Dmart is now valued around 2,13,000 crore. At 15-20 PE, the company should make a profit of 10000 crore to justify this valuation. There are less than 15 companies in the entire country making more than 10000 crores. Even at 30 PE, there are only around 20 companies, making more than 7000 crore profit.

While the sales and operating cash flow growth has been brilliant, the ROCE and operating profit margin have not been best in equity . The owner is a financial genius able to sell dreams at 20 times book. Also there is heavy competition and the company has already covered areas in the country having greatest sales potential.

I am a concentrated investor and have some stocks with 60 or 70 PE, and while impressed with Dmart, it still appears to be a gruesome business based on Warren Buffett’s financial criteria.

Hence it is too early to count the chickens before they hatch. For consumers sake, I hope Dmart pulls it off.

There is no doubt that Dmart will earn 10000 cr before 2027. Opportunity size is so big that they have captured nothing. As ROCEis concerned, we should look for incremental ROCE. Walmart is selling at 28 PE even after saturation . Profits as well as QIP money are reinvested to grow faster. This is unique company.

Disclosure - Largest holding.

15-20 PE for a growing retail business in India? Even some PSU banks are currently trading at 50 plus PE. Not sure how you arrive at this valuation figure.

Yes, greater than 100 PE certainly makes the investment rationale shaky, however this has some fundamental reasons which is attracting the smart money.

Huge opportunity for growth. It reached 1million plus population cities as of now. The growth in urbanisation and employment(more workforce)% will also help in getting more numbers.

Operational efficiencies are one of the best in off-line retail if not the best. After sometime, the inefficient ones will make way for efficient ones.

The promoter is one of the most successful investor in India and infact comes under good promoter. The return ratios and financial viability etc will be checked. Mr Radhakishan Damani would have easily started the franchise model to give a spurt in growth figures in short term but then he understands long-term and so never considered the franchise model.

Dmart is a platform/toll bridge kind of business. They will have to spend less for capex and also once they master the volume game there is network effect. Once the company’s growth gets saturated, the further growth comes from making in-house products. There is no end for in-house products. Batteries to medicines to chips etc

Great balance sheet with no debt which is different from many other growth chasing retailers

Long-term investment - The base for long term investment is certainty. The question to ask here is , how sure you are whether Dmart can sustain for next 10/20/30 years. Under a good promoter(great investor) whose majority of wealth gets created by growth in this company, I think this makes the market give it a longer rope.

Capital employed in the business was 1000 crore in 2012 which has increased to around 6000 crores in 2019 at a cagr of 29% to give a profit of 1000 crores. If Dmart were have to employ additional capital at this rate, for the next 9 years, to increase the capital employed to 60000 crores, they would make a profit of 10000 crores in 2028.

If the stock were to be valued at 30 times PE in 2028, the market cap would be 300000 crores from around 213000 crore at present, giving a measly return of around 5% from present levels. Even if you were to buy the stock at half the present levels, the return would be 16%

Again 30 PE for a growing and established retailer in just 7 years from now, when india is still an early developing nation…how are you arriving at sometimes 15 PE today and 30 PE in 2028? Would be good to know logic as you are bewaring…

Not just the maths, I think the confluence of many factors including credibility of the promoters, the strong business model, the predictable of earnings, the huge growth the country presents in the coming decades etc are making the PE reach exorbitant heights, it may remain elevated and undergoes a time correction or it may scale new highs, I don’t know.

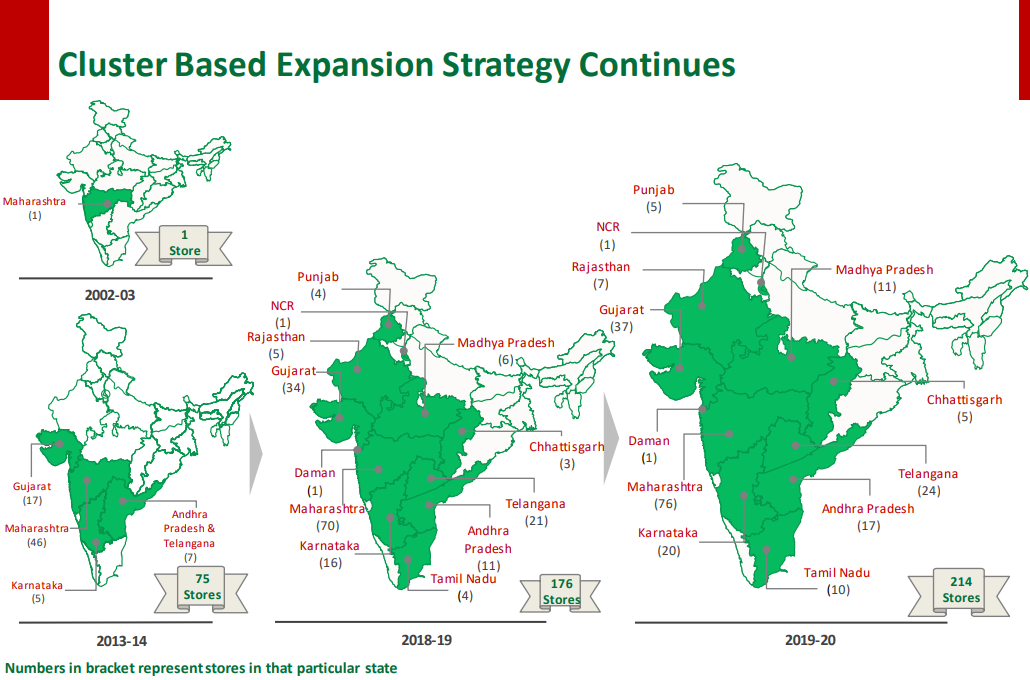

It has presence in only 11 states, mostly concentrated in west and south and it is yet to enter the other regions and states, will they face any difficulties in these regions and states need to be seen, as each state present different challenges which may be new to the management. It is already started facing stiff competition from the likes of Reliance and others but as the addressable market is huge, it will thrive.

People who still have the time or the liking to buy things from physical stores will always exist and the brick and mortar will not go away completely and in the difficult times of rising unemployment, people will be more cautious of the price.

And as Dmart’s online presence also looks good and if need be, the management may concentrate more on their online business. The reviews Dmart Ready app it is getting from the women folk is very good which only means the online platform is successful and is reaching the primary targeted segment.

As per the screener, there are only 13 companies in the country having profit above 10000 crores. Leaving aside a cyclical stock, the highest PE given by the market for these companies is 35.

As and when the profits get larger, the PE has to come down. For elephants, 15-20 is the safe bet PE, while 30 is a bull market PE. Growing 29% from a higher base without making mistakes is a difficult assumption.

All over world retail gets very high PE. If business model starts to fail, stocks are dead. Even struggling companies are given long rope. Here we have company with impeccable business model . It deserves long rope. Opportunity size is very huge, we can not guess. To capture this opportunity, management has to come with QIP time to time like Bajaj finance and HDFC Bank. Every time they come with QIP , rerating is done. I think, opportunity size dictates everything. One cannot cap profits at 10000 cr for Dmart model. It is anybody’s guess. It depends, how management can transform it’s processes, procedures to be able to grow continuously beyond 10000 cr profit company. Yes, opportunity is there to grow beyond 10000 cr profits. Saturated companies with strong moat are still growing at 10-15% in India like Titan, Asian Paints, Kotak etc. See the PE ratio. PE predicts the runway for growth. It looks these companies.have no end to growth in next 20+ years. Here Dmart is 35-40% grower, it depends how much they could execute in particular year.

Execution capabilities are increasing for Dmart, we can expect growth little faster. They don’t have dearth of money to grow, it all depends on execution capability.

For vast opportunity size companies, market can not value company in present price. This has been proven in case of Asian Paints, HDFC Bank etc. Otherwise these companies were trading always at high PE then why are they still compounding at high rate ? They should appreciate like bond, right ? Titan would have got Rs1 lac cr market cap in 2005, right ? But market does not work like this. Gurus have written a lot on this subject. They say market cannot imaginate or calculate future for consistent growing companies. Excel sheets will give infinite value.

In 1995, Tata steel touched 500cr annual sales. This was the highest ever achieved sales at that time for Indian companies. It was made a big event by media. It was discussed on tea stalls all over India. Now 500cr is what ? This is micro cap.

In Dec20 company earned 450 cr profits.Businesses were still having COVID effect. More than 2 years old 160 stores were running at 96% of previous year. Now consider 100% and add inflation if not SSR and try to guess how much profits could be made if No Corona. Now consider company has 4000 cr in bank it amassed through QIP. Company has retained profits too. Now consider that company has established itself in last 3 years as crowd puller. Builder community is desperate to offer to Dmart in their new Mega Mall. Now try to calculate profits for 21-22 Fy and derive present PE.

You will find that Stock is trading at less PE than median. Now imagine how fast Dmart can grow. We have to guess in stock market.

For me price is just number, I am more interested to listen management what problems they are facing to execute. I am very long term investor here.

i. According to CEO Neville Noronha, the current level EBITDA margin of ~8.6% is high and there is no scope for further improvement if DMart plans to maintain its price leadership while competing with online and offline retailers.

ii. Same-store sales growth (SSSG) has consistently declined from 26% in FY14 to 10.9% in FY20, even after extending operating hours of stores by 2-3 hours – mainly driven by lower incremental revenue growth from stores older than five years.

iii.While demand in older geographies have almost reached a saturation point, DMart has been unable to find attractive catchment areas in new geographies ahead of its competitors. Couples with escalating real estate costs, this has led to increased operating cost.

iv.As DMart has expanded to poorer states in terms of per capita GDP, it has failed to replicate historical throughput rates – one of the primary reasons it still has zero stores in eastern India

v.While DMart had created DMart Ready in 2016 to provide an omnichannel experience, a narrow focus on profitability, operations restricted to only Mumbai, relatively high delivery charges and absence of same day deliveries have prevented it from taking off. DMart Ready had sales of only Rs 354 crore with a net loss of 57% in FY20.

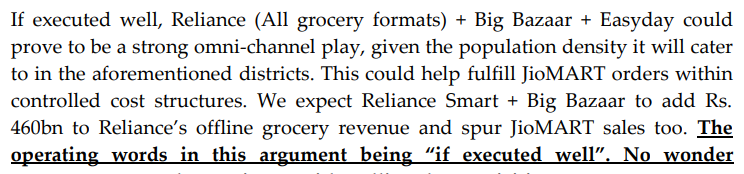

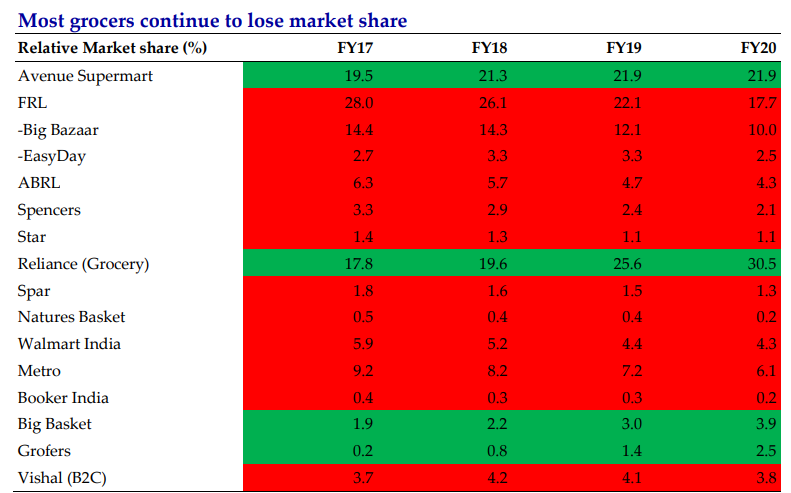

And then there’s the fact that Reliance has decided to focus on DMart’s turf. With deep pockets, a much larger footprint throughout India with 797 stores, fast growth in grocery segment and a strong omni channel presence through JioMart, Reliance Retail has already captured 29.4% of India’s organised grocery market, ahead of DMart’s 23.1%. COVID notwithstanding, will DMart’s conservative approach be able to persist against Reliance’s sky high ambitions? Only time will tell.

SSR is always for new stores. Now Dmart is established brand. From the day one sale starts from peak. So it is better not to consider SSR. Only revenue per bill and inflation is to be counted. This is reflected in SSR. As India grows, revenue per bill will increase.

Most F&G retailers while improving on inventory management, haven’t been passing on the savings to vendors (as DMART does). This is primarily as most can’t afford to accentuate their cash burn further. - HDFC Sec

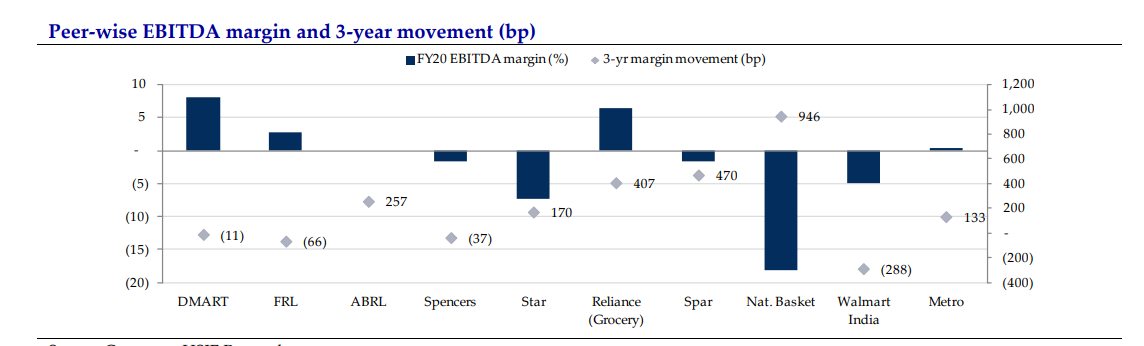

Its operating margin has actually increased (also as a % to expenses its expense heads has remained the same). OPM in 2012 6% and in 2020 9%.

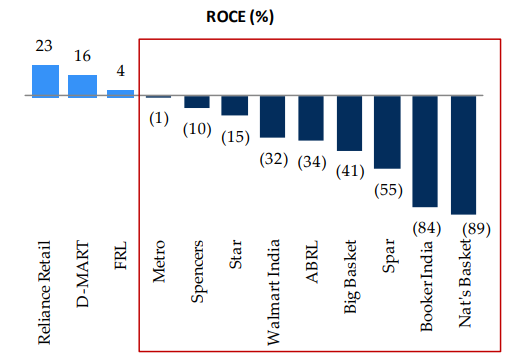

Market share is not deteriorated for Dmart. As a recent report says “Reliance + Future Retail > DMART in store density: Post integration and, if executed well, the Reliance Retail + FRL store network is likely to get nearly

as dense as DMART’s …” Operative word is ‘if’.

Also its a cluster based approach and perhaps rightly so to go after where the juice is worth the squeeze

Do compare across likes here. For instance Avenue Supermart: a compounding machine? - #1239 by deevee

Dmart ready is there in Ahmedabad, Bangalore and Hyderabad also. With plans for more cities and pin codes. Its a soft launch and rightly so. They have 2 fulfillment centers also now.

Reliance had turned bigger even after 12-18 months of IPO of Dmart. That is not a new fact. Though Dmart is holding onto its market share but looks on a shaky wicket.

Is it important to grab only market share ?

Reliance jio mart is far behind in profitability ratio in comparison with Avenue supermart …can any senior highlight this with numbers?

Yes indeed. Thanks for replying your thoughts. Brother I agree with you but one thing that comes to my mind strongly as I think is that all these big companies that we see now are “old economy” businesses. The new economy - the consumer, retail and other new era businesses are yet to reach that figure. And when they reach that figure, some of these old economy one may make maybe say 50k plus profits…so eventually 10 k would not be that big and also the growth rates of these new era businesses at 10k profits may still be much more than that of these old economy ones today at 10k profits…that’s point one

Point 2 is that if you see example of IT…the behemoth Tcs commanded 15 PE until maybe 2 years back as all learned men in markets (including the not so learned… me) thought that that’s what supposed to be for big companies and expected slow growers etc etc. Today it commands 35 plus PE…and even in bear market few months back it’s PE was always more than past bull market PEs…except the astronomical ones at time of extreme exhuberance in 2000 (not of TCS per se but other IT companies). Point is…as big gets bigger, the PE may not always contract as expected. Markets have unique ways of making us learn that do not underestimate the power of good businesses and ethical businesses…but yes agree avoid exhuberance…

Disc. Invested in Dmart and other high PE stocks therefore biased. Not a buy/sell recommendation. Just personal thoughts on consistently high PE companies and I can be completely wrong in my assessment.

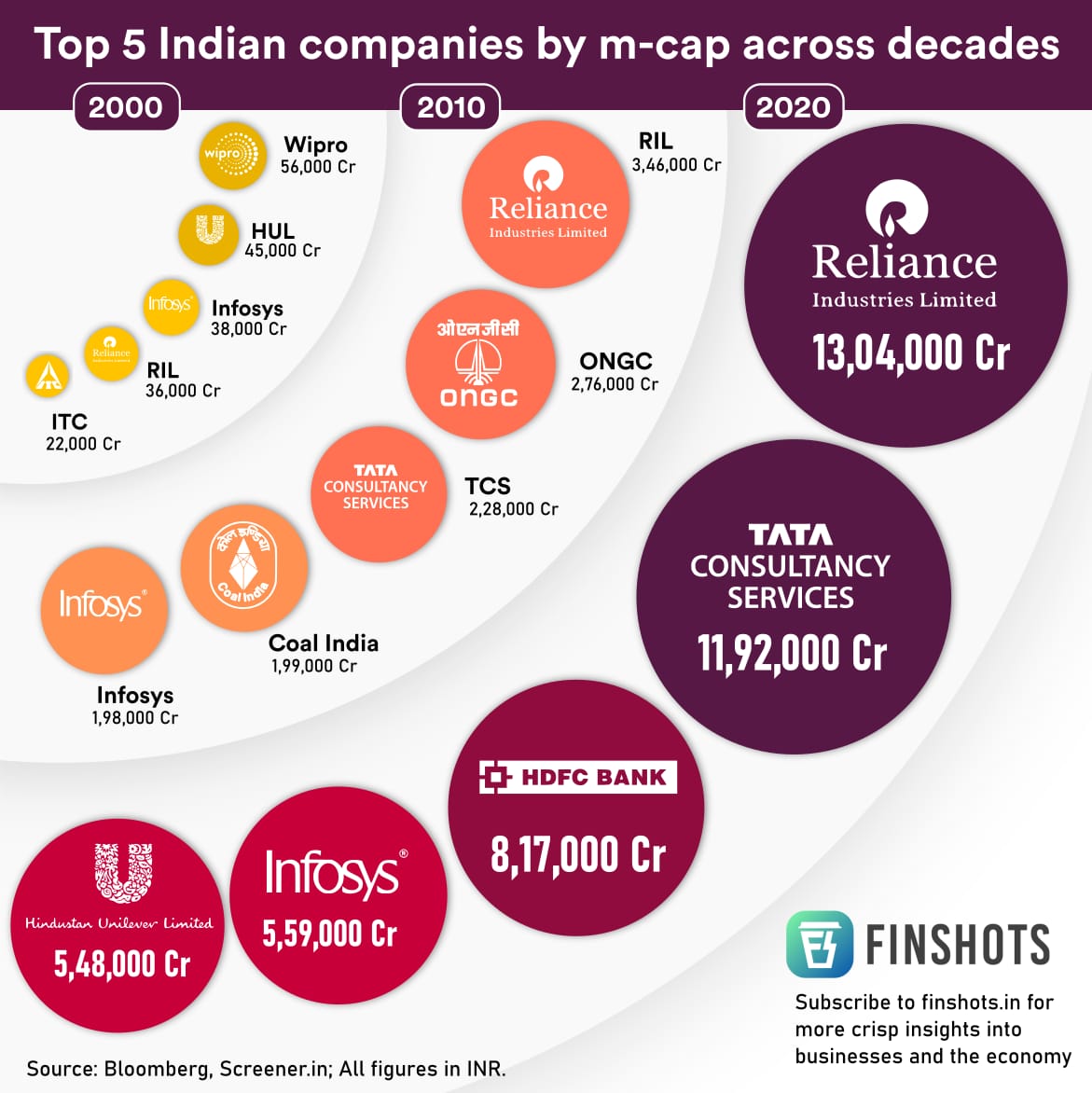

Another way to look at this finshot is only companies that have shown real growth, their share price has eventually caught up. In other words, only companies that have shown growth have actually survived in the top 5/10. (RIL, Infy are consistently across all 3 spaces and few more have occurred twice)

Back in the IT boom days, Infosys, Wipro showed considerable profits and market rewarded their share price accordingly. This continued with Coal India,and ONGC making profits and their share price playing catchup. Right now HDFC, TCS alongwith RIL show considerable profits and that is why they command a higher Mcap.

The key is in finding the next big companies. Just imagine what this chart would look at in 2025, 2030, 2040 etc. My guess is with a booming economy, booming stock market and ‘India Shining continously’ by 2030, RIL & TCS could probably be at 22-20 lac cr and we could have DMart at around 10-12 lac cr or may be a bit more. Whichever way you look at it, I think it would be in top 5 companies by MCap by 2030. Dmart in 2020 is comparable to TCS’s Mcap from 2010.

(I am not even going into the PE debate…Just giving a view of sales/profit growth vs. mcap)

Apart from their business model, my reasons for the belief in their growth are 1. It is actually in a Real estate business spread across the country and this asset is always appreciating. Companies holding huge pockets of limited assets (land) will always be richly valued 2. Debt Free (okay very minimal debt) and doesn’t look like this will change 3. I have personally seen DMart customers swear by it’s loyalty. In the business of retailing, customer loyalty is extremely rare and if a company has it, it counts as their moat 4. A lot also relies on execution and the promoters. So far, Mr. Damani although camera shy, but is counted amongst the respectable business leaders (like Kotak, Mahindra etc. and a few more rising stars)

All this is obviously based on extrapolation, assuming the current growth remains and they continue to add stores and increase their footprint considerably across India. In the next few year, they could fund all the expansion using internal accruals which is something that market leaders command

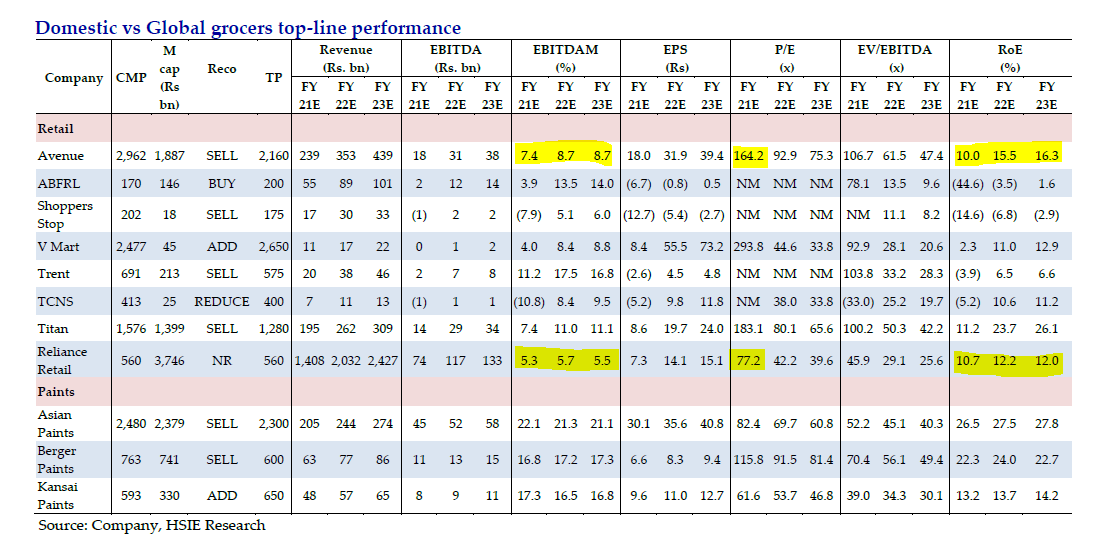

If you notice one thing that HDFC sec which is bullish on Reliance Retail has brought its estimated RoEs down by a significant % from Apr 2020 to Feb 2021. Apr 2020 they said RoE FY21e is ~27% and in Feb 2021 they say 10.7% similarly for FY22e the number has been brought down from ~26% to 12%.

HDFC sec Dmart Jan 2021

HDFC sec has nice coverage of both Reliance Retail and other grocers.

Complete novice here. I’m yet to grasp the significance of investing at low/reasonable PE especially in a growth company like DMart.

Right from the beginning of this thread (4 years ago!) when the price was around ₹500, the concern was high PE. Irrespective of these concerns, DMart kept growing (about 40% CAGR as per screener.in) and still the concern is high PE. People who didn’t bother about high PE 4 years ago would have made 4-6x of their investment! I understand we can’t just pick one instance to justify my ignorance. But I would like to understand what I should consider as reasonable PE and why.

Also I read somewhere that PE shall be comparable only with the peers/sector. However there does not seem to be a profitable peer for DMart to compare with. So it is not clear to me how this high PE is a concern when growth story is intact sofar.

Most of the justifications for high PE here are qualitative. Are there any quantitative justifications that support this valuation or otherwise? (I think there are some quantitative discussions like revenue of 10k cr expected within a decade but I didn’t quite understand how it was arrived at)

screener tells me that the PE at this time is whopping 213. But I think this takes current EPS of about 15 into account. It is possible that the market thinks that this is only COVID EPS and profitability will go up as the situation is normalizing. I think forward PE comes into picture here. So do we still treat the current valuation as very high PE?

I would be grateful for any light on these aspects. Thank you.