Acquired Goyal distelleries, promoters selling stake, now SEBI notice, not sure what to make of the recent developments

As an investor in BCL, it has been a roller coaster ride this year. Below is a summary for anyone who wants to come upto speed with BCL:

Good

Company’s transition from Edible Oil to pure-play Green Energy continues with good momentum. Here is a summary of the declared plans for the next 2 years.

-

As per current disclosures, in around 2 yrs time, company will have 1100 KLPD Ethanol-ENA (current 700 KLPD), 150 KLPD Bio-diesel, 20 MTPD Bio-gas, plus country made liquor business

-

Edible oil business will be shut down in the next couple of quarters, required machinery will be moved to where the Distillery is located and land on which Edible Oil business is, will be sold. Proceeds (40+ crs) from that will help in bringing down debt or help in capex. Shuttering of Edible Oil business will also help in substantial reduction of working capital in addition to the proceeds from land sale.

-

75 KLPD Bio-diesel plant under construction in Bhatinda along with power plant, planned completion by 1st quarter next FY

-

150 KLPD of Ethanol plan under construction in Bhatinda, planned completion by 3rd quarter next FY

-

Another 75 KLPD Bio-diesel plant construction will start at the W.Bengal subsidiary once the first Bio-diesel plant stabilizes

-

Edible oil business has low single digit margins, while the Green energy business will have mid teens margins. Should help the company command better multiples than what it did in the past

Not so good

-

SEBI notice - Update* It seems to be about alleged violation of Regulation 31(4) of SEBI - which stipulates that the promoter of every target company shall declare on a yearly basis that he, along with persons acting in concert, has not made any encumbrance, directly or indirectly, other than those already disclosed during the financial year.*

Will try to get info from company IR/CS. -

Margin pressure (discussed above) - I believe it is a short-term phenomenon. Once new maize harvest comes, maize price should cool down. This year more area is under maize cultivation. Rice is rotting in FCI godowns but govt still not releasing it at subsidized rates like they did in past, for Ethanol is disappointing. Allowing companies to participate in e-auctions won’t help much due to high auction price

-

Promoter selling - for me promoter selling 1.6% when they hold ~60% stake is no biggie. Promoters sell for various reasons, buy only for one. When asked the reason for selling during the Arihant Rising stars conference, Mr. Kushal Mittal mentioned that his parents are over 60 yrs now and they needed money for personal/social obligations. He said that promoters have always put in money in the business when required, so recent sales shouldn’t raise too much concerns (not his exact words, but that’s what he implied)

-

Low cash flows - according to Management it is primarily due to Edible oil business constraints e.g. The flip-flopping govt policies related to custom duties, made it very difficult to plan inventory, often resulting in substantial inventory losses. Now, with EO business shuttering over next few quarters and major Distillery capex starting to generate returns at higher margins, cash flow should improve substantially.

Disclosure: Invested. No recommendation.

company has jumped from frying pan into fire… edible oil was bad business and good it exited… but grain ethanol is no better with no margins… that too with such huge investments made…

maize prices unlikely to correct much as very large capacity addition has happened in grain based ethanol… many distilleries have defaulted on supplies of ethanol to OMCs.

even international maize prices have gone up.

Please refer to this post by me - exactly the same things covered in this mint artilce.

Due to huge excess capacity and negative margin, Grain based ethanol industry will face a huge crunch… many of the companies will default… capacities will shut down and then balance will be restored. even then the returns will be very moderate…

the companies realising this and folding up earlier will be better placed as the more they delay the interest accumulation on defaulted loans can be extremely high… and what is the point in holding… at the end the industry is going to be low margin for a very long time…

unless Govt. allows import of GM maize… which is vurtually impossible in our country… even for ethanol production.

If others can share their views… it can give a clearer picture on how this industry will evolve.

In Sep quarter Elara fund has exited BCL by selling remaining 3.2% stake.

DII - Nil holding

Retail - increase from 35 to 40%.

At last company managed to post good results even in the tough grain inflatory environment by using some wet maize procurement at lower price in Q2, but it’s not the case in Q3.

Expecting crop in RJ, PN & JH which may cool off current maize price ~ 25/- to some extent.

As per management current margins can be sustainable in Q3 & Q4.

Capex:

75KLPD bio diesel plant can comission in Q1FY26.

150KLPD batinda expansion can be commissioned in Q3/Q4 FY26.

250KLPD Goyal distillery equipment finalization is under process, exact time line of comission can be known after equipment order placement. If ever thing goes well then we can get this on stream by FY26 end or else spill over to FY27. Funding route is yet to finalized for 350Cr acquisition.

From the current 700KLPD to 1175 KLPD by FY26 end or mid of FY27 i.e 68% jump in capacity in 1.5 to 2 Years.

Edible oil:

Exit from this segment could be Q4FY25/Q1FY26.

Even though top line would be impacted meaningfully 800-1000Cr but impact on the bottom line would be < 20Cr, which can be compensated by biodiesel plant.

WC finance cost would also decrease after exiting from the edible oil.

Over all down the line 5-6 quarters numbers would be similar to Q2 results, I am not expecting any good jump in numbers unless there is substantial reduction in maize price or increase in ethanol price . FY27 would be good year as all capacities would be on stream

Thanks for the insight into low input prices and how it helped in better PAT - i was wondering how they managed to do it when maize prices were more than Rs. 25/kg . That means Q3 could be very low profits. As prices have starter coming down in October that could be some relief. But i expect prices to go up again by Dec as more grain based ethanol capacity has been added.

Where are you tracking maize prices

https://in.investing.com/commodities/ncdex-maize-feed-futures-streaming-chart

Prices were down only for a few days after which it has started moving up again. Maize based distilleries have one more year of losses after which it will be clear where this industry is going.

LNG/CNG is picking up very fast… and prices expected to come down next year it is going to add problems to the ehtanol producers.

4-5/- increment in the ethanol price. If its realized then it can give some relief to the producers but surprisingly grain prices will also shoot up based on this news.

https://www.chinimandi.com/ethanol-price-revision-proposal-sent-to-cabinet-for-consideration/

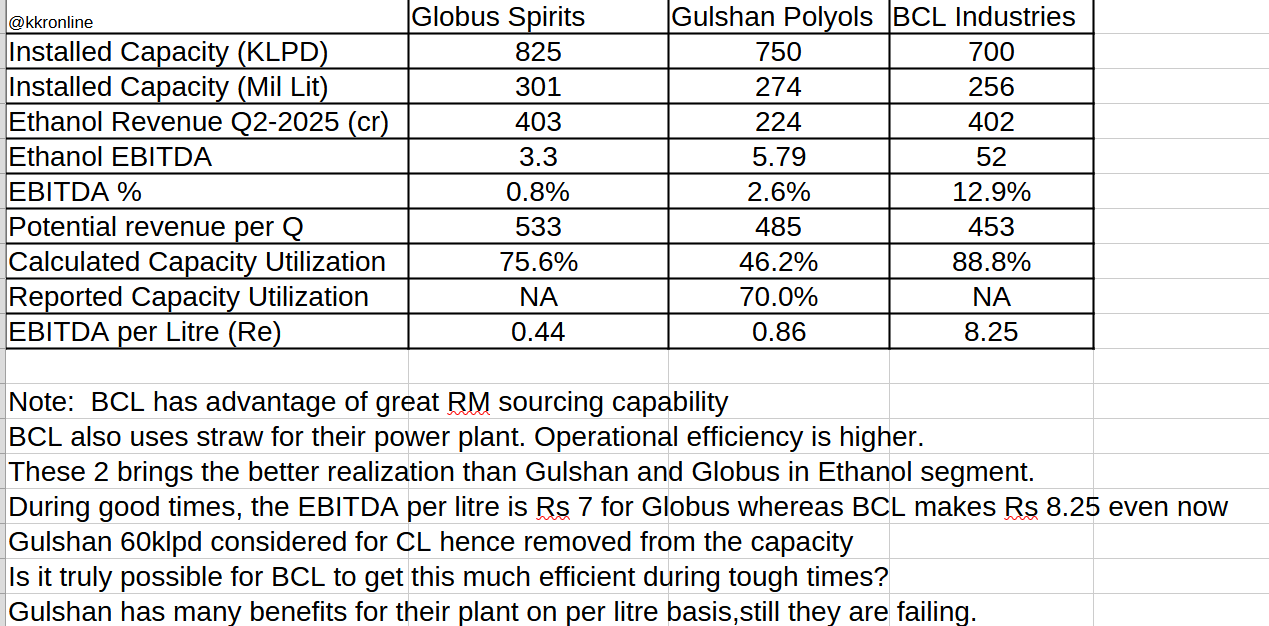

Just a comparison of all the grain based ethanol players. Pl share your opinions if there is a correction needed.

Inputs from my friend(already took permission to use his content in valuepickr)

This is in response to comparision table.

Some of my observations are as under :

(1) Gulshan has operated at around 50% capacity utilisation during the quarter as against 100% capacity utilisation by BCL. Even Globus has operated at around 55%-60% capacity utilisation as they claim to have 30 crore litres capacity at 5 locations.

(2) BCL has the biggest advantage of its 300 KLPD which can be used for ENA also and which they use for supplying to IMFL producers like Amrut, Mohan Mekins, etc. out of total 700 KLPD.

(3) Gulshan is struggling with its capacity utilization issue and even their ESY24-25 allocation is for 14.25 crores as against 18.25 crores for BCL(rest capacity can be used for ENA). Globus has not declared its Ethanol allocation for ESY 24-25.

(4) Elevated raw material prices and its availability are hurting both Globus and Gulshan to the extent of speaking on their EBITDA margins. BCL is also effected but due to its networking and innovative practices is able to survive and it does not speak on their capacity utilisation. However, their EBITDA margins are also contained but still far higher than Globus and Gulshan.

(5) Globus does not have any plan for further addition of Ethanol/ENA capacity rather they have gone into launching some high valueIMFL brands which is still in its initial stage and not making any contribution to EBITDA. Their regular brands are contributing EBITDA only source of their survival. Regular brands are just 30% of total turnover.

(6) Globus also does not have any further Capex lined up except some around 50 crores for minor work. Gulshan does not have any muscles at present to do any expansion/diversification/greenfield project.

(7)BCL has identified and gone ahead with further capex to the tune of around 500 crores or so in the next two years. (i) 60 crores for 150 KLPD expansion at Bhatinda (ii) Biodiesel 75 KLPD backward integration through DDGS by product of Ethanol costing around 150 crores which will be operational in the first quarter of next financial year. (iii) Ready to go “Goyal Distillery Pvt Ltd” capex of around 300 crores for 250 KLPD Ethanol Project in Haryana and 20 MTPD CBG Project. Land and all regulatory clearances are in place. (iv) Two more biodiesel projects are to be launched at Kharagpur and Fatehabad once Bhatinda facility becomes operational. So Company is upbeat on capex.

Last year BCL did an EBITDA of 200 crores which I expect this year to be 250 crores in spite of the first half being a challenging one with 113 crores.

Globus also will take some time to come back on rail.

Gulshan may get some support to their EBITDA if financial incentives are released by State Govts of MP and Assam.

Second half of FY 24-25 should be a better one as new crop has hit the market and price may remain somewhat contained.

Good comparision.

As per my understanding globus spirit doesn’t make much ethanol for sale, they will use distilleries for captive ENA.

In case of Gulshan, they might be holding some capacities due to unfavourable economic conditions. Coming 2 quarters would be very crucial for grain based distilleries.

BCL managed Q2 with some wet maize purchase, but Q3 would be tough.

I am waiting for announcement of ethanol purchase price for the new ESY, expecting some 5-6/- increase in ethanol price to beat the grain inflation, Then only industries can sustain. As soon as we get new price then that will be applicable for immediate supplies, Last ESY new price revision came in the month of Jan.

Capex plans of BCL are impressive but economics should improve to stay invested or else huge hit on margins & bottom line.

last time maize based ethanol price was increased but sugar based was not. This time most likely there will no increase in maize based ethanol price.

crude prices have come down and are expected go go down further. Govt does not have any room to increase prices.

many standalone grain based ethanol companies are already up for sale.

If there is no revision in the ethanol price then we can exit BCL as improving the margins is impossible with the growing maize ![]() prices.

prices.

Further only 75KLPD bio diesel plant will come on stream in the FY26, remaining all capex will be completed by FY27 & FY28.

with this king of demand supply of maize, prices will not come down - which can already be seen as inspite of harvest prices have not come down. next few month prices could go up to Rs. 30 per kg.

Crude oil is coming down… how will Govt increase ethanol prices.

this industry is in a soup… smaller ethanol distilleries have realised this and have started selling out as they are not able to sustain - and there are no buyers of these plants.

Companies like BCL could sustain but with lesser margin.

Article is behind paywall.

Does it explain how maze is related to oilseed and cooking oil?

Govt intention to blend ethanol is not making petrol price affordable, they want to save forex reserves by importing less crude oil.

On this contest they may take a small hike in prices but as the ethanol prices increase i am expecting jump on the maize prices as well, Its happened in the last year. Margins went down further with new ethanol prices due to jump in maize prices.

Over sector become risky, one should wait for good time to exit

its better to exit as i think it will get worse. with maize prices at Rs. 24 now (during harvest) it will go up to Rs. 30 by Feb/ March - when operating margins will be negative. we can see the impact of high maize price on poultry industry.

BCL promoters also have sold good amount of shares… Institutions investors have also sold most of holding.

BCL is increasing capacity in low margin scenario… going to hit them hard.