Disclaimer : i am invested in bandhan bank, I am not a sebi registered investment advisor. This is not investment advice. Please do your due diligence before investing.

1 Like

From the concall the management mentioned that 180+ DPD accounts were written off amounting to ~3400cr

They have utilised ~2000cr from the stress provisions and revised the collection estimates from the stressed borrowers to 1500cr from 2500cr leading to a higher provisioning in Q2

I have a feeling that the slippages will be high for the second half as well but it is looking like next FY will be normal

Also they have tightened their credit standards (NPA customers who pay in full wont immediately get another loan, they have to wait for months) and inducated loan growth will slow down to 18-20%

Three very bad years for bandhan, covid 1 and 2 and assam floods.

With their guidance of 20% RoE from next year it implies a valuation of ~12PE

4 Likes

The reaction to the results is extreme. The management revised the credit cost to 3% ± 0.15% from 2.5% earlier so even on the upper end of 3.15% credit cost for the FY, H2 should have a credit cost of 2.5%

I think the steady state pat per quater should be 800cr (similar to Q1) and if i add the 600cr hit in Q2 we should end this year with 2600cr implying a valuation of 14PE and next year if things normalize with a 15% growth we get 9 PE which is reasonable

2.5% credit cost seems conservative and i have a feeling that the management will start creating more provisions going forward. Once the earnings are predictable the valuations should improve as well.

One risk i see to earning is a delay in CGFMU payout which would force the bank to take the provisions from the PnL

The more reasonable ratio to value banks and nbfcs is pb ratio.

2 Likes

I feel PB is not a good metric here since the return ratios (RoE and RoA) are much higher than a regular bank which means the book would grown faster

Do you have any strong reasons why PB would be more apt?

A good bank or nbfc with good track record trades at high pb ratio. pat can be manipulated easily by lowering or increasing the provision. so roa, roe and asset quality determines the pb ratio. check hdfc bank pb ratio and bandhan bank pb ratio for example. for past 7-8 years. higher the roe higher the pb ratio. provided that they have good history. check arman finance pb ratio. ot has 30 roe trades at premium pb ratio. when u buy bank or nbfc u r buying the equity portion which is nothing but cash. what roe the bank or nbfc can generate determines at what multiple u will buy. some bad banks like the PSU banks trade at cheap pb ratio.

3 Likes

Agreed but book value can also be inaccurate, if there are a large number of provisions that have to be done the book value itself will be volatile and it is easier to concentrate on the earnings

Bandhan has a book of 18k crores and an unprovided stress pool of 4k cr so focusing on pb right now will make things complicated and hence I am using cashfows

The corellation between book value and earning espically in banking is very high. This is majorly becasue you need to maintain CET ratio. You have to lend more to earn more.

There are 4 category you can make out of this

-

High PE high PB- These company banks get high valuation becasue of brand. Like hdfc, kotak

-

Hight PE low PB- You can conclude that the banks has lot of money but is unable to make profits. This is generally going to be temporary because of high provision or low efficiency and there is scope of improvement

-

High PB low PE- In this case the bank is making unsustainable profits becasue it does not have the book size to support earnings or the earnings are being distrubuted to less shareholders and dilution is likely. These cases should be avoided

4 Low PB low PE- this is generally for psu becasue of their image or some pvt banks like federal bank because of concentration in kerala.

Bandhan bank is getting a PB of 2.2 which is what axis and indusind are getting today. Book value also shows your ability to absorbe shocks.

Despite bandhan having low credibility, lower asset siize and lower capibility to absorbe shocks than axis,indus it was getting PB of 3.

But market should not discount the NIM bandhan bank has and further correction in this counter can be a good opportunity. People over react on banking stocks always. We can see the hammering in RBL and UJJIVAN and there after the bounce back.

10 Likes

Unlike HDFC and ICICI groups, kotak is still a conglomerate of all BFSI. So it’s value is generally higher.

Excellent explanation by @manhar. Thanks!

3 Likes

Have invested in this post pandemic , mainly depending on the experience of the management. Not sure why they are not able to break out of this range over the past 1.5 years. The latest NPA sale was a disappointment in my personal view as I had placed a good amount of trust in their words about their collection rates etc.

Still waiting as I feel they have good room to grow - e.g. main focus is only east. Guessing that the GRUH synergy factors have not yet come into play.

Am going to track/follow for 2-3 more quarters before deciding.

- Disclosure. Invested. One of top %ages in my portfolio.

2 Likes

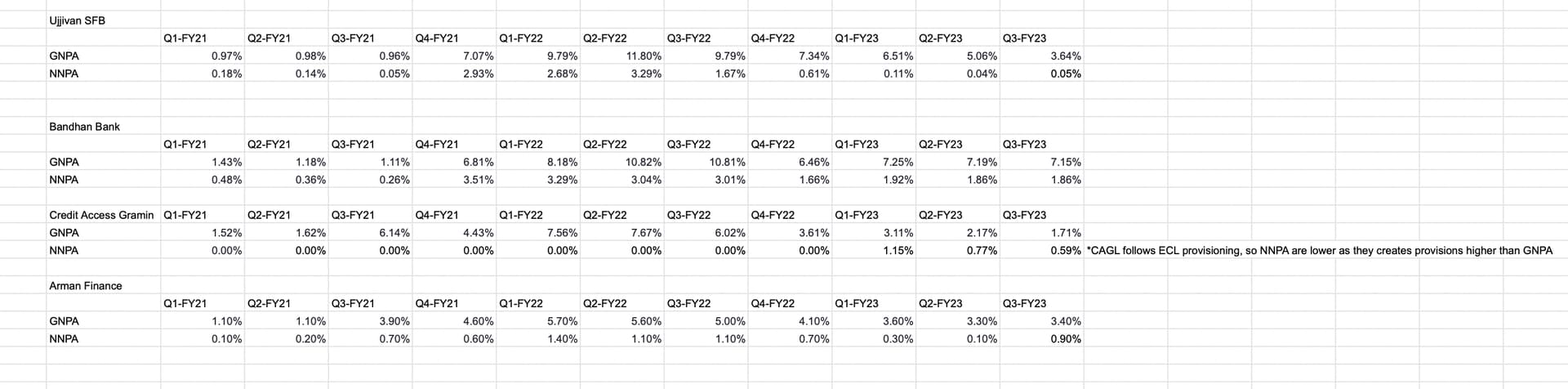

My view: Clear derating of business perception, all the good things are factored in initially and PB is flying high and now its just getting back more relatable valuation. I will give some parallel with Ujjivan bank which went on similar path during covid. Ujjivan has higher share of microfinance. They also crossed GNPA of 10+ %, they went ahead and provided for almost entire GNPA book and now they have nearly nil NNPA and credit cost. This clearly marks the base point for Ujjivan and it started recovering both from stock price and profitability perspective. But in case of Bandhan, even after providing for large chunk of GNPA, still they are guiding for 3% credit cost. Management trying their best, but there is no clear visibility in turnaround

On pure stock price, Bandhan is it still trading at PB of 2 which is okaish valuation and not too cheap. Even during deepest covid fear of Apr, May 2022, it is trading at 2. This also does not give deep value like RBL,UJJIVAN, Karnataka, South Indian, KVB, which everyone entered in recent times and made money. After seeing what this bank has gone through and still having its effects of covid, when every other bank back to their normal days, why would anyone value this at PB of 4. This may keep on having sideward movement for sometime.

This will definitely come back, but we need to wait little longer, but not sure whether market gives similiar premium valuation. What i think is, gone are those days, where Bandhan commands premium valuation due to growth rate, if we see other premium commanding banks like HDFC, ICICI, Kotak, AU, on how they navigated covid. Now people have seen what will happen to Bandhan when some unforeseen things happen.

DISC: No investment, just tracking as part of banking sector.

7 Likes

My views are that it has been a long and frustrating journey but we are close to the bottom of the credit cycle for bandhan. I sipped the stock for a year post the promoter disinvestment, the share price is realy beaten down do i dont see a point in selling now.

My initial thesis of investing for the long term has changed after i saw how aggressive the large private banks are getting rural finance, how i feel the best customers of bandhan will eventually move to hdfc and axis. This coupled with the fact that the management has gided for lower growth of 20% in the last Q2 con call has dampened my bullishness.

The rising interest rates also are compressing NIMs since the lending is mainly fixed rate and the RBI reversal of the PSL income is a big damper, they lose fee income and have to create RDIF deposits by raising expensive bulk deposits

But with the actions that the managent has taken over the last week with the arc sale and the CGFMU happening before the next quater makes me thing we are closer to the end of the credit cycle for bandhan. The NIMs should normalize by next year once the hikes taken by the bank flow through.

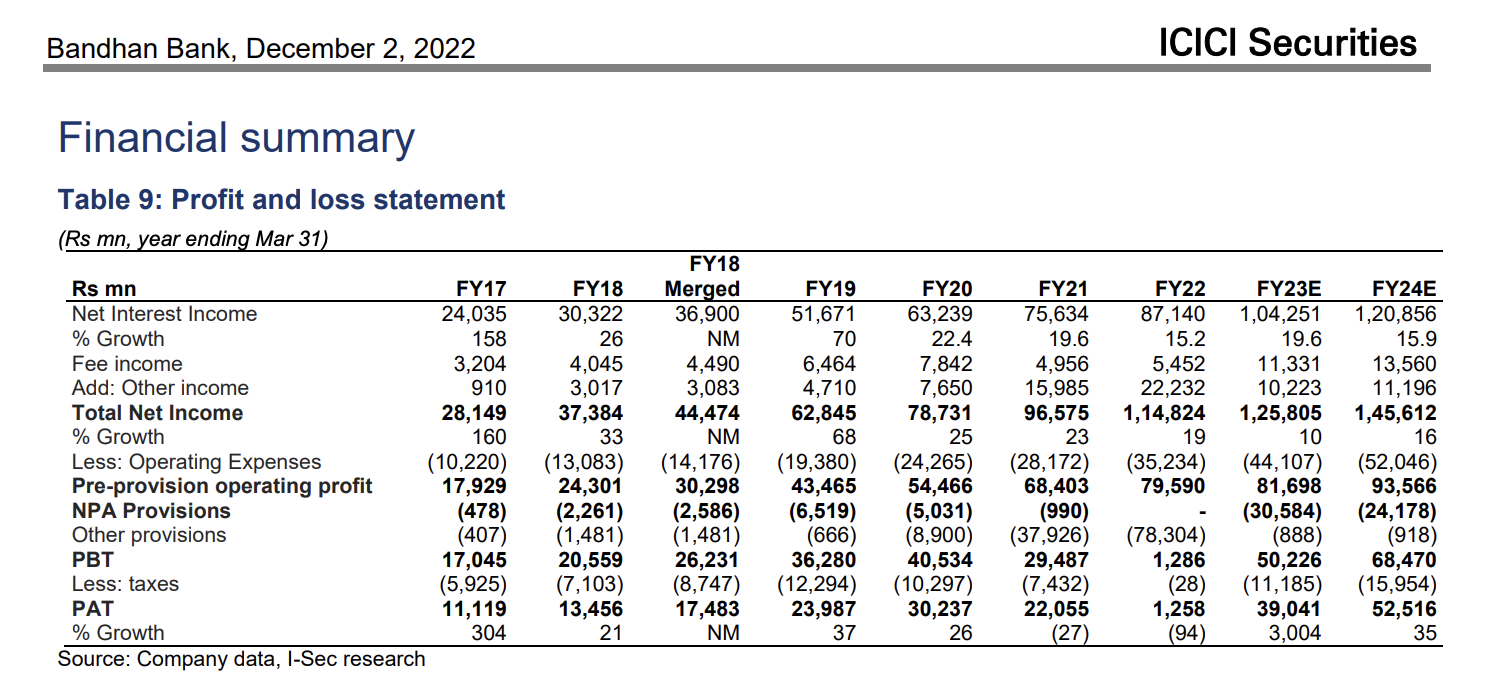

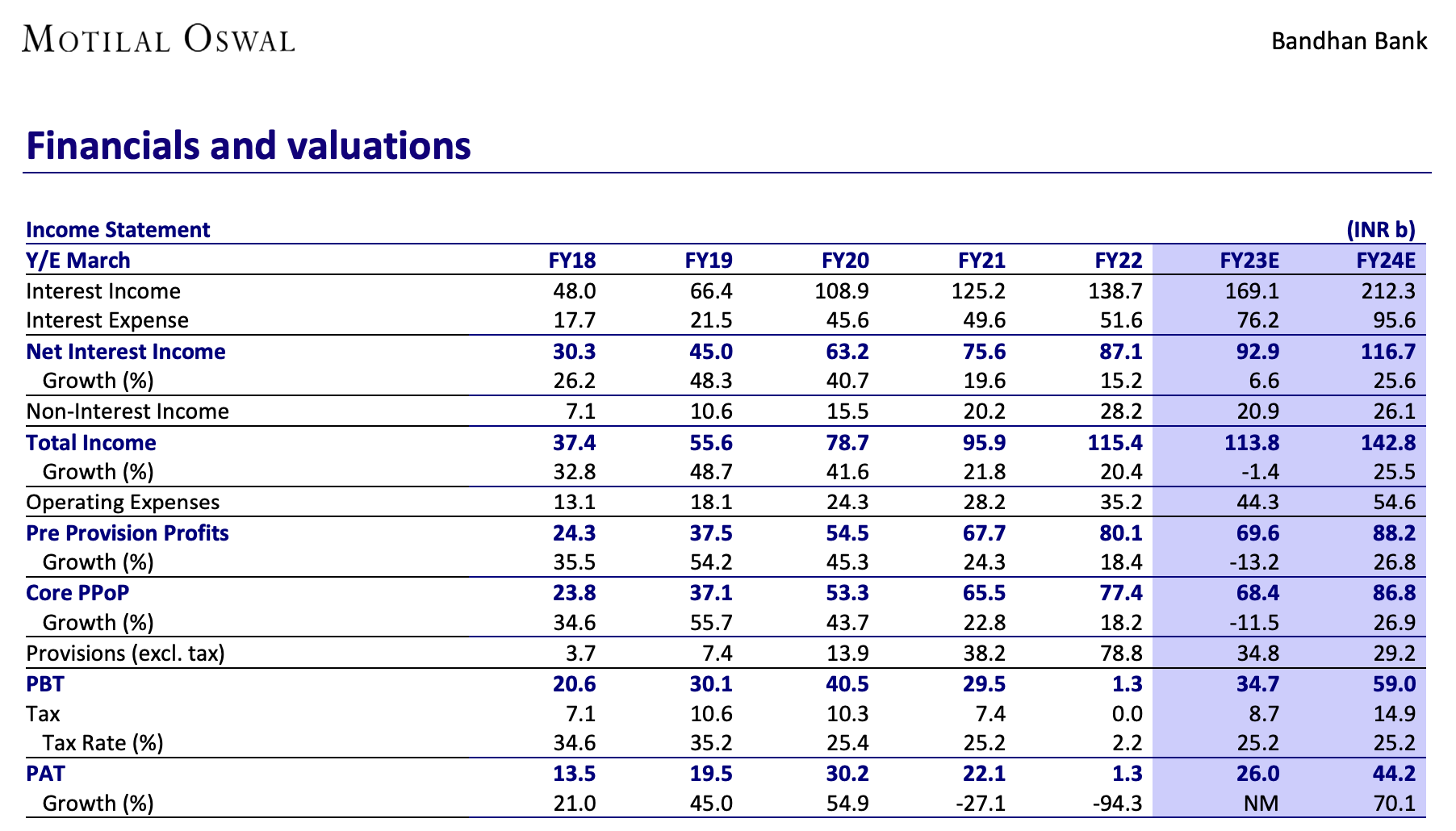

If there is no forth wave of covid or anything that can cause a major macro shock we should see a very strong earnings next year, my estimate is ~40k cr (Motilal and icici sec have estimates 44-52k cr) so still holding on atleast for a year and then evaluate things from there

6 Likes

Hi guys,

I would like to present my view on Bandhan bank today. Since I have recently started analyzing this bank I might miss some points and I might have some understanding gap as well.

Lets start from everything related to stress pool.

-

As we all know the reason for increase in SMA1,SMA2,NPA(DPD bucket) in FY23 was majorly because of 4660cr of restructure book coming out of moratorium and moving into the DPD bucket.

This movement started from Q4 FY22 and it has a lag effect on provisioning or write-off. EXAMPLE- If SMA2 moves to NPA more provisioning is required and Bandhan bank has a policy to write-off NPA after 180days so write-off eats provisioning and this creates more requirement. -

I see Q3 as the last quarter which might have some impact of the restructured pool. Q2 FY23 they had slippage of 3954cr out of this the non restructured slippage was 1200cr( For Q1 FY23 non restructured was 750cr).

Bank did write off of 3539cr for Q2 and total provision of 1280cr. Total recovery and upgrade of 530cr for Q2 and 538cr for Q1. -

They have already done provision of 1900cr for H1 and though they did want to give any figure but still they said for H2 as per credit cost it should be 1100cr (±200cr).

ANALYSIS

-

Now on the conversative side I can assume 1000cr of non-restructured slippage for Q3( This is between 750crQ1 and 1200crQ2) This is conservative because collection efficiency has improved in provisional figures for Q3 and Q2 has floods impact hence higher slippage for Q2.

Now EEB restructure pool is 0 we will not have slippage form restructured pool.They have a seasonality in their business(H2 is better than H1 can see from previous result but don’t know the logic) so recovery should be high for Q3 but let us take 500cr of recovery and upgrade for Q3.

Last quarter net non restructured slippage was (1200-500) 700cr taking 70% provision for this 490cr this means rest of the provision was because of write-off which is 750cr. -

Now for Q3 assumed net slippage is 500cr so 80% provision comes out to be 400cr. To be extremely conservative let us take 70% provision form write-off of Q2 amount. This is 70% of 750cr so 530cr.(This is conservative because they cannot have write-off of 2800cr this quarter this is 55% of NPA)

-

So on the conservative side we can say 1000cr provision for this quarter(Though I have a gut feeling that this is too high).

-

Now they are receiving 950cr(100% confirmed) from CGMFU (I don’t know how does accounting happen here. Does this flow through profit or can be used for provisioning). This amount completely covers Q3 conservative provision estimates.

-

They are expecting 150cr from assam relief in Q3(But they don’t have 100% clarity here)

SUMMING UP

- Management is saying 1300cr max provision for H2 I am assuming 1000cr for Q3 which looks like it completely gets sett off from CGMFU recovery.

- Assam Relief 150Cr expected in Q3 and taking previous year trend it should be 500cr++ for Q4(conservative)

- Net interest income is higher for H2 because of seasonality and recovery is also high.

- By Q4 things get normalized.

- 65% of advances is Fixed so having thought time with NIM they are expecting it to normalize by Q4(8%).

I don’t want to project profit for Q3 will want to wait and watch but from above post we can see provision requirement.

I love predicting price as well which I will do after Q3. I had lot more to talk but post will become too long. Any body having any question I would love to answer.

4% of portfolio at CMV of portfolio with 239 avg price.

Thankyou

8 Likes

Thank you for sharing your analysis on Bandhan Bank. It seems like you have a good understanding of the bank’s financials and provisioning requirements.

Regarding your question on the accounting treatment of the recovery from CGMFU, it depends on the nature of the recovery. If classified as an exceptional item, it would flow through the profit and loss statement. However, if it is classified as a regulatory or statutory adjustment, it would flow through the balance sheet as a provision reduction.

It’s always good to be conservative in your estimates, and it seems like you have taken a conservative approach in your provision estimates for Q3. The expected recovery from Assam relief is also a positive development, but as you mentioned, it’s not yet fully confirmed.

Overall, it’s good to see that you are keeping a close eye on the bank’s financials and are willing to wait and watch before making any projections or predictions.

1 Like

Seems entire sector is out of the GNPA and Asset Quality issues leaving behind just a Bandhan Bank

Secondly,

They sold bad loans worth 8900 crores to ARC for 801 crores.

Seems the wheels have come off this one, and stock is back to covid lows. Post aggressive disbursements just post covid. Loans coming back to bite them when the sector is recovering…

Key lesson for me through this case study: Stay open to evolving facts and be extra careful when things go wrong in banks. As often we don’t know the extent of black hole in asset quality.

Disc: invested in Arman & Ujjivan Fin services. Tracking Bandhan as a case study. Views can change is situation evolves (Be open like 1.5 years ago on aggressive lending).

(Never invested in Bandhan, tracking the case study)

7 Likes

Alleged sharp lending practice at Bandhan.

6 Likes

Clarification from Bank : The said media article is baseless, malicious and far from the truth.

1 Like

Did Bandhan bank started lending to other areas/segments in housing segment apart from what GRUH finance originally lending? And is it any different from Aavas and Home First Finance book?

Thank you for the analysis. Could you provide full form and definition of the following abbreviation you have use.

1.SMA1

2.SMA2

3.DPD

4.EEB

5.CGMFU

Any updates on outlook after Q2 FY24 concall.