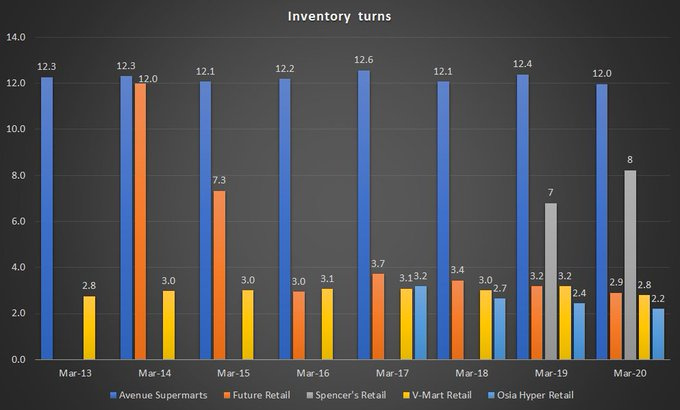

Tweet on Dmart’s high Inventory Turns.

Tweet on Dmart’s high Inventory Turns.

Hi, I am not willing to get into D’mart at current valuations, but here are some questions I hope someone can answer to help me understand more about the business.

1 - The tug of war has always been there between retailers and the brands. Who is winning this tug of war in India? I believe the distribution of power may be rightly gauged at by looking at changes in the slotting fees contribution to D’mart over the years. An increased contribution over the years as a percentage of the same to the total revenue might imply power transfer to retailers in India vs brands and vice versa. Why the revenue breakdown in such categories is not available in annual reports?

2 - What kind of slotting fees is charged across various categories by D’mart for new entrants vs established FMCG giants across various categories?

3 - What percentage commissions do they earn on different consumer categories? In short on what products do they earn the highest commissions and on which ones do they earn the lowest.

4 - What product categories clock the highest volumes along with decent margin that might make them the ones generating highest revenue contribution in a year?

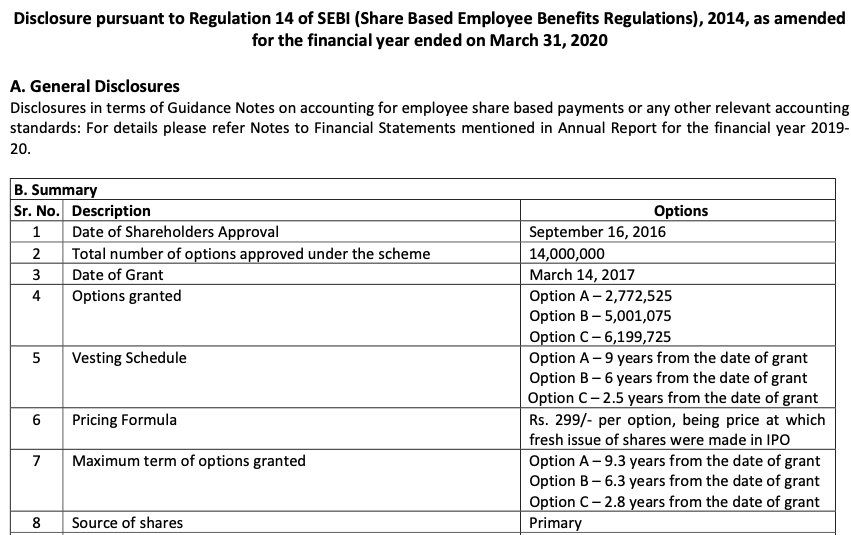

5 - I don’t understand the following. These options are granted in 2016 but allocated in 2019. These options after 9 years may gain 20 times if exercised vs a shareholder who might have bought a share from open market at approx 2000 rupees in 2019 who only might pocket a gain of 3 times. I do understand they were approved in 2016 but what is the procedure to get them approved for when they cross the threshold of 1.4 crores stock options? Will the price be still set at the fair value as they say at 299 or the fair value at the time of consideration? If the PE multiple still remains high, can we ignore the difference that might occur in the pricing of options vs the price of the stock?

Hi

Recent report by CRISIL

Strengths

Strong market position in the organised retail market: ASL’s market position is reinforced by steady same-store growth and retail productivity, and short gestation for new stores. ASL currently operates 220 stores (as on Sept 30, 2020) under the D-Mart brand, which reported healthy same-store sales growth (irrespective of their vintage) of about 10% in fiscal 2020.

Strong procurement abilities, lower priced products along with strong cost control have led to strong footfalls in past. This leads to high inventory turnover and revenue per sq ft and translates into industry leading retail store productivity. Aggregate revenue per square foot at about Rs. 32970 in fiscal 2020, is significantly higher than most retailers in the same segment. The operating profitability of the company had seen improvement over the years though fell to 7.6% in fiscal 2020 due to impact on operations in March 2020 due to COVID. Operating margin to moderate in current fiscal by up to 150 bps on account of sub-optimal fixed cost coverage and restriction on sale of high margin non-food products during Q1FY21.

Currently, ASL’s operations are largely concentrated in West and South India. Expected large cluster focused store addition over next 3 years will benefit to diversify geographic reach of the company. CRISIL believes strong track record of outpacing its peers in growth, its strong merchandising and compelling value proposition, benefit of economies of scale will benefit to strengthen ASL’ market share in organised food and grocery retail in India in the medium term.

Going forward, impact of consolidation in the industry and intensity of competition mainly from online retailers will remain key monitorable.

Solid financial risk profile and healthy liquidity

Financial risk profile is driven by a sizeable net worth (Rs 10973 crore as on March 31, 2020), and strong annual cash generation, despite continuing store addition. The company has been able to maintain healthy operating metrics, while adding stores, and also prepaid debt through proceeds of its QIP in fiscal 2020. This has translated into strong debt protection metrics. In fiscal 2020, the company incurred capex of over Rs 1895 crore and increased the retail space from 5.9 million square feet to 7.8 million square feet.

CRISIL expects ASL’s prudent expansion plan will entail a sizeable increase of about 20% per annum in existing retail space of around 8 million square feet by fiscal 2021. Strong cash generation of around Rs 1300 crore per annum is expected to be sufficient for capital expenditure (capex), resulting in low dependence on external borrowings. Furthermore, liquidity is expected to remain healthy.

Weakness

Susceptibility of operating performance to increasing competition

Consolidation in the industry will increase bargaining power of ASL’s competitors in the brick and mortar retail which may impact gross margins of the company in near to medium term.

The competitive intensity is also increasing due to increasing focus of e-retailers in the F&G space. While ASL is a small player at present in the online F&G space, other major players such as BigBasket and Grofers and new entrants such as Jio mart are registering aggressive growth. Though, currently e-retail is a small proportion of overall retail it will remain key monitorable over the medium term.

Rgds

Disc: Continue to be invested

Can anybody tell me that in states like Maharashtra, Gujarat , Telangana where DMART has presence are people going to stores directly?

My personal opinion if DMART expands its store in non-metro regions their business will prosper more because people want to go out as there is no issue of traffic or pollution in general compared to cities like Mumbai, Bangalore etc where online can prosper.

What are your opinion on this and does anybody has any idea in future where DMART is planning to more stores- metro or non-metro?

Dmart broadly has 3 delivery models

a) In store sales

b) Online sales and home delivery

c) Online sales and go and collect offline

When share prices were sluggish around the 2000-2100 mark for long, i decided to myself check out option a at Thane, a suburb of Mumbai. This was couple of weeks before Diwali. As usual I was greeted with the parking full board. Once I managed to get into the store it was buzzing as usual. I thought people must be stocking up for Diwali and hence did a revisit a week after Diwali and the result was not too different and I got some assurance that they are back in the game.

I see daily delivery by dmart in my housing complex under option b right from 8 AM

I have also tried option c. The collection outlet nearer to my house usually had one or 2 customers in Q. But the last time I went there were 6 customers waiting to collect deliveries.

Though online continues to be the preferred choice in this pandemic era, there is very little doubt in my mind that loyal dmart customers are shying away.

This is a very good & a detailed information provided by you, can anybody else also post his observation if they have visited Dmart store in the near-term. One thing I am not able to understand, where does dmart plan to open its store, is it the metro or non-metro regions. Depending on where the company opens its store, will provide a future trajectory to the growth of the company?

We have consistently seen a negative Free Cash Flow (FCF) since inception. Does that make you uncomfortable?

Actually, I’d rather they generate negative FCF for the next 10-20 years.

They’re a best in class player in an underpenetrated market, why should they generate free cash, they should reinvest everything they generate and more (via leases and equity raises) into their business.

The number you should be looking at is a no-growth, steady-state free cash to equity holders

= Cash from Ops - Interest Expense - Maintenance Capex

On which they are very profitable.

While keeping in mind the very lofty valuations, the Nick Sleep framework of Scale Economics Shared can also be applied to Dmart.

The idea is that businesses that share the benefit of scale (economics of scale) with the customers build the sort of customer loyalty that ensure these customers (due to the value proposition) come back and spend more money, in turn driving more scale benefits. And this becomes a virtuous cycle.

I think on one of the last 2 quarters Earnings calls, the CEO mentioned that they’re not going to focus on increasing the gross margins anymore, they’ve reached the peak. This suggests the scale economics shared argument.

Furthermore, if there’s 25%+ compounding in the earnings, and that engine sort of continues, even if the multiple falls to a more sensible (relatively) 50x, share price appreciation will be pretty good.

Just before the Q3 results one of their store is seized in Hyderabad for selling poor quality of material. I know that they will reopen the store in few days but such incident is not good for Dmart Brand

This is not first incident involving D Mart in Hyderabad. D Mart has expanded well in Hyderabad and stores are usually crowded. The perception has been quality with good and honest discounts as far as groceries are concerned. Periodic incidents of store closures will dent such image. They need to be more careful.

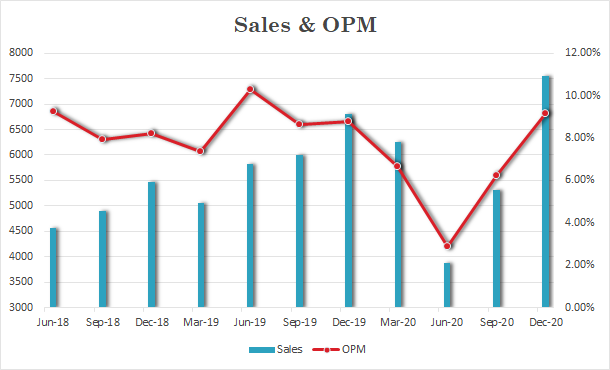

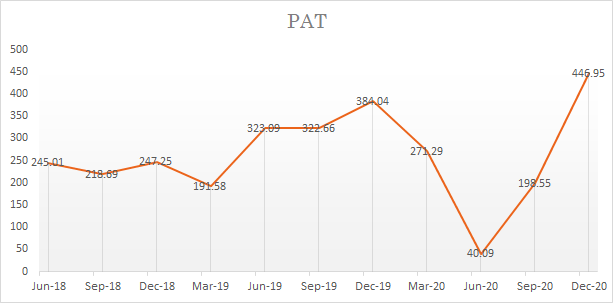

DMART Q3FY21 EPS Rs. 6.9 vs Rs. 6.14 YoY (Rs. 3.07 QoQ)

Cons. Revenues up ~ 11% YoY!

Cons. PAT up ~ 17% YoY!

Cons. EBITDA Margins at 9.1% vs 8.8% YoY!

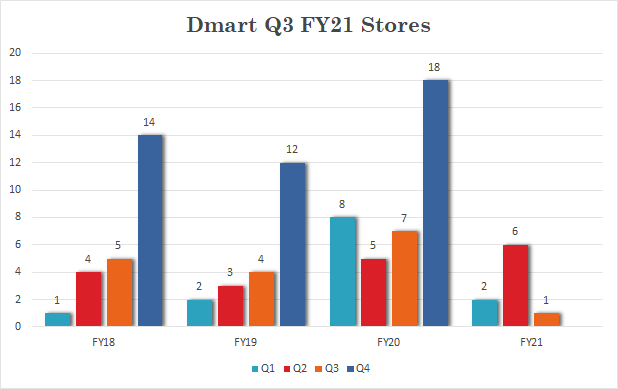

9 stores were added in 9MFY21, 2 were closed & converted into Fulfillment Center for E-commerce buisness.

Even with 2500 cr annual profit say in FY22 or FY23 its at very expensive valuation. Is it bubble or something unseen which I am not aware.

Do any one have comparison between Dmart and Reliance Retail?

Hi

Quickly went through the results. Pasting some pointers from the commentary.

Store opened was mere 1.

Sales & PAT were highest ever I think. If somebody can corroborate that data point.

OPM crossed previous Dec 2019 and also highest since then. Still the old stores as said in the commentary are not doing as well as that in Dec 2019.

And offcourse valuations the whole investing world is divided on this one ![]()

Let us see how it goes.

Rgds

Deepak

Disc: continue to be invested.

Majority of investors have a complaint with Avenue Supermart is that it’s so overvalued and running at PE multiples of 120+ and at times 200+ (like nowadays). One thing is well proven in the markets is that a stock’s price and PE is always a function of market’s perception about it. Higher the confidence in the company’s growth, higher the price/PE.

This reminded me of a comment from @hitesh2710 in which he explains why some high quality businesses remain at elevated multiples for a long time. And I think his explanation suitably applies to Dmart as well.

Regarding valuing companies like Asian Paints, pidilite and page inds, one needs to take into account the kind of longevity of growth these companies have. Some studies done my Motilal Wealth Creation studies indicate that if the company is a high quality, less prone to disruption and isnt exposed to too many variables and has a very long runway for growth, then over a pretty long period of time say 10 plus years, the price at which the stock is bought might not mean much and the investment will yield very good returns. I think the coffee can investing also stresses on the same points.

On how to buy these companies the ideal way is to go ahead in a SIP kind of method If one is buying for 10 plus years then I think the buying also has to be done on an extended timeframe.

Key remains in buying the right companies and not going by companies currently in vogue and hence market favorites. One has to see long term history of these companies of how they have fared over good and bad times and then take a call. Usually the companies that qualify in these lists would be dominant market leaders in their segments and the opportunity size in the sector is big and growing as the years go by. These need to have top class managements, great balance sheets and excellent financial ratios.

These companies will always fail the PEG test as these are well discovered companies and there is nothing unknown about them. Over a long time period even the minimal variables in these business tend to equalise. e.g in case of asian paints crude price is important and it tends to go up and down but over a longer time period these things tend to normalise.

The other option to buy is to buy them during market meltdowns when during the final phases of market corrections these too correct and one needs to have courage and conviction and money to buy these type of companies.

The lack of free cash flow is a big drawback for defensive investors for investing in this company at such high valuations. And why no free cash flow for not even a single year?

Even Walmart had occasional free cash flows in the beginning, but then the market never gave it such high PEs even though it was expanding rapidly adding atleast 100 stores per year.

And Dmart can never be compared with high PE companies like Nestle, Asian paints or Pidilite, which have better ROCEs and regular free cash flow.

Of course there is the logic, that the company is in the growth stage and the free cash flow will come when the growth slows down. But then it should be known that there is the possibility that expenses may be getting capitalised, and you have to trust the management, regarding the true profits.

Food & Grocery sector report from HDFC securities - DMART Vs peer comparison.

Analysis of HDFC Securities (shared here) compared DMart with most retailers including Reliance Retail.

This report also includes the case study of Grofers and how the heat is being felt by offline grocers.

Yes, many investors do get skeptical every now and then while contemplating an investment in Dmart. Mostly due to the higher valuations of Dmart in terms of PE multiple, which has always been on the higher side ever since it got listed :

Nothing new in that. This has always been the case with the companies clicking up exceptional growth over a period of time. Because profitable businesses are less risky than unprofitable ones. So, an apt consideration of revenue growth & net profit margin in the last few years (which helps in drawing an informed view on the sustainability of the profit growth) can suffice that argument for Dmart.

Having said that, sometimes statutory profit levels are not the only guide for gauging the long-term moat in the business. There should be some qualitative inferences to buy a company that tells a good story to investors. Dmart do come up with such a story that can possibly be the distinguishing factor that separates it from its peers. There are some qualitative aspects that stands out over a long term , those that can’t be described in numbers: