If we look at from market cap perspective the top companies are TCS, Reliance, HDFC and they are in range of 6-8 lac crores. With 1 lac crore DMart doesn’t offer multibagger opportunity (at least for me)

3 Likes

“With 1 lac crore DMart doesn’t offer multibagger opportunity (at least for me)”

It depends person to person. Each investor has different investment approach and different goals/expectations from market. For people who are happy with 15-20-25% CAGR safely for next 10-15 years, Avenue is sure shot multibagger. For others who want more, even HDFC Bank is not investment worthy.

Time will teach to revisit investment thesis for many.

8 Likes

Nice read…may be somewhere I can relate American Costco of 1980’s to Indian Dmart of 2019’s.

Some aspects which don’t get discussed much

- Apart from being very good in business execution, promoters are best stock market operators (not in a negative sense) this country has.

- During IPO, much was left on table for retail investors but within months stock tripled. Hoping just coincidence.

- Last stake dilution was as seamless without price movement that it was almost breathtaking

- As long as this stock is closely held with such high promoter stake, it is pointless to discuss stock behavior.

Coming to business metrics, highly probable this good business will continue to remain so. It is good entirely because of their execution skills in an otherwise brutal business. Don’t see how execution will deteriorate

5 Likes

If it was possible to make 25% cagr or more for a long time, most investors will be billionaires. Unfortunately getting even 15% cagr is not easy in the long term. Less than 1% of investors may be able to make 20%+ cagr and they are God.

7 Likes

For some valuation related inputs one can refer to raja iyers detailed comments about dmart in particular and his way of looking at valuations in general. According to him market is perhaps valuing other sources of revenue for dmart at 45k cr . He is profiled in the book masterclass and one can also read his excerpt for free on the website of the authors of masterclass.

Ofc one is encouraged to arrive at dmarts value independtly using whichever framework that is appealing. Earlier I used to think that valuation could be derived numerically by using financial statements but over time I have realised it’s more of an art rather than science. With experience I guess seasoned investors can Intuit whether something is cheap or expensive. In my interactions offline with some of them I have seen no one use DCF. Raja iyers simple way if looking at valuation has given me food for thought and I use it now to triangulate my own calculations.

On the other hand some ppl I know in institutions use DCF extensively and it’s part of the process of valuation. However they have extensive data available to them from different industries over time and their assumptions all have some detailed reasoning. These are not available to us to formulate assumptions.

What I do know now is that this valuation business rests on some key assumptions. Whether one intuits it using experience and knowledge or bases it on datasets , the quality of your assumptions is what seems to differentiate a good investment from a not so good one

17 Likes

To add to your point, DCF is like a hubble telescope: a fraction here and there, your entire outcome goes for a toss.Businesses are so volatile and bound with so many intangible factors that its impossible to quantify the future growth for the next 5/10 years.

Lets not go too far; in August 2018, auto sector was growing tremendously, maruti was on the cusp of touching 10000 value; who would have thought in the next 4 mths(by Nov/Dec 2018), its a complete reversal of fortunes.

You are right,most of these folks have a great intuition.

Ramesh Damani said about RK Damani that he could smell which side the market is going to behave.Such was his sense of the market.And he never used DCF etc.

12 Likes

Hi abhijain

Just to be sure, I fall into the camp that uses DCF and reverse DCF. However, the assumptions that I make I try to validate by talking to some ppl from the industry like how a businessperson would do. Business people are surprisingly liberal with sharing their knowledge and so far business people that I have spoken to all think in terms of simple things like margins, salary, rent, what kind of product will move, credit lines, supplier payment, receivables , discounts , customer service etc. They are also optimistic by nature and believe things will be better tomorrow than they are yesterday. I am trying to inculcate these habits in me while looking at cos. Also business people are respectful of competition and try to co exist rather than get into wars that leave everyone worse off. They want everyone to succeed

Best

Bheeshma

8 Likes

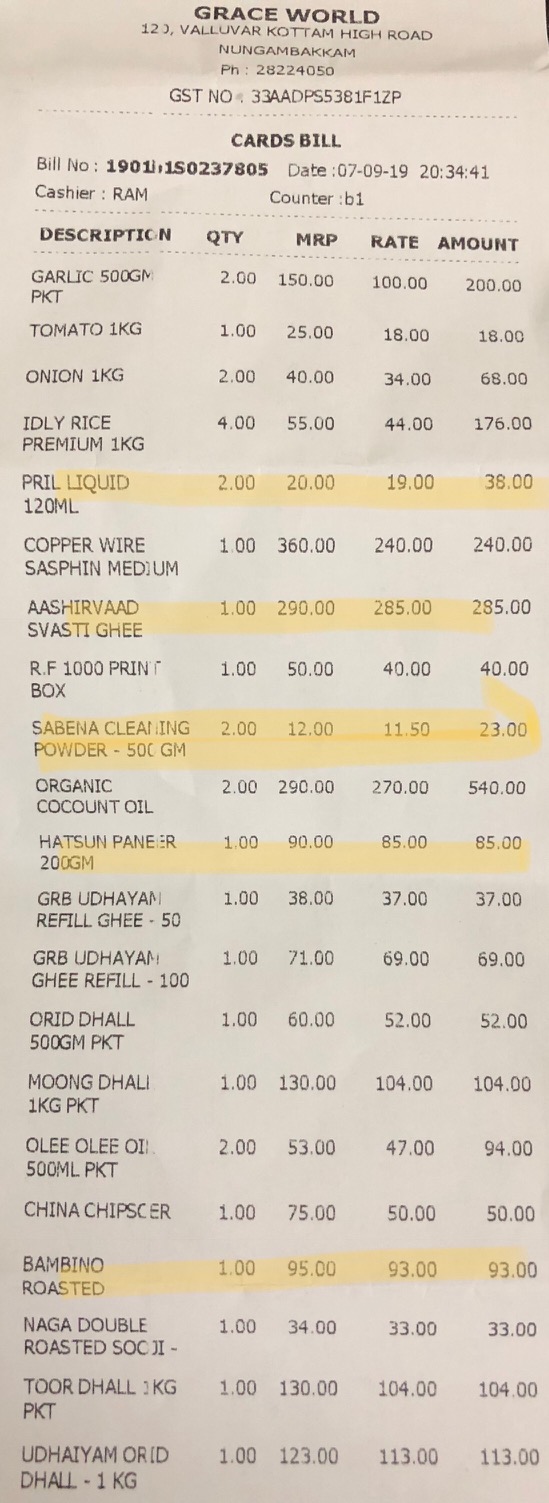

We buy our monthly quota with Grace (apart from other places like local kirana, Amazon, etc.). Here is our bill for yesterday:

Discount for FMCG items (leaving out private label items, vegetable, utensils) ranges from 1.7% to 5.5% only. Average about 2.5% discount on MRP. Of course there is no DMart but there is a More, Reliance and Big Bazaar near by.

Apart from the discount that Dmart offers, there are bank offers for Dmart (of course some are limited period only and with TnC):

- 5X reward points for American Express SmartEarn Credit Card

- 10% cashback for HDFC Bank’s PayZAPP (valid for Dmart Ready only)

- 7% discount on Visa Contactless card

I have not seen any other offline retailer offering bank offers like the way DMart does. If we are able to take advantage of these offers, the cost for consumers comes down even further.

DMart still does not accept Sodexo card/coupons (maybe due to high MDR?) which if they start accepting, there will be even more sales. I know folks who buy at Nilgiris (and other sales at MRP places) because they accept Sodexo cards.

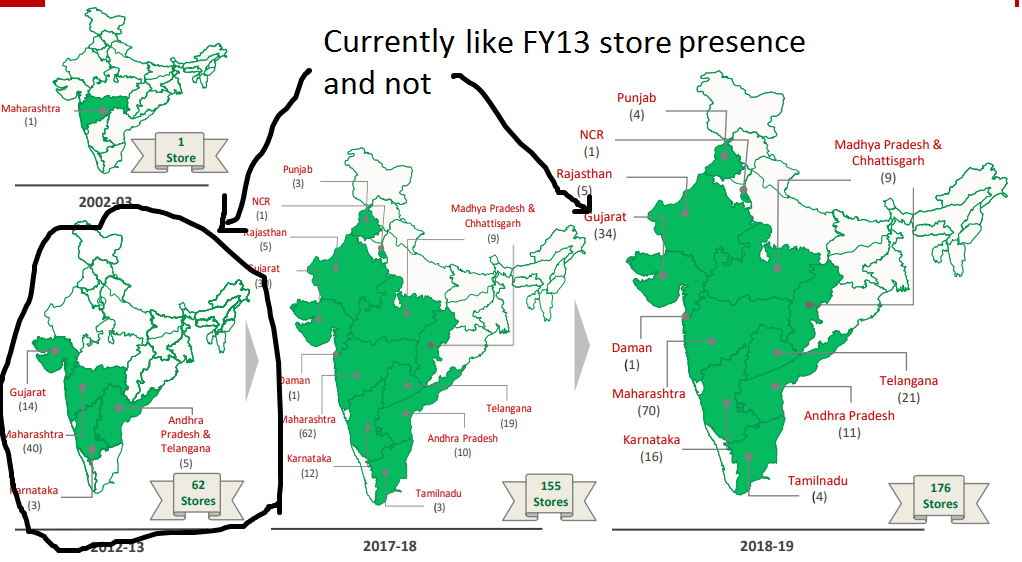

DMart has good store count only in Maharashtra, Gujarat, Karnataka, Telengana and Andhra Pradesh.

And even in the above states, there is opportunity to open more stores and offer alternate formats like DMart Ready.

I think it is easy to sound smart by being bearish (“expensive valuations”, “Something to worry about for 110PE stock”, “What kind of returns should a retail investor be expecting by investing at these rates”, etc.). It is very rare to see a minority shareholders friendly company who put consumers before shareholders. HDFC group is very shareholders friendly but IMHO, they are concerned more on profits than customers. MNC companies are again not worried about quarterly results but they aren’t that pro consumers.

Avenue Supermarts is one of a kind company and the valuations reflect that. I feel we can’t buy gold at silver rates or Re 1 for 50 paise. ![]()

12 Likes

They have now started a large store format (3 floors) just like Dmart and give minimum 10% discount on FMCG too but it seems to be only for certain shelves.

Nevertheless Dmart is definitely better as they have exclusive packing for some items which shows they are able to negotiate pricing. Reminds me of Walmart vs say a Family dollar.

Sodexo coupon is moving digital & have tie up with RBL, it is in the name of ZETA which is acceptable at Dmart. Certainly they don’t entertain physical coupons

I get a meal voucher amount from my employer which is loaded to a Sodexo Meal card. It is not ZETA for us and many have this non Zeta card which is not accepted at DMart.

opportunity size :-

To plan a store of 15,000 sq ft, one has to target a neighborhood potential of 20,000 families with Rs 2,500 as minimum spending in a store that offers basic day-to-day needs. There can be at least 8,000 such locations in India. This will account for 50 per cent of the population only. So the potential is very high. Having said that, ‘number of stores opened’ is not the right unit to measure growth, as maintaining a big supply chain is equally challenging.

4 Likes

Sounding smart is not going to get me anything. However, my hope is that, if I speak my mind, and indeed if there is an opportunity, I will see it in the discussion. Around a year ago, I was dished with supercilious remarks on the threads of Page and Yes Bank (Gruh) as well. All are still good businesses, just trading much lower. Call me old fashioned, but I believe that one finds success in buying equities, if a good business is bought for cheap.

Dmart is as good as a business gets, but is it cheap?

My perspective:

I do not expect Dmart to assume growth rate any more than 12%. Punching in 12%, it will take 20 years for this stock to generate yields as much as the FD rates.

During this period of 20 years, I am fairly confident that there will be a temporary hitch, and I will get an entry with comfortable valuation. In the meantime, I am not worried about any opportunity cost of not investing in Dmart, as I do not expect the stock to be further re-rated.

13 Likes

Hi

I thought I will chip in here on Sodexo Zeta etc.

Sodexo are closed loop payment instruments based on archaic business model of yesteryear. I don’t think many people will accept it in future. Merchants don’t like it either. If Dmart has not done an integration for this closed loop instrument they will not accept. I also think they should not, its not worth the roi imho.

Zeta now a part of corporate benefits of Sodexo (a merger I think) offers an excellent product which is open loop (a MasterCard) along with an app for payments. This is what can be used at any relevant store.

Thus Dmart accepts this open loop meal voucher. I haven’t tested it but I am certain it will as it will have the requisite merchant category code.

Rgds

3 Likes

Yes dmart accepts zeta. I use it for all my visits there. It’s like a normal debit card payment

The online player like Big Basket are eating away the pie of market share from Dmart. In stay in Mulund - Mumbai and used to buy from Dmart but it is so crowded that I have given a miss to Dmart and started to buy online from Big Basket and Tata star online platform.

Dmart as the cheapest retail has been increasing price in some categories which could improve their margins but not good from customer perspective.

In addition to this they have started with their online App but the cost which is the most important factor seems to diminishing.

Big Basket is really great business from my point of view but its sad that its unlisted, It has BBdaily as online platform which is doing really great its taking away business of unlisted Milk ,vegetable and fruits suppliers. Dmart should really think the way Amazon’s way of Hatkey strategy and should buy stake in online platform.

Their is saying that Good is not always good and Bad is not always Bad. I wanted to my observation, hence posting on this thread.

Regards

Rishi

Disc- Not invested

3 Likes

Is Big Basket profitable? What are it’s margins?

1 Like

It’s unlisted, so I don’t have the calculation figures for it.

Nevermind. A simple google search led me to these figures.

Key takeaway: It is really difficult to build a profitable business with healthy margins especially in grocery. Subsidizing revenue growth while funding losses isn’t the right answer. Big Basket can become a great business, but the present model doesn’t seem to be the right fit.

4 Likes