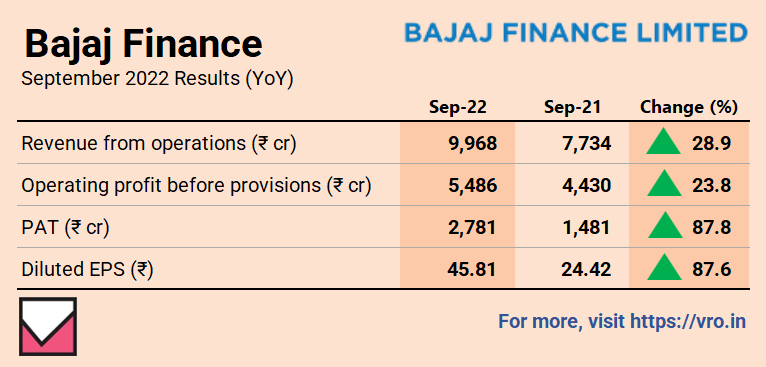

Bajaj Finance Q2FY23 performance has reaffirmed that the already big, strong Bajaj Finance has turned even mightier after the pandemic. Over the past 15 years, it has grown its loan book at a compounded annual growth rate (CAGR) of 37% and profit at a CAGR of 51%, with an average ROE of 17%. The lender showed improvement across loan growth, profitability and asset quality. Robust growth in assets, better asset quality and fall in provisions/credit costs underlined performance even as operating expenses increased during the quarter. Through digital transformation, Bajaj finance intends to not only double its existing customer base but also mine the wallet share of its existing customers in a cost-effective manner. Asset quality trended better, with NPAs reducing further.

Parth as you have mentioned, Bajaj Finance scored high marks in its Q2, 2023 results. Even its its gross NPA and net NPA as of September-end stood at 0.24% and 0.11% respectively, against 0.39% and 0.24% in the year-ago period.

Also, Bajaj Finance’s loan losses and provisions for Q2 stood at Rs 734 crore against Rs 1,300 crore.

I am not going more into its details as you all are familiar with the results. What I want to juxtapose it is with the share’s performance post the results.

This is disheartening for a novice investor like me. To my thinking I invested in it based on its past performance. Obviously, the market also expected it to keep up.

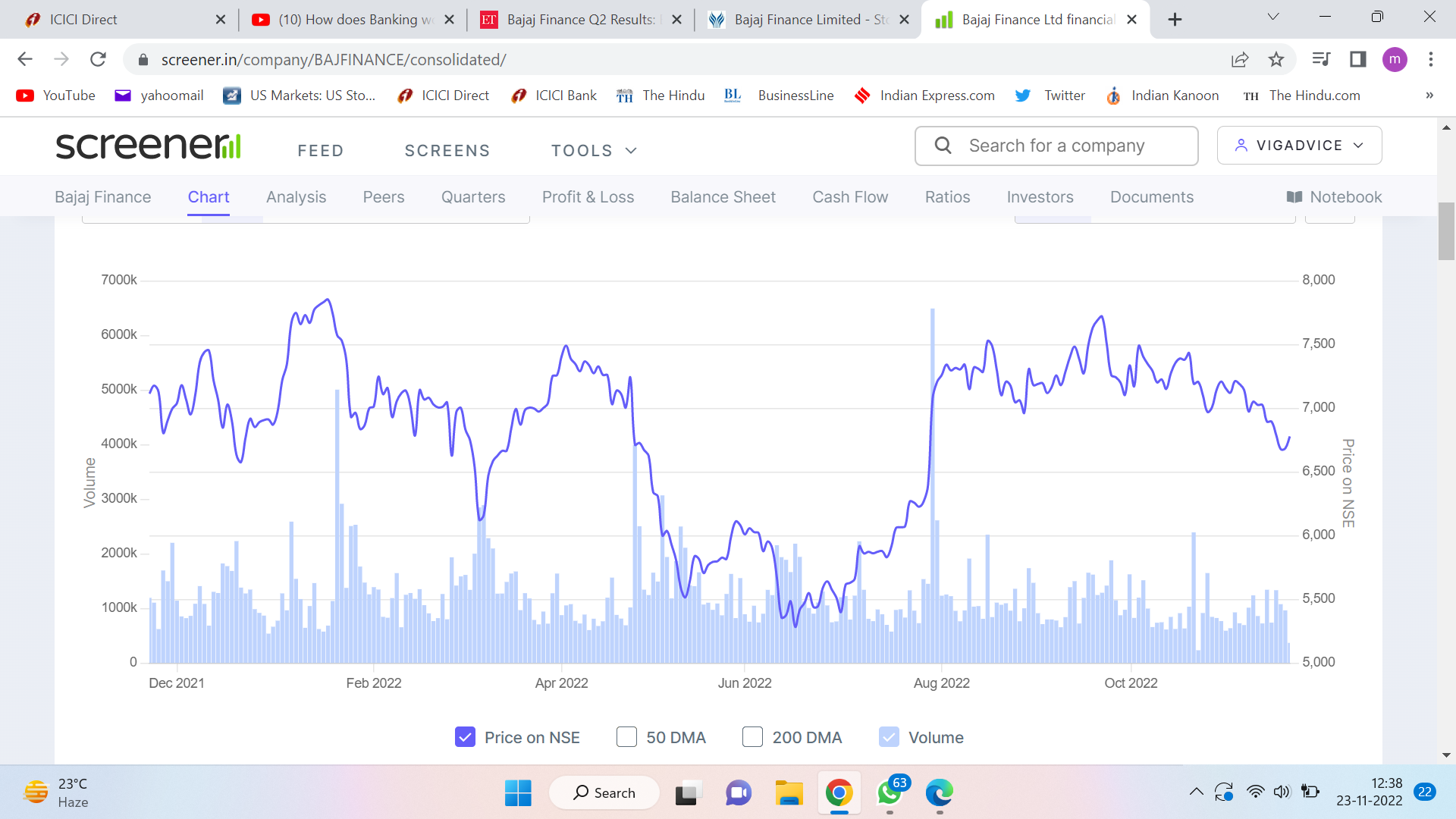

While one understands initial profit taking by some traders who invest in anticipation of good results and trade in their shares for ready money, its continuous fall, as the screenshot from screener would show, its continuous fall from September is unnerving. Let me put it more simply- if people made investment in it before the results in anticipation of good performance, to my eyes nothing has gone wrong during these months.

Sometimes there are fears that the market knows something we do not. My question to the community is- how do we, the long term investors, deal with such situations?

This is why markets are called the great humiliator. Markets are by nature random and past performance are no way guarantee of what may unfold in future. Keep your horizon for well managed companies with good runaway for growth for atleast 2-4 years. Also such cases will help you appreciate the term “margin of safety” or reverse dcf. asset allocation and diversifying also helps as there will always be some laggards and some super movers. Keep investing by tracking the business and industry outlook. Patience is generally rewarded.

Best

Divyansh

Valuations. In the past, BF was growing at 30-35% and others were growing at 12-15%, so valuation gap made sense. In last few years, BF has slowed down while competition is growing faster. When the growth delta is not so high, valuations catch up (either price or time correction).

Today, Bajaj finance is growing at 25% and is valued at 8x book value, ICICI is growing at 20-25% valued at 3x. Valuation Gap is huge. Most banks are today available at less than half the value of Bajaj finance with similar growing potential in mid term. In such a scenario, these valuations will keep the share price suppressed.

Reliance’s entry in Financial services is another recent headwind and still to show in the share price.

Disclosure: was invested, recently sold off after Q3 results and moved to other players in BFSI space. Hence, Biased.

sir… if BF business continues to outperform then price will catch up over time… it’s richly valued so you can’t expect price to always go up… it will undergo some time correction… you are saying that you are a long-term investor but you are worrying about last 3 months performance? just focus on results and valuation…

As I said above, for a similar risk profile, private banks and some second rung nbfcs provide better value. In a credit growth cycle, all boats will be lifted, but the ones available at cheaper valuation will get a higher lift.

It is a bit strange that BAF did not participate in the current bull run in NIFTY 50 stocks despite results being stellar and no threat whatsoever from any slowdown. It seems some major FII’s are exiting or exited towards other sectors/scrips which we will come to know in weeks to come. If the Co continues to deliver, no reason to believe it will not bounce back. However in the last 11/12 years every year it has given positive return with 2022 being an exception. As retail investors-do we have any other choice but to wait?

Any specific reason for sharp fall today? Stock down 6%. Are the numbers reported yesterday are not good.

Promoters bought 200 crores rupees worth of shares around 6500 few days back. Still market is hammering the stock. Is it just normal correction or something else.

Brokerage houses saying that growth is slowing down and numbers are below expectations. Bajaj fin use to grow at 35% and now expected to grow at 25% (acc to some brokerages/experts) , hence the stock correction due to high valuations.

However promoters buying 200 crores of shares at 6500/- , just 2-3 days before reporting numbers makes me confuse. Should we assume that promoters are good in business but not in calculating correct valuations or they are optimistic about the business and thinks that such valuations will sustain and growth will be similar like past. People tracking this company please share your views.

It is valuation correction vs builtin expectations. They will grow at 25-27% vs 35%+ earlier with no competition whatsoever. Now with banks growing @ 20-25% there is competition hence valuation compression. End of the day, FII’s drive and compress valuation. Guess in 6-8 months it should find the right valuation levels.

Seen this movie many times in the past. Narratives come up to match stock price action. News items, brokerage reports etc get all aligned very quickly…Investor need to learn to filter out such noise. Price is a function of demand supply and hardly any no one knows why any stock is going up or down in short term…

Bajaj Finance has created a limitation on its growth by sheer size that it has grown too. You can ask people and now even tier 4/5 folks are getting calls from Bajaj Finance for loans. If they had slowed while over all environment became much slower then market would not bother about it but it is not the case. Others are growing aggressively while it is slowing. Significant correction which will be painful is ahead which often happens with stocks once they lose the fancy of leader of bull run. Happened to many names in the past like Laurus Lab/Divis Lab/Jubilant Food/even Asian Paints etc and ridiculed names such as ITC can also start to do well after years of beating and underperformance if market starts to like them. If anyone is expecting the stock performance as good as last 5-8 years in Bajaj Finance then it is unlikely. Law of the large numbers catches up and stocks which were multibagger becomes compounder then become slow grower safe houses like ITC. That is natural.

So, another lesson here is that if you are content with fixed+ stay with them, otherwise letting go of a Bajaj Finance or HDFC Bank may not be such a heresy.

Like the animal kingdom, a time may come for the patriarch to relinquish the throne. And a younger animal takes over. Recognising that younger one with promise is the dream of all long-term/fundamentals investors.

Which younger one’s do you have in mind that according to you could take over the throne from Bajaj Finance?

The throne that you are talking about is really a grand one, and to find a suitable replacement for it (replacing the mighty Bajaj Finance) would really be something. The performance Bajaj Finance has shown all these years is really difficult to replicate and according to me even though the company can show some degrowth in the near future (which would be temporary) but it will still show leading industry growth.