My thoughts on Bajaj Finance - Positives, Negatives and how I am thinking about valuation.

What Warrant Buffet said on Financials/Lenders: Lenders sell the most commoditized item: Money. In such a commodity-like business, only a very low-cost operator or someone operating in a protected, and usually small, niche can sustain high profitability levels.

Bajaj Finance is a classic case of how an NBFC overcame the advantages that banks may have due to lower cost of funds for banks over the years. It kept on adding new product lines over the years and in the process finding some niche areas and creating new income streams and focusing on cross sell. It has been mining its increasing customer franchise (now at 42.6M) products like health card, health insurance. It came up with innovative products like “zero interest EMI” in consumer durables space, a space that was initially ignored by Banks.

Positives

-

Liquidity is not an issue for BAF – Survival is not an issue. Its liquidity surplus is very strong with overall liquidity surplus of ₹ 20,900 crore as of 15 May 2020 on consolidated basis.

-

Consolidated borrowing mix for Money Markets: Banks: Deposits: ECB stood at 42%: 38%: 17%: 3%. BAF has a well-balanced liabilities profile. It is witnessing sharp decline in borrowing rates.

-

Enough fire-power in the PnL and balance sheet to absorb credit shocks. The above chart compares Bajaj Finance with some other NBFCs in terms of ability to absorb credit shocks measured by % of credit cost needed before tier 1 capital would come down to level below which NBFC would want to raise money.

Overall, some of the attributes which makes me feel that Bajaj Finance will survive and come out in a reasonably strong position from this crisis are –

- High Pre-provisioning operation profit margin

- Strong capital position

- Access to funding. It has been raising money at low rates post liquidity support announcement measures.

- Ability to accelerate and decelerate lending across different products depending on outlook as exhibited in previous crisis.

- Management’s agility and ability to innovate and react to new reality.

- Lower competition for those who survive with good balance sheet post this crisis. Not only that the larger players who survive the current crisis would be able to grow faster with lesser risk post the crisis due to lower competition.

I am not trying to mistake the current crisis with IL&FS crisis or demonetization. Covid-19 is by far the biggest crisis that any lender has faced. But what we have seen is that BAF came out stronger post some of the earlier crisis.

We have also recognized that Bajaj Finance has by far the best disclosures (significantly better than all the top banks). While this is not an enough reason to become positive, it speaks good about the management and the group.

Negatives/Concerns

-

Constrained environment which limits economic transactions for longer time than expected – Business conditions do not reverting to normalcy for the entire year, leading to demand depression. One near term development that may take place is that due to short tenor of large chunk of loans and very low disbursements in Q1, AUM fall in Q1 may be higher (even though at this stage, I would expect flattish AUM growth for full year and BAF to catch up in the 2H).

-

Extension of Moratorium by 3 Months – RBI has extended moratorium on repayment of loans till Aug 31, 2020 in order to help borrowers manage cash flows better. There is a risk that this may hamper the credit culture and may lead to defaults. In some cases, we have come across reports where certain customers have been unhappy with Bajaj Finance as they have had to pay high interest rates on the zero EMI loans.

-

Lower business will put pressure on fees in FY21 – Fees (from 54% YoY growth in FY20) should see a significant decline YoY in FY21 (baking 30%+ YoY decline) due to lower loan origination fees, moderation in cross sell fees and decline in card related fees. Insurance distribution will provide some support.

-

Higher share of unsecured loans and rise in share of high yielding assets over the years. This is a genuine concern which is why stock has corrected by over 50% and to address this one will have to build higher credit costs. It also needs to be noted that this is what gave BAF higher PPoP margin.

I have taken note that even if adjust for Covid-19 provisions of INR9b (0.6% of loans) that company built in Q4 results, the credit cost still doubled between FY19 and FY20.

-

Some top banks have been able to narrow the gap on some of the strengths that Bajaj Finance had. Many banks with their NBFCs, small finance banks have got into small ticket lending in consumer durables category where BAF has an edge. Having said that BAF is also getting into newer products. For example, Gold loan is one area where BAF has been investing.

Valuation

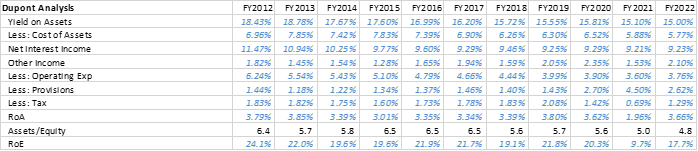

Bajaj Finance has been generating best in class RoA/RoE post its restructuring in FY09. For FY21, I would expect RoA/RoE to dip to ~2%/10% (bear in mind that Bajaj Finance leverage is lower so that is the reason for lower multiplier on RoA) driven by loss provision of 4.5% of AUM. For credit loss, I have assumed ~100% increase compared to FY20 levels. The credit cost has also been backed with the assumption that if 1/3rd of morotorium loans were to slip and building an appropriate LGD depending on the product segment. Baked in 100% increase in credit costs from FY20 level which already included INR9b of Covid-19 provision. This would bring the RoA to ~2%.

FY22 numbers are erring on conservative side. Leverage is on the lower side.

While credit cost should come down in FY22 from FY21 level, it may still be elevated if the economy is in doldrums, there is high unemployment rate and elevated stress level at SME level. Even if we assume, loan loss provisions of 3% in FY22 and some NIM contraction over FY21/FY22 from FY20 levels due to higher liquidity buffer and lower incremental lending to unsecured, RoA/RoE in FY22 can be 3.7%/17.7% which will be best in class. Should the credit costs start normalizing by FY23 (loan loss provisions reaching 2% of assets), BAF may reach RoA of 4.15% and RoE of 20%+ by FY23E.

For reference, HDFCB makes an RoA of ~1.8-1.9% and may make RoA of ~1.4-1.5% in FY21. Prior to Covid-19, Bajaj Finance traded at 70-75% premium to HDFC Bank owing to higher RoA and growth. This premium has now collapsed to ~35% currently with correction in valuation multiple of both HDFC Bank and BAF.

I believe that in the longer term, bank structure may have some advantage over the NBFC and hence I am inclined to give Bajaj Finance similar valuation multiple (and not a premium at this stage of the crisis) to HDFC Bank despite the higher RoA for BAF. One also has to recognize that Bajaj Finance in its current business model has not weathered the same number of crisis that HDFC Bank has weathered.

Overall, I may be inclined to start staggered buying once the current price comes somewhat below ~3x FY22 ABV knowing that the lenders who survive this crisis with a decent balance sheet will benefit disproportionately post the crisis.

Disclosure: Not Invested