today you can not see Gruh shares in your demat account,any idea when those will be transferred and reflected as “Bandhan Bank” shares (1000 Gruh shares for each 568 Bandhan shares ratio)?

No communications that i have seen from Gruh in this regards. Since Oct 17 is the record date, so the process should start from 18th Oct. I guess by next week , the Bandhan shares should be visible.

Targetting The Hardcore Poor.pdf (1.6 MB)

A research paper from the Nobel Laureate about Bandhan

Quick action show nice ground work… hope we see similar expansion for Bandhan branches as well

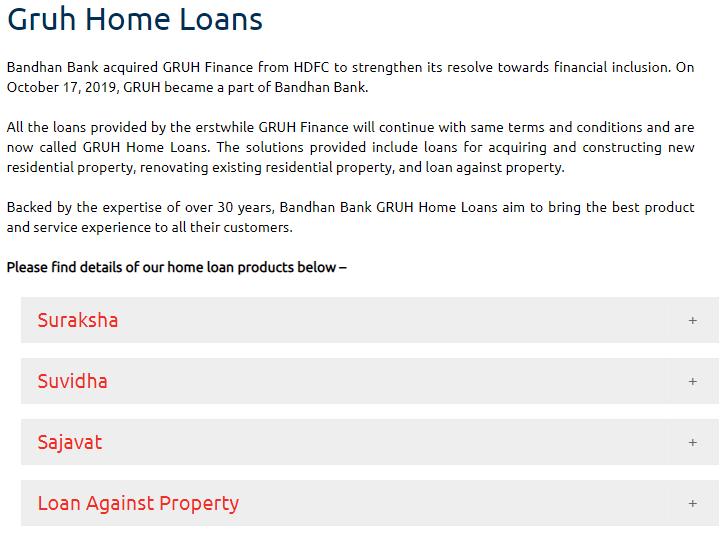

I heard in some interview that management had indicated Bandhan offices will offer Gruh services & vice versa… let us see how it pans out…

An interesting point related to Mutual Fund Managers

Everyone was aware of amalgamation & 1000:568 ratio . Gruh always traded 5-12% cheaper after announcement of amalgamation scheme. If we observe the Mutual fund holdings… They continued buying Gruh and selling Bandhan. I thought that its retailers only who look into these small gains but above data confirms that Mutual Fund managers also exploited this.

anyone having idea by when bandhan shares will be credited for those who held gruh share

For Indusind + Bharat Fin it took around 10 days for shares to be credited, but it can take up to 30 days

many reports coming from Macquarie Ambit Sharekhan on overheating of MFI sector specially in Bengal while Bernstein report disputed it .

Whats your n other VPers view on this overheating and how it cud impact Bandhan and other MFIS in diff region of India?

Tomorrow is the result, lets see the numbers. Could you please share the reports you are referring, I am not aware of any such reports. Healthy criticism is always welcome.

We heard such issues almost a decade back & again in early 2017. Are you referring to same old reports or you have access to something, which can be shared with VP community (if its not restricted circulation)

If I read it correctly these reports are on valuation NOT on above issue raised in earlier post

Gruh always traded at premium & I take these valuation concerns lightly as it was proven business for quite long with best performing parents.

Yes, all are Gruh merger valuation related concerns. No issues with Bandhan bank business operation.

I am about to finish the book: “Bandhan-making of a Bank” by Tamal Bandyopadhyay.

Indeed, the kind of stellar rise of this franchise is one of its kind. There are very rare business which start from grassroots and rise so much( Reliance industries, Paytm,Flipkart being others that I can think of). In a highly sensitive and difficult market like East, they have done wonders.

But one thing I want to mention and seek opinion of the fellow boarders. The culture initially at Bandhan was micro-management where Mr Ghosh used to track when is someone arriving to office and when is he going ( at one point, its mentioned that everyone would have to say bye to him before leaving for the day, so as to let him know that he was working till late).I hope with much bigger things to manage, Mr Ghosh is a changed man now. Discipline is good but micro-management irritates the employees and impacts performance ( to some extent, Aditya Puri also has similar style, he still ran the show for more than 20 yrs ![]() )

)

With Gruh being in the kitty carrying a different culture and being supervised by Bandhan now( no matter how much they say it will work independently, the management control will change), I wish the 2 entities work with synergies and give space to each other.The history says mergers have been mixed bag, mostly unsatisfying.

Disclosure: Both of them are a good % of my portfolio.

WB has the highest loan outstanding per borrower. The thing in microfinance is that it is absolutely wrong to generalize any given data. Last detailed research I saw on overheating in the sector was done by dvara trust. They went into district level data and targeted districts with highest number of microfinance providers activity, highest loan book growth relative to borrower growth. There is so much granularity in India and this sector that is difficult to form any thesis with any certainty.

There are bounds to be areas, sub-districts, districts which will be over-leveraged. Even in district level data, % of borrowers over leveraged is what matters. Generally, it is business as usual as long as the borrower does not befall any tough times. The closest analogy is the NBFC sector, for a long time everything is good and suddenly when liquidity dries up or few business bets turn sour due to slowdown in economy or some calamity the loan/asset becomes distressed.

One can go through my post in Ujjivan’s thread to learn more about the sector. I have posted a few sources for secondary research. As much as I have studies the sector, my reading is it is really tough to determine with certainty when bad times in any form will befall. Best to invest in this sector with a basket approach and try to determine and stay with conservative lenders.