The India ethanol story can be played through a builder like Praj Industries or sugar molasses companies or the grain alcohol companies. Amongst the grain alcohol companies 4 come to mind Globus Spirits, BCL Industries, Gulshan Polyols or Coastal Corporation.

Company Background

BCL is a part of the Mittal Group founded in 1976, by Late Shri D. D. Mittal. Under the stewardship of Mr. Rajinder Mittal, the company has now grown into an Rs1400crs business empire.

Promoter stake at 61.36% with skin in the game

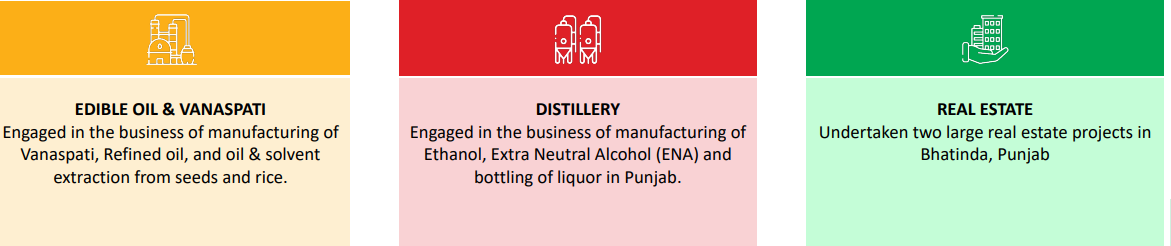

The company is a diversified conglomerate in manufacturing and development with business interests spread across a variety of industry verticals namely Edible Oil and Vanaspati, Distillery and Real Estate.

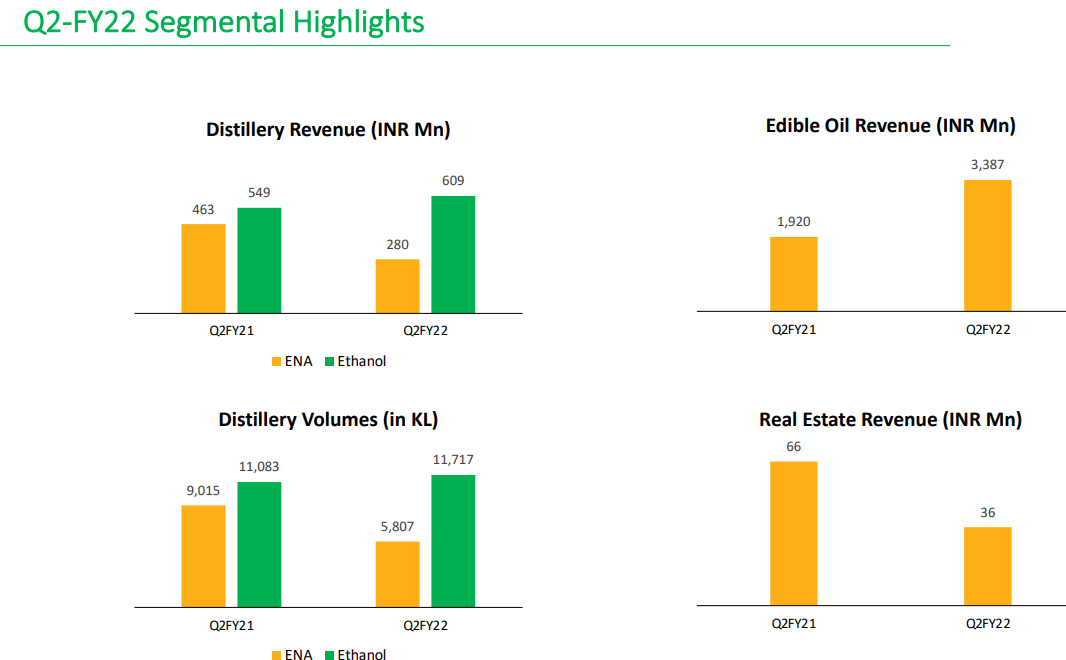

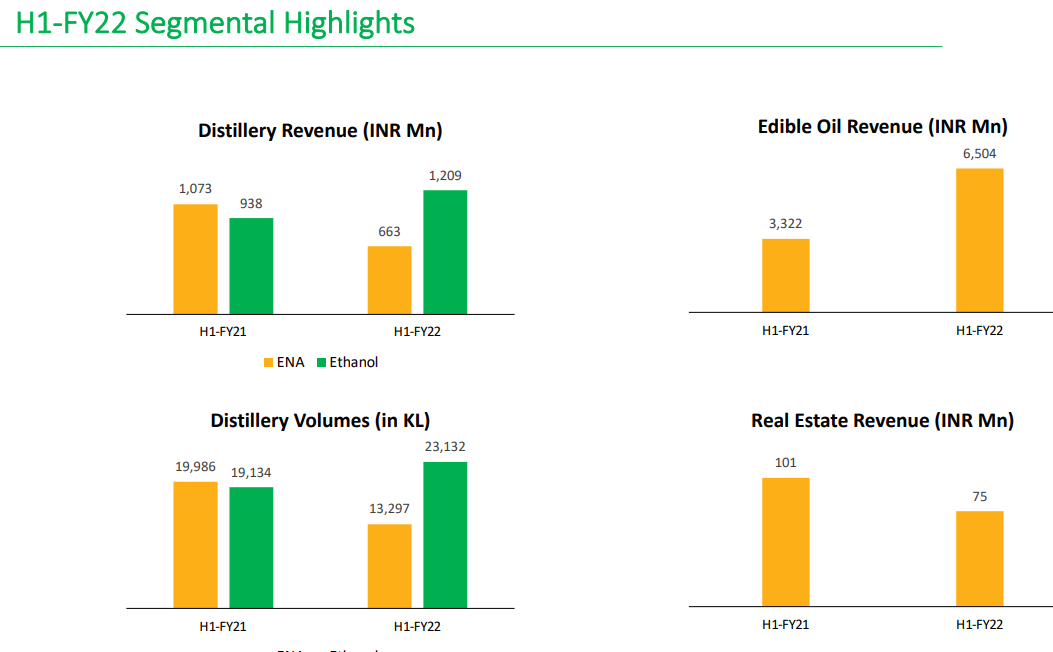

Distillery business

BCL entered into the distillery business mainly to diversify away from edible oil business. The company mainly produced grain-based Extra Neutral Alcohol (ENA). Apart from being used in alcoholic beverages, ENA is also used in cosmetics and personal care products like perfumes, toiletries and pharmaceutical products such as antiseptics, drugs, syrups, etc. The company has developed long term relationships with clients like Pernod Ricard, Radico Khaitan, Punjab Chemicals and Crop protection limited and Wonder healthcare. The company had also launched 8 different Liquor brands like Asli Santra, Ranjha Sanufi and Red Royal Whisky.

The company distillery can also manufacture Ethanol along with ENA. After the launch of the Ethanol Blended Petrol (EBP) program the company converted 130 KLPD of its existing capacity into production of Ethanol.

Oil marketing companies (OMCs) have recently allocated BCL to supply 36mn liters of ethanol from its manufacturing unit at Bathinda. Further, the company has also applied for additional quantity of 5 million liters. The total sellable quantity to OMC’s will be 41mn liters for the period from 01st Dececmber, 2021 till 30th November, 2022. BCL has been supplying ethanol to the OMC’s since 2018.

BCL distillery can manufacture ENA/ethanol from multiple crops which has reduced its dependency on a single crop and thus the company can avoid the vagaries of raw material price fluctuations.

Capacity expansion of 3.5x times

The company currently has 200 KLPD capacity in Bathinda.

300 KLPD addition in West Bengal

BCL wants to capitalize on the ENA deficit demand scenario of North-Eastern India by setting up a 200 KLPD state-of-the-art ENA plant at Kharagpur, West Bengal. The company has joined hands with M/s. Svarna Infrastructure in building this capacity and owns 75% equity in this new project. The capacity is expected to come online by Q4FY22.

The company plans to further expand this capacity by another 100KLPD by Q3FY23 as land and power required for further capacity expansion is already in place.

200 KLPD addition in Bathinda

The company has obtained permission to add another 200 KLPD Grain Based Biofuel Distillery in Bathinda. All the prerequisites for expansion like land, power and cheap finance (interest subvention) are already in place and capacity is expected to start production in Q3FY23.

Latest update on capacity expansion as of Jan 11, 2022

We hereby submit business update that the initial plant testing at the 200 KLPD Ethanol plant of Subsidiary of the Company viz. Svaksha Distillery Limited has begun and the commercial production at this plant is expected to commence in the next few months before end of financial year 2021‐22. The Unit is being set up without raising any debt.

Further, the Subsidiary of the Company has also obtained in principal approval from MoEF for enhancing the capacity by another 100 KLPD at the same premises. The Subsidiary has all the requisite land and utilities arranged for the expansion. The work to install and establish another 100 KLPD will begin soon after commissioning commercial production at the 200 KLPD plant and will be executed at minimal capex due to the existing facilities. The 100 KLPD expansion is expected to be completed in financial year 2022‐23.

After the commencement of commercial production at Svaksha Distillery Limited in year 2021‐22 and the proposed expansion plant of 100 KLPD, the total capacity of the Subsidiary of the Company shall be 300 KLPD.

Further, as already informed, the Company (BCL Industries Limited) is also undergoing the expansion at Bathinda Unit by way of setting another 200 KLPD plant. The work for the Bathinda plant is on‐going at full swing. After commencement of commercial production in its new plant, the total capacity of the Company in Bathinda shall be 400 KLPD.

With all units of the Company and Subsidiary generating production, the total capacity of the Company (BCL Industries Limited) together with its Subsidiary (Svaksha Distillery Limited) will be 700 KLPD and we will be one of the largest producers of Ethanol from grains in private sector in India.

Key risks

Broken rice is mainly used to produce ENA and any rise in its price will directly impact gross profit.

Final product prices are decided by state/central governments and/or OMCs (oil marketing companies) and hence, regular price hike is not a guarantee for profitability.

Ban on sale and consumption of alcohol in Gujarat, Bihar, Nagaland and Lakshadweep. If the governments in states that BCL operates in decide to ban or restrict the use of alcohol, it will have an

adverse impact.

Execution risk as the expansion undertaken is massive.

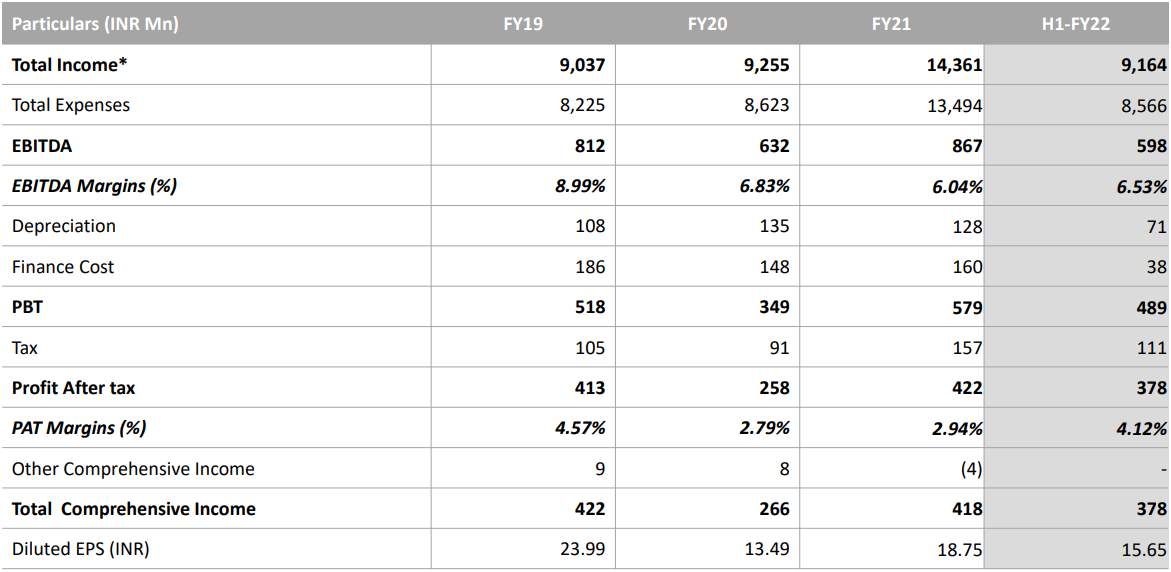

Financials

Extrapolating 1HFY22 numbers the company is set to do Rs80crs plus in FY22 and is trading a P/E of

14.1x at the current market cap of Rs1127crs with 3.5x capacity expansion over the next 2 years

Other resources

Company website https://www.bcl.ind.in/

Latest results concall transcript https://www.bseindia.com/xml-data/corpfiling/AttachHis/46718bab-8eba-4cea-8f5f-9b0406a19ec9.pdf

Disclosure: Invested