Nice report…

It states

"Near-term asset quality and growth impact is inevitable, not only for BAJF but for the … "

“Expect AUM growth to pick up in FY22…”

Nice report…

It states

"Near-term asset quality and growth impact is inevitable, not only for BAJF but for the … "

“Expect AUM growth to pick up in FY22…”

I think any assessment of FY 22 can not be made at this stage.we should factor in for pandemic to recede, assess the delinquent loans, NPAs, job losses, vaccine development and availabiity and change in buyer’s behavior post pandemic.All these are not easy answers as of today and any assessment without these factors could be too much off the reality

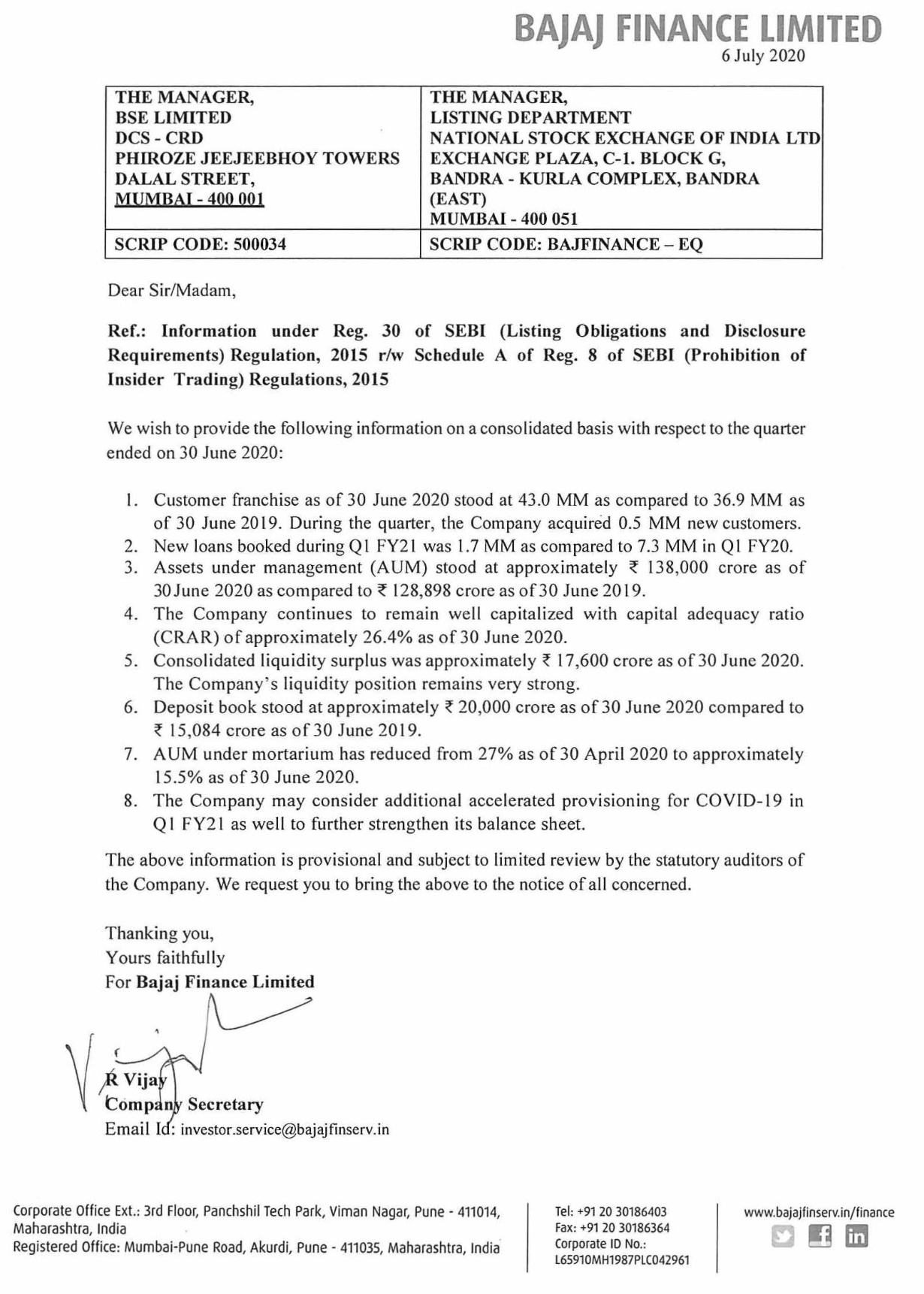

The annual report for FY 2019-20 is published:

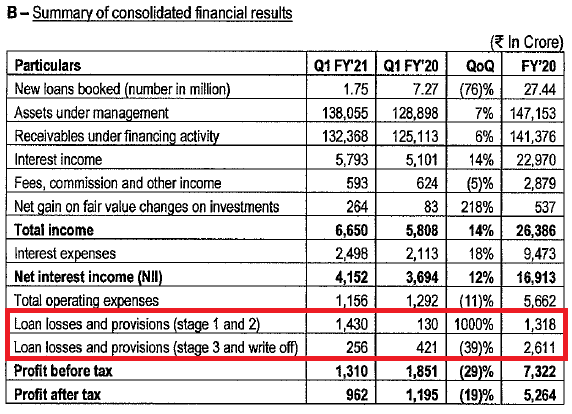

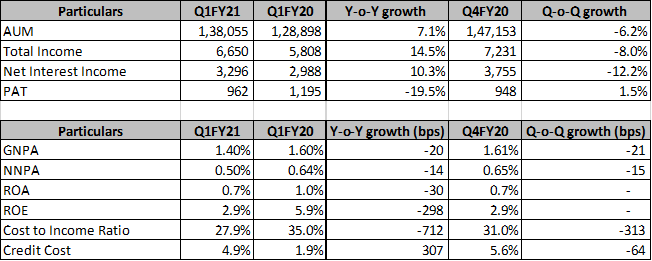

Q1 Results are out now. Brief summary of consolidated results and operational highlights below

Q1 revenue at 5793 Cr, up 13.5% YoY and down about 8% QoQ

Q1 PAT at 962 Cr, down about 19.5% YoY and up marginally by about 1.5% QoQ

Operational Highlights

Consolidated moratorium book has reduced to f 21,705 crore (or 15.7% of AUM) from f 38,599 crore (or 27% of AUM) as of 30 April 2020 owing to reduction in bounce rate coupled with better collection efficiency

They have made an additional contingent Expected credit loss provision of Rs 1,450 Cr during the quarter

This takes the overall contingent expected credit loss provision to Rs 2,350 Cr as of end of June 2020

The contingency provision for COVID-19 is now at 10.8% of consolidated moratorium book.

This contingency provision together with existing expected credit loss provision of 623 crore provides an overall provisioning coverage of 13.7% on the consolidated moratorium book

Further, based on their estimate and judgement, they have reversed expected un-collectable component of capitalised interest amounting to Rs 219.51 Cr charged on loans against moratorium

New loans booked during Q1 FY21 declined by 76% to 1.75 million from 7.27 million in Q1 FY20

Customer franchise as of 30 June 2020 increased by 16% to 42.95 million from 36.94 million as of 30 June 2019.

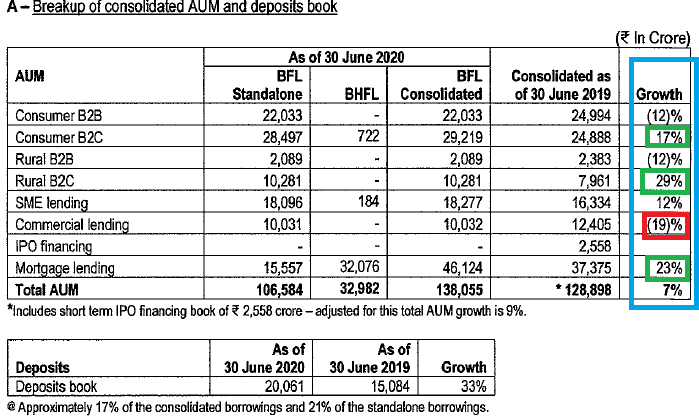

Assets under management (AUM) as of 30 June 2020 grew by 7% to~ 138,055 crore from ~ 128,898 crore as of 30 June 2019

Net Interest Income for Q1 FY21 was up by 12% to ~ 4, 152 crore from ~ 3,694 crore in Q1 FY20.

Total operating expenses to net interest income for Q1 FY21was27.9% against 35.0% in Q1 FY20.

Loan losses and provisions for Q1 FY21was~1,686 crore as against~ 551 crore in Q1 FY20. This was due to additional provisions made, as stated above

Gross NPA and Net NPA as of 30 June 2020 stood at 1.40% and 0.50% respectively, as against 1.60% and 0.64% as of30 June 2019.

The provisioning coverage ratio as of30 June 2020 was 65%. Standard assets provisioning (ECL stage 1 and 2) stood at 273 bps including contingency provision for COVID-19 and 101 bps excluding contingency provision.

Capital adequacy ratio (including Tier-II capital) as of 30 June 2020 stood at 26.40%. The Tier-I capital stood at 22.56%

Complete details at

https://www.bseindia.com/xml-data/corpfiling/AttachLive/6a748c60-4d91-46a5-9821-544c570dc17c.pdf

Q1FY21 Results (₹ in crore)

Key Highlights -

Consolidated moratorium book is ₹21,705 crore (or 15.7% of AUM) from ₹38,599 crore (or 27% of AUM) as of 30 April 2020 owing to reduction in bounce rate coupled with better collection efficiency

During the quarter, an additional contingency provision for COVID-19 of ₹1,450 cr taking the overall contingency provision for COVID-19 to ₹2,350 crore as of 30 June 2020. The contingency provision for COVID-19 is now at 10.8% of consolidated moratorium book. This contingency provision together with existing expected credit loss provision of ₹623 crore provides an overall provisioning coverage of 13.7% on the consolidated moratorium book. Addltionally, as a matter of prudence, the Company has also reversed ₹220 crore of interest income from the interest capitalised during moratorium period.

Overall liquidity surplus of approximately ₹ 17,700 crore as of 30 June 2020 on consolidated basis. The Company’s liquidity surplus as of 20 July 2020 was approximately ₹ 20,590 crore

The Company restarted its urban B2B, rural B2B, auto finance, gold loans and loan against securities businesses from 10 May 2020 with stringent loan to value (LTV) and underwriting norms and focus on existing customers. The Company restarted its home loans and credit card distribution businesses from June 2020. The Company deferred restart of other businesses viz. loan against property, SME, urban B2C, rural B2C and commercial businesses to July 2020 due to extension of moratorium

GUIDANCE - At this juncture, based on our assessment, 75+ cities should revert to pre-COVID volumes by October, 40 75 Cities by end November, 10-40 cities by January and top 10 cities by March. All this is of course subject to Government of India not enforcing a 2nd national lockdown. Based on this assessment, the Company estimates AUM growth of 10-12% in FY21 .

GUIDANCE - The Company last provided an update on its credit cost scenario model on 6 April 2020. The company considered lockdown of up to 50-days for its various scenario planning. Estimated an 80-90% increase in credit costs (₹ 5,400-5,700 Crore for FY21) assuming lockdown till 15 May 2020. However, the national lockdown continued for 68 consecutive days till 31 May 2020 and it was followed by multiple district / state level lockdowns imposed by respective local authorities. At this juncture, big cities like Bangalore and Pune are in midst of more stringent lockdown than the national lockdown. The Company has now updated its credit cost scenario model for FY21 considering extended disruptions. It now estimates its credit costs to increase by 100-110% ( ₹6,000-6,300 crore for FY21) over the pre-COVID credit cost of previous year. The Company has strong pre-provision profitability to absorb increased losses caused by COVID-19.

Added 2,800 collections officers and approximately 16,000 collection agency staff to manage the increased bounce volumes caused by COVID 19.

The Company has revised its margin profile in certain businesses to protect its overall profitability. On mortgage business, the company is facing significant pricing pressure and is repivoting its mix marginally for short to medium term.

The Company is accelerating its 3rd transformation journey conceptualized in Q3 FY20. The company is utilizing this pandemic time to completely transform itself by depolying “Zero Based Budgeting” methodology to reimagine all its business and functions. All businesses and functions are getting into micro detail of every process, customer moment of truth and cost lines and completely reimagining them. As a result, plan to come out of this crisis as a company with enhanced customer experience, stronger digital orientation and a leaner cost structure. As and when demand comes back fully, we will be ready to leverage this transformation to grow our business rapidly.

Business Potential - At this juncture, company has access to 10.5 cr customers and prospects. It intends to create an ecosystem of sales finance products and complete range of financial services for these customers and prospects. Existing customers would be able to access financial services across lending, insurance, investments and payments in maximum 3 clicks.

BFAL_Q1_FY21- Concall Notes and Highlights.

BFAL_Q1_FY21_CC.pdf (348.5 KB)

Hi guys, Does anyone know the outstanding gold loan AUM for Bajaj finance. They used to disclose this earlier (until their FY19 annual report), but this number is missing (or I couldn’t find it) in their FY20 AR. If anyone can point it to me, it will be really helpful.

HDFC Sec has initiated coverage on Bajaj Finance.

Interesting tie up with V-Guard Ind. for the upcoming festive season.

Whats good is that ticket size is Rs 3000 & above which I think is taken care of.

Saurabh Mukerjea on why Bajaj Finance and Asian Paints are Big Data Analytics companies - watch this very interesting take presented at the Edelweiss Virtual Conference - https://www.youtube.com/watch?v=ewSKcUTF1kM&t=3027s

RBL Bank, however, decided to take a different approach. It told customers of ‘Bajaj Finserv RBL Bank SuperCard’, launched in February 2017, that they could withdraw cash with no interest levied up to 50 days. A flat processing fee of 2.5% would be charged.

Better Regulatory Risk Navigation by Sticking to Affluent Customers.docx (842.7 KB)

Regards

Sunny

Hi…I am new to this thread, so pardon my ignorance.

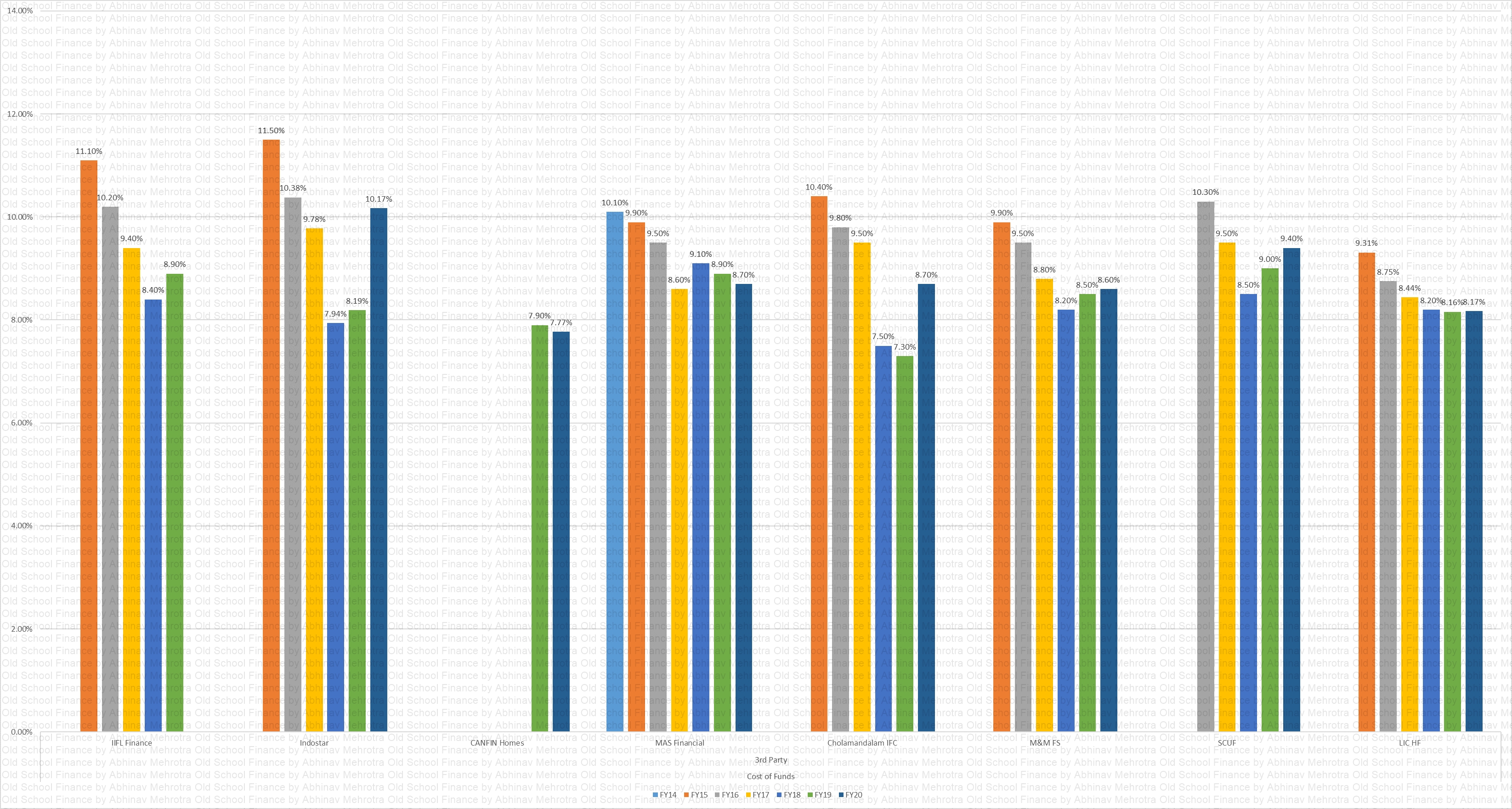

Can someone guide me as to where can one research for / find the commercial paper rates at which Bajaj Finance is borrowing vs other NBFCs like Sriram Tpt, Cholamandalam, Mahindra Fin etc.

Because if the rate differential is substantial, it would be a major source of competitive advantage.

Thanks.

Thanks a lot…@hack2abi

Can u also guide me to the source of this data for future ref.

It ll be a great help !!!

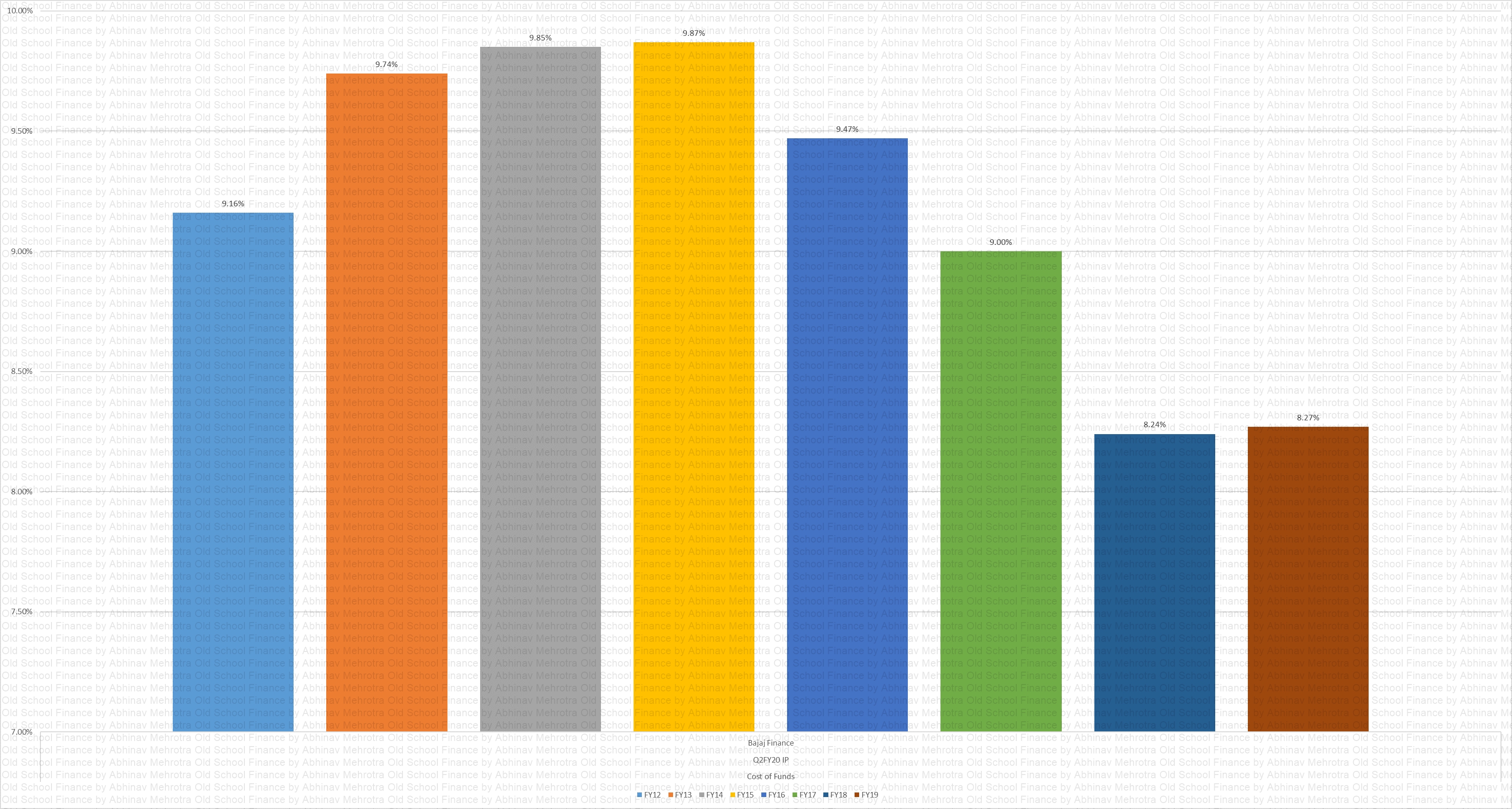

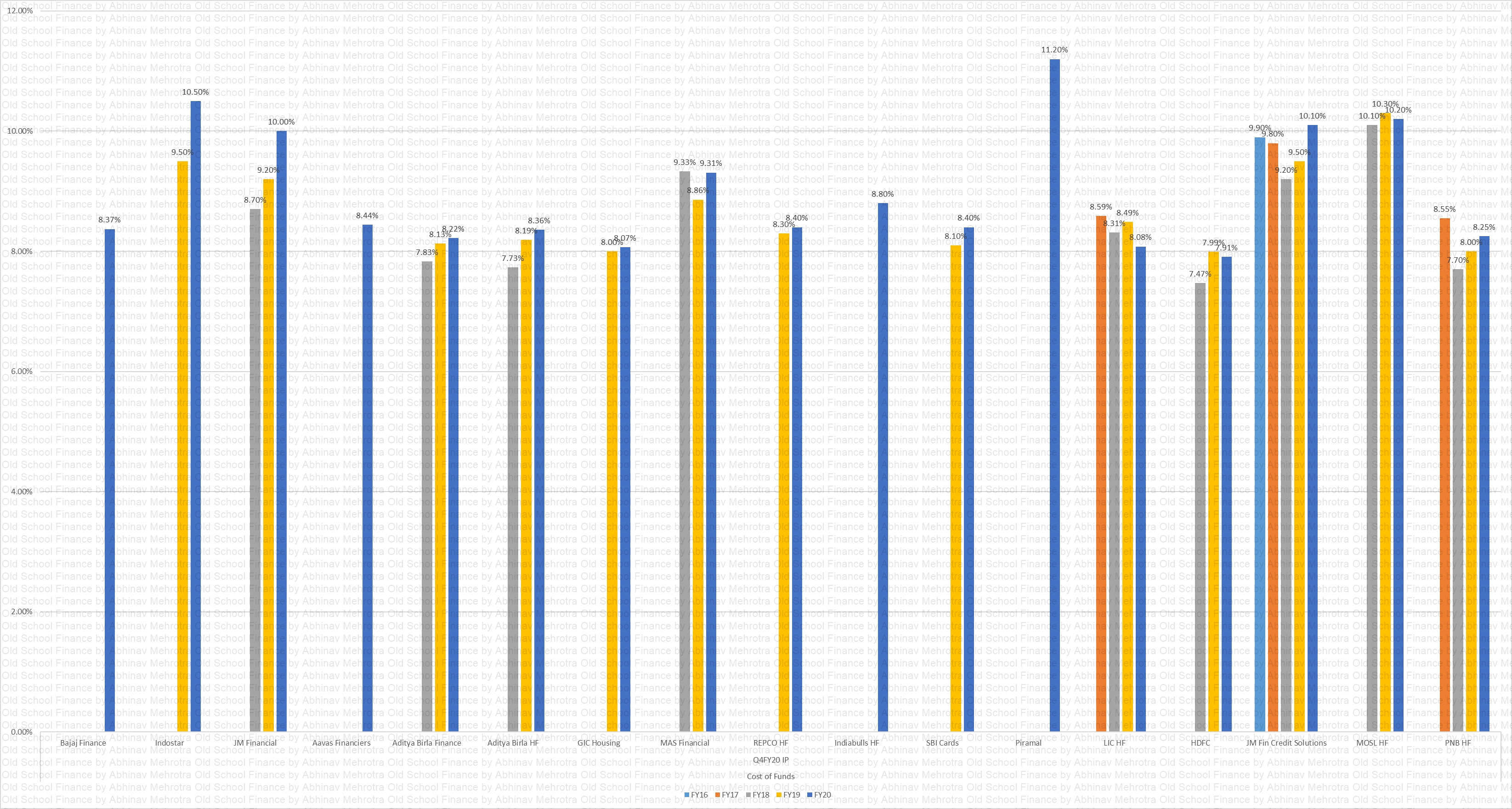

Thanks @ranvir for addressing that. I am also trying to find that. By looking at the the chart seems like Bajaj Finance cost of borrowing is not low. I heard they are borrowing at 3-5% rate. @hack2abi can please shed some light on it

Collected from various investor presentations, Annual reports, press releases made by companies from time to time.

@sandyinfo These are weighted average figures provided by the companies. The incremental cost of borrowing will be somewhat different depending on the market environment.