Related with microfinance industry in general. Bandhan bank had mentioned that many of their customers were capable of paying even during the lockdown but the collection executives could not visit them and conduct the weekly meetings . i think if these customers transition to digital modes of repayment everybody will be benefited.

Repayments are resing in micro loans

Repayment rising in micro loans; mixed bag for MSME, retail - The Economic Times.

Disclaimer : i am invested , my opinions my be biased.

Okay this is off topic, but what i am about to say will definitely help vp boarders and their families

All of us here are busy seeking ways to create wealth , what is often more important is defending the wealth we have created or will create in the future.

i have done a lot of research on bank mediclaim . Bandhan bank offers one of the most “cost effective”(did a lot of comparison) mediclaim for youngsters and SENIOR CITIZENS up to age 70. its in tieup with an established insurance company. On the bank website only the features are mentioned, premium amount is not mentioned for competitive reasons

it has very good features like doubling of sum asssured if there is a critical illness like cancer.

and premiums generally remain stable over long periods of time unlike individual policies

this Bank mediclaim falls under group insurance and generally group insurance is better than individual policies in claim settlement.

Premium doesnt increase the next year just because you make a claim unlike some individual health policies.

Ps : can shift this to a new topic called mediclaim if the mods agree. i have mentioned the above because in my life i have seen too many people come to grief due to inadequate(people overestimate ) health ,life coverage, personal accident & critical illness coverage.

Note :this is not some kind of promotion.

Disclaimer :i am invested in bandhan bank , my views may be biased .

i personally believe the borrowers bandhan lends to are not as hard hit as the market believes. And the fact that bandhan lends to women who use the money to increase their business as opposed to pure consumption like a mobile phone purchase loan is a huge plus point.

Disclaimer :i am invested in bandhan bank , my views may be biased

My understanding is that this doesn’t say much, as lets say they get a peak efficiency of 90% which means 10%*Leverage(=4) ie. 40% MF book is lost.

What is critical for any valuation call is - What % of book would be lost, till then valuations remain a guesswork. more so for unsecured lenders.

All one can do now is compare different MF lenders at one point of time and see how each is performing relatively, but should one like this data or get scared of is anyone’s guess.

Bajaj Finance has only 27% book under moratorium and still people are scared. That is the trouble of a levered business.

90%collection efficiency means 10% of the loan book which of course includes leverage is either irrecoverably on dpd or delayed. I am unable to understand as to how it can be considered as 40%.Could u PL explain for my understanding. Thanks

Disc: Invested

.

Banks are leveraged entities, give loans as a multiple of equity(Book value). Total loan book is leveraged 3-4 times for Bandhan and 7-10 times for bigger banks or housing finance companies. Bandhan bank leverage is low because it is into microfinance.

So if a bank has equity of 100 and it lends for 400. If 10% of 400 is lost i.e. 40. Which means out of equity of 100 only 60 is left. This 100 or 60 is equity or book value per share and banks are valued as a multiple of this number.

If 25% is lost, 25%*4=100 i.e. entire equity is gone… Not saying this will happen here.

PSU banks can have 10% NPAs and 10x leverage - so entire book comes to question. So PSU banks need regular input of capital from government.

Hi.

I just finished reading ‘Bandhan: The Making Of A Bank’.

I would encourage anyone who is looking to understand the business model of Bandhan Bank to give it a read.

Business models sometimes go beyond numbers, graphs and ratios (which are good for Bandhan Bank by the way). Business models involve understanding the demand and supply dynamics at the grass root level.

Microfinance was championed as a financial tool for poverty alleviation but no business model has been as successful as Bandhan Bank.

It has taken time and persistent effort by the management to create a branch network in rural India. Creating this network is not as easy as opening a branch in a city. Any ‘financial’ institution looking to do daily transactions with the rural household has to gain acceptance locally. It has to become a part of the village social dynamics and be accepted by people. Bandhan Bank has done just this.

For example, a woman defaulted on her weekly payment to a field collection officer. When the officer went for collection, he found that her children were alone at home and crying due to hunger. The officer took the children to the office, fed them and then dropped them back home. The mother made the outstanding payment that very night.

You might view this as another instance of a good man showing humanity. I think that this a durable moat. Bandhan Bank has woven itself into the social fabric of the working woman of the village household.

Not specifically directed to this instance, but just a general comment.

In my view, any books or features are to be taken as propaganda pieces. While it may provide some insight of the internal working / thought process, most of the negatives are glossed over or not dealt with satisfactorily. Also interesting tit bits (whether fact or fiction is anybody’s guess) are splattered all throughout the write up which make the persons / brands relatable by latching to the readers emotions. The whole idea is to weave a narrative which becomes a frame of reference for future conversations. Hence I personally take such books with a pinch of salt (case in point books on Biyani, AM Naik etc). The only bottom line that I want to highlight is that advertising is an all pervasive phenomenon and impacts our judgement (be it nepo Bollywood star or goods or people or brands) and we need to be constantly on the watch for subliminal messaging trying to distort our thought process.

Hence, as an investor it is much better to follow investigative pieces (if available) and try to find out negative evidence to revalidate our investment thesis.

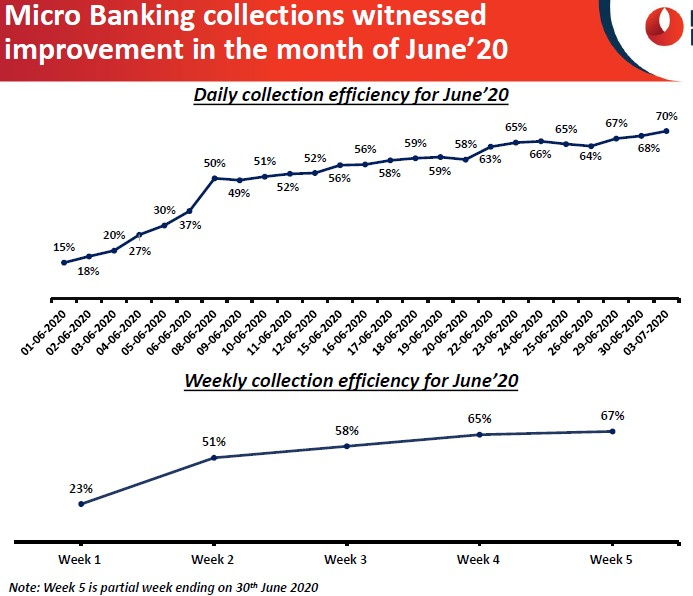

Bandhan Bank’s Micro-banking collection efficiency has reached to 67% at end of Jun-20 from 25% in 1st week of Jun-20. They are expecting 90-95% collection efficiency by Sep-20

All their micro-banking customers were given mandatory Moratorium till 31/May/2020

Mortgage book and SME book moratorium at Jun-20 end is close to 20% and 25% respectively

55% of their customers are in 4th cycle and above

They expected increase in Credit cost in FY21 by 150bps to 200bps

Can you please share source of information for this?. Seems 67% is quite decent collection efficiency given current situation

Interaction with Bandhan’s Management

Official communication from Bandhan bank7911a5b9-897c-46e8-b492-cb432d2a2802.pdf (1.1 MB)

Mortarium is at 30% which by given backdrop too good.

70% collection efficiency in such uncertain times is fantastic . it validates what bandhan mgmt has been saying all along "borrowers are ready to pay but our field staff couldnt reach them "

punishment meted out to bandhan stock over the past few months has been rather excessive .

targets of 65 (doomsday scenarios) were being painted.

if they can raise casa ratio to around 43% in the next two years it would be great.

bandhan offers a higher interest rate above 1 lac .

i personally feel micro borrowers are a lot more reliable than big corporates when it comes to repayment. the only risk being the government announcing some kind of waiver.

Still if the borrowers who use the money from bandhan for increasing business stop paying where will they borrow from in the future .

there has been talk about ESG (socially responsible investing) in other topics on the vp forum. bandhan definitely makes the cut for such a portfolio because

the interest rates charged by bandhan are a lot lot lower than rural moneylenders (can be as higher than 60 % or more per annum ) who lend to women at the bottom of the pyramid.

infact if bandhan reduces its interest rates excessively theres a risk of borrowers turning lenders themselves.

Disclaimer :i am invested in bandhan bank , my views may be biased

Bandhan Bank Q1FY21 results

KEY HIGHLIGHTS -

- During the quarter the Bank has taken accelerated additional provision on standard advances amounting to 750 crore. With this provision and additional Standard Assets provision that Bank is carrying in Micro banking portfolio total additional provision in books stands at 1,769 crore

- During the quarter, the number of employees of the bank has gone up from 39,750 to 41,563

- Added 0.21 million Customer during the quarter with total customer base reaching to 20.31 million (Micro Banking- 15.46 million, Non Micro– 4.57 million and Housing – 0.28 million)

- During the quarter ended June 30, 2020, the Bank has received Rs 474cr (quarter ended June 30, 2019 Rs 370cr) from sale of Priority Sector Lending Certificates. Out of the aforesaid amount, Rs 118.5cr (quarter ended June 30, 2019 Rs 92.5cr) has been recognised in the Profit and Loss Account during the quarter on an equated basis from the quarter in which the sale has occured and the remaining amount of Rs 355.5cr (quarter ended June 30, 2019 Rs 277.5cr) will be recognised in the Profit and Loss Account over the remaining three quarters.

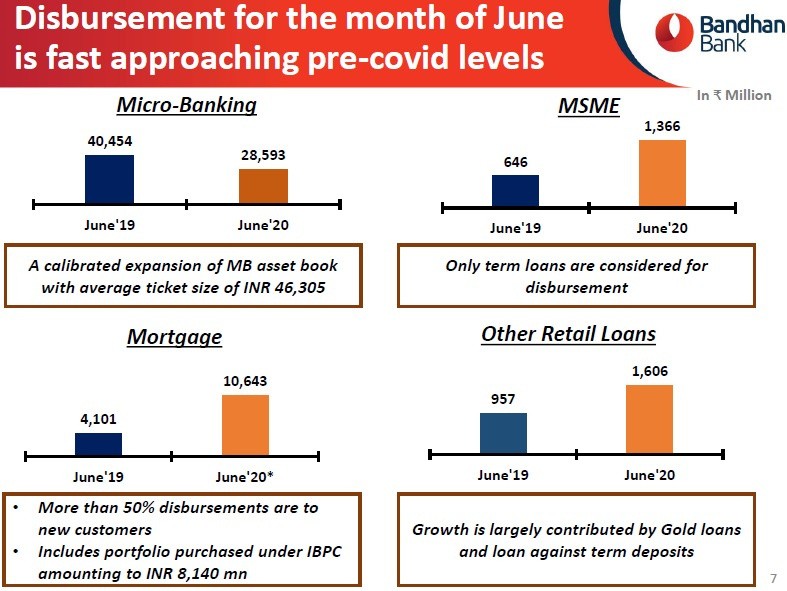

- Average ticket size of micro-banking loans is ₹46,305

Bandhan Bank Q1FY21 Earnings Call Highlights:

Participants:

- Elara Securities

- Buena Vista Fund Management

- ICICI Prudential Asset Management

- Macquarie

- ICICI Securities

- Kotak

- JP Morgan

- CLSA

- Reliance Nippon Life

- Enam

- IIFL

- Motilal Oswal Asset Management

- Emkay Global

Business Overview:

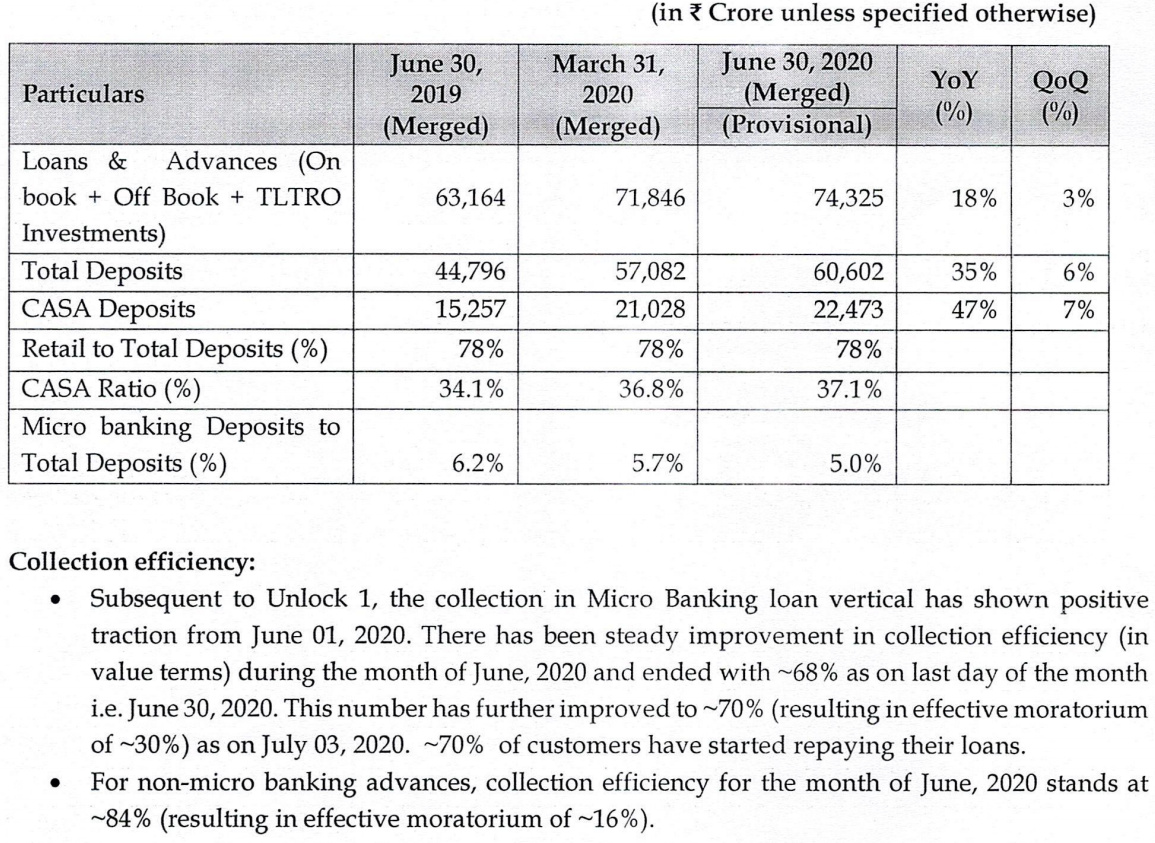

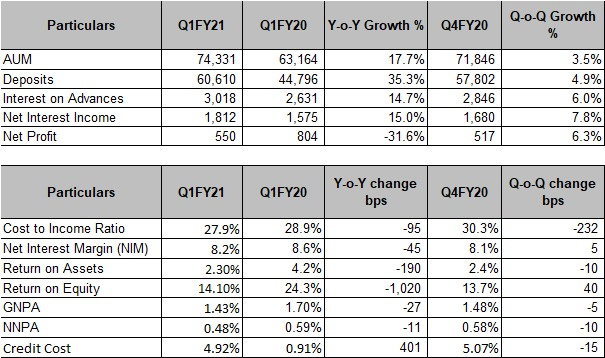

- Advances grew 17.68% YoY and 3.46% QoQ

- Micro credit portfolio comprises 61% of overall portfolio

- Gross NPA at 1.43% vs 1.48% QoQ; Net NPA at 0.48 vs 0.58% QoQ

- Deposit has increased 35.3% YoY and 6.18% QoQ to Rs 60,610 crore

- CASA grew 47.30% YoY; CASA ratio at 37.08% (excluding GRUH deposits 37.83%) vs 34.06% YoY. CA at 4.94% and SA at 32.14%

- Retail Deposit to total deposit at 77.7%

- NIM at for the quarter was 8.15% vs 8.13% QoQ

- Cost to has improved to 27.94% from 28.89% YoY

- Capital Adequacy Ratio remain strong at 27.29%

- Bank is expecting things will be normalized by September this year

- Employee base has increased to 41,563 from 39,750 in last quarter

- Customer base has increased to over 2 crore and borrower base to over 1 crore

- Micro credit portfolio: 70-75% of the portfolio in West Bengal, Assam, Bihar and Tripura

ConCall highlights:

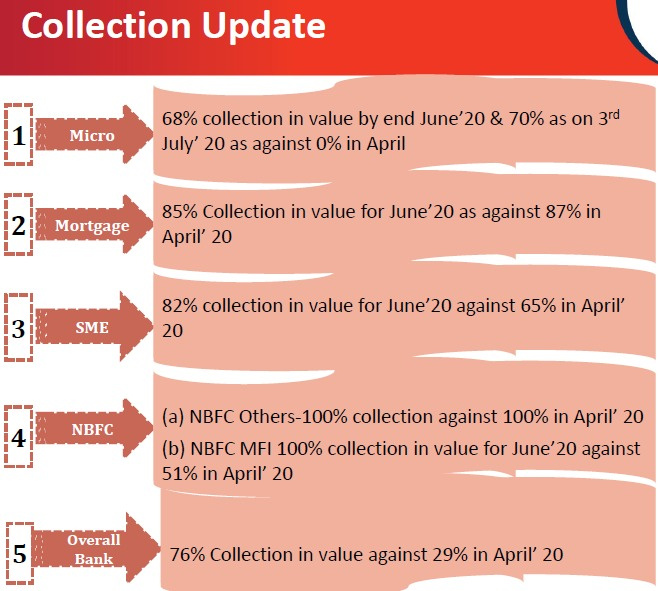

- Collection efficiency in June for micro credit was 68% and for overall banks was 76%; as of now collection efficiency has improved to 73% for micro credit

- Flood in Assam and Bihar and Amphan Cyclone in West Bengal has affected the overall business

- During the quarter the bank has made an additional provision of Rs 750 crore on standard advances; with this provision and additional Standard Assets provision that Bank is carrying in Micro banking portfolio total additional provision in books stands at Rs 1,769 crore. 75% provisions is for micro credit

- 44.4% of borrowers are involved with agriculture and allied activities; 30.3% borrowers are in food processing or having small retail stores

- Close to 30% of borrowers have not paid anything during this moratorium period

- New customer acquisition in the month of June has surpassed pre-Covid level

- Collection efficiency is highest in Andhra, Telangana and Bihar, but Andhra and Telangana is very small part of the portfolio. Collection efficiency in Assam has come down to 61% from 66% due to flood. Maharashtra (54% collection efficiency) and Tamil Nadu has the lowest collection efficiency

- New customer acquisition in micro finance business is around 100,000; 5% of existing customer has received new loan. Average disbursement is below 50,000

- Bandhan currently disbursing gold loan from more than 500 branches

- NPA has increased in loan against property (LAP) book

- PSLC income for the quarter is Rs 119 crore; last year PSLC income was Rs 453 crore

- New customer acquisition would be lower this year; existing customer will drive the growth

- Currently bank is charging 18.75% interest rate, which is 1% higher than earlier on incremental lending to existing borrowers

- Once a customer started paying their installments, 99% of them are regular

- Bank has 58 lacs micro of credit borrowers which is 51% of total borrowers. 16 lacs micro credit borrowers has Rs 100,000-150,000 loan and 40 lacs borrower has Rs 50,000-100,000 loan. 50% banks borrowers have availed loan from Bandhan only

- Disbursement in housing finance is close to 77% of pre-Covid level; during June bank has disbursed Rs 240 crore while in February it disbursed around Rs 300 crore

- Bank will merge the holding company with itself it RBI allows, which will also reduce the promoter holding

- Bihar is one of the best performing state for the bank