the sales shown in p&l statement as true sales and same for the profit

22 Likes

Thanks a lot for clearing doubts.

FII are selling ,DII are selling, Smart investors like Ashish Kacholia has also reduced his stake, but retail investors are increasing stake considering it will be a multibagger. Look at the Charts and red signals. You have other stocks also to make money …

Disclosure: Exited long back due to several red flags … Please readearlier comments

7 Likes

General update.

1 Like

Stock 12% down after results… Any update on receivables ?

Does anyone have any clarity on:

- How on earth their Q-3 Dec, turned out to be so horrible.

Homogeneous drop Q on Q drop in topline in excess of 50% Q on Q means there has to have something horrible happened in their business or imply the previous few quarters were one off.

YOY is terrible as well.

Depleting margins both q on q, and yoy

There must be some sort of explanation/ justification for that?

Is there any guidence by the management to clock in excess of 2000 in topline with a margin guidence of around 15-18%?

Dicl: intresting stock to watch out for, in process of due diligence before jumping in.

Seems like the sector itself is in bad shape. Its peer UPL (Nifty 50 stock) is also showing weakness.

1 Like

At the cost of repetition…

FII are selling ,DII are selling, Smart investors like Ashish Kacholia has also reduced his stake, CFO has changed, whole time director has resigned, Finance cost increased, borroiwng increasing, no concal in last quarter, sales and margin both are declining with PAT losses… but retail investors are increasing stake considering it will be a multibagger. Look at the Charts and red signals. You have other stocks also to make money …

Disclosure: Exited long back due to several red flags … Please read earlier comments

7 Likes

17c87d70-87dc-4a6b-9948-119b3d0b879c (1) (1).pdf (1.2 MB)

Acquiring a non performing target company with same set of promoters , in cash deal( related party transactions)

It is a cause of concern, Can promoters be trusted?

Results are horrible.

Couldn’t by any worse.

No investment rationale coming into play on this counter as on today!

Yes, they are just using public funds in a very wrong manner. The company they acquired is already like their own company and they have bought it at astounding valuations and are using public funds to acquire them. All of this is just wrong. Would heavily tell anyone to avoid this company.

1 Like