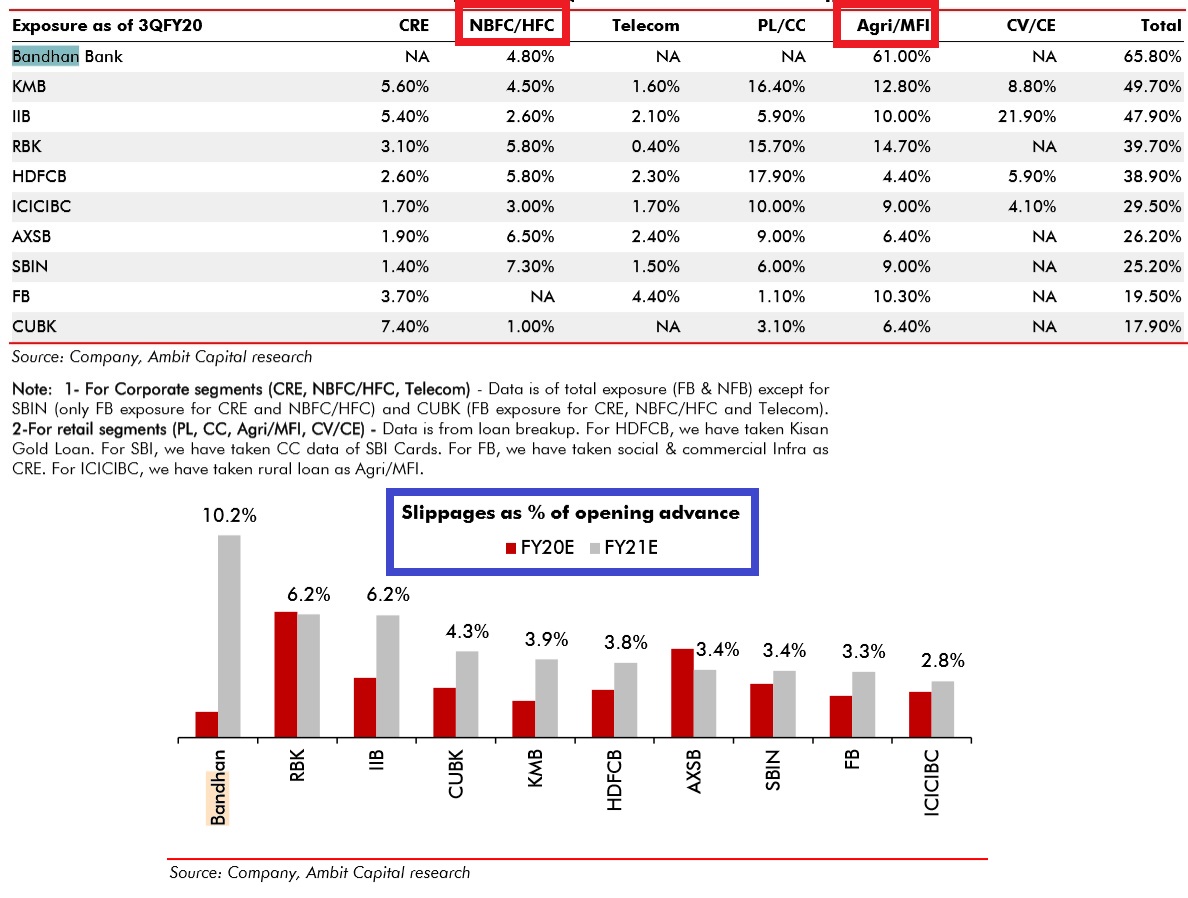

Putting aside Bandhan Bank, one thing is clear…those banks heavily into HFC/Agri and MFi are going to have a tough time for next 2 quarters

The Ambit report is damning but it seems that they don’t understand the industry that well and are overestimating the impact.

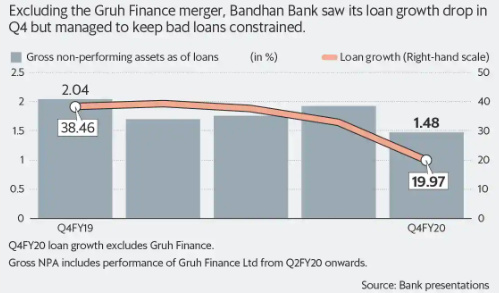

The management has clarified before that upto 3 months the situation is sustainable without a major impact, but yes growth will be impacted, as will be the case of all large banks.

Ambit reference to SKS situation is before the mudra bank and GOI focus on microlending started. Secondly, SKS had internal issues too that brought them down apart from political problems.

Time will tell ultimately. Perse microfinance presents a huge addressable opportunity for a good management. Bandhan has the management and the bandwidth, so this is a test of the management.

8 Likes

This CRISIL report makes a lot more sense

3 Likes

1 Like

As of today, corona rates are lower in Odisha, WB and Assam. Coming days will throw more light.

Health is of paramount importance and will play a major role in post corona recovery, both in terms of speed and the extent of recovery…

The impact to watch will be in Q1 and Q2 FY21. There are two questions to ponder about -

- Impact to the business parameters - loan growth, deposit growth, asset quality.

- Valuation - Based on the current book value (before the possible hit due to NPAs) it is still valued at 2+. Once it commanded 7 times book. With financials going out of favor, will it regain the valuation.

Personally I feel the higher impact on share price will be due to #2. Their customer base is resilient and they will need credit as life will come back to normal. Bandhan has lived through floods, demon - that experience will be handy as they deal with this larger crisis. Business will bounce back in a couple of quarters. But valuation?

I feel that IT, financials and chemicals are business/ life enablers and will never go out of favor…the composition and players may change. Obituaries were written in 2008 for financials, but everyone saw how they led the rally thereafter.

As of now no one can estimate the asset quality and NPA for even large banks. Post corona things will be much clearer. These days axis bank, ICICI, Kotak as well as HDFC Bank hv seen downgrades by brokerages. So time needs to play out.

If the economic scenario worsens, smaller players will run the highest risk of going belly up while as we go higher consolidation will be imminent.

The moratorium has created more confusion and seems to be doing more harm than good and NBFCs are sandwiched.

1 Like

Year-on-year, the bank’s deposits grew 32% to Rs 57073 crore and advances grew 60% to Rs 71,825 crore. Bandhan’s share of current and saving account (CASA) deposit was a at a robust 37%

1 Like

A deep-dive template attempt for Bandhan Bank, trying to bring in the numbers aspects of the business, updated till Q3FY20

Bandhan Bank_20200502 1900.docx (677.4 KB)

14 Likes

Bandhan Bank has under performed year-to-date (-52 per cent versus Nifty -24 per cent) which has made the valuations for this “specialist” microfinance and mortgage player attractive.

Markets are increasingly concerned about a sharp increase in credit costs for the micro finance segment in F21 given loss in income, high leverage in East India and aggressive lending in the industry. Against this, Bandhan Bank has exceptional track record in the MFI business: it has incurred minimal credit losses through successive industry crises over the last 10 years.

Even through the recent stress period in Assam (September-Deccember 2019), the bank had largely normalised its collections by March- 20. Sector-leading operating profit margins are an added offset. The bank went into this lockdown with strong collection efficiency (98.7 per cent), high capital (CET1 23.1 per cent, Assets/Equity 5.8x) and strong liquidity (LCR 161 per cent). As lockdown gradually lifts and collections start normalising over the next six months, I trust the business can rebound quickly.

3 Likes

Detailed result

2 Likes

There are a lot of questions around the MFI space and Bandhan in particular. This tweet explains the reality. Is the coming time going to be so bad for Bandhan? Insightful thread!

3 Likes

While it’s a good read and the first slide is similar to what Mr Ghosh spoke on a channel recently,the writer should provide his details and data source to bring in transparency in communication.

3 Likes

About 40% of Bandhan Bank’s business seemed to be from West Bengal.

Covid impact + Level 5 Cyclone could be challenging, especially for the Micro Finance business

Yes I agree

kolkata is expected to be worst hit

And if that happens

It will take another 15-20 days to come back to normal

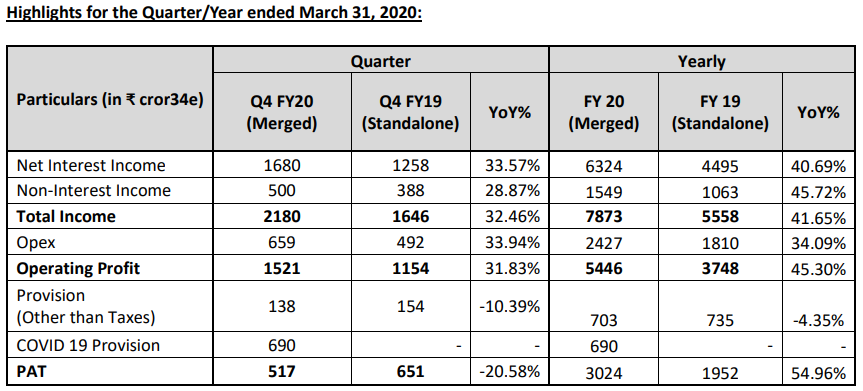

Bandhan bank Q420. Rough notes…

Red zones : 5%; 78% green zones businesses not in lockdown; 16% orange ; 76% of our portfolio is in green and amber ; even in green zones we cannot collect ; 85% of our customers businesses are not affected by Covid

43% in green business; 33% in amber zone; 23% in red zone of our portfolio…pan india

IN GREEN zones we have not been able to start collections; LOCKDOWN IMPACT WILL COME NEXT QUARTER

_ customer is ready to come and pay…and our ppl also cannot collect. Collections not happening right now

CASA : CA is 30%…SA is 6% : 36% CASA ratio (March – May 1.5-2% deposit growth)

IN past experience in bad business cycle loss ratio is 0.5-1% …when credit culture desire not to pay losses went to 3-4%

- earthquake…Surat & Vapi….post earthquake…they moved out…took a while to service their loan…no problem…of salaried ppl on their obligations unless something happens to whole group

- this time will be a new experience for us…salaried ppl also effected or not ?

75% of borrowers have…balances with us…4 weeks of installments…in our savings banks…3000 rupees. they are not withdrawing and we are not adjusting from their accounts

Unique to Bandhan : 50% customers…Bandhan and another lender is 80% of customers/loans

Assam 690 cr provisions……in Q4…covid provision ; 2700 cr loans could be stressed

net NPL is 0.5%

customer mandate is direct payment from their bank account to our account.

87% of April installments was paid in our account.

Affordable housing segment is resilient : 40% formal workers loan portfolio ; 45% informal

9.5 lacs.avg loan. 14-15 lacs property value ; 85% customers have incomes less than 50 k rs. 15% below 35k rs.

96% of our offices are open

collections idea what ppl will be comfortable with : instead of 25 group make it 7 members. 1 hour meeting…make it 20 min…; come to our brand, or pay by UPI… or go and pay and we will pick up

we haven’t started collection

Loan book hasn’t grown this year ?. avg loan size is same

Assam 93% collections ; total portfolio 98% collections

Last decile of customers,creates all NPL issues

borrowers are women……payment info not disclosed to men.

experimentation of 3.5 lac portfolio : 30% of existing customers can migrate from 1.5 lac to 3.5 lac…not in 1 year…over time…this will also be unsecured

even if 10% of our customers go to 5 lacs…huge no

ASSSAM portfolio : 690 provsiions. taken 200 cr last qtr for Assam provision. 3% NPA in Assam. we have written off 200 cr

Borrowers are risk takers….their business …is not so demand elastic…their alternative is money lenders. so formalization….and livilhood basic business…demand supply doest change much…for demand of our customer business

90% of borrowers are repeat borrowners….these custommers 5-6 years with us…; 10% new customers…will slow down…we will slow down for 6-9 months…till we get to know the customer

growth : will focus more on existing branches than growing new branches

New loans…higher limits : for customers who have never defaulted ever. will give loan when business has restarted

98% of customers have paid full installments

18500 affordable housing : LAP : 9% ; developer porffolio : 4%…rest housing

no need to add collection ppl. borrowers are mature. borrowers can collect and come to office

group lending : joint liability…moral responsibility to collect from others…but not compulsorily.

8 Likes

Impact of Amphan on Bandhan.

As per bank’s estimate, the business of around 65,000 of our micro banking borrowers,

amounting to an exposure of approximately Rs.260 crore, could be impacted due to the

cyclone.

The major impact has been in the district of South 24 Parganas.

Referring prior experience of Fani, the cyclone that caused large scale damage in Odisha in May 2019, the impacted portfolio took 3 to 6 months to achieve normalcy, aided by the

committed workforce and customer loyalty. On the back of this experience, bank expects the

Amphan affected portfolio to regularise by Q3 of FY21.

3 Likes