Hi, can anyone please share the registration link or connection details for today’s Earnings Call?

BANDHAN BANK HAS GIVEN LOAN OF RS 22750/-CR.

85% has already paid by customer.

Pending amount Rs 3310cr.

bank has received 927 and 300cr additionally from customer and authority.

Now remaining amount is 2283cr. Bank has made provision 88% which comes to 2009cr.

Remaining amount is just 280cr. Calculated conservatively.

I am holding the shares.

4 Likes

NCGTC forensic audit of evergreen loans

Same issues are raised last year around April 2023.

Waiting for the outcome to size the issue (if they found any)

2 Likes

I am reading about this business and trying to answer the question - Why is the stock price under tremendous pressure? Few things that caught immediate attention were:

- Lack of growth in Housing Finance portfolio: Merged GRUH, which had a portfolio of ~₹181 bn, in Dec19. GRUH as an independent company used to grow at ~20% CAGR, implying an expected loan book of ~₹375 bn by Dec23. However, overall Housing Asset as on Dec23 is ~₹284 bn. In the last 4 years, two heads for ‘Housing Finance’ have moved out.

- Uncertainty due to the ongoing forensic audit initiated by National Credit Guarantee Trustee Company Ltd. (NCGTC).

- Higher unsecured book | Geographical concentration | Loan book concentration: These 3 are being mitigated slowly by the management. However, they seem to be progressing slowly.

@manhar : Would appreciate your latest view since you would have reflected on this business for more than a year now.

2 Likes

Hi sir,

I sold them about a year back, I am not tracking them anymore.

The biggest learning for me was banking is like quick sand you don’t know the end, you don’t know how bad the book is , them moment you think thing are improving you are going deeper and deeper into the sand.

I though they were over provisioned and now we can see some write backs, lol a banker would never even in his dream writeback, max he can do is less provision next qtr

The point is I tried to predict the recover and my lesson was in banks the cycle are long don’t predict let them show some sigh of recovery, let them show 2 good qtrs, you don’t have to buy it at bottom, we can miss some 20%, 30% return

@Surender don’t have much to say on business , just these small learnings

Disc- sold 1yrs back

6 Likes

My few takes on banking / NBFC

- Financial industry is backbone of India’s economy and their health/stability is important for economic growth to sustain.

- Hence these are highly regulated industry

- RBI is now continuously monitoring them to predict early warning signals and then reduce/mitigate any structural weaknesses that may arise.

- As per me this is good for long term sustained and stable growth (especially during downturn) of the economy and the banks as well.

- RBI is also ensuring that there is significant transparency and reasonableness to the charges they avail from clients, especially retail customers, this will show some dip in fee income from penal charges etc.

- The above points are giving me confidence of investing in low valued/corrected stocks like Bandhan.

- However don’t think sustainability of very high valuation (Bajaj Finance, for instance) in this segment is possible.

Bandhan_Bank_13Mar24_Kotak_Inst.pdf (484.8 KB)

CEO Chandra Shekhar Ghosh resigns!

We will never know whether he resigned due to “retirement” or RBI action forced him,seeing the performance of the bank in last few years and ngctc audit latter seems to have more weight because in 2021 they had sought a 5 year extension for his tenure but RBI granted only 3 years extension.

1 Like

Kotak Buy recco reason

We took a call to be positive on the bank based on the following metrics, but note that the current development would weigh in a little to our reasons.

(1) There has been an improvement in asset-quality metrics in recent quarters, though stress is still higher than peers. While we have no visibility on the outcome of the independent audit, we made a macro call that the microfinance industry is largely returning to normalcy and Bandhan would soon follow suit.

(2) The liability franchise was largely unaffected by this crisis.

(3) The bank was steadily strengthening its senior management team, and our recent conversation suggested that the current team has the requisite experience to carry the bank forward.

(4) Mr Ghosh would continue to oversee the bank.

(5) Bandhan Bank was relatively inexpensive (given the above factors) in the segment in which it is operating. The risk-reward appeared to be favorable.

Bandhan_Bank_08April2024_Kotak_Insti.pdf (455.2 KB)

2 Likes

Bandhan Bank Q4 Concall Summary

- Expecting INR 60-80 crore from ARC (Asset Reconstruction Company) this year, which they sold last year.

- Targeting 1.8% credit cost.

- Targeting 18% growth in the overall loan book (14% for Emerging Entrepreneurs Portfolio (EEP)).

- Targeting 5% Gross Non-Performing Assets (GNPA) for EEP.

- Confident about EEP.

- Current Net Interest Margin (NIM) of 7.3% will face some pressure as they diversify.

- Targeting 3% slippage ratio.

- Operating cost is high for this fiscal year and will remain the same in the next fiscal year.

- Expecting INR 1,200 crore recovery from audits (CGFMU).

- Targeting 2.5% Net Non-Performing Assets (NNPA).

- The portfolios written off are from the years 2019-20 and 2020-21 (pre-pandemic period).

- The search for a new CEO is ongoing.

- Expecting recoveries from written-off loans as frontline staff may not be aware that these accounts have been written off.

- Individual EEP loan size is INR 1.5 lakh (50 basis points lower interest rate compared to Group EEP).

Disclosure - Not invested, worried about the asset quality as management is always optimistic and as the company is looking for a new CEO."

4 Likes

Bandhan Bank Q1 FY25 Concall Summary

- Ratan Kumar Kesh has been appointed as the interim MD and CEO of the company, effective from July 10, 2024 for a period of 3 months or until the new appointment whichever happens earlier.

- Q1 previously has been a soft quarter for the bank, however there were improvements this time. Reason stated was due to more focus on secure lending. They’re trying to reduce the seasonality effect.

- There was slight increase in the cost of fund but they were able to maintain their margins.

- Gross NPA is at 4.2% and net NPA is at 1.1% versus 3.8% and 1.1 respectively in Q4FY24.

- Due to RBI mandate on risk weights, the board approved an increase in the risk weight for the EEB (Emerging Entrepreneurs Business) portfolio from 75% to 125% which resulted in decrease of CRAR by 362 basis points.

- Some new products launched recently - LCs, Forex, Bank Guarantees, Bill Invoicing and remittances in our transaction banking space, BharatQR, Tax Collection service.

- 5 states contributed 59% of the gross advances, West Bengal with 24%. 5 states contributed about 64% of total deposits of which West Bengal contributed 39%.

- Continuing with the guidance of NIMs in the range of 7% to 7.5%

- The bank intends to maintain a stable outlook on its lending to NBFC MFIs and more focus on secured lending, mention of muted growth in the segment.

- The bank plans to continue its strategy of growing its secured loan book, with a projected loan book growth rate of 18% to 20% with higher deposit rate than the secured loan book.

- Not looking to raise capital, confident to maintain growth and risk for the next 3 years.

- New branches will be lesser than previously, bank staff has increased however going forward, the addition may be less compared to last 3 years due to digitization.

I’ve tried to mention whatever points I felt were of value. If someone wants to add more points feel free to do so. For the number crunching, Link to PPT

Any and every feedback is appreciated.

1 Like

1 Like

Lot of noice around Microfinance portfolio. Can we say this is the quarter with max pain and situatatio will start improving from here on once the interest rate start reducing ?

Bandhan Bank keep saying their GNPA will remain in the range of 3.25 to 3.6 %. I hope they deliever same this quarter.

3 Likes

IMO… Indusind bank offers a better overall package for future after today’s hammering.

3 Likes

Is the stock in distribution phase now? So many analysts upgraded it ![]()

2 Likes

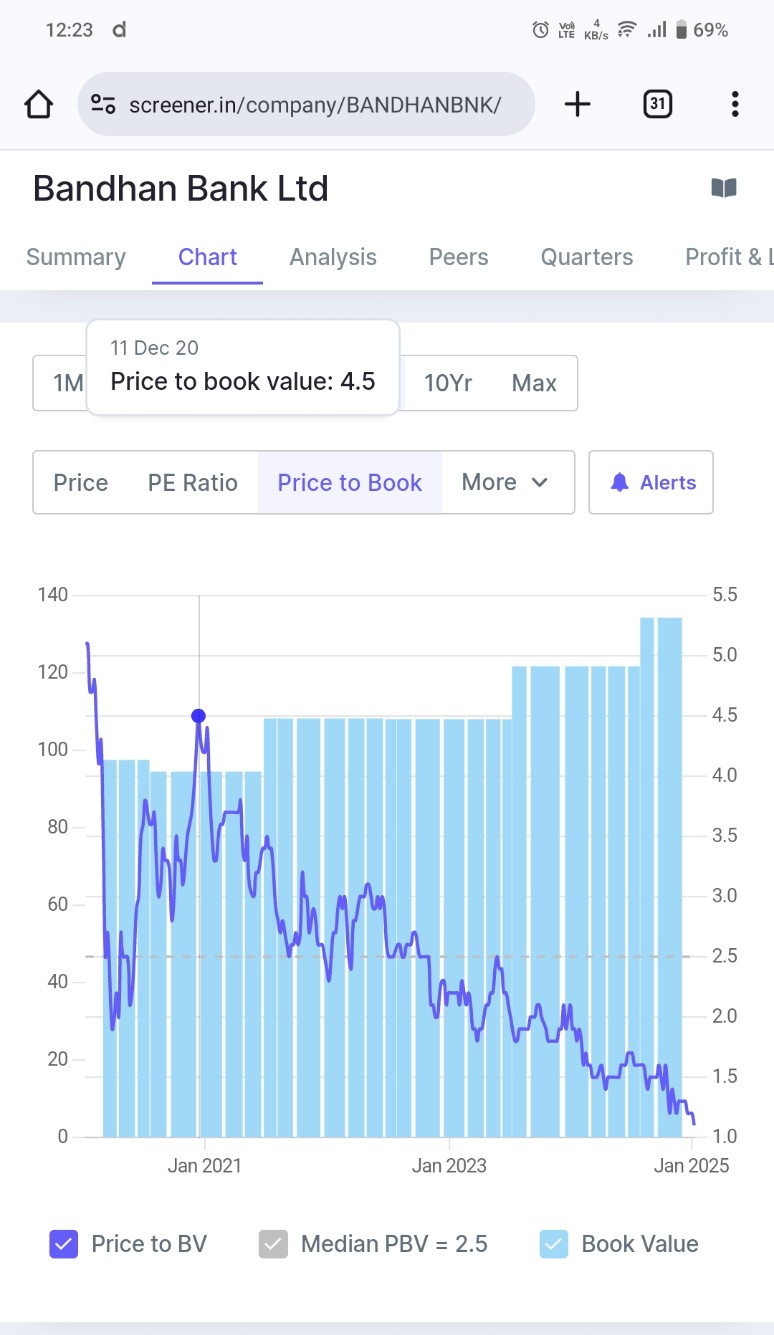

The 2020 support price (152) is also broken now and is trending down (no supports now)

Company is profitable and Price to book is 1.15 with Price to earnings of 8.7 now

2 Likes

As per screener there are contingent liabilities to the tune of 9214 Cr. What are these liabilities?

1 Like

Bandhan seems to have become a CXO Factory for all ex-gruh leadership.

Is there any single leader who stayed till date with bandhan?

From my limited research it would be interesting to make a chart of all the leaders and where they went – and look at those companies instead !

2 Likes