Question here is about valuation, BF has shown retardation in growth which will compress its P/B and PE ratios both even it is growing to adjust long term valuations. Lot of small fintech companies have filled the gap with tying up to NBFC and banks hence no clear major winner here, everyone eating cake. Niche of BF has been demolished now its a normal NBFC.

1 Like

Jefferies Upgrade Bajaj Finance from Hold to Buy with TP of 7,280 +24%.

The main thesis:

-

Although AUM has softened it is likely to remain above 25%

-

BAF is planning to get into newer markets like CV financing, car loans, microlending. In addition, opening up of the credit card business can account for 5-10% of profits in the next 2-3 yrs.

-

AUM is expected to double from 2trn to 4trn in the next 3 yrs as per management.

-

As rate cycle peaks, pressure on NIMs are likely to reduce.

-

Two catalysts: peaking of interest rate cycle and RBI allowing its credit card foray.

-

Risks: Increased competition from newer players like Jio Finance.

13 Likes

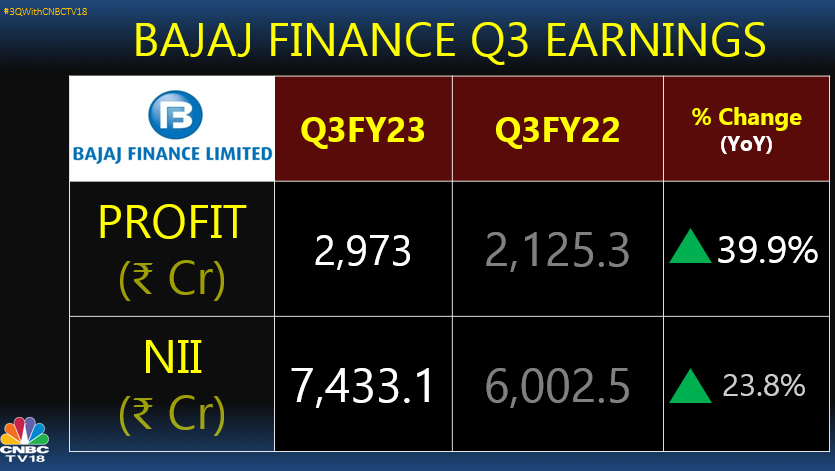

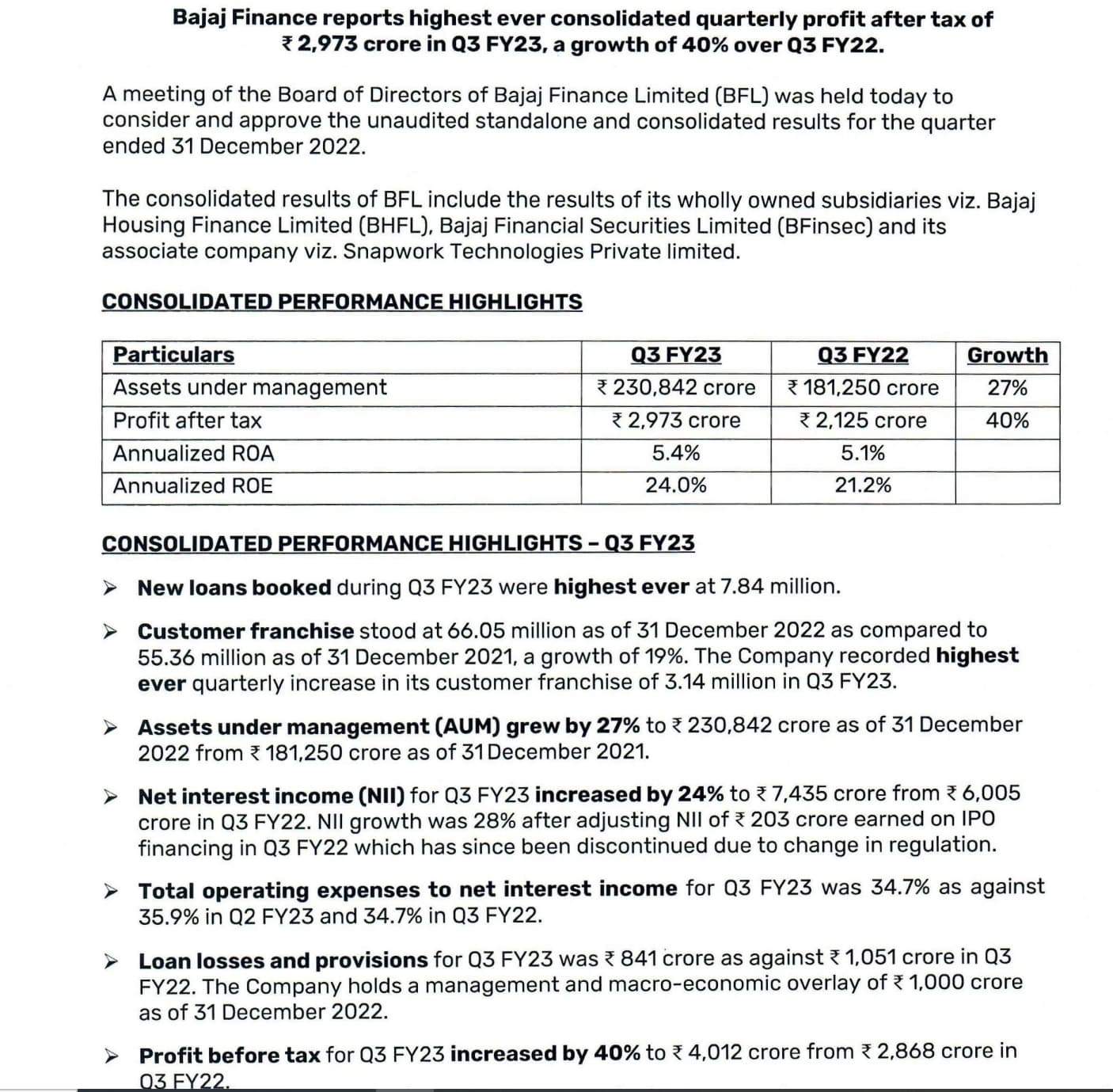

3QFY22-23 Results

Presentation

Conference Call

Call Transcript

https://cms-assets.bajajfinserv.in/is/content/bajajfinance/b3-2023pdf?scl=1&fmt=pdf

Financials

https://www.bseindia.com/xml-data/corpfiling/AttachLive/7100fbaf-306f-49b8-947b-bf221eb37f29.pdf

1 Like

Results announced. PAT up by 30% , Dividend of 30 Rs.

V detailed presentation. People who understand this business and track this company please share your views on recent results. Prima facie results looks good to me but I am not an expert in understanding financials.

dc2c9ce5-f0cd-44d5-8d93-da71e8350bd2.pdf (bseindia.com)

Disclosure: Invested since 2015.

1 Like

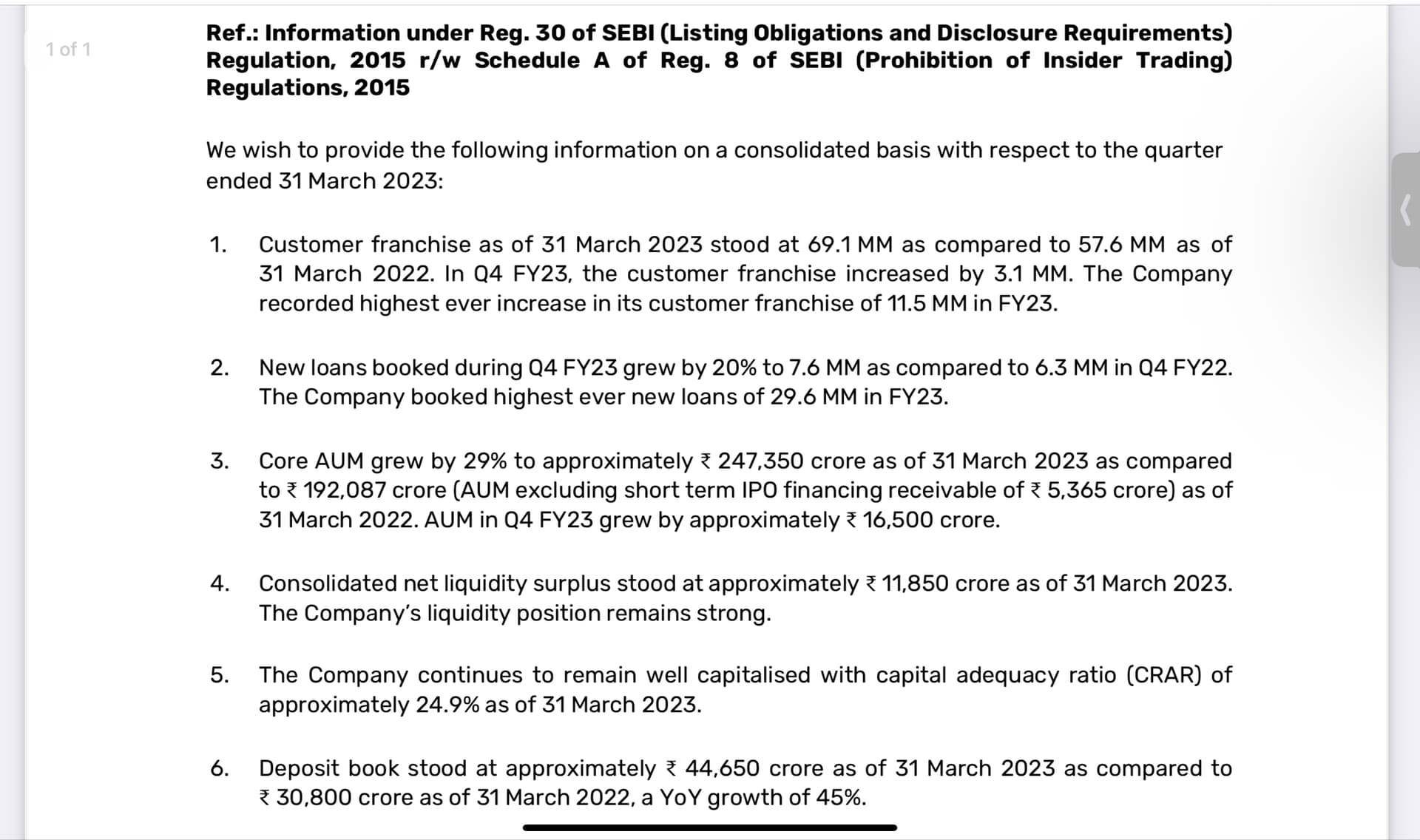

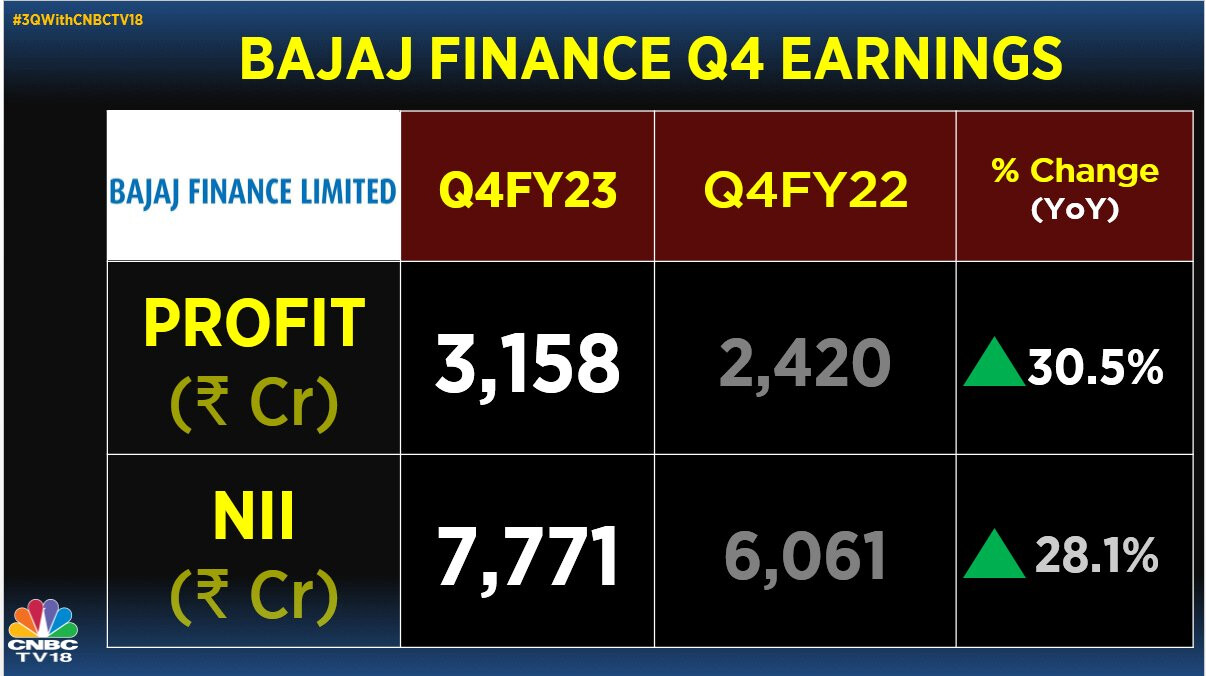

Q4FY22-23 RESULTS

CONFERENCE CALL

TRANSCRIPT

PRESENTATION

FINANCIALS

https://www.bseindia.com/xml-data/corpfiling/AttachLive/0aa8cd4e-6b9c-400f-b6dd-379d7563fa1a.pdf

Q1FY23-24 RESULTS

Concall

Concall Transcript

https://cms-assets.bajajfinserv.in/is/content/bajajfinance/transcript-q1pdf?scl=1&fmt=pdf

Presentation

Financials

https://www.bseindia.com/xml-data/corpfiling/AttachLive/9f04d98f-d7f7-448b-9f91-fe57f3008c08.pdf

5 Likes

Result summary

-

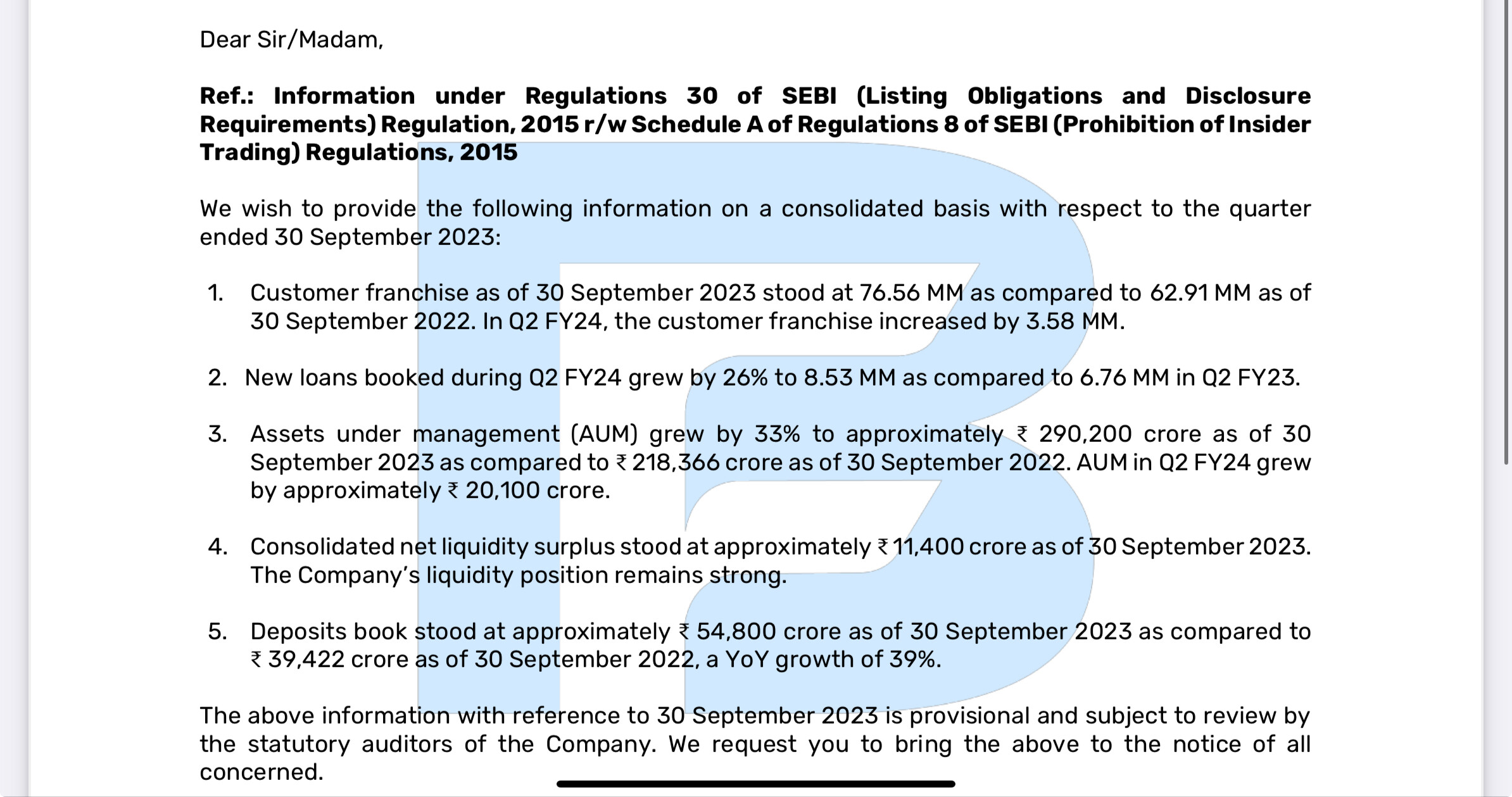

The company aims to add more than 12-13 million new customers in FY24, and in the current quarter, they added 3.84 million new customers.

-

Core AUM increased by 32% to 270097 Crore as of 30 June 2023, compared to 204018 Crore as of 30 June 2022.

-

The company achieved the lowest ever GNPA of 0.87% and NNPA of 0.31% as of 30 June 2023, compared to 1.25% and 0.51% as of 30 June 2022.

-

Deposits book witnessed a YoY growth of 46% and stood at 49944 Crore as of 30 June 2023. Net deposit growth in Q1 was 5278 Crore. Deposits accounted for 21% of consolidated borrowings as of 30 June 2023, and deposits as a percentage of Total Borrowings were also at 21%.

-

NIM declined by 11 bps in Q1FY24 and is expected to decline by 10-15 bps in the next two quarters each.

-

The AUM growth guidance is maintained at 25-27%, while the PAT growth guidance remains at 23-24%.

-

The management has observed strong momentum at the beginning of this year and has increased the AUM growth guidance to 29-31% for FY24. They also expect operating leverage benefits in the upcoming quarters as the ‘Opex to NIM’ has peaked.

-

The tech industry witnessed a significant feat with 1.5 crore downloads per quarter, driven by organic means.

-

Except for Rural B2C, AUM growth remains strong across various segments. The management introduced a new segment, ‘new car financing,’ alongside its existing vertical of used-car financing, with plans to expand to 80 cities.

-

Despite increased competitive intensity in some segments like ‘personal loan,’ the management believes the industry’s growth is sufficient to accommodate their own growth. Additionally, they do not intend to increase the proportion of Developer Finance composition to more than 15% of the book for the Housing Finance business.

-

Attrition rates at junior levels have decreased from 28% to 13.5% due to steps taken by the management, while senior or middle-level hires experience minimal attrition.

11 Likes

-

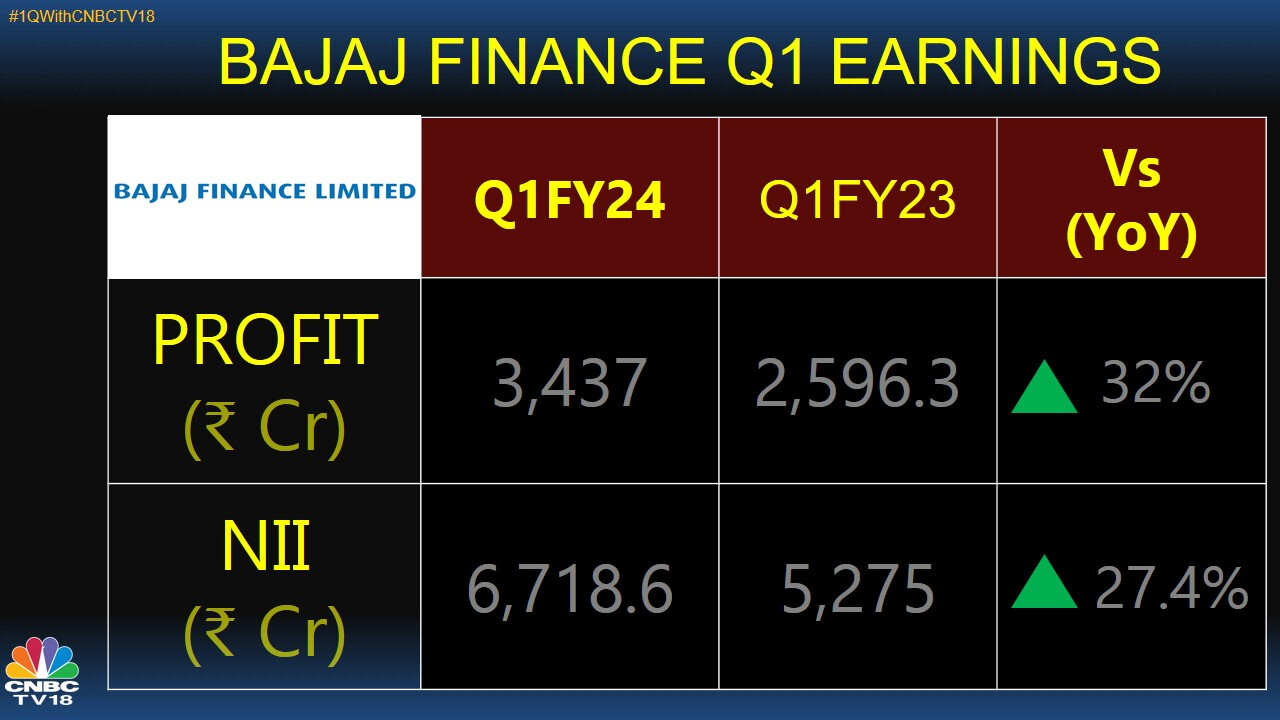

Q1FY24 Net Interest Income (NII) increased 26.5% YoY to Rs. 8,395cr.

Q1FY24 Net Interest Income (NII) increased 26.5% YoY to Rs. 8,395cr. -

Profit After Tax (PAT) rose by 32.4% YoY to Rs. 3,437cr, aided by better operating leverage.

Profit After Tax (PAT) rose by 32.4% YoY to Rs. 3,437cr, aided by better operating leverage. -

Highest-ever quarterly AUM growth of Rs. 22,718cr.

-

Engaged in lending across retail, SME, and commercial customers, also accepts public and corporate deposits.

Engaged in lending across retail, SME, and commercial customers, also accepts public and corporate deposits. -

Asset quality strong, with GNPA/NNPA ratios at 0.87%/0.31%.

Asset quality strong, with GNPA/NNPA ratios at 0.87%/0.31%. -

Market leadership, strong distribution reach, customer additions, digital transformation, and robust AUM growth bode well for future performance.

Market leadership, strong distribution reach, customer additions, digital transformation, and robust AUM growth bode well for future performance. -

NIM levels may moderate in upcoming quarters due to rising cost of funds, but long-term growth prospects are promising.

NIM levels may moderate in upcoming quarters due to rising cost of funds, but long-term growth prospects are promising. -

Reiterated BUY rating on the stock with a revised target price of Rs. 8,252 based on 6.1x FY25E BVPS.

2 Likes

-

Bajaj Finance successfully weathered crises like taper tantrum, demonetization, IL&FS turbulence, and COVID-19 better than Indian rivals.

Bajaj Finance successfully weathered crises like taper tantrum, demonetization, IL&FS turbulence, and COVID-19 better than Indian rivals. -

Exceptional asset quality except during the global financial crisis (GFC).

Exceptional asset quality except during the global financial crisis (GFC). -

BAF gained market share post-GFC by focusing on retail loans like consumer durable, unsecured, and home loans.

-

Bajaj Finance aims to expand into microfinance, new car and tractor financing, and gold loans while maintaining a balance in unsecured loans (42-44% of AUM).

-

Nomura projects a 27% AUM CAGR over FY23-26F, 10% net interest margin, 1.6% average credit cost, resulting in 25% EPS CAGR, 4.5% RoA, and 24% RoE.

-

A key risk is potential conversion into a bank due to size limitations, impacting RoA/RoE and leadership tenure.

A key risk is potential conversion into a bank due to size limitations, impacting RoA/RoE and leadership tenure.

3 Likes

Bajaj finance board approved fundraising of total 10000 cr.

Bajaj finance ROE is about 25% (ROA of 5% multiplied by leverage ratio of 5 times) Which means they can keep growing at 25% without raising funds. Banks or NBFCs needs to raise funds when they want to grow at higher rate than thier ROE. Mr market is now excited because market now believes that Bajaj finance management has the visibility to grow higher than thier last given guidance of 24-26% which they gave in the last conference call.

When balance sheet attains a particular size there is a risk of slow down in growth. Street was fearful after witnessing recent valuation crush played out in HDFC bank, though there are multiple reasons for that. It looks like Bajaj finance is still some time away from slow down due to large size if that time ever has to come.

The timing of there capital raise is always exemplary. Last they raise the capital was back in 2019 before the Covid at 10 times price to book. That raise enable them to sail through entire covid cycle without any fresh raise of capital when valuations in terms of PB multiples were below there historic levels. And now again they found a period of good valuation for fresh raise of capital.

Disclosure: invested

8 Likes

The other and more likely interpretation can be that the management may be expecting ROE to drop from 25% and hence may need to raise funds to sustain growth.

Disc : Not invested.

2 Likes

2nd Quarterly Result FY 2023-24

Presentation

Financial

https://www.bseindia.com/xml-data/corpfiling/AttachLive/30fb5fe1-8f30-4723-a0b9-22aa0a1b930e.pdf

5 Likes

the Company has entered into a binding term sheet with Pennant Technologies Private Limited (‘Pennant’) on 16 October 2023, at or about 8:40 p.m., for acquisition up to 26% equity stake in Pennant.

The object of the strategic investment is to strengthen Company’s technology roadmap.

This is significant for the long term strength of the company. Jio Finance in it’s presentation has clearly shown it’s focus on Tech to grow business.

2 Likes

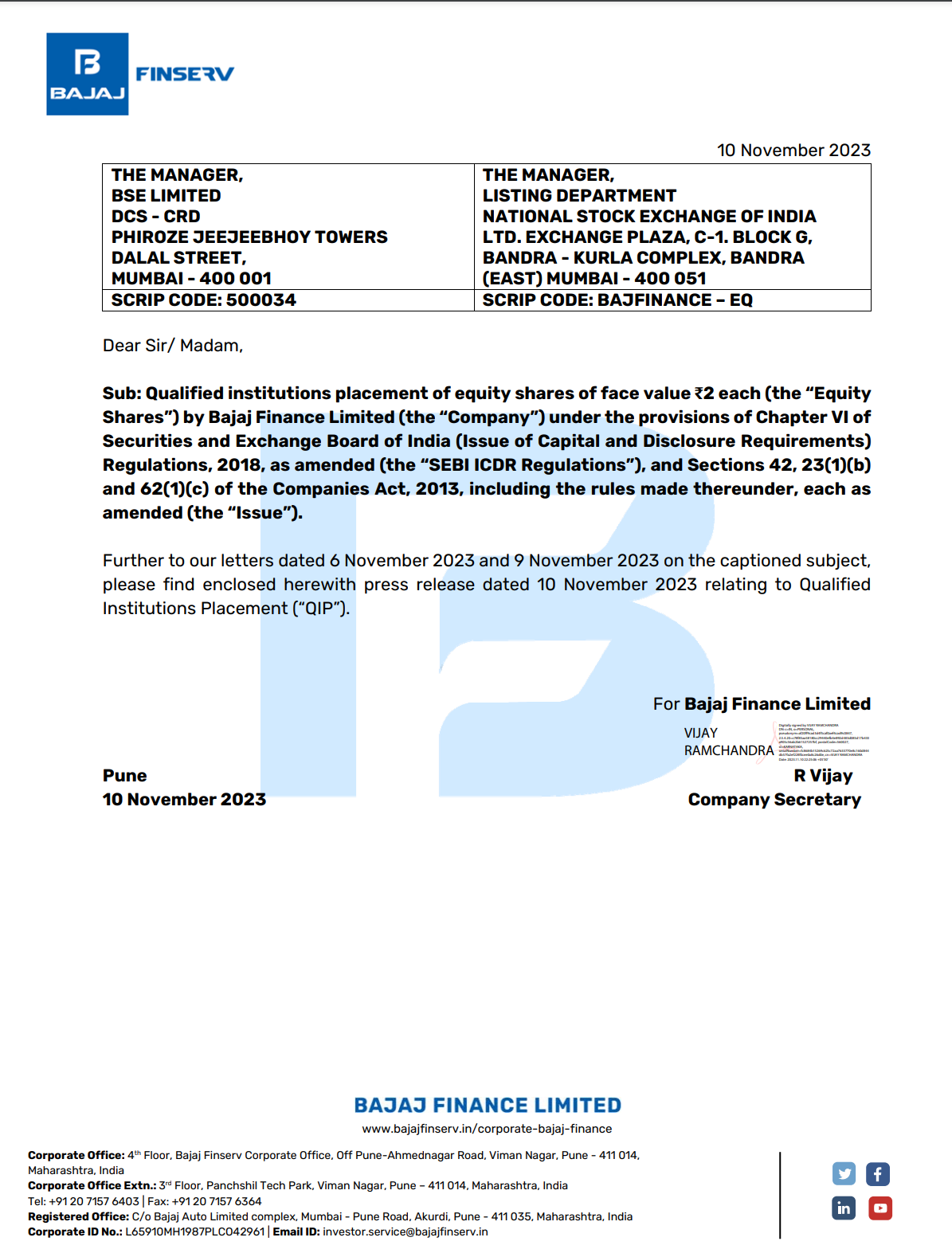

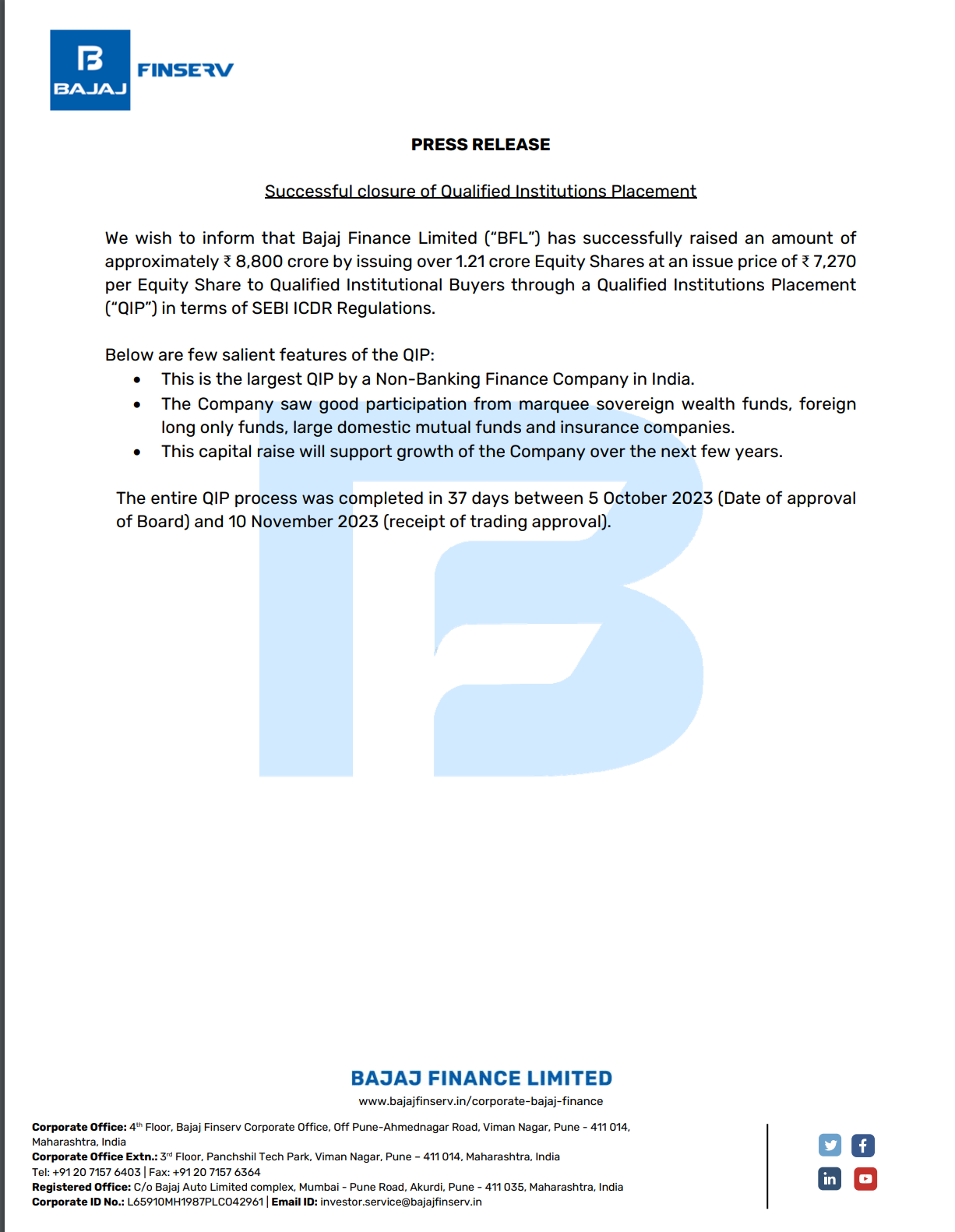

Bajaj Finance successful closure of a Qualified Institutions Placement (QIP) of equity shares.

- They have recently completed a Qualified Institutions Placement (QIP) of equity shares. This is a way for the company to raise funds by issuing shares to qualified institutional buyers.

- The QIP raised approximately ₹8,800 crore by issuing over 1.21 crore Equity Shares at an issue price of ₹7,270 per Equity Share.

- Some key highlights of this QIP:

- It is the largest QIP ever conducted by a Non-Banking Finance Company in India.

- The company received substantial participation from various entities, including sovereign wealth funds, foreign long-only funds, large domestic mutual funds, and insurance companies.

- The capital raised through this process will support the company’s growth in the coming years.

- The entire QIP process was completed within 37 days, starting from the approval by the Board on October 5, 2023, and ending with the receipt of trading approval on November 10, 2023.

8 Likes

6 Likes

After QIP as number of shares will increase, it will affect the EPS, so there will be any correction in stock price due to this ??

2 Likes

Should not be. As QIP at higher price will increase the book value of company.

However Bajaj Finance under time correction for more than 2 years, when it will break the hurdle not clear. But a kick will definitely come if there is Loan growth above 35%.

2 Likes