Bata

1QFY21 takeaways

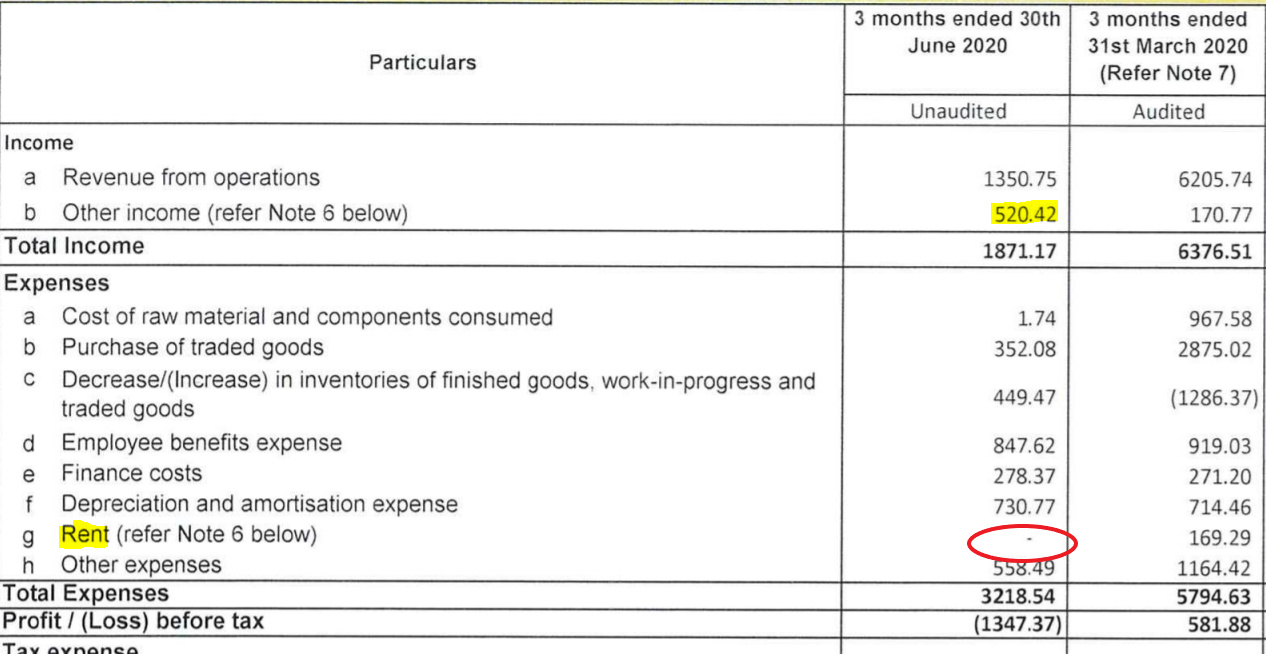

Bata recorded poor revenue in 1QFY21 as stores were entirely shut in April and May and were operational for a limited number of days and working hours in June. Seeing the consumer behavior in the June, Bata believes that signs of improvement are there and the festive season could witness considerable improvement in demand.

During the quarter, retail and non-retail business in terms of footwear pairs were down by 81% and 82%, respectively YoY. Retail business in terms of revenue was 15% of the revenue recorded in 1QFY20 and non-retail was 17% of 1QFY20 revenue.

Bata is witnessing a shift in demand towards open footwear (slippers), casual footwear and sportswear. This has caused a decline in average selling price YoY.

Bata’s End of Season Sale is live since 2.5 weeks and should continue for a week or two. The time frame for the sale would largely be the same as last year but the company will try to align it with the market. The percentage of discount being offered is also in line with the discount offered in FY20. End of season sale revenue contributes approximately 8%-10% to the total turnover for a year.

Bata had hired manpower for its distribution business in February and March of this year and has indicated that it has put hiring on hold for the time being. The company will resume hiring only if necessary.

At present, 85%-90% of the company’s stores are open, except in states like West Bengal and Telangana, where the stores are operational for a limited number of days and for a limited period of time per day. However, footfall is not in line with that of last year.

While the e-commerce business is growing, the contribution from online business is only 5%-6%. It had significantly expanded the range of footwear being sold through the online route.

Bata has adequate inventory at present and does not foresee any shortage of inventory going forward. Bata is trying to maintain its inventory at the same level as last year to avoid shortage or excess inventory. The company is buying input material strictly on need basis.

Bata is expecting schools to reopen in October and is hoping that its inventory of school shoes will clear once the schools open. Bata is selling school shoes both through its physical stores and online channels.

Bata has received complete rent waivers for the lockdown period for most of its properties and has agreed to a revenue sharing model with some landlords for the remaining part of FY21.

Bata has kept advertisement spend on hold and will decide on the same on the basis of the market condition going forward.

Curtailment of Chinese imports would not have a material impact on Bata, as it is not dependent on them. Bata’s imports account for only 4%-5% of total cost for design purposes. In terms of raw

material, Bata sources 95% of its raw material from within India.

On the wholesale side, Bata is entering into partnerships with new distributors and wholesalers and is hopeful of an improvement in business.

Bata has planned to open over 500 franchisee stores in the next 3-4 years. At present, Bata has ~150 franchisee stores. Business in Tier 2/3/4 cities is improving at a faster pace as compared to metro cities. Bata indicated that it derives ~50% of its revenue from Top 10 cities.

The management stated that ~40% of revenue comes from the sale of leather shoes. This is followed by sale of school shoes, ladies footwear, etc. The margins and ASP for leather shoes is higher than that of casual slippers.