After named in MAHADEV batting APP scam/ DMCC etc., I dig deeper to find history of pramoter and found this FIR for their KISSAN FAT Limited, Rajinder Mittal(DIN-00033082) pramoter of BCL. Though NPA case settled but what I find is Report of Forensic Auditor. Forensic Auditor observed that the borrower company had diverted the funds to sister concern viz. M/s. BCL (Bhatinda Chemical Limited) and M/s. Ganpati Townships Limited. The firm had prepared two sets of audited Financial Statement for the year ended 2014 i.e. one copy for bank and other for ROC/ Income Tax/ Statutory authorities.

BCL FRAUD_compressed.pdf (5.1 MB)

9 Likes

Results are very disappointing, we are expecting improvement in margins but nothing improved even the ethanol selling price is hiked by 9%.

Management commentary on the margins is also not satisfactory.

2 Likes

In any company, my first take is in the integrity of the promoter over and above the business. Whatever may be business/ fundamental, if the promoter is not genuine then nothing to shareholders at large .

I smell manipulation of books of accounts in the past. Now, we will dig deeper for the last 4 to 6 year’s accounts to judge the promoter’s integrity and honesty etc. etc. Please can anyone give comments for the above matters…? Anyone has issues for the company, let us know so that while doing research we can keep it in mind and as a joint effort of all of us, we can reach a conclusion.

4 Likes

I was also expecting better margins. Management could have communicated better during the Q3 call about the impact on margins because of elevated Maize prices. What most of the investors took away from the call is that in Q4, we will benefit from

- Cost savings from the Boiler plant

- Hike in Ethanol prices

Management has now said that this dip in margins should reverse as Maize prices have cooled off due to bumper harvest. Lets see.

Even if there isnt much improvement I expect the following in the current financial year:

Revenue around Rs 2400 cr (Rs 1750 cr for Distillery and Rs 650 from Edible Oil (EO))

EBTDA of around Rs. 240-250 cr (Rs 220-230 cr from Distillery, Rs 20 cr from EO)

*Wild guess for EO numbers, as I am not clear on the path to be followed for EO business.

I actually am eager for them to ramp down EO business as fast as possible, and the company to be not categorized under the Edible Oil sector. It impacts the margins of the business as well as the multiple the stock gets from the market.

Sometime after the current EO plant is wrapped up and some required machinery moved to the Distillery land, BCL will also receive proceeds from selling the 11 acre plot in Bhatinda where their current EO complex stands. Anyone who has idea about Bhatinda land values can do some scuttlebutt and share what may be the ballpark figure.

Now what an investor needs to decide what should be the stock price of a company generating around Rs 250 cr EBITDA at around 10% margin (13-14% for Distillery, low single for EO). I feel it is undervalued currently by a fair margin.

The year after we will have hardly any EO, margin accretive 75KLPD Biodiesel and 150 KLPD additional Distillery capacity)

Disclosure: Invested.

4 Likes

I agree with your view that fraudulent management will always look into different ways to cash out money from business.

1 thing I don’t understand is that BCL management doesn’t take any dividends, dividends are only for minority shareholders. Why they took this decision and lost the dividend amount

2 Likes

Some thing which is beyond our understanding is there, RM cost increased slightly but It should be mitigated by the higher ethanol prices.

In Q3 call also Kushal told that new harvest will decrease the maize price but nothing happened in Q4, so I am not expecting any softness in the prices and improvement in margins.

Only WB 100KLPD numbers will be added from Q1 onwards, no more further triggers

3 Likes

While I share your disappointment, I do believe that Kushal was talking about the new harvest from Bihar and he stated that the benefit would accrue in the ‘coming quarters’ (we believed that it would be from Q4, we can say he should have specified that it won’t be in Q4).

We have to keep few things in mind

- Though the call was for Q3, it was being held when half of Q4 had already passed, Kushal had clearly highlighted that the current procurement cost was Rs 24.3, which is a jump of more than 10-15% as generally the procurement cost was Rs 21-22. That quantum of jump is by no means small. The price hike of Ethanol was around 9% while the cost increase was 10-15%.

[Edit: I think I understand why some investors consider that the cost hike was small and margins should have still been better as Ethanol prices increased by Rs. 5.9 while maize price increased by ‘just’ Rs 2.5-3.5. We need to think in % terms rather than absolutes, specially when 1 Kg maize doesn’t produce 1 ltr of Ethanol] - Compare BCL performance with its peer Gulshan Poly (in distillery segment), BCL has done better in terms of margins consistently. Even their margins were subdued because of raw material pressure.

- Agree, other than additional revenue from new 100KLPD coming online this quarter, there are no other ‘triggers’, but if the current price is below its fair price, that could itself act as trigger and once (if/when) some bigger players start entering and the price starts showing momentum, retail will also start piling on which they are now leaving for a broken company/stock.

Disclosure: Invested since 3-4 yrs and pyramiding. Not a buy/sell reco. Just sharing my thoughts here.

5 Likes

Came across this article which nicely explains the benefits of Ethanol from corn/maize to the Economy, environment and farmers. The author has laid out what steps the Govt should take to support this budding industry which will help us in energy security and sustainable development.

1 Like

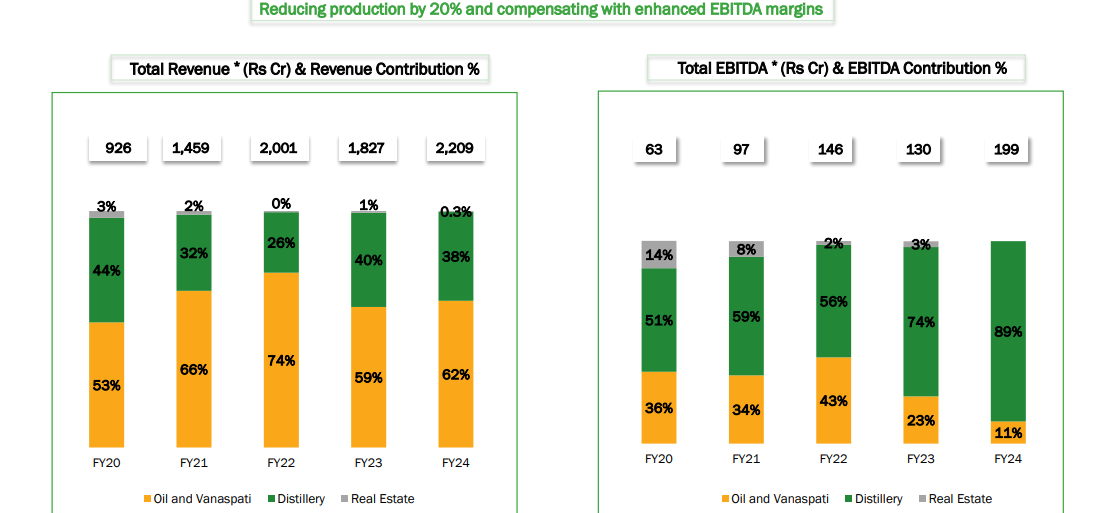

As per the presentation 62% of revenue contributed by Edible Oil and page No 39 of said ppt shows 831cr revenue from edible oil… Both figures dont match… Kindly share your thoughts…

It’s a typo. 62% should be for Distillery and 38% for Edible Oil (EO).

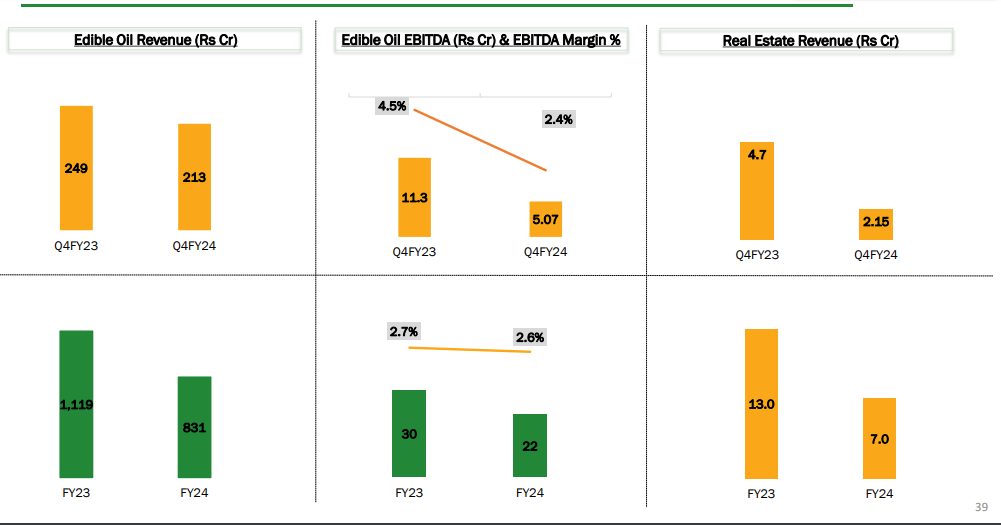

Since past few quarters BCL’s main revenue generator is Distillery segment, and this segments contribution to profit and cashflow far outweighs EO segment’s contribution. This gap is only going to increase with the 100KLPD additional capacity now online. For this reason, I had written to company’s IR few months back to explore the possibility of changing the categorization of BCL on exchanges from Edible Oil to something which more aptly suggests company’s new focus, its margin profile and profitability drivers. EO is generally a low single digit margin business while ENA+Ethanol+Biodeisel is around mid-teens. That greatly impacts the multiples a stock commands in the market.

3 Likes

I expecting some uptick in revenues in this quarter due to addition of WB 100 KLPD & increase in utilization levels of Batinda 400 KLPD may hit 100% but worried about margins due to grain inflation. As per previous call there was some minor drop in the maize price as compared to Q4

1 Like

From the recent conference calls that I have attended of companies which make Ethanol and/or ENA from grains, I understand that those Managements think that it is highly likely that FCI rice will soon be available. Obviously, none of them stated it as a done deal as no one what’s to second guess Govt policy actions, especially after seeing so many twists and turns, but all of them suggested the same thing. FCI Godowns are full till the brim and there’s hardly any space left for the upcoming harvest. That makes them and me hopeful. If this happens, it most likely will cool down Maize prices as many Ethanol producers would move to Rice, thus reducing demand pressure on Maize.

Disc: Invested. Till announcement comes it’s just a conjecture.

3 Likes

Agree with your view.

Uptake in the margins of grain based distilleries is seems impossible as long as there is no availability of FCI rice. As distilleries keep on adding capacities but maize supply will be 2-3 years behind the required demand.

1 Like

Why No DII shows interest in the company? With all capacity additions, I believe that the business will do well in the near term.

I am comparing with Globus Spirits. Not much DII holding there too.

True. It has been disappointing. Even after the company attending Investor conference organized by their IR and some 1 on 1 meetings, company hasn’t been able to attract any big investor of note.

Company can do EBITDA of 260-280 cr next year, still no takers. The recent technical action of stock hasn’t been good.

BCL is of the most efficient grain processors and grain-based Ethanol manufacturers, with assured demand for it products. Still, it has not attracted big players, while stocks doing a fraction of its Revenue/EBITA/PAT at lower margins are flying high, with bigger market caps based on some made-up stories/MoUs most of which won’t fructify.

Anyways, it is what it is. Market is supreme

2 Likes

Have you looked into thier Balance sheet and Cash flow stmt? Thier CFO is low, particularly, many years have negative Account Payables!

There are various risk involved in the business, which are restricting the MF/FPI’s to invest in the company.

- RM price volatility

Even though they had plans to close the edible oil business due to Raw material price volatility, risk is still existing in the distilary business due to volatility in the maize prices.

Maize prices on raise since last 3 quarters–> 23/- per Kg in Q3, 24/- per Kg in Q4 and now its 25/- per Kg in Q1FY25. Margins also shrinking QoQ due to this.

I am expecting Q1 margins to shrink further due to this. - Product price is in the Govt control

Neither ethanol nor ENA prices can be controlled by the company due to RM price inflation. This is also a setback for company. if Govt see some surplus ethanol in the coming years then they can decrease the price of ethanol irrespective of the RM prices.

Being a commodity based company re rating in the valuations difficult, price movement would be based on EPS growth only.

As there is no further addition in the capacities in this FY, margin compression can downgrade the price further.

Only 1 trigger to boost the margins/profits is release of FCI rice for ethanol production, industry is expecting the decision soon as all FCI’s are full of surplus rice but the price of ethanol would be low for rice route as compared to maize.

3 Likes

Absolutely agree that these are not ideal and caps the multiple BCL can command.

Regarding low cash flows, I agree that it has been on lower side but I did a comparison some time back with its PAT, the numbers were OK i.e. no red flags (Cumulative PAT of last 5/10 yrs not >>> Cumulative CFO) which would indicate Financial shenanigans. With the nature of business changing from low margin Edible Oil to mid-teens Distillery, we should expect higher cash flow. The same has been mentioned by Management (Mr. Mittal).

Product price is controlled by Govt, agree, but same Govt assures the uptake of its product, so we are assured of ~100% capacity utilization. Moreover, EBP is one of its pet projects and so many Ministeries keep harping about it, be it Petroleum, Transport or Farm. Right now, India has a deficit of Ethanol (if it has to reach 20%). Surplus Ethanol is few years later and do note that BCL’s manufacturing capacities are fungible between Ethanol and ENA. With the demographics of India and rising affluence, alcohol demand is only going to go up. I am not even considering Ethanol for Diesel.

I 100% agree that for BCL market cap to go up, earnings need to increase and like you said, FCI rice availability is the (only) hope in near term. Based on what I understood from the answer to my question to Mr. Mittal during Q&A, BCL doesn’t intend to use FCI rice even if it’s available. The benefit BCL will have in such a scenario (FCI rice is made available) is that since many Ethanol producers will shift to FCI rice, it will ease demand of Maize, thus reducing its price.

Disc: Invested so maybe biased

1 Like

Maize prices are currently > Rs 25 per kg - at this price operating margin (for making ethanol) is either Nil or negative… this has been the case for past few months… it will reflect in poor Q2 numbers.

Q1 was still ok as maize prices had come down to 21 / 22 in Q1 (due to Rabi crop harvest) and then shot up in July to 25.

Prices could come down only in Oct/ Nov due to kharif harvest…

Very unlikely that rice will be released by FCI.

Another possibility is if Govt allows non-food maize to be imported… but that too wont happen as Bureaucracy is too slow and conservative and the politicians are occupied with elections !!

1 Like

I just checked the CFO and Net Profit for last 5 years and as well since 2017. Its not really matching but seems like major culprit could be higher inventory in the last 2 years in addition to having negative payables.

1 Like