company has undertaken debt-funded expansion but profits have not increased much…

Q2 could be very negative due to high maize prices… better to wait and watch…

Disclosure - monitoring only.

company has undertaken debt-funded expansion but profits have not increased much…

Q2 could be very negative due to high maize prices… better to wait and watch…

Disclosure - monitoring only.

Maize prices strong and expected to go higher in Sept and Oct - till new harvest starts.

While the Grain based Distilleries, Poultry and Strach industries have been complaining about high maize prices, there are also cases like these.

Regarding allowing FCI Rice and Maize Import, I agree it seems highly unlikely, specially seeing how tentative the Govt has been recently. They would not like to be labeled as ‘anti-farmer’ by allowing imports or preferring ‘fuel over food’ by allowing FCI rice for Ethanol, by the opposition, just before State elections.

Hopefully it is a short term (1-2 Quarters) issue.

As govt allowed distilleries to produce ethanol from sugar crane juice and B heavy molasses, there is hope that they will up with some action for grain based distilleries also.

For Grain based distilleries, they have allowed 23 lakh MT FCI Rice to be made available for Ethanol making. This should help some companies go for FCI rice, instead of Maize, thus helping ease some pressure on Maize. It has to be seen at what price is FCI rice will be available for Ethanol.

Next action is Ethanol price revision for upcoming Ethanol year- starting Dec. Most likely sugarcane-based Ethanol will see price hikes as it wasn’t increased last time, lets see if there is any increase for Ethanol made from Maize.

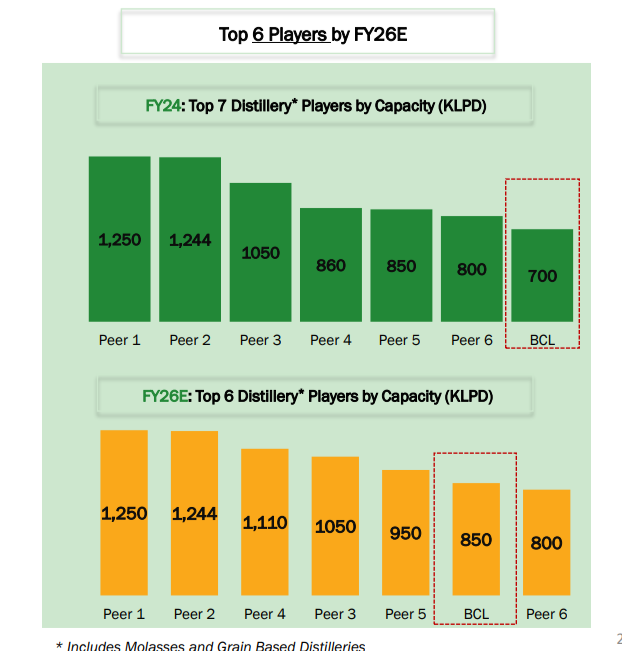

In the presentation of the company they’ve mentioned a few competitors, can folks help with the names of these bigger ones?

Any research report with distillery capacities of all players in the market?

Peer six could be Gulshan poly and globusspirit also comes in between, remaining all could be sugar based distilleries.

Any idea at what price is FCI giving rice to distilleries.

Maize price is very high and operating margins are negative for ethanol - BCL is headed for a very bad quarter! medium / long term still uncertain for ethanol - both grain and sugarcane.

Globus Spirits - #204 by tushar_raghatate?

Please see if this is useful

As mentioned earlier, assuming, even if FCI rice was a viable option, BCL management had no plans of using FCI rice. The only benefit BCL would have had with the availability of FCI rice is easing of pressure on Maize availability and its price as some players would have moved from maize to FCI rice. BUT even though the Govt has removed the embargo on FCI rice for Ethanol on paper, but practically speaking it is as good as not being available IMHO. Landed cost of FCI rice will be 30+/kg and Ethanol price produced from FCI rice is lower than that produced from maize, so I find it difficult to see who will opt for FCI rice, maybe only those which cannot process Maize at all.

There was no way Govt would have gone back to making FCI rice available for Ethanol at around Rs. 22 when States like Karnataka are procuring rice from FCI at around Rs. 28-30. That would have generated lot of heat for Central Govt.

Regarding Q2 results, I agree it doesn’t look pretty. I don’t know how much lower cost (~Rs 23) inventory they had available to be processed in this quarter. BCL is one of the most efficient players, so its results maybe among the least bad. Every Tom Dick Harry knows about the raw material prices plaguing Ethanol industry, I will be surprised if the ‘Market’ isn’t discounting the Q2 results.

I guess the more important aspect is the next years Ethanol price which will be published soon by Govt. If there is any negative surprise, that will move the stock price more substantially than 1-2 subdued quarters.

Disc: Invested. Frustrated. Possibly Biased.

any idea on the operating metrics for rice and maize - how many litres of ethanol/ ENA produced from 1 kg of grain.

maize prices are still high at Rs 25 plus / kg.

Ethanol prices cannot be increased beyond a point at they have to be benchmarked with landed price of petrol which currently around Rs. 52-55 / litre due to crude prices coming down.

As per BCL presentation, roughly 0.42 ltr/kg for maize and 0.5 ltr/kg for rice.

Add to that DDGS variability as its price depends on protein content/kg, availability etc. Around 0.8kg DDGS is made as a byproduct per liter of Ethanol.

Absolutely, Ethanol price cannot be hiked forever. Infact I do not expect Ethanol from maize price to increase as they were increased few months back. Hike will be for Ethanol from Sugarcane producers.

But at the same time, you cannot compare it with landed cost of Crude. Yes, it is a factor, but you have to consider the benefits of circular economy due to EBP. It saves FX - money stays in our economy, generates jobs locally, tax revenue for govt, higher income for farmers, environmental benefits.

EBP has multiplier effects, Govt cannot/will not just compare Ethanol price to landing Crude price and say since Crude prices are low now Ethanol producers should sell Ethanol to OMCs at 50/ltr.

At current Maize prices some marginal players are already defaulting on their OMC commitments, no way Govt can make Ethanol less remunerative and expect it to hit its ambitious EBP targets.

In one of the interviews, I heard management of BCL competitor Gulshan Poly asking Maize Ethanol price to be increased to Rs 81. Mr. Kushal was in same interview, he didn’t ask for such outlandish hike, he just wished for more certainty related to raw material availability. I am sure he (and us) wont mind a hike though ![]()

then cost of production is higher than sale price of ethanol… with price of maize ~Rs. 26/ kg and rice Rs. 29/ kg ethanol is loss making business.

As crude prices are falling and expected to fall further, Govt will not be able to increase ethanol price.

Entire ethanol industry has gone for toss - there will be many plant shut down…

sugarcane based ethanol is marginally positive…

We will see many grain based ethanol plants and sugar mills closing down this year.

I believe there is no doubt that rice is a high water-consuming crop, which is why the government intends to shift to ethanol production via maize. This is evident from the increase in ethanol prices (the latest price rise) via the maize route. However, if we compare the price differences among the three routes—sugar-based, grain-based, and maize-based—the variation becomes clearer. Maize, however, is not only used as a feedstock for ethanol but also in animal feed, fish feed, and shrimp feed, which keeps its prices elevated. To address this, Oil Marketing Companies (OMCs) need to adjust prices accordingly.

It is also important to consider that the economics of ethanol blending with petrol should work in terms of cost savings in the final petrol price, while also helping to reduce crude oil imports. Additionally, broken rice from the Food Corporation of India (FCI) is a by-product that needs to be allocated somewhere. During the election phase, a mix of broken rice was distributed under the ‘Bharat Rice’ program to provide affordable food to those in need. The rice inventory is in plenty with FCI

Furthermore, many sugar-based ethanol producers have made significant capital expenditures that need to be factored in. However, grain-based routes typically have a dual feed advantage (utilizing both broken rice and maize). I might be wrong in my assessment, and I welcome any views on this topic.

Hence the recent decision of GOI is well thought to keep the prices of maize in check

Govt. banned ethanol from sugarcane to keep the price of sugar under check - then sugar industry went into problem with farmers not getting paid.

Govt banned sale of broken rice by FCI for ethanol production to keep the price of rice under check - then the grain based ethanol industry went into problem with many of them in losses. To save them Govt. increased price of ethanol from maize (much higher than petrol prices - which consumers are paying for) then price of maize shot up which did not help the ethanol producers… further it led to problems for animal feed industry (and consumers are paying for high prices)… Farmers didnt benefit much but middlemen made money as at time of harvest maize prices were low.

Now they have allowed ethanol from sugarcane when there is no molasses and cane harvesting season is yet to start… so no impact on ethanol supply - no payment to farmers, no benefit to sugar mills… at current FRP rates of sugarcane ethanol is only marginally profitable for sugar mills. Dont see how farmers will get paid on time - in some cases even paid at all !! They may increase ethanol price and force OMCs to blend at higher prices (as crude oil is falling) and then fuel inflation will not come down impacting the whole economy !!!

All in the name of keeping sugar prices down… prices of maize, rice and even sugar has gone up and everybody is paying for it !!! Sugar/ ethanol industries and animal feed, poultry, milk all are affected… Is the Govt even thinking before making decisions??

Investments decisions should be made on facts and not hope - so i think sugar and ethanol companies are very unattractive right now…

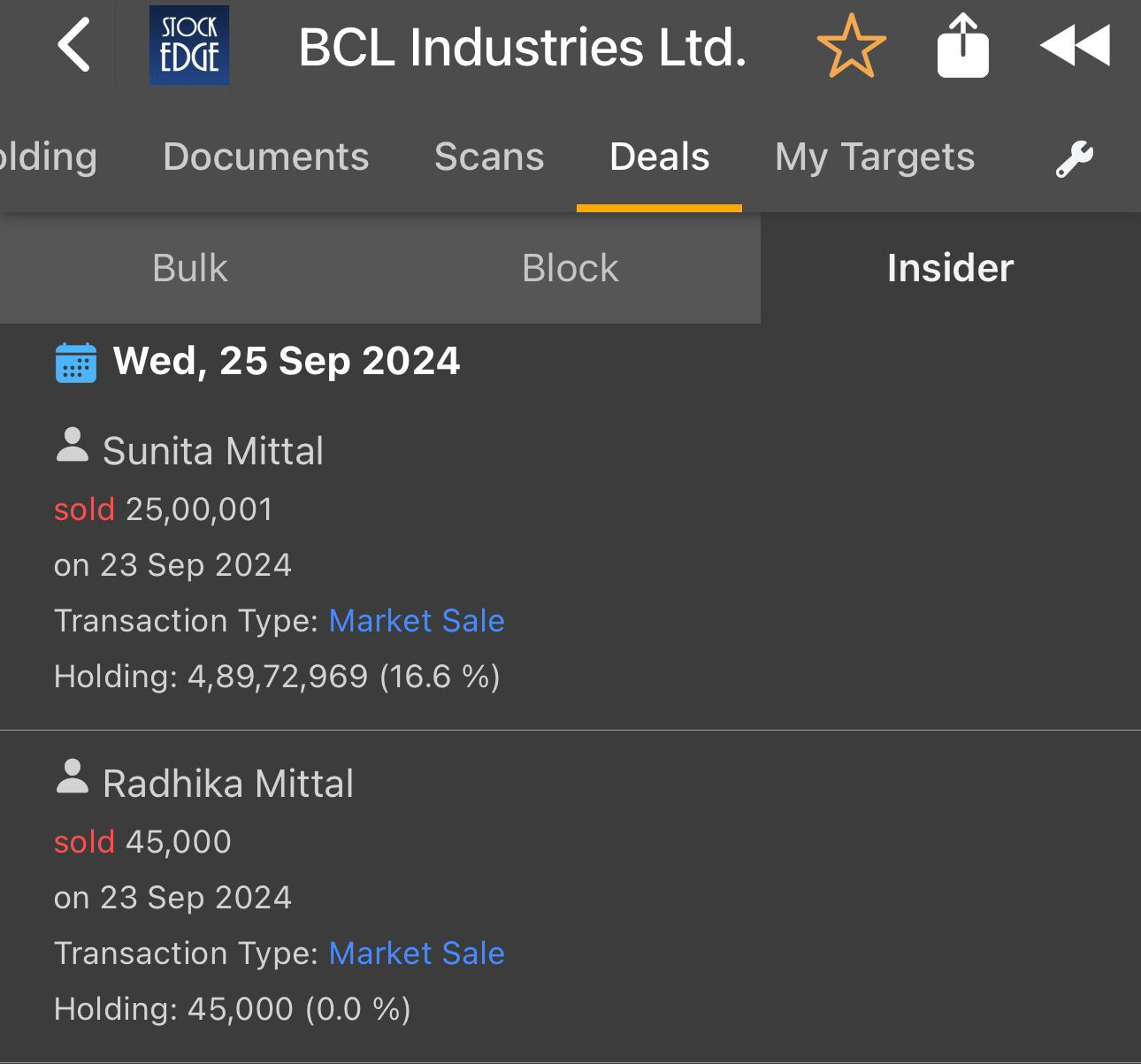

Rajendra Mittal sold 2500000 shares yesterday, it could be a clear sign of hit on Q2 numbers

I had pointed out earlier that Q2 is expected to be bad… but promoters selling due to that is not good news at all… that too they have been allotting warrants to themselves at low prices only in June and then selling shares at higher mkt price… clearly fooling retail investors…

I have been monitoring this company but havent invested due to the bad economics of grain based ethanol plants. But now promoters selling after warrant allotment is not good governance either… it is no go for me at this price… if it corrects Rs. 30-35 levels can think about taking the risk !!

If anybody has analysed the price of allotment of shares to promoters through warrants and mkt sale price of promoters please share. … thanks.

I think warrants are allotted at 36/- in Mar’23