Annual report…

Disclosure: Invested in correction at lower levels from cmp.

Annual report…

Disclosure: Invested in correction at lower levels from cmp.

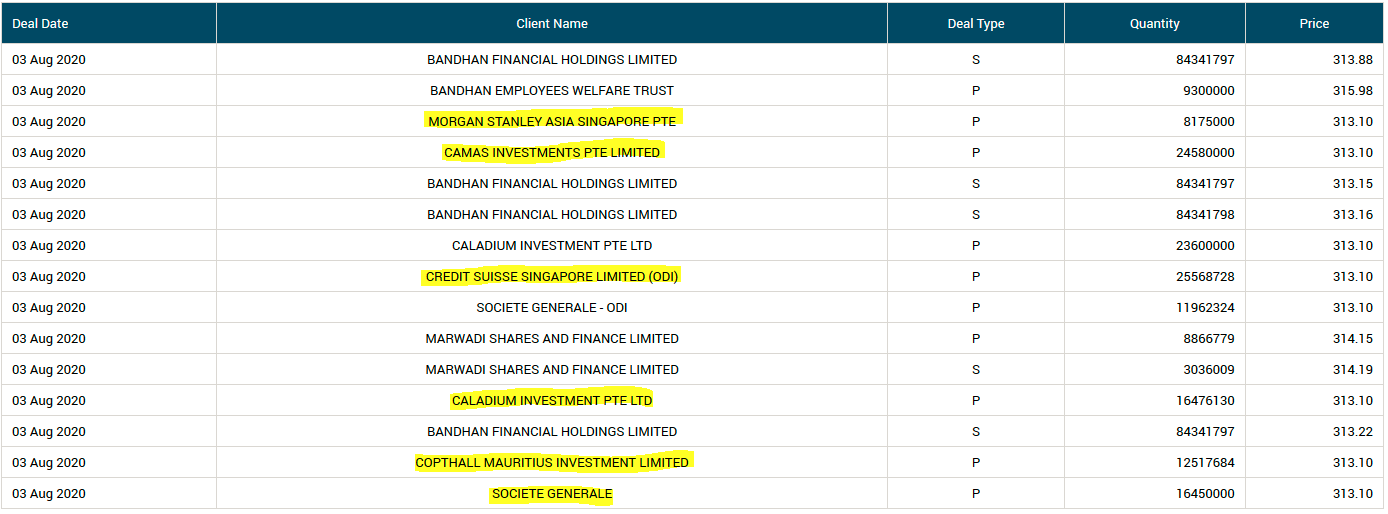

Bandhan bank promoter offloading 20% stake which will help to comply the RBI rule. And OFS is priced at 313 rupees . Interesting to see around 10000cr worth of shares going to exchange hands which is huge quantity. Lot of floating shares created in mkt now. Interesting to see stock price movements going forward.

Q1 FY21 UPDATE

Some things I found interesting -

Consolidation Game

Bandhan Bank is playing on front foot where it is trying to consolidate customers with Bandhan+1/2 loans to exclusive to Bandhan customers. This is a mixed bag and how this plays out needs to be tracked. Being an exclusive banker to small businesses is always a good progression - where banking relationship is an important part of overall business for customer. That Bandhan is thinking of doing it and can do it (largely owing to lower cost of funds being a bank) is also a competitive advantage. But Bandhan has larger ticket sizes than many other players (larger vintage too) and this will further increase the ticket sizes. This increases the risk probably.

Disbursement

I had expected Bandhan Bank to report very poor nos and even losses in Q1 but instead it reported growth in interest income which was surprising. So I wanted to know who are these customers to whom Bandhan is lending. As explained in conf call, the disbursement are to 5% of the existing customers and they fall into new categories. 1) Top up loan to existing good borrowers (consolidation game) 2) Several customers typically close loan in March end and take a fresh one for their business. A lot of these loans could not be disbursed post lockdown and they were disbursed in Q1.

Real NPA Numbers

The real NPA numbers would be known only in Sept quarter or in Dec quarter. The NPA clock got frozen on feb 28. On Sept 1, this clock would be unfrozen + clock will start ticking for all the borrowers who are not paying. e.g. clock would start ticking for 5% customers if collection efficiency is 95% on Sept 1.

Few other things on this front that Bandhan is doing to manage are - increasing interest charged by 1%. They have ~3% provisioning on AUM so far and might be able to increase by 1% each in Q2 and Q3. This along with 1% increase in interest rate and hopefully falling interest rates (rising spreads, MTM gains, trading of portfolios etc.) shall provide another cushion of 1.5-2%.

Mr. Ghosh feels very strongly that collection efficiency will cross 90% by Sept end.

My sense is company might return to reporting normalized profits from Q4 or Q1. These can be delayed further due to Floods or any natural calamities etc. In Q4/Q1, the focus will move from asset quality to growth and how company performs on these fronts. In this context, it is good to see Bandhan growing in gold loan portfolio. This product is now offered in 500 branches compared to 75 branches earlier. Gold loan nicely complements to existing Bandhan portfolio where in it has high RoA and highly liquid asset to back up the loan. How this new product grows would be interesting to see.

Disc - Invested, not a buy/sell recommendation.

Bandhan SHP post block deals forced by RBI regulatory requirements

No of Retail shareholders increased by 59401 (more than 20% from march nos) It translates to 0.34%

FII : Increased 14.28% (more than double of previous holding)

The above are some of the most dangerous traits that I see in a financial. There is no need to be brave and it is much better to shrink your balance sheets rather than go aggressive. In times of crisis where financials are facing liquidity issues most of them will be very happy to let their weaker clients go and if Bandhan is happy to accumulate them good luck to them.

Also it makes sense to have an idea of how much of the loans actually end up in consumption and what is its priority when considered against the basic needs, school fees, housing loan etc. The more an MFI loan ends up as a consumption the more difficulty it will have to recover.

Also it will be helpful if folks who are invested try to talk to people around them who have MFI loans instead of just getting one side of the facts from the management.

Discl.: No holding. My views can change very fast depending on data.

Bandhan is filtering out weaker clients & providing top up loans to GOOD Borrowers

I understand that their collection efficiency reported periodically during covid & till date shows continuous increase

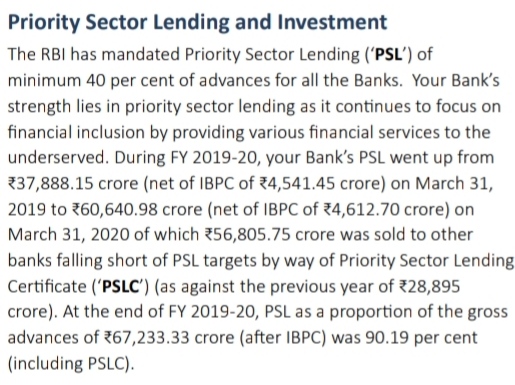

Priority Sector Lending :-

Source : Annual report, page no. 119.

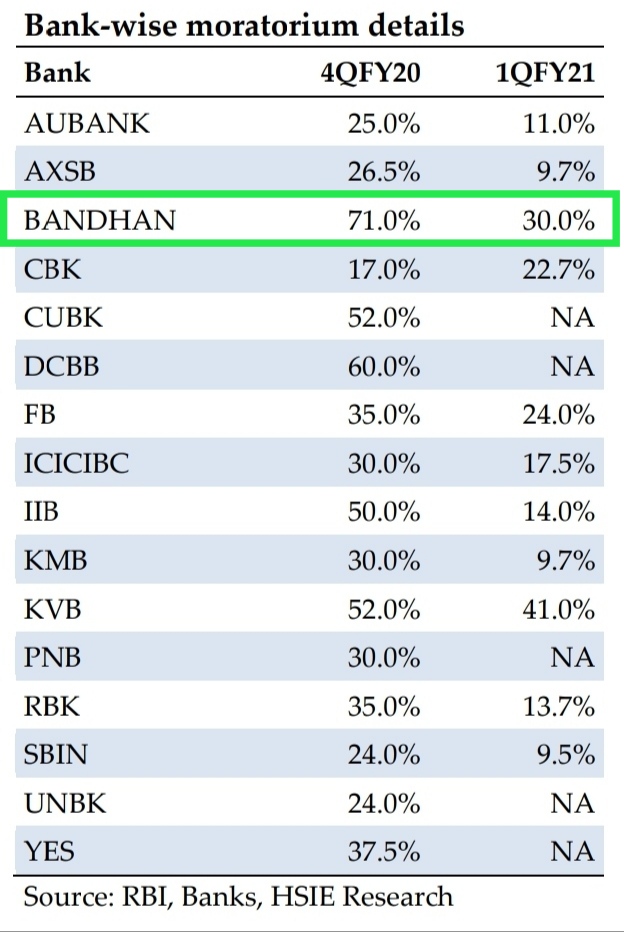

Moratorium details :-

Source : HDFC Securities research report.

“It’s about financial inclusion, its about development, its about serving a poor country, etc. So if you want ownership of banks that are on the forefront of financial inclusion, they need to operate like Bandhan Bank .”

Bandhan Bank Collection efficiency ratio has increased considerably, which shows people are willing to repay loans.

According to Crisil, while the bounce-back has been faster than that envisaged earlier, improving it to the pre-pandemic levels of 98-99% will be an important monitorable from an asset quality perspective.

All the regulatory restrictions imposed by the RBI on the Bank are now withdrawn.

Not allowing me to post more than three consecutive replies,so adding into last post.

The housing finance book is targeted to grow five times to Rs 1 lakh crore in the next five years from the present level of nearly Rs 20,000 crore, chief executive and managing director of Bandhan Bank Chandra Shekhar Ghosh said.

When asked about setbacks like repayments impact due to the anti-CAA protests over the last year, Ghosh said till date, not a single rupee of loan has been written off in Assam and the reverses it faced because of the protests are a part of business.

Going ahead, its parent is also set to launch its insurance and asset management company businesses, Ghosh said, adding that the bank “may” turn to its distribution partners.

Collection efficiency of microfinance securitisation pools fell to 3% in April 2020. Thereon, it recovered to 21% in May 2020, and to 58% in June. It remained significantly lower than 83% recorded in March 2020

Looks like the better of the two scenarios modeled by the paper (40% loss of repayments) seems to be already met in June and things have only improved from there and should only go on improving. It may just be an academic exercise after all. Yes, NCD issues have spiked.

Poor folks have credit ratings to think of and loan-cycle upgrades. Even with moratoriums on offer and obvious difficulties, repayments seem to have reached back to the usual levels. Rural/urban divide may be there in performance though.

Disc: large chunk invested in MFIs

Post:

Bandhanbank renamed its micro-credit vertical as Emerging Entrepreneurs Business (EEB).

The lender expects collections to normalise by December.

Bandhan Bank has roped in ICICI Bank’s former executive Kumar Ashish as the head of its new vertical titled Emerging Entrepreneurs Business (EEB) to focus on small businesses. The bank has named Kumar Ashish as the Executive President and Head of the department, said the lender in its communiqué.

“In addition to microloans, the vertical will also manage the newly-launched product lines – micro home loan, micro bazaar loan and micro enterprise loan,”said Bandhan Bank in its official statement.

Good discussion on Micro finance sector’s covid effect conducted by CARE Ratings (Dated: 19th Aug2020)

Disc: Invested

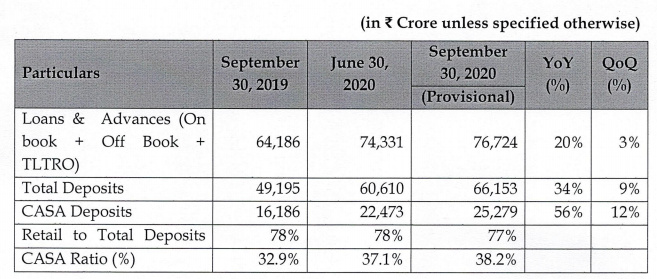

Deposit growth is strong

Dep at +34.5%YOY & +9.2%QOQ

CASA at +56.2%YOY & +12.5%QOQ (part of loan book is always kept as deposits too)

CASA ratio at 38.2% vs 32.9%YOY & vs 37.1%QOQ

Advances at +19.5%YOY & +3.2%QOQ

During the quarter the Bank reduced minimum interest rate on saving bank deposits from 4% p.a. to 3% p.a.

Liquidity coverage ratio (LCR) as on September 30, 2020 at ~157%

Collection efficiency for the month of September 2020 was ~92%. Business wise break up of collection efficiency is as under:

Micro Finance ~89%

Mortgage ~98%

Others (Includes SME & NBFC) ~98%

Overall Bank ~92%

~94% of Micro Finance customers paid in the month of September, 2020.

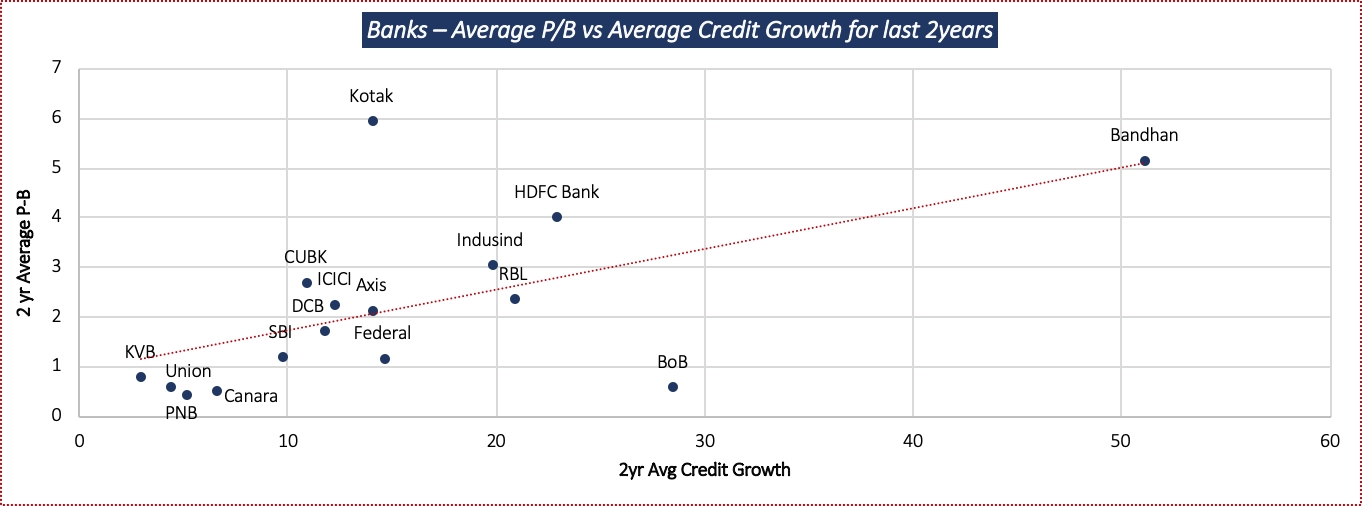

Was working on valuation of the banks and what drives it. One strong correlation is between Credit Growth vs P/B for banks. Market is willing to give much higher value for growth like is case in other sectors. Bandhan Bank is right up there.

If you have the data available, then plotting NIM/RoA against the P/B might be a more interesting plot

I don’t agree with this even if it shows high correlation mathematically. In banking just credit growth is not enough. We can see clear outliers like HDFC Bank and Kotak who have moderate growth and some of the highest PB. In banking credit growth is easy compared to top line growth of other industries, so it does not make sense intuitively as well.

If you have the data, comparison of ROA vs PB will be interesting.