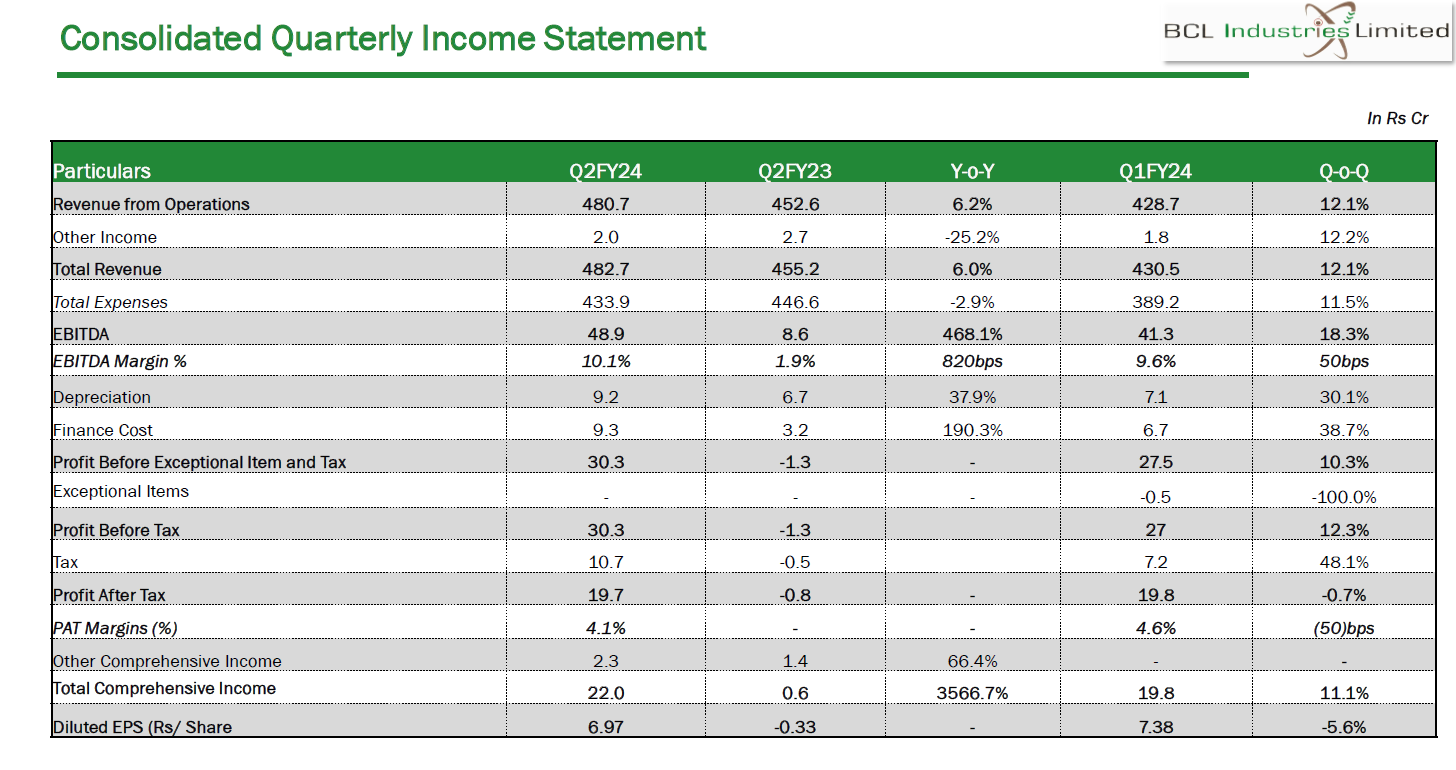

Good Quarterly Result from BCL Industries.

Note - Invested and may be biased

Its positive news for the company, even there might be some dip on revenue but we can get stable margins from the distillery business. Bottom line contribution from edible oil business is very low, if they discontinue this biz then working capital cycle also will improve, less depreciation, interest and better margins can lead to some re rating in the valuations.

In Q3 concall we can expect a clear way forward on this

Agree.

Also i was wondering how come BCL Industries is moving up, despite bad news on Ethanol production circular (Sugar Cycles: 7-8 years of losses followed by 2-3 years of super gains! - #1513 by nithin_Shenoy). BCL make ethanol from Grain, whereas sugar stocks are getting impacted due to sugarcane restrictions on Ethanol.

Seems everything going good for BCL at this time.

Q3&Q4 numbers will stable with all 600 KLPD capacity on stream, I am expecting distillery revenues ~400 cr from the existing 320Cr quarterly run rate.

FY24 EPS could be ~5/- and FY25 could be ~8/-. Price still at ~10 PE of FY25 Earnings.

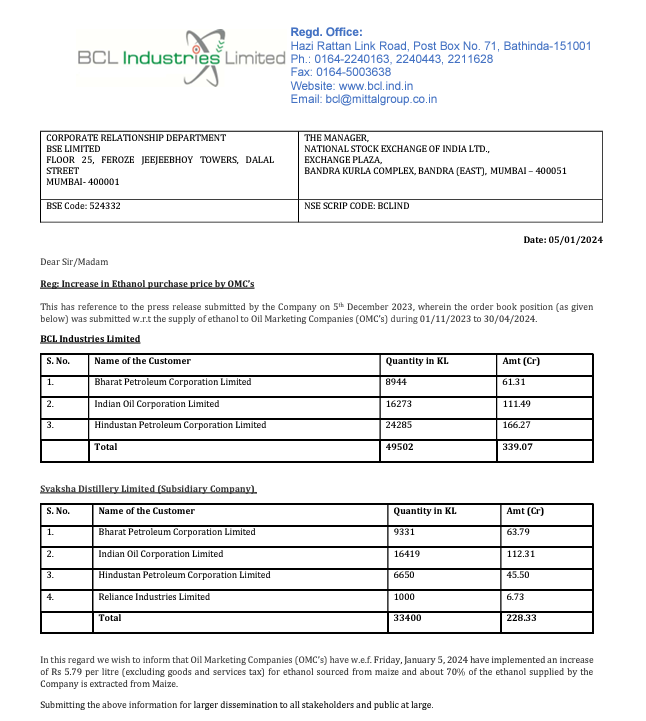

I think the revised rates are applicable to the earlier issued orders also.

This price hike will improve the margins further in addition to the softening of RM price, This could improve PAT by 70-80 Cr annually.

After recent price hikes, Management seems more confident about the sustenance of the Ethanol/Bio-fuel business and taking following steps:

They are planning to invest around 700 crs in the next 3 years in the Bio energy biz.

Source:

https://x.com/ETNowSwadesh/status/1744266267203383312?s=20

https://x.com/ETNOWlive/status/1744311070234423718?s=20

They were talking about Green field expansion in MP also in addition to the batinda 150KLPD, as long as they are investing in the business no issue in holding.

Results:

Significant margin drop is observed in Q3FY24 in the distillery segment (14% → 11%) irrespective of the uptick in revenues at Batinda as well WB plant.

Need to check with management whether the hike in the ethanol price from Jan can get the EBIT margins back to 15% level or not.

There is some inventory gain in this Quarter either in Oil or distillery segment, if i exclude that then results are not so good due to margin pressure.

BCL Ind Quarterly Investor call notes:

Todays call was short one as the Management had to cut short the call due to disturbances at their end.

I like that

Disc: Invested.

Thanks for your quick summary on con call, i have missed the call today.

As per presentation avg realization of ethanol is 66/-, if we consider new price of ~71.86/- then its almost add 20 Cr revenue in Q4. if we assume that RM cost is stable in Q4 then we may see decent jump in profits of Q4.

Agree. I also am of the opinion that most if not all of the price hike will flow into the bottomline. According to Mgmt, the RM prices should remain stable if not cool a bit because of the bumper Maize harvest in Bihar. Also, the ongoing farmer agitation is more for rice/wheat rather than Maize, so it wont have any adverse impact on the company. As mentioned in the presentation, avg. market price of Maize is already higher than MSP.

Mr. Rajendra is talking about new process from Govt to supply maize directly to distilleries at 22.91/- per Kg as compared to CMP of 24/-.

This will reduce risk the fluctuation in RM price and give security to the RM supply to distilleries.

They may complete 150 KLPD ethanol and 75 KLPD bio diesel expansion by FY25 end if they can receive EC in 1 or 2 months.

WB 100KLPD will be completed by Mar/Apr’24. So there will be no further addition in incremental revenues till FY25 end, FY25 Q1& Q2 will add numbers from 100 KLPD (70-80 Cr) and any improvement in RM price will boost the bottom line.

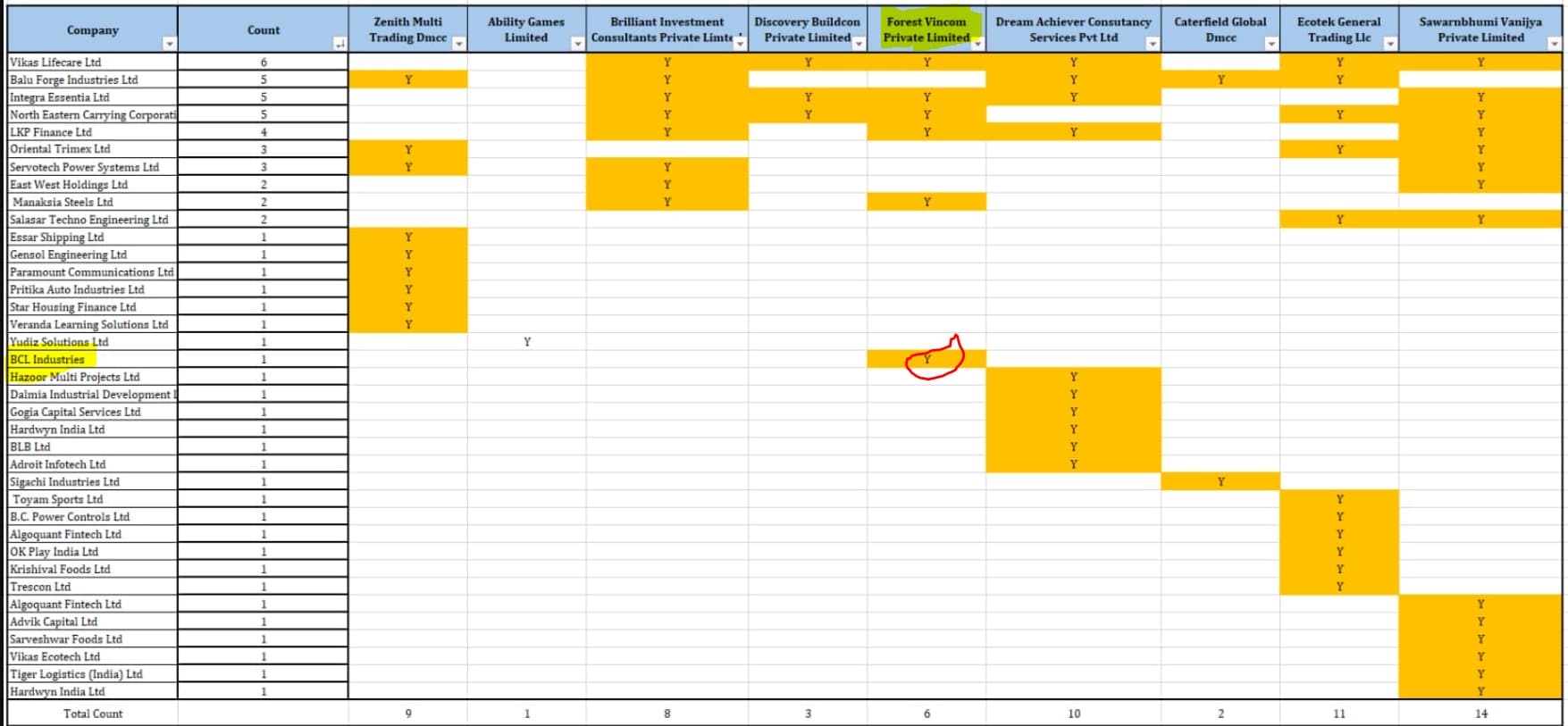

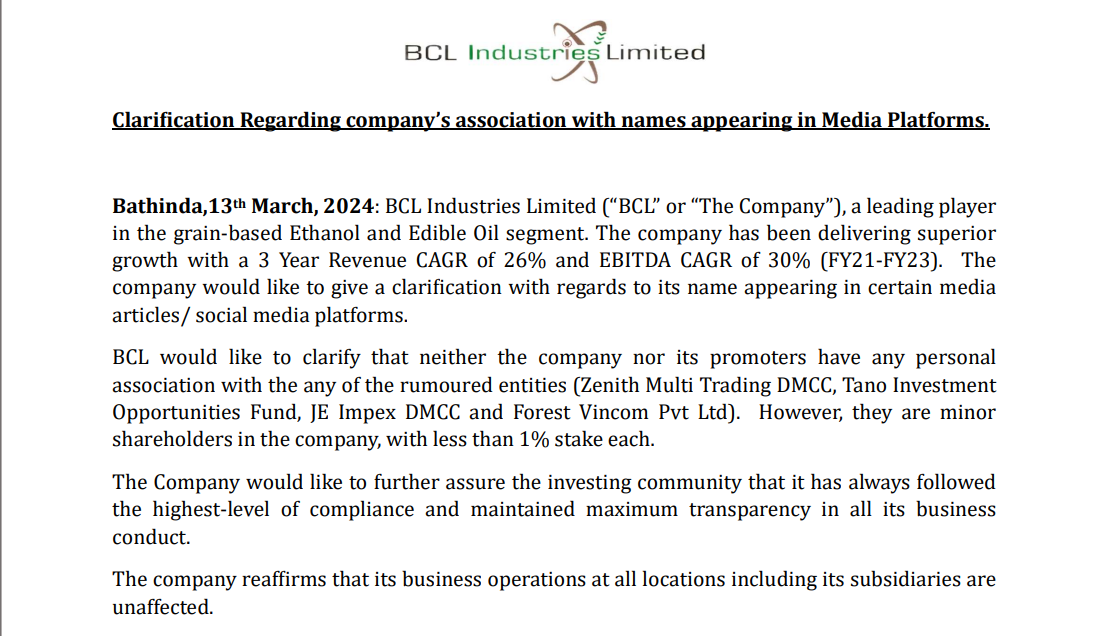

BCL is also dragged in this case due to holding of forex vincom pvt ltd.

I feel that promoters are clean in this case. Forex vincom purchased shares almost 1 year back and there is no pumping and dumping in the price sharply after their purchase, price is almost at same level for next 7-8 Months, unlike other entities where they entered at very low price and exited at the peak.

from where did u get the list, can u share the link

It’s from exchange filing - https://www.bseindia.com/xml-data/corpfiling/AttachLive/8f85d640-324e-472d-a850-f1ef882e7413.pdf

Where did you get such a detail data? I was looking on screener could not get the names of these SH. Appreciate if you can share the source.

I found it in one twitter post, you can search block deals of these companies in trendline.com like below

Any idea, why the price of this stock is continuously falling since last quarter despite of good numbers. I am invested into it .