I am not an accounting/audit expert so can’t comment where exactly the problem is in operating cash flows (other than inventory and receivables) and hence posted my query.

We can justify that receivables / inventory as a ratio to sales are under control, etc. But the problem is still the fact is that the cash flows are negative since last some time. I am not saying there something wrong or right fundamentally with the company, just trying to evaluate the reasons.

Also note the increase in Trade Payables (Rs 220 crs, equal to its net profit before tax for 6 months ending sep 22). Sooner or later company will have shell out money to pay this.

Hi Ashish! Very good company and you caught it much early. I just want to get an idea of your thought process on this company like how you look at it? a.) Company which enjoys super normal growth for some period and then growth starts maturing or even starts de growing as some molecules fail or may be competitive intensity in some key moecule increases. So is tracking this company molecule or say some of their key product wise is the right way? If it is can you suggest some sources where it can be tracked. b.) Consistent compounder wherein existing sales is safeguarded by some means and new sales is generated as time goes by company’s moat and it goes on growing as the time goes. I mostly think it will be in the first category but if you have any alternative views. Just wanted to know your thought process.

Quick comment: The only difference with Best Agro (vs other formulators like Dhanuka) is Best Agro is doing three way combinations vs others selling two way combinations. This is because Indian government started approving three way combinations only recently, and Best Agro has a first mover advantage. There has also been some allegations against Best Agro as to how they are the only ones getting these registrations in very quick time (less than a year for 9(3) registration is unheard of, it takes 2-3 years generally).

Best agro is also importing the intermediates (largely from China), getting Ravi Crop to convert it into a technical, and then making their own formulation in their Noida facility. This is exactly what everyone else does. So, they are not doing anything different per se. Their patents are for combination of different technicals, and not for new technicals. Its important to differentiate these things, while also recognizing that they have been doing well due to 3-way combinations.

Disclosure: Not invested (no transactions in last-30 days)

Rightly said. So, product like Ronfen has a global patent for 20 years. So, we can’t expect any competition in these combinations for 20 years not only in India but also in other countries if I am not mistaken. However, was there any patent for two-way combinations by any Indian players in the past if @harsh.beria93@ashurathi any of you have any idea. I think it will help us to understand the competitive intensity it can get. Obviously, it would have cost advantage compared to just the seller of Solo Technicals. Also going for backward integerations and manufacturing technicals will surely give an edge in future.

Thanks for sharing your perspective. While working on the company, I couldn’t understand a few things and will really appreciate your perspective on them.

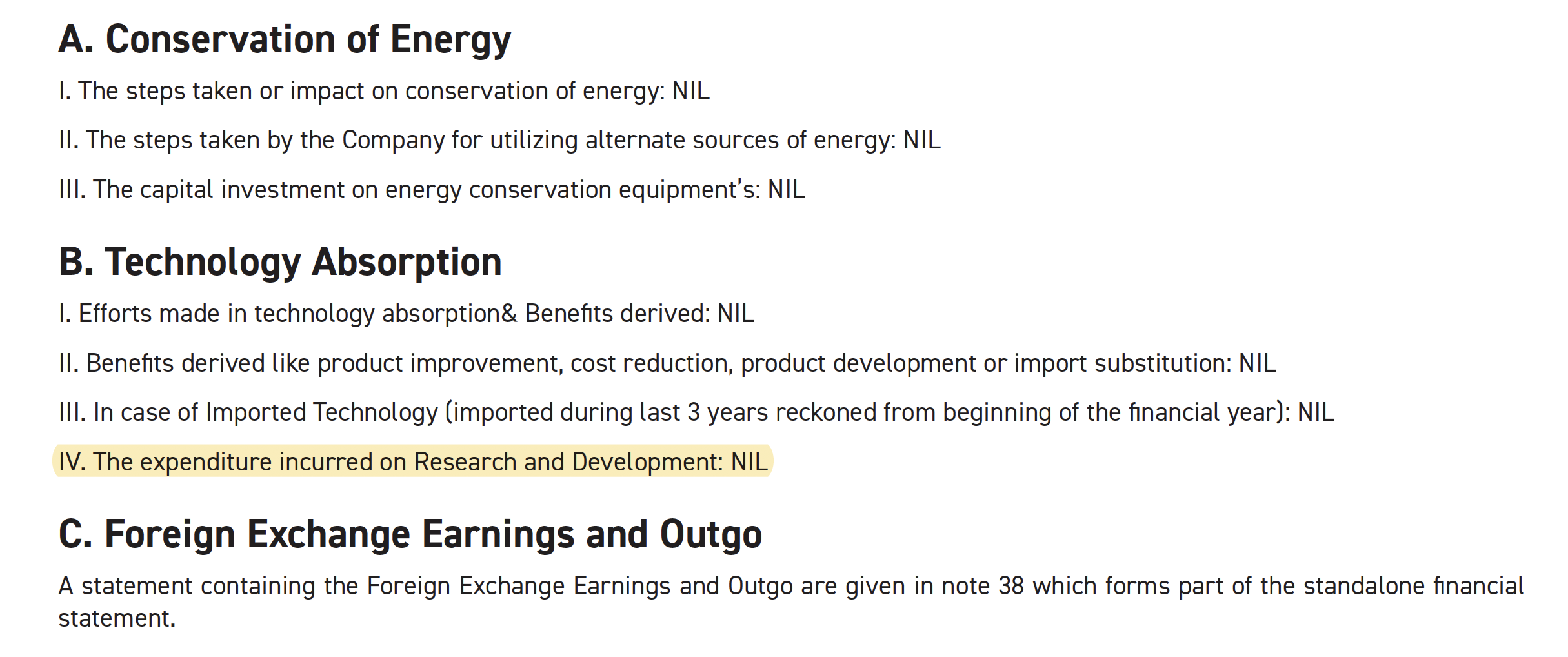

1. R&D costs

Do you know why Best Agro’s R&D costs are mentioned as zero in their annual report? I imagine that generating trial data for getting patents and registrations will require some investments. What is the line item that this will get reflected in?

2. Freight outwards expenses

Their freight expenses are very low at 2.6 cr given the size of their business. Dhanuka, which is of similar size in terms of topline has freight expenses of 39 cr. Why are these so low for Best Agro?

3. Other expenses

Best agro has other expenses of 36 cr. on topline of 1211 cr. vs 155 cr. on topline of 1478 cr. for Dhanuka. Does such low other expenses imply that they are largely trading in agchem segment?

Also, their audit fees is on the higer side at 45 lakhs (vs 21 lakhs for Dhanuka which has higher revenues).

4. Consolidated vs standalone nos

I was also looking at H1FY23 results, and couldn’t reconcile (consolidated - standalone) numbers.

On a consolidated basis, revenues were 1164 cr. and EBITDA was 249 cr.

On a standalone basis, revenues were 1009 cr. and EBITDA was 100 cr.

So if I wanted to understand contribution from subsidiaries (consolidated - standalone):

Sales: 1164 - 1009 ~ 155 cr.

EBITDA: 249 - 100 ~ 149 cr.

How are their subsidiaries making such high EBITDA margins (close to 96%)?

If you can help me reconcile these numbers, it will be really useful. Thanks in advance.

Given that we are both invested in RACL, i think we will appreciate that not all cos point out R&D expense in a line item separately for R&D. See notes from July Concall

I vaguely remember seeing this in Gufic too. In fact most indian cos ive seen are not very fussy about where to put true R&D expenses most just seem to fill it with “nil”. Now that Co is doing concalls, interested investors can always ask in Concall about level of R&D spends & headers where these occur.

Freight accounting is quite diverse from what I have seen. Many cos dont account since freight is borne by distributor or customer or retailer. Definitely an important question we can ask management in concall.

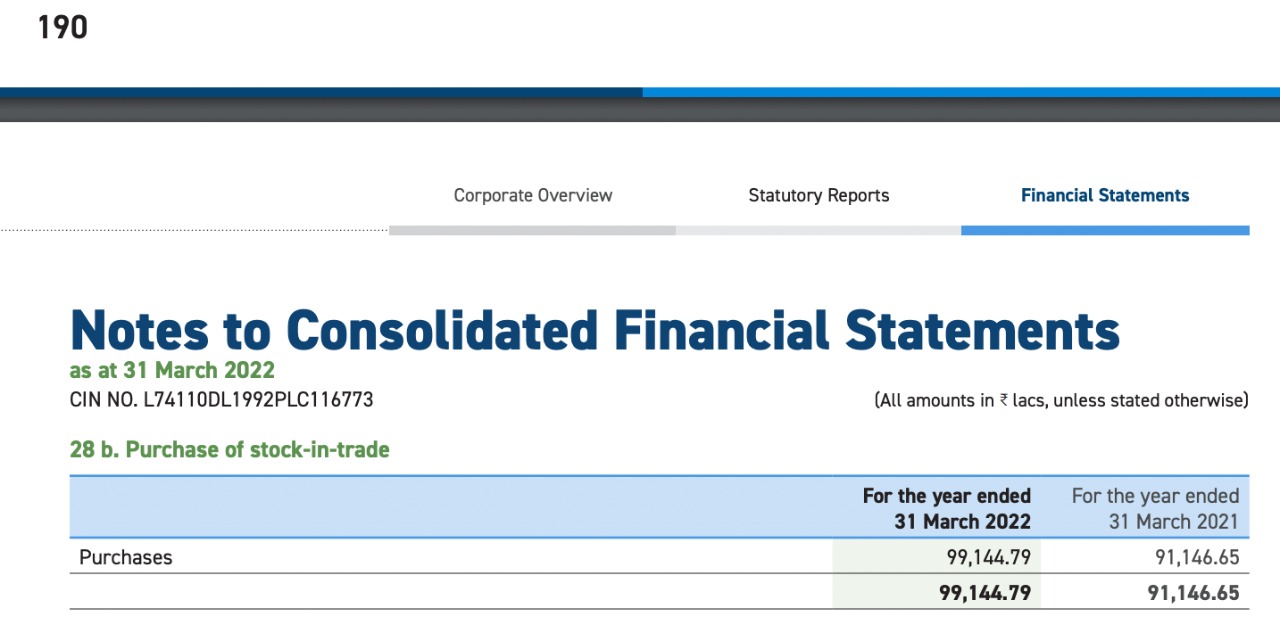

Definitely yes. Also see the purchase of stock in trade for BAL which is quite high.

This clearly shows that a large part of their revenue is based on purchases of off the shelf products (i assume at least AIs and potentially formulations as well). Another key question to ask management.

I think this one is relatively easier to answer. I have seen several instances where co does expenses for sub from parent P&L & vice versa. This is definitely not clean accounting but as long as Sub & parent are working towards same goals, id just analyse consol P&L and not break it down too much (unless i am confident of accounting hygiene)

Question to ask is whether and how much of these negatives are discounted by valuations.

To me personally, the biggest red flag is the cashflows which are non existent. Given their large push to B2C, the receivables specially are quite concerning. I do remember that BR had similar cashflow concerns and once cashflows came in, stock did quite well as investors confidence improved. A key monitorable IMO.

In short, im afraid investors cannot. Only management can. I encourage you & every other investor to join the public concall & ask these questions, i think that is best way to proceed.

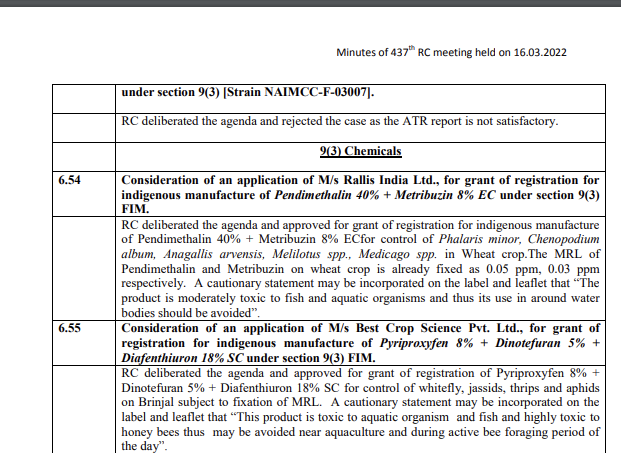

On the positives side, one can definitely checkout http://ppqs.gov.in/ to confirm that indeed, co’s products are being approved by Govt. Eg: Consider http://ppqs.gov.in/sites/default/files/minutes_62nd_cib.pdf

MINUTES OF THE 62

nd MEETING OF THE CENTRAL INSECTICIDES BOARD

(CIB) HELD ON 09.05.2022 AT 1400 HRS THROUGH VIDEO CONFERENCING.

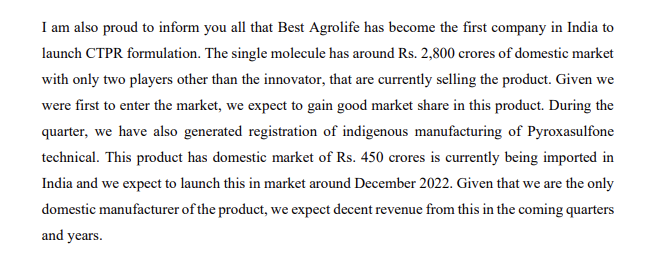

I think harsh’s notes while quite gooddo miss out on a few critical aspects of the investment one can derive from the concall. Most important is that co has a pipeline of 20 odd products which are similar in size & scope to Ronfen.

I think the accounting concerns are quite genuine, dont give much confidence. The risk of capital loss is high (what if co is outright fraud & all numbers are cooked up). This is why valuations are also quite poor. I do think it is worth diving deeper, because the upside is also asymmetric (if one can simply establish some confidence in co not being outright fraud).

I will try to visit their factory when i can (the one in Noida). Will try to attend their next concall too.

Disc: Small position of 2-3% only to be scaled up if higher confidence in accounting & cashflows can be established. To be exited if co seems to be indulging in outright fraud.

Positive:

Company started concal.

E&Y as Investor Relation Agency

Hosting Calls with Mutual fund.

Company is in a regulated industry and its not easy to make blatantly false claims in this sector as all registration and other details are available online.

Patent of formulation and process can be verified.

Formulation/Technical approval and registrations can be verified online.

Mutual Funds are invested

FIIs are invested.

Promoters buying at current levels also and increasing their shareholding.

Negatives:

Hard to believe the capabilities of Company with so low spend on R&D.

But then patents and registration of technicals and formulations are there to support their claims.

Consideration of application of M/s Best Crop Science LLP for grant of registration for

Technical Indigenous Manufacture (TIM) of Thiocyclam hydrogen oxalate technical

86.00% w/w min. u/s 9(4).

Consideration of application of M/s Best Crop Science LLP for grant of registration for

Technical Indigenous Manufacture (TIM) of Kresoxim methyl technical 94.00% w/w

min. u/s 9(4).

Consideration of application of M/s Best Crop Science LLP for grant of registration for

Technical Indigenous Manufacture (TIM) of Sulfentrazone technical 95.00% w/w min.

u/s 9(4).

198996 BEST CROP SCIENCE DINOTEFURAN 20% W/W SG Satisfactory

Based on above message, I came to know about GSP crop. Planning IPO next year. By just adding Suspo-emulsion (I am not expert in agrochem field, and writing this just based on observation in news articles), co got patent for Pyriproxifen and Diafenthiuron combination similar to Best agro (dual combination vs triple for best agro) despite strong opposition from best agro legally.

This shows patents are fragile and sometimes difficult to protect. same company is behind CTPR, too!!

This co is also having turnover of 1200 crs or so, in the range of best agro.

better we focus on marketing at ground level, and who is winning there as multiple players can do the same, so there won’t be monopoly as such.

4. Consolidated vs standalone nos

I was also looking at H1FY23 results, and couldn’t reconcile (consolidated - standalone) numbers.

On a consolidated basis, revenues were 1164 cr. and EBITDA was 249 cr.

On a standalone basis, revenues were 1009 cr. and EBITDA was 100 cr.

So if I wanted to understand contribution from subsidiaries (consolidated - standalone):

Sales: 1164 - 1009 ~ 155 cr.

EBITDA: 249 - 100 ~ 149 cr.

How are their subsidiaries making such high EBITDA margins (close to 96%)?

As per my understanding:

You will have to adjust inter Company sale of around Rs 220 Cr which will effectively give contribution of around Rs 375 Cr in sales from associates and margin will be around 42%

I had got the number from Related party transaction report

Standalone sales : 1002 Cr

Consolidated : 1164 Cr

Sale of subsidiries : Rs 597 cr as per Auditors remark.

So inter corporate sales should be : 1164-1002 =Rs 162 Cr and after adjusting

597-162 = Rs 435 Cr

Inter corporate sales should be Rs 435 Cr , however as per related party transaction details furnished by the Company it is not matching up.

Best Agrolife standalone Sales of Rs 1000 Cr is purely trading sales as it is only a trading Company .All manufacturing sales are from subsidiaries, however figures are not matching up.

It reminds me of Manpasand Beverages:

On a consolidated sales of Rs 1164 Cr if around 1000 Cr are trading sales, what valuations should it command ???

Further trading margins are generally 3 to 5% whereas in case of Best Agro it is substantially high.

I had contacted many retailers but none of them had RONFEN or any other product of Best Agro.

Disclosure : Invested with a small tracking position.

Not a big fan of accounting but at least broad figures like sales should should be reconciled on a standalone and consolidated basis after taking into the effect of inter corporate sales as per the related party transaction disclosure made by the Company.

When there are exponential growth in sales and margins these reconcilations become more relevant for me…

It is not feasible to do the reconciliation like that for any company.

Consolidated Financial Statements can’t be deduced based on a related party transaction disclosure, simply bcoz RPT disclosure does not provide sufficiently complete info for carrying out that task. For example, transactions between subs aren’t disclosed in RPT disclosure, but one wud need that info when consolidating bcoz transactions between sub & sub wud also need to be eliminated along with the ones between parent & sub.

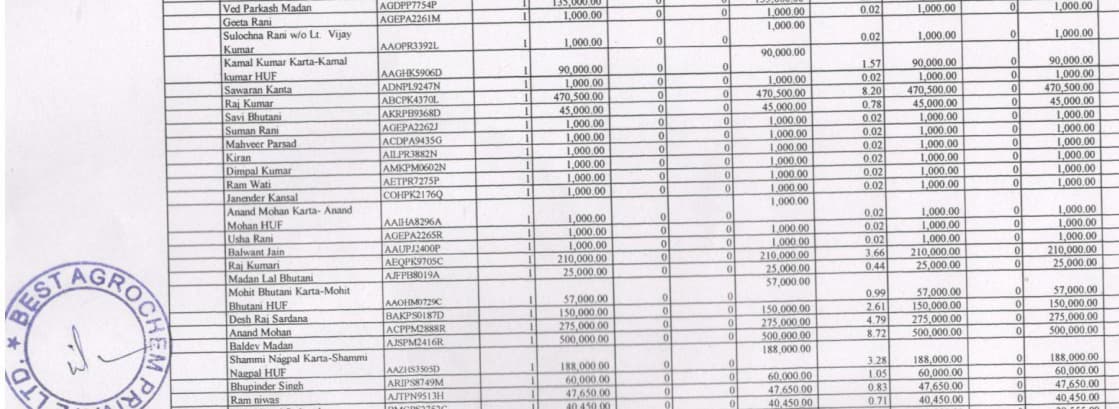

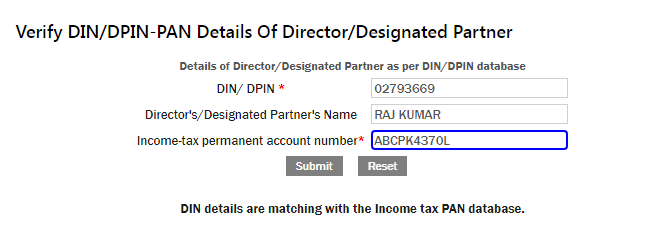

One of the major Public shareholder is Mr Rajkumar with holding of around 11.81%. Mr Vimal Alawadi in one of his interactions confirmed that they are not aware of retail investor with name of Mr. Rajkumar.

In social media I had read that as Mr Rajkumar has large shareholding he can and is manipulating share prices( source not verified).

Related party of the listed entity are Best Crop Science Pvt Ltd and Best Crop Science Ltd and they have a Director with name Raj kumar. I have not verified whether retail shareholder and the Director are one and same entity.

Share holding of Rajkumar is appearing since june 2020, the same time after which promoter shareholding has also increased from 5.10 to 38%.

Now biggest question is … Is this a red flag or not?

In an interview, Promoter has said “Raj is not related to promoters and he is an investor and promoters are not aware of his future plans”. Promoter is neither accepting nor denying connection with Mr Raj !!!

Now a days it is a new fashion where even promoters are openly selling to some well known investors, its upto individual how he/she reads this.

Another Raj kumar associated with Sidhivinayak Chemtech Private Limited is different person as per matching with PAN card.