I have made some edits to my comment above from earlier today. So, I was wrong about the revenue contribution from Best Agrochem amalgamation being incredible.

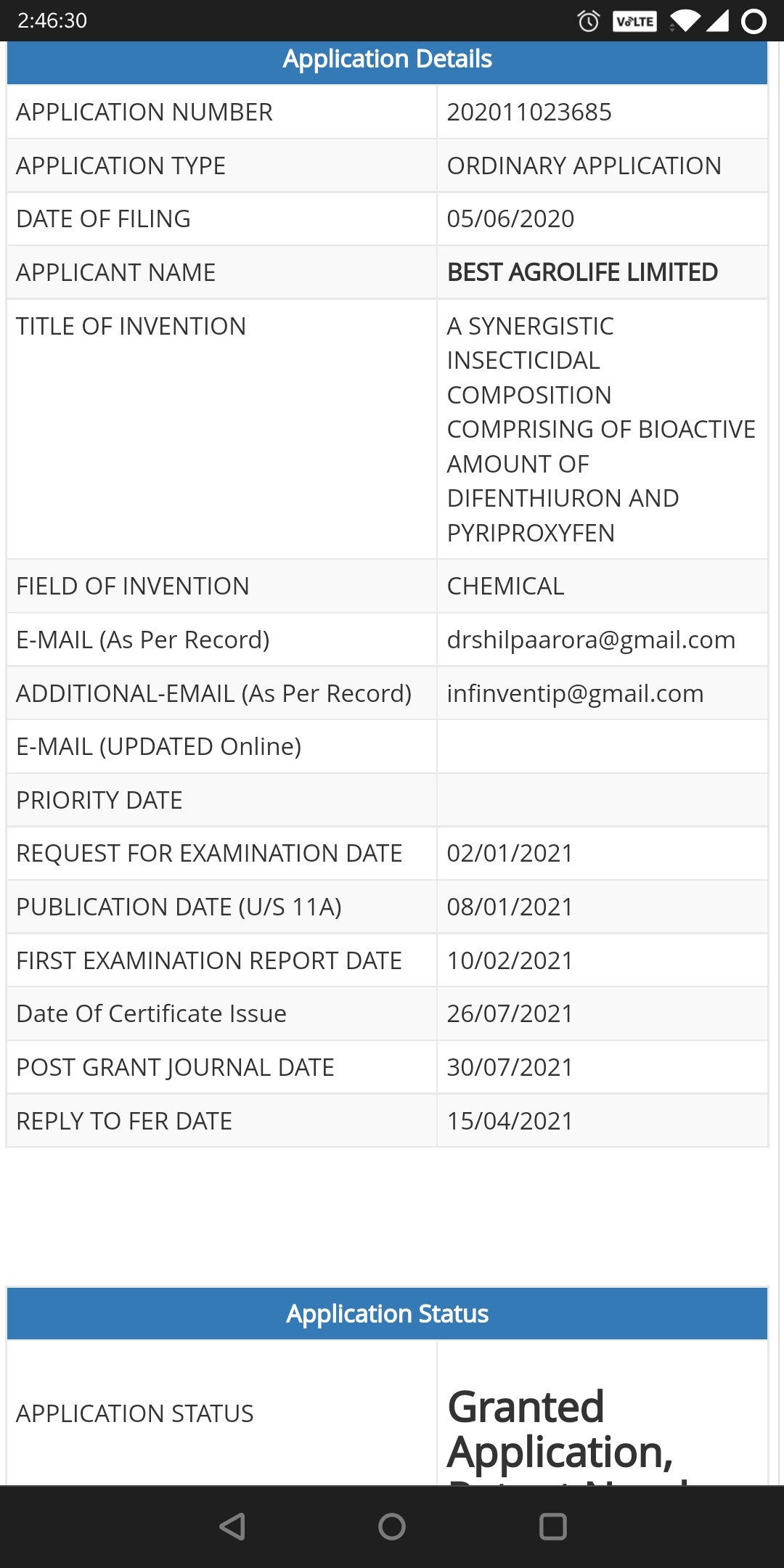

Earlier, I checked the patent filing by the company recently in the news via the Indian Patent Search website. This also does check out fine.

I want to conclude this discussion from my end. Based on my evaluation so far, the company does have at least some substance although the corporate governance is not the best. Right now I am not very pessimistic about the company but there is a lot of lacking information. The revenues and growth still look incredible to me, so personally I will stay away. If true, these are really great performance by the company. It would be interesting to watch how the story unfolds.

Yes, totally agree with what you have said. Without trust, conviction building is impossible and I respect your say in it.

Being small cap, we have to be extra cautious with it. I have build up my conviction with lot of studies in this company. Will have a wait, hold and watch approach with the company until I get answers to some of the questions you have raised.

I am relatively new to investment, recently studying best agrochem. And i came accross this related party transactions list, loans are being given to subsidiaries of huge amount, co is paying rents to individuals from co. What can be made out of this? Inputs will be helpful. Thanks…

Key positive

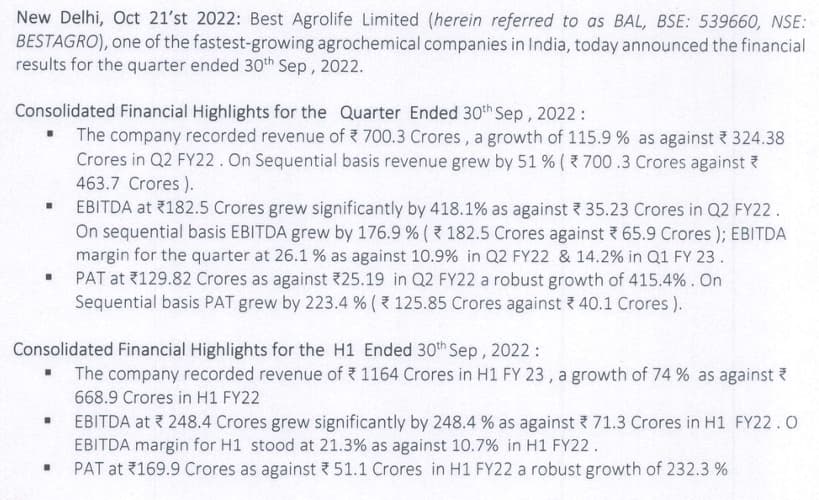

Company has given a guidance of revenues of Rs1500crs + for FY23, 20% + margins and Rs220crs PAT in this interview. At Rs220crs PAT company is trading at current price of Rs1265 at Rs2991crs (market cap)/ Rs220crs = 13.6x P/E FY23. 1Q profit at Rs40crs.

Key negative

Stretched working capital because company growing fast and introducing new products. Unlike to normalize till company growth slows down and company focusses on WC instead of just growth

Thankyou @Tanay_Malpani for the research. Would be thankful if you can tell how did you identified this company? This doesn’t show in any of my screeners because of less number of years but still it would be interesting to know how did you found Best Agrolife.

Chemicals/pharmaceuticals has remained my Achilles Heel. What I understand is that agro chemicals are now commoditized. In such a scenario how does Best Agrolife command such high ROEs? How are their products different from already existing agro chemicals? From their growth it looks like these products work like magic.

Thank You @Patel_Bhai for your appreciation. As discussing about the screening of script is not a relevant topic to this thread, lets discuss this in personal chat via the message feature here.

Let me try to give my opinion on Best Agrolife commanding such high ROEs -

Company is in a super growth phase at this moment which is likely to continue for a few more years. In a recent interview, Mr. Vimal mentioned that 28 new products are in the pipeline and will be launched in phases. As such, new products every year is confirmed for the next few years.

Now is this confirmed that these new products will be successful! Here, we can only talk about the probability and as such it is highly probable that these products will be successful majorly. I am asserting this because of two reasons. Firstly, Best Agrolife are analyzing the gaps in the agro-chem space and this dictates their R&D findings. They are focusing beautifully into molecules which are not manufactured in India but imported from abroad. As such, filling this gap provides cost efficiency to their clients as well as their home brand - BEST. So, MNCs prefer sourcing molecules locally rather than internationally. So, the offerings of Best Agrolife naturally comes into demand.

Next, the company is focusing on discovering unique products. For , example one shot product for various crop problems. These will be well sought by farmers as it provides them a great opportunity to save on buying multiple crop protection products. For this, Best Agrolife needs to excel in just one thing i.e. reaching to the farmers. Once they do it, halo effect and stickiness will follow.

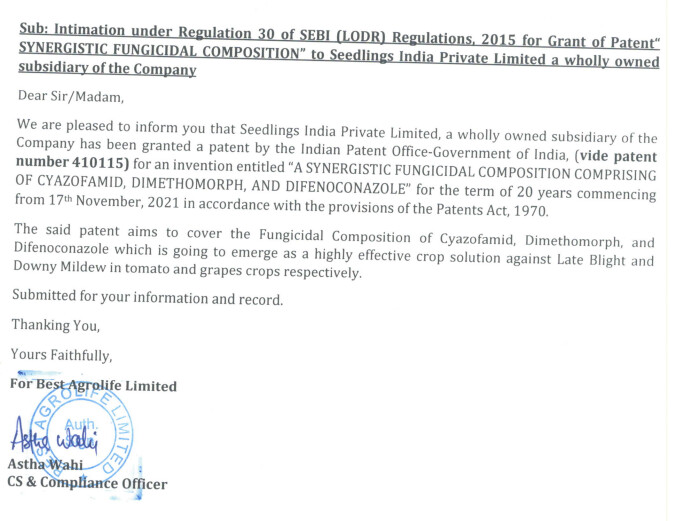

This is the most important point . The company is heavily invested into consolidating its backward integration. This is what maximizes its cost and operational efficiencies. In fact, just today, they disclosed that : “This is also to inform that Seedlings India Private Limited, a wholly-owned subsidiary of the Company shall further increase its formulation capacity by putting up an additional herbicide unit with the proposed capex of up to Rupees 25 Crore which shall increase value addition by Rs.300 Crore.” Now, this ensures cost efficiency and boosts their top and bottom lines.

With these factors empowered by the company’s fantastic R&D capabilities, the company can deliver the 30% topline and 20% EBITDA growth as promised. As, I have said since the beginning that the Moat of Best Agrolife is its R&D capabilities, the company is well in place to deliver with high efficiencies resulting in high return ratios - ROE, ROCE,ROA.

With its farmers first approach , the company is delivering what the farmers actually need. With the molecules being “Made In India” , the cost of the final products comes down and hence affordability for farmers increase. Also, 40% of company’s revenues comes from tie-ups with various MNCs such as Bharat Rasayan, Mahindra,etc to which they provide molecules/ technicals on a B2B basis. The rest comes from the BEST brand. As such, even when competitors grow, the company’s income grows. This is another MOAT.

I hope I have answered reasonably to the query. Also, this has been a week when good things have happened with Best Agrolife.

“Seedlings India Private Limited, a wholly owned subsidiary of the Company has introduced two new CTPR-based formulations, CITIGEN and VISTARA, which are intended to combat harmful insects in various crops including sugarcane and rice”

“This is also to inform that Seedlings India Private Limited, a wholly-owned subsidiary of the Company shall further increase its formulation capacity by putting up an additional herbicide unit with the proposed capex of up to Rupees 25 Crore which shall increase value addition by Rs.300 Crore.”

In an interview, Mr. Vimal mentioned that the team is working on Strawberry chemistry.

Ace Investor, Ashish Kacholia recently became a shareholder of the company. It must be noted that his firm, Lucky Investment Managers and Best Agrolife had an Analyst Meet recently on 10/08/2022.

The company has won the Award for “India’s Most Innovative Agrochemical Company -2021” at the Business Mint’s NationWide Start-Up Awards-2021 on 25/08/2022.

Disc- Invested + I have topped up my position in the company.

In one of the interviews to a news channel, the management clarified that he doesnt belong to promoter group and he had no discussion with management regarding selling.

The company organized its first ever post-earnings con-call. It was a great interaction and the link of the recording is mentioned below for the benefit if all members tracking the company.

30’000 MTPA formulation + 7’000 MTPA technical capacity. This capacity can support 2500-3000 cr. of sales

Q2 is the highest quarter in domestic market

Ronfen launched significantly to growth in current quarter, was launched in July and has seen a bumper response. Technical is produced in-house

CTPR: 1st indigenous manufacturer. FY24 will be growth year and aim for 20% market share

Their products are at 25% discount to innovators

Patent for 3 products (CTPR, Pyroxasulfone technical, …)

Distributors increased to 5200

Formulation (B2B + B2C): 61%, technical: 39%

Working capital was stretched due to new product launches. Plan to bring it down to 90-100 days

Strong in Strobilurin chemistry (will start supplying in export markets as well). 60-65% fungicides are based on this chemistry

Have started working on registrations in South east Asia and LATAM. Plan to sell patented products in these markets

Major contributions from exports will come from FY25. Strategy is to sell own patented combination formulations + strobilurin based intermediates and technical. Will sell through own distribution in some countries and through partnerships in other countries

R&D: 1.5% of sales. Will go to 4% in next few years with increasing registrations

Disclosure: Not invested (no transactions in last-30 days)

Can you make your observation more clear as to what aspect of operating cashflow are you referring to. As long as receivables and inventories are under concern, that’s a normal trend in the industry as end users are mostly farmers.

One concern is Receivables as a percentage of Sales. That is slightly on a higher side for Best Agrolife. I might be biased, but as the company is in a super-growth rate phase, this is acceptable. As per my observation with PI industries and some other peers, it was in a similar trend when they were in their supergrowth phase.

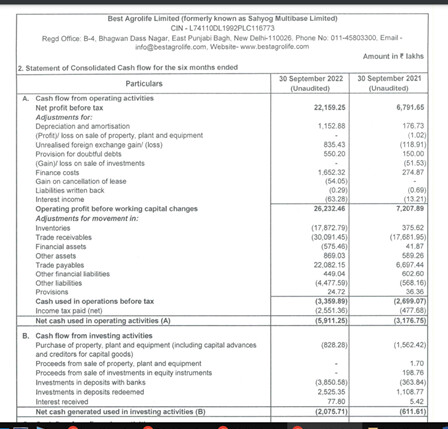

1.The working capital changes are more than profit made at the end of the year. More than PAT the inventories are increasing. See CFO and WC changes.

2. The Plant and equipment in balance sheet are skeptical. It looks as if the expenditure was made in 2021. Are they outsourcing the production?

3. All the increase in capital is from short term borrowings. The long-term borrowings are not increasing.

I am not an expert in accounting, but I am not able to understand these figures. If a product is so successful, it should be asset light. If anyone answers i will be happy to learn.

I am unable to understand the first half of the point. However, regarding the change in inventories vis-à-vis PAT is concerning. Either a) the company is not able to convert to sales resulting in poor Inventory turnover ratio or b) it has kept excess inventory c) it has launched new products which are yet to accelerate in the market. Now, the inventory turnover is 2+ , so looks decent . Also, with numbers it is evident that the company is able to make sales. So, it can be a case of factors b and c. Now, the main concern is that these sales are in a high percentage in Trade Receivables. This exposes the company for bad debts, interest cost and opportunity costs.

The PPE change is due to the company’s acquisition of Best Crop Science Pvt. Ltd and J&K Agrico Chemicals in its quest for backward integration. As far as I am aware, other companies outsource from Best Agrolife. Whether or not is Best Agrolife outsourcing is something to enquire and dig deep into. Hoping for these questions to be asked in the next con-call.

This again is to be asked. Short-term borrowings are cheaper than long-term borrowings. As such the company may be preferring short-term borrowings considering their growth rate and Times Interest Earned. They might be positive on repaying their loans in short term with the kind of growth they are exhibiting. Failure to repay the loans in short term is one factor to look out for !

We all know the history of the company and how and when it entered into the agrochemical business. So, we know that currently the company is in its super-growth rate stage of its life-cycle. As such, company has to be high on assets to capture the market. Maybe we can see the company becoming asset-lighter in the years to come.