Quarterly results analysis

1 Like

Hi

DMart is not looking at bulk customer. There is no Lower limit for purchase. Billing is very fast.

More people buy more bargaining power of D mart with vendors

Is there anyone here who has visited both DMart and Reliance Market? If yes, could you share some comparisons in prices, product range, service etc. RM is currently small with few stores but could give good competition in the future.

I have visited both and both these are at a radius of less than 2KM from my house. I do go to Reliance once in a while. Initially they used to have decent merchandise. Now it is so so. Probably the response is not as expected. Honestly I do not care about Reliance Retail stores.

Yesterday was a festival in Mumbai and I thought will go to DMart because people will be celebrating and not necessarily shopping. How I was proved wrong. DMart store was full to the hilt. It is no fun josling with 1000 shoppers in that large yet jam packed place. We picked up what we needed for about Rs.7K. We did not get about 10 items which we needed but the store ran out those. There was some issue with the integration between POS terminal and card swipe. It got resolved in less than 5 minutes unlike other stores where we go into a rut sometimes.

We came to Reliance for those items which we did not get in DMART. The number of shoppers were about 1/20th of what we saw in DMart. The baskets were much smaller. The bills were much lower in value. No comparison. My daughters said we dont feel like buying from Reliance. Anyway that is immaterial.

So Reliance is the first mover, opening up the markets for DMart to come with their precision and efficiency. I bought some more shares in Avenue today morning.

Disclosure - Have invested in the stock.

20 Likes

There is an undocumented rule.Where there is a D-mart, the chances of survival of any other similar grocery store within 2 kms radius is minimal.And I have observed it myself in Thane,Mumbai.

There were earlier More,Reliance stores but they had to change their location or either close the shutters because they could not cope up with DMart.

Apart from the product quality,D-Mart carries few SKUs which are fast running; thus the unsold inventory is minimal. The billing turnaround in DMart is exceptionally fast compared to Reliance.

In Reliance, I have been to their few stores, but never found the sense of ownership amongst floor sales persons as well as managers.The waiting time on billing counter was very disappointing.

I think we have to look at the retail space holistically rather than just comparing with Reliance market.

With ecommerce in full swing and gifting bulky discounts on the cart value, in the short term, there is some customer churn for DMart specially in metros.But this wild distribution of money will not last very long.A business that does not run on the green bottomline is sure a recipe for disaster sooner or later.

And we are seeing that now. Paytm mall was very aggressive in giving cashback to the tune of 25 to 40% few months back.Now its no longer there.The customers are super smart.There was a drop in 90% sales once offers dried. Now it is having a deserted look. Paytm recently said they want to focus on their core business.

Same is now happening with the likes of Big Basket and Grofers. I can sense that they are in the path of Paytm mall. Only the exception is Amazon Pantry(which will last ever and thats the only competition with DMart)

So, net net I find a bright future for our company.

Disclosure: D-Mart is a good % of my portfolio

17 Likes

It is a superior business. This is indisputable.

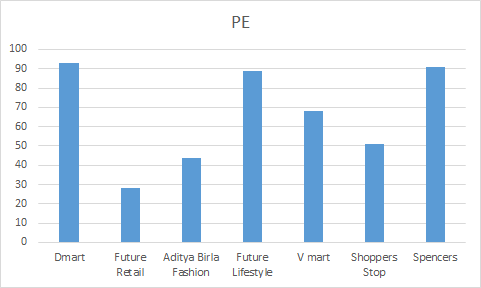

But, what about the stock. It is currently available at 110 PE. What kind of returns should a retail investor be expecting by investing at these rates.

I am unable to decide. Because, in the past, a select few stocks have been able to deliver returns if bought expensive.

3 Likes

I did not say DMart is looking at looking at bulk customers. However, in Bangalore the DMart I visited is not in a prime location. Traveling a long distance to buy 500 bucks of grocery is not worth it in my humble opinion. Also, as I said not everything is ultra cheap, a lot of the items are at the same prices that a More or an online retailer will give.

I believe they are pretty profit conscious too ( and rightly so ) and might be balancing prime locations with few non prime ones to keep cost under control . Moreover there would definitely be other factors too like sq feet area of store etc which they would take into consideration eg larger stores , they can start with more categories of items apart from the usual ones . They might be planning to have larger stores in non prime locations or these might be " to be developed areas " where real estate is cheaper to own or rent .

Their ability to grow rationally and not haphazardly is further displayed from extract from agm notes shared by @bheeshma

Thanks so much for sharing agm notes @bheeshma

Disc - Invested . I am not a sebi registered analyst and this is not a recommendation. Pls do your own due diligence before investing

3 Likes

Hi @hack2abi

Reliance Market is a different format as it is a warehouse wholesale cash and carry store servicing registered members and targeting traders, retailers, restaurants etc on the lines of Best Price stores in India (however normal customers can also buy). These types of formats are generally situated some distance away from the main city and are like 75000-1Lac+ sqft in size. Wholesale Cash and Carry as a format has not done as well in india compared to its retail counterparts.

Reliance however remains well positioned with many different formats in place like Reliance Fresh, Retail, Market and a plethora of category specific formats in shoes, electronics, jewelery etc. The Reliance industries group also has proven itself multiple times on the execution front and once they do their planning they execute those plans with precision where many retailers tend to falter. Big plans but half hearted execution. All reliance formats are certainly a threat but so far there is no format that is every day value at the scale Dmart operates at.

5 Likes

I haven’t seen any Dmart open and then close down. Probably there are but never seen one in the places I know of. I’ve seen reliance close stores. I’ve seen big bazaar close stores and and every other retailer. Never DMART.

Does that mean anything for reliance? Probably not. Does that mean anything for DMART. Definitely. It shows how meticulously they have planned their store locations. I might be biased but DMART has captured the mind space of shoppers. People assume they are the best.

As for reliance their advantage is the ability to throw money, loads of it at a problem. But sitting at a net debt of 200,000 crores can they afford to throw vast amounts of cash at problems? If so why are they talking of being a zero debt company in 18 months?

I think reliance will continue to do well over a period of time. But hopefully we will get into a level playing field where reliance will not need to depend on the support of government and regulatory bodies to compete with the others. It will be good for the society if that happens.

3 Likes

Hi

I agree with you. I don’t think most of the people on the forum or outside have any reasoning as to why Dmart is an average or inferior business. But when its a question of valuation we have clearly defined two sets of people. The first set justifies that its worth paying 90 times earnings and the second thinks the first set are fools, haven’t they read Graham.

So I try to avoid this stock specific valuation discussion. I like looking into some history. It wont repeat as they say it will rhyme.

Walmart listed in 1970 at $16.50 with 200,000 shares outstanding. In 1971 they had an EPS of $0.3 and in $0.47 in 1972. The stock split and both in 1971 and 1972. Both the years in December the closing price was roughly $45-$50 a share. The PE was 150+ in 1971 and 100 in 1972. The peak PE in 2018 was roughly 60 still for Walmart I believe and is now 23 (forward in the 20s)

Now this is survivorship bias. But lets see what the future holds. At the end there will always be regret in the both the above two sets of people - first one will say I should have added more or I shouldn’t have bought any and the second set will be I should have bought or could have I shorted somehow if I was so sure.

Thanks & regards

9 Likes

Walmart’s business model was new for its time and hence had very little competition. Due to which it could press upon its suppliers, from world over, for low-cost good quality, and sell at a handsome profit to not so price conscious Americans. It sold everything from small packs of milk, baseball bats, fertilizers to construction material and guns. Dmart is nothing quite like it.

Other disadvantages of Dmart.

-

Its customers are lower/middle class for whom price is most important. Therefore Dmart does not get pricing premium. Just quantity discount due to bulk purchase.

-

Dmart has healthy competition from

a. Local Kiranas, who are really smart people themselves. Their purchasing power is no less compared to Dmart. In my locality, local Kiranas are usually packed at certain hours during the day.

b. Online retailing is giving Dmart, if nothing more but a temporary hitch. -

Dmart needs real-estate to grow, which is expensive. It could rent, but yet getting space in prime locations is expensive. Walmarts are huge warehouses, located at outskirts of a town, with never-ending parking space, acquired at low cost and managed by fewer people per square feet.

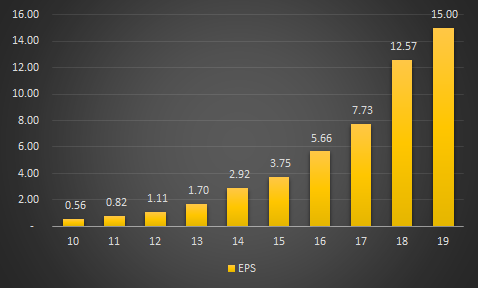

Point is, in case of DMART the demand is absorbed by competition and the basic requirement for expansion is real estate is expensive. Therefore, I think the management will be hard pressed for growth sooner than the investors at 110PE imagine. This might be the reason why its TTM EPS is showing negative growth. Something to worry about for 110PE stock.

And given the harsh economic environment, paying 110PE is a tough call.

I am ignoring:

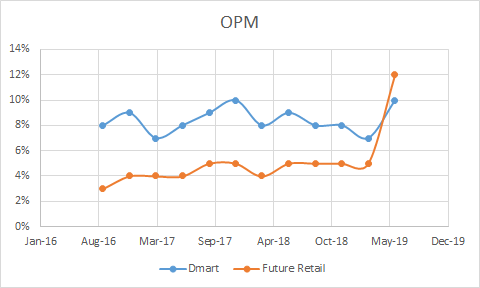

a. Low OPM%

b. No Free Cash Flow, hence a possibility of increasing debt which is the case for most companies which are on a strong growth path but require a lot of money to grow and hence cannot do it organically.

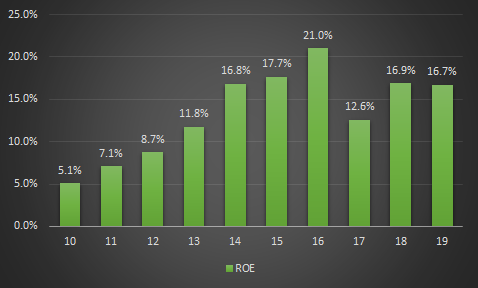

c. Ok-ish ROE

Because I am not really a numbers guy.

8 Likes

There is a Dmart near my house which gives 6% off. To compete with it, a local chain called Grace has started giving 10% discount on all items. Another advantage over Dmart is the availability of vegetables. Customer always wins!

2 Likes

Rating Agencies keep on upgrading trust level on D’Mart.

Credit Rating Agency, CRISIL Limited, has assigned its “CRISIL AA+/Stable” (pronounced as CRISIL double A Plus rating with Stable outlook) for Non-Convertible Debentures of Rs. 200 crore of the Company.

In earlier assessment during March’2019, they had assigned CRISIL AA for Non-Convertible Debentures of Rs. 416 crore.

Finance experts : Do we see such upgrade based on amount as well? I see this rating is for NCD of 200 Cr, while earlier was for 416 Cr & prior to that was for 800 Cr. So rating is upgrading with reduced amount.

5c1bb217-89b6-4eaa-89d1-2cd03658276c.pdf (543.8 KB)

1 Like

Hey

My point of using Walmart was to showcase historically that people paid up in excess in past for a business and then we had statements like 'If you had invested in Walmart 100 shares druing IPO you would have…" you can complete the rest . In other cases we thanked the stars we didnt invest in some solar business etc.

I am using it as an example and not comparing businesses.

Anyways.

Some of the inferences on the numbers you have made are misplaced.

OPM:

Dmart has one of the best operating margins. Infact it has better margins than Walmart has ever had (not that we are comparing here). Walmart since IPO has never touched 8% I believe.

PE:

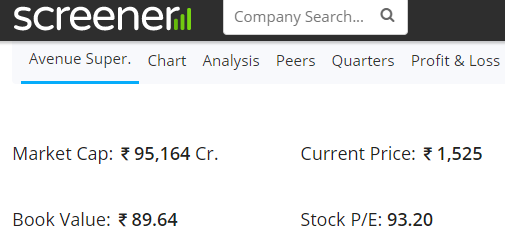

Not sure how have you calculated 110 PE. Screener says 93.xx. Not that 90 vs 110 has anything a lot different.

EPS:

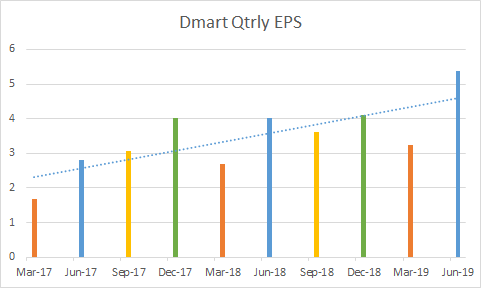

Negative growth? There is not one quarter in the last one year in which EPS is lower than the quarter of the previous year’s.

FCF:

I see positive cash flows for Dmart in my calculations. I use the following formula

FCF = NOPLAT *(1- (NOPLAT Growth/ROIC))

More here VP CHINTAN BAITHAK GOA 2017 : Bheeshma Sanghani : INVESTMENT JOURNEY/PHILOSOPHY - #13 by deevee

Aside its negative for Future Retail for instance.

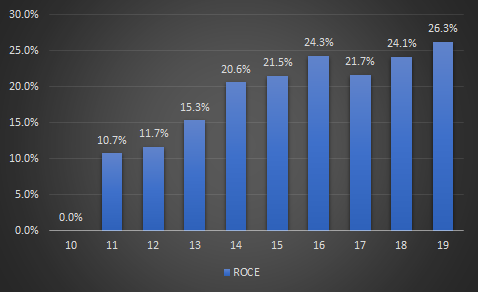

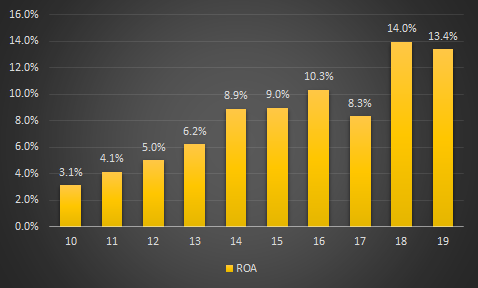

ROE ROCE ROA:

They seem quite appreciable infact.

Aside competition in India is not consistent on these metrics. Walmart though not comparable had 15 years of over 30% ROE. Also they had like over 30% ROE in their initial years.

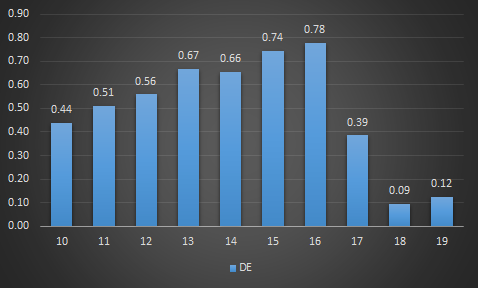

Debt:

Dmart is good here too. A Future Retail has 0.7 DE.

Rgds

20 Likes

Actually that is a wrong way of looking at things. At DMart the minimum discount is 6%. But on many things I’ll get much more. I got a container of muesli for a discount of Rs. 120 like 30% off. Ghee for a discount of 100, like 20% off. In detergents you get 200 off for a 4+2 kg box.

Even if a grocery shop gives me 10% on MRP it will be much less than what I get from DMart. In fact the MRP is not even a consideration for me when I shop from DMart.

In Saffola gold I got Rs.20 off on a Rs. 150 pack. I usually get deodorant at 50% discount. So Dmart discounts can range from 6% at the minimum to 50%.

4 Likes

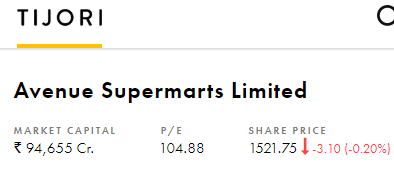

Don’t want to jump into & divert the discussion but I have heard lot of debate on high PE. Refer below snippets from different sources (tijori & screener) surprisingly there is huge difference (& yes these are captured just now). Is it that screener adjusts it for quarters & Tijori adjusts it on annual basis? need to play with the numbers ![]()

No doubt that its on higher end but do we (read so called analysts) use them based on their convenience as most of the retail investors consume the data presented and don’t go inside for minute details.

Having said this EPS is inching northwards & prices remaining stagnant for almost a year… PE has cooled down.

Wish we start discussing valuation from other perspectives.

1 Like

That is what I meant when I said:

I am ignoring:

a. Low OPM%

b. No Free Cash Flow, hence a possibility of increasing debt which is the case for most companies which are on a strong growth path but require a lot of money to grow and hence cannot do it organically.

c. Ok-ish ROEBecause I am not really a numbers guy

I only wanted to bring avid investors’ attention towards the fact that good businesses are sometimes bad equities as they are acquired at top prices, which imply high growth rate, which is often difficult to meet.

Dmart is there in 1) Electronic City, 2) Hongasandra/Bomanhalli 3) Extreme end of Bannerghatta Road 4) Whitefield [Nothing in North & Central Bengaluru]

Costco also follows the same model; on the max. 3 private brands [own or outside]

What I have experienced - they stack up the products keeping in mind the local crowd [not whole city]

Initially, before 6-7 years, I found vegetables with them but they have stopped it. [Source: I used and shopped from 6-7 stores of Dmart in Ahmedabad and Bengaluru]

Avenue’s profits for Jun quarter are Rs 335 crores. Just for the purpose of calculation if we multiply it by 4 without considering any growth, annual profits come 1340 crores.

ROE = 1340÷5594=23.95℅,

PE = 95164÷1340= 71.

If you consider growth, moat in business, in September 2020 no one will say that Avenue is costly if the share price is same. We forget that Avenue share price has not increased for one year and so PE is contracted. ROE is improved a lot. Time is very important iin Market. I consider it a super compounder from here.

Disclosure-I have been investing continuously for one year in this scrip. Now it is big portion of my portfolio.

4 Likes