Concerns over the near-term impact of its merger with Gruh Finance and the pending promoter stake dilution among others, has weighed on investor sentiment for Bandhan Bank, which had a great listing in March last year. With a fall of over 16 per cent in its share price in the last three months, Bandhan Bank has also underperformed the Nifty Bank index that fell by 9 per cent during the same period. The correction, however, has led to a sharp fall in the valuation of the bank’s stock. It currently trades at 3.6 times FY21 estimated book value, which is an 18 per cent discount to its average one-year forward valuation since listing and a sharp 42 per cent discount to its peak valuation.

Though the Gruh Finance merger, which is expected to be completed over the next two quarters, would impact earnings growth to some extent, Bandhan’s long-term return profile remains intact.

Emkay Research’s recent note says, “We like Bandhan Bank due to its remarkable liability ramp-up among SFBs (small finance banks), asset diversification strategy away from MFI (microfinance institutions) and a sustainably higher return on asset (RoA)/return on equity (RoE) business model.”

Even over the next two years, Bandhan’s calculated RoA would remain almost at FY19 levels of 3.9 times levels as compared to below 2 times in case of other small banks, say analysts.

Besides a likely strong loan book growth, healthy liability franchise and lowering operating expenditure improves Bandhan’s return ratio outlook. Given the pricing power, mainly in the micro finance business, maintaining deposit base going ahead, is unlikely to be tough. Even in June 2019 quarter, Bandhan’s deposit base grew by 42 per cent year-on-year versus low double-digit growth for the entire banking sector.

Higher deposit base would also help curtail margin pressure expected from the lowering of its high-margin microfinance book. The latter’s share in overall loan book is expected to decline to around 50 per cent over the medium term from 86 per cent at present.

Overall, long-term investors could bottom fish on corrections. The lowering of promoter stake, however, would be key to watch.

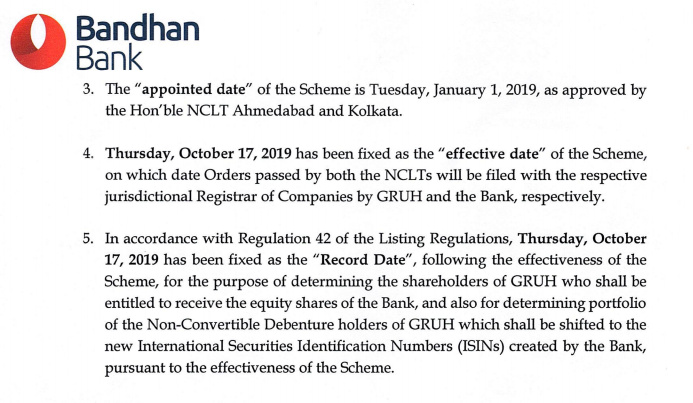

Read our full coverage on Gruh Finance Bandh