Good Management will ensure good customer base. Poor Management will chase lower quality for returns. If You feel customer quality is a bit suspect that reflect on Management. We need to evaluate there credit evaluation process. If they depend completely on SIBIL score then we should be worried.

Never miss the forest for the trees

Bajaj Finance has been a classic case of what I feel people forgetting the big picture and missing the overall big picture apart from the fact that trees don’t grow to skies (pun intended).

The big picture in itself has been enormously high amount of profits along with enormous growth in many financial firms. While investors dealing in companies in diverse sectors such as chemicals, manufacturing used to get all juiced up by just thoughts of incremental revenues of few hundreds of crores (which can possibly re-rate such companies by more than 50% in many cases), when it came to even a small-cap financials the incremental profits in itself used to range in a different stratosphere. How financials got more than 40% weightage in NIFTY even when none of them are monopolies, have considerable amount of existing regulation and future regulatory risk and where threats from technology exists more than ever is a case study in itself. The reason was very simple - the market is huge because everyone wants credit and hence runway is very long and hence lets just extrapolate the last few years into eternity and give crazy multiples - even though the example of high RoE and high growth over 2 decades or more is just one in the entire space (even Kotak suffers from low sub 15% RoE) - which means that most of the growth is non value acretive. Infact in India, most value in book value terms has been created by raising funds right at the peak to mathematically increase the Book value per share by smart managers of financial firms rather than through lending operations.

Can many such financials continue to post 30-50% profit growth easily while GDP and core firms are struggling to grow in single digits just on account of penetration argument forever. Or there are risks which are being more than usual which are not accounted in these high profits - I certainly don’t see how many such firms like IndusInd (1800 to 350), RBL Bank (650 to 100) and many others have crashed only because of Covid.

When one lends, as Rajeev himself said in an interview, all the profits reside in the last EMI being paid. That is one risk to the earnings which is not captured in the financials under the accounting systems, especially for the organizations where the growth is high, loan tenure is short and most book is new. The only way to do the lending right is to be right just like a stock market investor - rapidly increasing the pace of lending when the times are bad and when great book can be built at decent rates as others are not lending and vice-versa. However in the pressures of market make most succumb to chasing highest amount of growth possible at precisely the wrong time - most firms end up choosing efficiency over sustainability which hampers them badly when the macros take turn for the worse.

Bajaj Finance in itself did not suffer from most of what I have written which probably is more true for most others. The credibility of the management is definitely high. What however they still suffered from was the way market extrapolated their profits like a simple excel model. If that would have continued for 5 more years for few of such firms, I am pretty sure their weight-age in NIFTY would have been maybe 60% of NIFTY and thinking in such big picture terms helped. Can 60% of all value cretaed in India come from just one sector. Currently there is one more gentleman in the markets falling under the trap of extrpolating last few years into eternity to think that 80-90% of India’s profits can be generated by just 10-15 firms (although none of these 10-15 firms are into technological innovation as such which is a data point completely different from USA if one has to look at global example). Yes sir, in which India will be no better in governance than many of African countries and will be a banana republic in which case one should possibly review the thesis of investing in our country itself.

Although brilliant Keynes have said that markets can remain irrational for more time than one can remain solvent, market is but a place for fair price discovery. Market exists for a reason and that is fair price discovery. In its search for the sole purpose of its existence, events that happen are only a reason to take things to their logical outcome rather than outcomes being dependent on the event itself. Market may have now (almost !!) permanently re-rated the leveraged financial firms to a new normal while on its way to also induce a massive time correction on low leveraged-low growth but exorbitant high valuation firms.

The current scenario is unprecedented, no one knows the impact on credit costs - one is still working with several assumptions like (almost) similar consumer attraction towards leverage and high ticket items post covid, no second waves, economy mostly back to normal by 4Q21 etc etc but then there is no surety about any of the above. When I read about gas leakage accident in Vizag and then plane crash in Pakistan today, I can think of some correlation. Its the same thing which happens to sports person on a game of football. It pains only when the game is over not in the heat of the moment. Complex systems unlike ceiling fans don’t start as soon and as well as before when switched on after it is switched off.

Bottomline is when the things are going great for any stock, investors tend to take things to extreme - all potential good things are priced in and all risks are shrugged off. As an intelligent and contrarian investor one has to always take into account both. Only then can a fair price emerge. Now when we have seen so many risks, I think one thing one must not do is to compare the Bajaj Finance today to its past either in financials metrics or in valuations metrics. People should also forget that it made a high of almost 5000 bucks and it grew 6x from demo to covid.

MARKETS DON’T LET YOU MAKE SERIOUS MONEY UNLESS YOU ARE GREAT TRADER OR A GREAT CONTRARIAN INVESTORS. A lot of great traders I know got stopped out of their positions by 4200 or above levels and a lot of good investors either entered pretty early at much lower levels than current price or sold out early enough. The remaining big chunk of people left were either momentum chasers without thorough discipline or or PMS fund managers making clients feel that it is so easy to make money in stock markets through them by only investing in firms showing highest growth. Many such managers even started to speak about financial firm valuations in terms of P/E although E can be highly volatile and of less meaning for a financial firm than the more conservative and cross cycle appropriate P/B which obviously looked far and far unusual for some such firms.

Independent, unbiased conservative and practical thinking is required where the big picture of current reality is not lost to take a call to buy or sell. If you don’t understand any of the above, understand just one thing - it is seriously very very hard to be a long term investor and to sit on a stock trading down or side-ways. Be sure of yourself before investing in some of these fallen angels.

All the best.

Regards,

Sarvesh Gupta

PS - I run a SEBI registered advisory firm. No current holding in Bajaj Finance. No trades in past month for myself or clients.

72 Likes

I don’t know why folks are flagging each and every post they don’t agree with. Don’t they know negative feedback loop is of immense value and helps achieve balance?

@adminph2 @Administrator @Donald @basumallick can the flag post criteria be tweeked by increasing the threshold reporting level for such as I feel this flagging will put off contributors both for and against a story? People will be walking on egg shells all the time. They may not be able to give honest negative opinion based on their interpretation of facts!

Dicslosure: Started investment in Bajaj Finance recently!

13 Likes

I found nothing offensive or against the forum rules in the post of Mr Sarvesh Gupta… Surprised to see this post being flagged…

1 Like

Thanks Aravind for bringing this important point up.

Certainly there should be enough space for both sides of arguments to be put up. For a healthy investigation into merits and demerits - of the case - as it currently stands and with unfolding developments which might tilt the balance of the odds stacked up. Notwithstanding the pedigree.

Think thresholds (for auto-hide posts) were higher earlier. Posts shouldn’t get hidden to a single flag (which might be a judgement error too on someone’s part (or newbies).

@pratyushmittal - please check the default limits set earlier

@basumallick - are you aware of any changes made

Another option for us to mull over - turn off flagging for folks with a history of using “flags” irresponsibly or maliciously. (if we notice that happening, often). As the community gets larger, we have to devise better mechanisms, before new users learn and imbibe the culture-fit!!

I will also check threshold limits set, from my side. Restoring the post for now.

14 Likes

Thanks a lot Donald. Your post on Bajaj Finance helped me build conviction and Sarvesh’s post helps me introspect on anchoring and looking at rear view mirror driving. Both + and - are of immense value to me.

Thank you for such a wonderful forum ![]()

6 Likes

Thanks Aravind.

In order to go beyond linear narrative-led arguments - weighed one way or another - we are coming up with Mental Models (hopefully soon, collaborating with passionate folks energised on this) for Banks/NBFC/MFIs - stuff that helps us focus on a weighted list of parameters - that move the needle the most.

That when used for a thorough dissection - I am convinced - will help point decisively to where the ODDS lie. And help bring about what Ray Dalio calls thoughtful disagreement. I go one step forward - from my experience I have seen when our mental models are powerful enough - they take us towards thoughtful agreements.

Meanwhile a simple construct to think more clearly.

Suppose you can construct the arguments why Bajaj Finance has all the wherewithal to survive (with data driven points) this period of uncertainty of moratorium extensions, and extend your horizon to 2 years out - before good growth returns - one can even think of it as a powerful Contra bet that one can keep buying cheaper, and allocate more. The underlying premise being those who are left standing till the agony lasts - will be in a winner-take-it-all mode - taking away more market share because of the space vacated by collapses.

Establishing that is going to take all our combined diligence and help from domain experts like @fabregas, @vaedermacher and many more still hiding ![]() . Once I have a decent handle on it myself, rest assured we will quickly get all the domain experts we need to solve this puzzle too.

. Once I have a decent handle on it myself, rest assured we will quickly get all the domain experts we need to solve this puzzle too.

I see it as an eminently solvable one. At an extremely interesting point in its journey.

Key is to remain flexible so one can change direction if conviction builds other way (even due to unfolding developments) or instead grow stronger in conviction.

Key is also to maintain small position sizes that can’t harm you. (Or, as some long-timers who rode from 2010 I know have done, quit 90%. I also know some long timers who are holding through from 2008 - with still significant positions - that can’t harm them).

Hedge our bets in a way that works for us. That we can sleep well at night. But keep working hard to help build conviction collaborating with the many smart minds/domain experts at VP and outside. Reach out! I have, have you?

18 Likes

I am not aware if there have been any changes made. However, all flags are decided by the moderators, so I dont see any major issues.

Disclaimer - I have never invested in lenders so far, so I might be guilty of being very superficial here. No position in Bajaj Finance

I am just jotting down some points as a neutral observer

BAF is unique in the sense that they can borrow long term and lend out short term. The debt market perception of the company is as good as it can get, HDFC Ltd and BAF are the NBFC’s who can raise money even in a dead market

The business is primarily built off unsecured consumer lending; irrespective of how good a job they do, the risk will always be higher compared to secured lending franchises like HFC’s and banks. No amount of management quality can work around this fundamental fact. For this reason P/B comparisons aren’t insightful, this is like comparing a standalone health insurer with a reinsurer. The inherent business risks are very different.

Lending businesses are unique in the sense that unit economics are back ended. I can make a 4 year loan today and have everything go as per plan for 42 months, then a crisis hits and takes away all the profit assumed over the initial 42 months. Most (if not all) of the profits in lending come from the last few EMI’s - that’s just the way it works. It is for this reason that lenders have a high element of cyclicality, every 10 years one will have a tail event that questions not just future growth but also past growth and quality. It does not work this way for a manufacturing or an IT business (unless one is talking of a cloud vendor where the situation can be similar - all profits coming in the last 2-3 years)

Businesses that go through a phase of hyper growth have one thing in common - they hit upon a template that works very well (either by design or by luck) and then they just replicate this template in an auto pilot mode in a market that offers multi year growth possibilities. That is till the underlying narrative or situation breaks, then they need to revisit the template which is no longer as relevant. See the story of Infosys, as good a story as one can get in terms of growth runway, management quality and corporate governance. Once they hit upon a template that was working, they just replicated that template (all the while telling their employees to just execute and not use their brains) for 10 years. But once the operating environment changed and the old template was no longer as effective, they had to look for a new template; they still haven’t found one that can replicate their previous level of success.

Moats and success stories are built on multiple small things that work together to reinforce things, once 2-3 of these go out of whack (for whatever reason) it is very difficult to replicate the previous level of success.

It is interesting to note that consumer durable plays like Whirlpool, Johnson Hitachi and even Dixon Tech for that matter have held up far better than BAF. I find it a useful construct to see the entire value chain in a theme and then compare business quality across these industries rather than just compare the business quality of a BAF w.r.t to another lender who is trying to compete with BAF. If one believes that consumer electronics will do well after the next 2-3 Q’s, I would compare investment ideas across all of these - goods makers across segments (TV, AC, Washing Machine, Refrigerator), businesses that support these OEM’s (Dixon, Amber) and the businesses that fund these purchases (BAF and other lenders focusing on this segment).

Bulk of the growth (and hence valuation) that BAF enjoyed was because they were sitting at the front end of this funnel but that growth comes at the cost of balance sheet risk.

As for post COVID, I do not see how BAF can benefit as much as what an HDFC Bank/ICICI Bank/Kotak bank can benefit. A bank needs a high amount of credibility and perception of safety to succeed, so no surprises if depositors flock to a large bank in a crisis since one is parking his hard earned money there. When it comes to lenders however this perception of safety does not assume so much importance since the consumer is borrowing money. Rates of lending are anyway a commodity, so it is customer acquisition and cross selling that matter most to a pure play consumer lender. Unless competitors go away in this crisis thereby leaving the field open, I don’t see how BAF can massively benefit from this crisis. I would refrain from comparing banking franchises to pure lending franchises for this very reason.

BAF will likely be the mainstay of it’s chosen business segment but my sense is that the previous level of success it enjoyed (in terms of stock returns) may not come back.

At some point of time over the next 2-3 months I will take a detailed look at BAF and approach this ground up rather than take the 20,000 ft view again

41 Likes

There is no doubt that this is a fantastic company with good management, but I am still not sure what is the best way of accumulating this stock. I can think of two ways

Option 1 - Take a small position, and keep adding on the way down as we get more information on the post COVID scenario and am able to build more conviction

Option 2 - Take a small position and patiently wait. Start accumulating only once the cycle recovers and tailwinds start supporting the business/cycle.

The Pro’s of Option 1 will be that I can build a good solid position at decent valuation. However the biggest drawback is that Market can remain Irrational longer than one can remain solvent and time correction can be quite long if the business cycle doesn’t turnaround quickly

The Pro’s of Option 2 will be that one can keep on analyzing the business cycle / business and invest only once the conviction is strongest supported by the Market trend. The drawback is that one may lose 20% - 30% of Profits or the chance to buy at decent valuations

More often than not I go with Option 2 and buy business with some tailwinds and it generally helps me to stay away from the Value trap’s

Any thoughts or suggestions are welcome

2 Likes

Admins/moderators are not interested in removing posts with a negative bias.

Posts which are flagged (and sometimes eve those that are not) are removed because

-

They dont seem to add value to the discussion being irrelevant, out of context

-

Abusive or offensive

-

One liner or two liner kind , “like thanks mr xyz” . Instead push the like button if u have liked what u read, or got your answer.

-

Posts which are repetitive in nature.

-

Posts which appear to be manipulative in nature.

Or some other such observations.

This is a thread on a specific company and henceforth we will stick to the relevant discussions rather than discuss the anatomy and physiology of flags ![]()

18 Likes

I would say wait for worst case scenario and buy decent quantity. For example with book value of 500 if you give price to book of 2 you will see price of 1000. Don’t buy if it does not come to that level.

1 Like

From a recent interview of Ramesh Damani with Madhav Bhatkuly,I fetched some figures:

Bajaj Finance Book is 150,000 crores

Gross NPA 1.6%; Expected to move by 80% which is an impact of 1.3% on balance sheet, thats approx. 1950 Crores.

Now,Variable cost can be tuned down significanttly.

Current spend is about 2600 cores

35% variable is 900 crores which can be saved

Direct selling agent commission is 1000 crores; it can be reduced by 50% ; savings of 500 crores

Travel, advertisement, employee reduction can be another 500 crores

Total savings: 2000 Crores

So, net net impact is squared off from Savings and cost cutting.

India with a 2.9 TN USD Economy, consumer financing is JUST 4.5 Bn USD

Let us not forget one universal truth: we overestimate things in short term and underestimate in long term.Bajaj Finance fell close to 80% in Global financial crisis, from Rs 42 to Rs 6; people would have thought then also that it is finished.

Money crunch and liquidity was far worse than what it is today.They are raising money at 4.5% which show the might and credibility of the franchise now that was not there in 2008.

The most important thing is Patience and temperament which unfortunately is getting extinct with the advent of technology and fast paced world.While it is easy to quote Buffett and Phil Fisher often “The best holding period is forever”. Truth be told, we tend to become shaky even at 1 or 2 bad quarters and start questioning ourselves.

I am optimistic(prediction is a waste of time though),2 years down the line, when we revisit this timeline on VPForum, we will again regret not buying at these levels.Do we really think that the human race will completely stop spending and buying new stuff, will remain fearful and jobless throughout!!!At least 200-300 yrs of history does not say so.

Will Covid completely wipe out the growth dynamics of Bajaj Finance( people will stop taking credit,moratage,rural loan etc), I do not think so.

Does the management have the firepower to look for new areas of growth? I am 100% sure they have ; healthcards,gold loans, more rural penetration etc. are some of the levers.

Only when you do not have clarity, you will get eccentric price of a security; if everything is clear, it would have been priced to perfection.

Morgan Housel in one of his recent blog wrote:

“Think of all the 2020 market forecasts published in December.Authors of these reports – most of which have been quietly removed – might say, “I couldn’t have foreseen Covid-19 in December, and it upended my entire forecast.” To which my response would be, “Yes, that’s my point.” If you claim an ability to foresee events, you can’t use events you didn’t foresee as an excuse – especially when unforeseeable events move the needle most. When a company reports poor earnings it’s often said they missed analysts’ estimates. But earnings don’t miss estimates; estimates miss earnings.”

40 Likes

Hi all,

This is not to discourage anybody from buying/holding/selling Bajaj Finance.

I had posted this on Hitesh bhai’s page and thought this needs to be posted on this page as well.

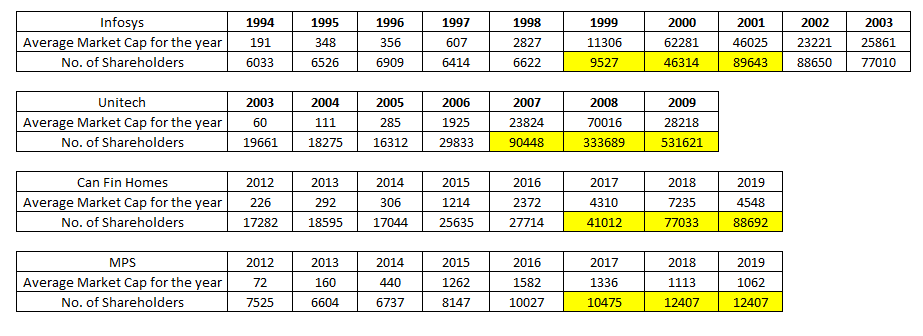

I think it’s lies in our sub conscious nature to catch falling knives

Here’s some data I collated from the annual reports of these companies. As we can see, the number of shareholders almost always goes up when a sector leader falls. Even after these companies’ glorious days were over, the number of new shareholders kept increasing. Like everything else in the stock market, there will be exceptions to this rule. But generally speaking, this pattern plays out. So we should watch out and not fall in the trap called Anchoring bias.

Maybe that’s why averaging up is almost always a better idea than averaging down. I would rather buy Bajaj Finance at 20% higher than whatever bottom the stock price touches than buying it today.

10 Likes

1 Like

Such public anger is quite visible in my district also. The collection agencies of Bajaj Finance is giving hard time to borrowers.

Searching tweeter hashtag #bajajfinance and #bajajfinserv also reflect anger of public

1 Like

I tell you if I had a nickel for every time someone said this 20% from bottom and average up logic - I’d be amongst the richest people on earth by now!

Sorry - I’m just quoting you and not picking on you as there are literally thousands of investors who say this average up stuff (many on this forum as well) but this logic has never ever made sense to me.

Let me tell you what I understand:

1. Bottoms can only ever be known in hindsight- Like now some people claim 23rd March 7500 was a bottom for the markets. Nobody said on 23rd March that right here right now is the bottom!

So that means an investor can never predict if today is the bottom! Only days/months later can we say that.

2. Now coming to why I don’t find logic in the argument of 20% from the bottom - please go check the price history on Bajaj Finance. The stock made a low of 2105 on 24th March and made a high of 2936 on 26th March closing almost at 2800 levels. There is your 20% from the bottom my friend! It’s much more than 20% actually - stock climbed 40% from the lows!!!

So I sit here and read your post and wonder why aren’t you already invested since the stock already fulfils your criteria of 20% from whatever bottom it touches?

And now coming to this averaging up which a lot of well known investors talk about as well - I averaged up in a couple of Multibaggers I was sitting on (Can Fin Homes 4x and Avanti Feeds 9x) - and all I ended up doing was SABOTAGE my returns of 4-5 years by reducing Can Fin to 2x and Avanti to 40-50% returns!

I have been holding Bajaj Finance since last few years from 1700 levels. So after losing most of my gains in Can Fin and Avanti due to averaging up - I was extremely wary of averaging up in Bajaj Finance when it was making highs from 3000 to 4000 to 4900 and even then I give it another shot but with extremely small quantities and it took my average price to around 2000. Thank god for not following AVERAGE UP again in a big manner

All this market jargon of catching falling knives, averaging up, let it bottom out…bla bla is mumbo jumbo and at best extremely contextual for each and every stock. None of these jargons might make sense for the way some stocks behave. Small investors better get their head around this else risk losing money big time.

Disc: Invested in Baj Finance

68 Likes

Just because averaging up did not work out for you does not mean it doesn’t work for everybody. Averaging up has worked for me many times and I will continue to stick to what has been working for me all these years.

These are the things that came to my mind when I exited Bajaj Finance

-

I never said I will buy 20% from the bottom when the business is still facing head winds. I should have mentioned, 20% from bottom ONLY when I see the company’s problems are starting to get resolved and I have at least some idea how much of an impact this moratorium is going to have on this company’s balance sheet.

-

Why on earth would I ignore the opportunity cost of staying invested in Bajaj finance and not move my money to a company with tail winds in a sunrise sector? By staying invested in Bajaj Finance, I was assuming that there are no better opportunities out there. It’s only logical to find a sunrise sector and move your money there. Everything you do or don’t do in the markets comes with an opportunity cost and each investors’ opportunity cost is different.

-

I am not the proprietor of this company. I am a minority shareholder. And as a minority shareholder I have the advantage to move my money to a business with better prospects. Why would I even want to give up this advantage? As Lord Keynes had once said “When facts change, I change my mind. What do you do, Sir?” And there’s no denying that facts have changed for lenders.

-

Doesn’t good investing mean one needs to cut losses quickly? If yes, then shouldn’t I be cutting my losses in Bajaj Finance and ensure survival.

-

Does anybody know how much of this company’s equity is going to get wiped out, by the time things normalize? No.

-

Does anybody know how long jobs and businesses are going to be down? No. By staying invested in this lending company we are assuming it’s borrowers will be back up on their feet in the next 4-6-8 quarters. This assumption itself is subjective to so many moving parts.

-

What kind of an impact will the moratorium have on Bajaj finance’s borrowers’ psyche? Nobody knows. Will some of them think, not paying emis is the new normal? Will bad behavior drive out the good? How will bad borrowers influence the good borrowers? We all know what happened to SKS microfinance when Andhra’s politicians stepped in to pass a law to protect their vote bank from loan sharks. Will history repeat itself and will the government intervene again and tell lenders, boss you are not going to use hard tactics to recover your bad loans. What happens to those low NPA numbers then? What happens when shit hits the ceiling? Nobody knows.

-

How much of the company’s equity is going to get wiped out from the balance sheet, for good?

-

How many borrowers will lose jobs? How many borrowers will close their businesses, for good? How many of those closed businesses are big ticket borrowers?

To me, staying invested in Bajaj Finance today, is the functional equivalent of analyzing macros. And as we all know macros are subject to a wide range of possibilities.

16 Likes

Hello everyone,

this is a very generic post on investors’ behaviour when their favorite stock starts falling. I am not an investor in Bajaj Finance and moderator can delete my post if deemed irrelevant here.

-

Not more than a year ago, I burnt my hands my Yes Bank stock. Now, I am not saying that BFL is anyway similar to Yes Bank as a lender, but a falling stock is a falling stock. There is a saying that all happy families are happy in same way, but all unhappy families are unique. Same is true for a falling stock on chart. They all go through distribution, then breach of 200 DMA, and then some retracement and then outright dumping. In my newbie technical analysis experience, I think BFL has skipped the distribution and started with outright dumping.

-

Around May last year, I started reading the books of Mark Minervini and I think most of the book is focused on cut your losses early and never average down. This is applicable for retail investors, because information-access wise we are at the lowest rung.

-

Around August, I was sitting at 50% loss in Yes Bank and exited the stock at around 100. I was told by few friends why I am booking loss, but that was the last time Yes Bank ever saw 100 Rs on tape. I could have been wrong, but it was not about being right or wrong but changing habits. One of my known eventually sold the stock at 20 Rs in March, taking almost 80% loss. Heard of some NRI in Dubai who had to sell one of his real estate investment to get out of long F&O position in Yes Bank.

-

Now why I am narrating it here? Because I am seeing similar pattern here.

-

Always always start with the position that “markets are never wrong”. If market has cut down BFL to 40% of Feb high, then there is some reason behind it. People who have sold the stock since Feb had much bigger holdings than retail investors and they have jumped the ship.

-

Someone above argued that I am ok buying stock at 20% higher, and then other person counter-argued that why you didn’t buy at 2300 when stock retraced. Point here is that stock is still under downtrend, even when it did some retracement, it was even less than HDFC Bank or Kotak. And mind you, even they did worse than retracement of overall market.

-

So all in all, BFL is even worst than other biggies of financial services. Overall market and most of the stocks put their lows on 23rd March and now trading over that, if even barely. BFL is good 15-20% lower than 23rd March closing. Stock has breached the support around 1950 it was barely hanging. So things can (and most likely will) go further wrong.

-

A stock which has fallen 60% can further fall 60% before finding the bottom and base formation. Now it’s not an advise to sell the stock right away, but just to tread with caution.

Thanks

13 Likes

HI, Good discussions on BAF. Some very interesting analysis and logic-ends. Having my fingers-in-the-pie (being a banker), I can relate to some of it. My two macro cents:

a. NBFC will remain an imperative leg towards financialisation of Bharat. With fewer banks in number and their BS position added with equally not-so-good healthy BS of most of new fintech-banks, NBFCs with nose-on-ground, ability to raise long-term funds at best-in-class cost, clean mgt will not remain away from participating in Bharat growth. Ceveat is… market believes and respect that growth structure.

b. With new life order of survival-of-the-fittest among NBFCs and ensuing NPA flood, competition to BAF is expected to be low and costly. Rather it is expected a number of win-win hand-shakes among some sensible players in near future keeping their regional or product dominance in place.

c. Growth of BAF in coming 2-3 qtrs is not to be expected but this time is good for strengthening BS and this aspect to be keenly watched. Mkt values growth, no doubt, its present value reflects this fact. BAF premium valuation was on the basis of innovative biz model, positioning ahead of mkt, nose-on-ground, clean mgt and lower CoC.

So what has changed?

-

BAF position of going slow on growth - Any lender who does this in this market will ONLY survive and thrive. Strong BS of any lender will make her ready for next wave of growth. No complaint on this front.

-

Higher level of NPA and higher haircuts - Yes… its going to hit BAF but not more than peers. With Tier ~21% and CAR at ~25% PPOP ~9% is better placed to take it up on chin than heart. Its CoC is estimated to be up 20-30bps higher in Y21 but its only guesestimates and in worst case might still go up another 20-30bps.

-

Customer Loyalty - It is subjective depending upon not only Lender’ behaviour / conduct but also Borrower’s conduct and ability to pay. GNPA at 1.6% (net 0.7%) points out positive on quality of customers and BAF underwriting. Temp inability of customers will cause temp NPA situation. So BAF shall provide for it and act sensibly to maintain the customer’s loyalty.

-

Physical touchpoints - this space will change and BAF has already moving to capture that customer base through digi-channels. This aspect requires further deco incoming months. It is expected from BAF mgt to bring its skills on table to take benefit of this new order with innovative offerings / solutions. A space to watch!

Disc- Am invested at very low levels and partially booked profits at higher levels and added more in last 10days. Am not a registered financial advisor and views expressed here are my personal and not aimed to solicit any kind of gain/ benefits.

Happy Learning!

9 Likes