I am thinking on the govt proposal to SEBI on bringing down minimum promoter stake from 25% to 35%. More float can take off the valuation? high PE

Interesting read on Target…

chrome-extension://oemmndcbldboiebfnladdacbdfmadadm/https://investors.target.com/static-files/46e2afef-c880-4562-9034-5300e9da0dd3

Another great read on retail scenario

Understanding Costco

3 Likes

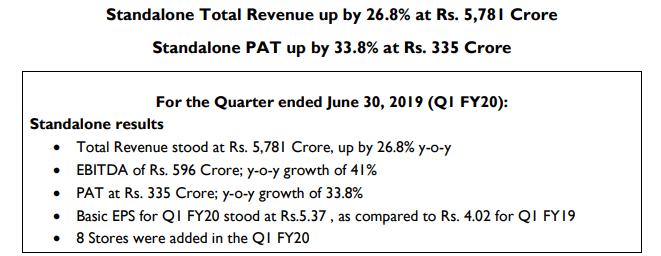

Standalone QoQ

EBITDA Margin 10.3% vs 9.3%

EBITDA 596 cr vs 423 cr

Net Profit Rs. 335 cr vs Rs. 251 cr

PAT margin 5.8% vs 5.3%

EPS 5.37 vs 4.02

dmart_Q1_2019.pdf (2.9 MB)

2 Likes

I think results are impressive amidst the slowdown fear pervasive across, also the big question of scaling up in terms of new stores additions can be put down at least for now (and hope they continue at this velocity for full year).

Above all, like the below statement from management on setting the expectations low, shows the character.

“As we have said in the past, Q1 margins are not usually a reflection of the entire year.

We opened 8 stores in this quarter, large part of which are a spillover from the previous quarter”.

No membership/loyalty programs, no ads on the discounts you offer, no fancy stores, no concalls, no big forecasts, no television appearance but relentless focus on keep doing what you are good at, dmart has always defied convention, a maverick.

disclosure: own it

15 Likes

Alongwith positives in quarterly result the concern remains with margin contraction to 9.74% during the quarter compared to 10.81% in same period last year.

Can you pls let us know according to you what they are good at? Thanks

In my opinion - result is good. The news of new stores is also good.

Plus, for a company of this repute, YoY profit-loss statements, balance sheets etc also looks good to me.

The only concerns is that Mr. Damani’s current shareholding is more than 80%.

According to SEBI rules - minimum public shareholding of a company should be 25%. The listed companies have to ensure the minimum public shareholding in three years from the time of listing.

DMart was listed in March 2017. Which means, there will be a supply of extra 5% stocks within next 8 months ie march 2020. Further, if SEBI implements FM Nirmala Sitharaman’s suggestion of minimum 35% public shareholding - instead of 5%, we may see of 15% surplus shares in the market.

Therefore, rather than buying it now, I would keep it on radar for possible entries at lower levels.

Disc.: Interested but not invested.

4 Likes

While we keep on discussing impact of online grocery sales, attached article related to BigBasket shows why brick & mortar retailer will have an edge.

New entrants will keep on coming, experimenting but huge size of market & low margin will always pose tough challenge for them.

I am interested in plans of Amazon & Reliance… hope they are also watching this space & specially tricks, experiments, reasons of success / failure of BigBasket, Grofers, PepperTap, and Localbanya. Having said all these were too small in comparison to Amazon & Reliance

5 Likes

I always wondered how can LFL Growth could be so high for D-Mart. I believed it should be around inflation or may be 2-3% higher than inflation.

After working out the numbers yesterday night, I realized most of the LFL growth is coming from the stores which were added just last year. Stores which were opened two years ago actually show LFL growth of about 7%.

Let me elaborate on how I came to this conclusion. For simplicity, let’s assume R19 is revenues in FY19 and R18 is revenues in FY18; and A19 is area of stores opened till FY19 and A18 is area of stores opened till FY18.

R19 = Revenues from stores opened till FY18 + Revenues from stores opened in FY19

Revenues from stores opened till FY18 = R18 * (1+LFL)

=> Revenues from stores opened in FY19 = R19 - R18 * (1+LFL)

Area added till FY18 = A18.

Area newly added in FY19 = A19 - A18.

Now, lets compare Revenue per area of newly added stores in FY19 vs. old stores opened till FY18 and put everything in a table.

| Stats | 2019 | 2018 | 2017 | |

|---|---|---|---|---|

| Revenue from operations (cr) | 20052.87 | 15102.5198 | 11926.2549 | |

| Retail business area (sqft) | 5900000 | 4940000 | 4060000 | |

| LFL | 17.80% | 14.20% | 21.20% | |

| Revenue from year-1 stores (cr) | 17790.76832 | 13619.7831 | 10425.25604 | |

| Revenue from newly opened stores (cr) | 2262.101676 | 1482.736704 | 1500.998863 | |

| Revenue / area from year-1 stores (rs/sqft) | 36013.70106 | 33546.26378 | 31307.07519 | |

| Revenue / area from new stores (rs/sqft) | 23563.55912 | 16849.28073 | 20561.62826 | |

| Growth of R/A from year-1 stores | 7.355326646 | 7.152340434 | #DIV/0! |

You’ll find that Revenue / area of newly added stores is less at around 20000 rs / sqft while it is 36000 rs / sqft. Actual LFL growth is only around 7% as per trend of Revenue / area of old stores. In the next year, this 20000 rises to 36000 * (1+0.07). And this is what is driving the LFL Growth of 15-20% for the company.

This helps me understand that D-Mart gets 7% growth for free!

And additional growth rate depends on how much area they add. Currently they are doing it at 20%. This implies revenue will grow by 1.2 * 1.07 = 1.28 => 28% growth. And this is the growth rate they are achieving at the moment.

Some questions exist like

- Why is two year old stores’ LFL 7% and why is it still higher than inflation?

I think the additional 200 bps of growth which D-Mart is enjoying must be due to new customers it is attracting. Or may be new kind of assortment they are doing. All in all, I would give that credit to the D-Mart team. - Why is Revenue / Area lower in newly opened stores?

This can be due to various reasons. The store might not get great traction during its beginning months. If the store is opened mid-year, it can’t capture the full year’s revenues…

Hope the model makes sense. I enjoyed a lot while playing around with those numbers.

Please let me know if you find anything wrong / miscalculated.

Discl: No holdings, however conviction keeps increasing with time. Unable to buy at current prices. Confused whether to buy or not. Requesting Mr. Market to give an opportunity. Please do your own research.

21 Likes

Good coverage on Dmart.

10 Likes

Completion of sale of equity shares of the Company held by the Promoter Mr. Radhakishan Shivkishan Damani in the Open Market for achieving minimum public shareholding.

Done within 2 days !!

1 Like

The AGM of the Company has started at 11AM at Nehru Centre Auditorium, Discovery of India Building, Ground Floor, Dr. Annie Besant Road, Worli, Mumbai- 400 018, to transact the business as set out therein.

We may get update on progress on fund raising to avoid frequent commercial papers & future growth.

Anyone attending, please share the notes.

Live webcast for AGM of Avenue Supermarts

1 Like

Can anyone please post the highlights of AGM…

- Current promoter holding is 80.2%

- QIP of 2.5 Cr is planned (& hopefully approved today… voting result will be announced later)

- Post QIP promoter still need to sell 1.375 Cr shares (or find alternate way to do so)

- Promoter has 7 months in hand, to bring their holding below statutory requirement

- Management is not considering dividend payout (based on light comment)

1 Like

AGM 19 Notes

-

No Dividend as of now. Prefer to reinvest and open stores as that’s the best utilization of money.

-

Real Estate in South Mumbai extremely expensive so no stores there as business will not be profitable. Lot of references to Dmart ready by shareholders esp about milk not being available in the morning but only post noon. Dmart Ready stores available in lot of areas of South Mumbai. Approx 45 pickup locations in South Mumbai and overall 209.

E-commerce biz extremely small we did a turover of 140 cr and lost 50 cr. We are in e-commerce because we know a certain section of customers value shopping online because of the convenience. No clue when we will be profitable and we are not looking at it like that. Our only focus in ecommerce is to build a sizable business without losing too much money and only that much that the balance sheet can afford. No reckless spending and thats why we have launched only in Mumbai. Mumbai is big with a pop of 2cr and its a good testing ground to test your hypothesis.

-

In crowded stores when all options to manage crowd are exhausted like opening more cash counters, reorganizing layout, etc - then another store is opened 2-3 km away

-

Prefer to grow in the same state and in the same location as opposed to going to more states. The reason is that its a low margin business and setup costs in new states are higher. We understand Maharashtra, Gujarat, AP, Telangana and Bangalore very well.

-

We will try to maintain the same level of store growth or better but no commitments as of now

-

We would prefer to own stores as opposed to leasing them. We have 153 locations that are owned and 23 are leased. Since these are not small stores but large-format stores we want to send a message to the developer community that Dmart is not averse to renting stores. 80:20 split between Owned stores to rented stores is ok. Right now we predominantly have an owned store model. If you move fast you lose money in this business. We evaluate very carefully the feasibility and try to make very fewer mistakes in adding locations ( Mentioned Nagpur investment in a store being stuck).

-

We are trying to accelerate the turnaround time to process new store additions. If something takes 3 years we are trying to see whether it can take 1 year or 2 years. In a lot of cities Building approvals are being done online - so things are changing.

-

SSG is not the only metric to evaluate Dmart performance. If a store is doing 17-18% growth and another store is opened then obviously the SSG will collapse. Nothing has changed otherwise in the business.

-

No guarantee on Gross Margins. We want to remain competitive and we are in it for the long term. By long term, we mean 30-40-50 years. Relevance to the consumer is the key. We want to stay relevant to consumers. If competition becomes aggressive on prices we will also compete and vice versa. However, retail is not only about pricing and price wars. Margins are highest in clothes, steel utensils etc

-

A lot of our employees have come up the ranks. If you visit Dmart have a conversation with them, they will tell you what they were doing 3-4 years ago. Internal promotions are a focus area in Dmart and we are proud of that fact.

-

Allied Retail is into Manufacturing and Distribution of Food grains and they supply to Avenue Supermarts and Avenue Ecommerce.

-

ESOP scheme is 2016 scheme.About 1.39cr shares were granted and 1.2cr shares are live. Rest have lapsed.

-

On giving dicsount vouchers as done by other retailers. Dmart is a everyday value model customer should get best prices everyday and anytime they enter Dmart.Bhav itna sasta hain and aur bhi sasta karenge to Shareholder ko dividend kaun dega.

-

We have very strong procedures as far as freshness is concerned. When goods are received at Warehouse every receiver is trained to not accept goods if it doesnt pass the balance shelf life test. At least 60% -75% balance shelf life should be there depending upon category to category.

Best

Bheeshma

39 Likes

I had my first visit to a D-Mart store recently and here is my two cents on what I observed.

The store is on the outskirts of Bangalore and about 10 km’s from my house. We could visit it because we had a day off during the weekday and hence decided to pay a visit.

- D-Mart undoubtedly offers the biggest discount on the products that they stock. The key here is the number of products. They have obviously done their analysis and store most of the larger selling brands. However, if you are looking for things which are a little less mainstream, you are not going to find the same.

E.g. There were only two brands of corn flakes on display. The discount was huge but only those two brands - a comparable store from More would have around 5 to 8 brands whereas a Big Basket would have in double digits.

Same was the case with say varieties of rice - there only a few. (I saw 4 types)

-

Some common ingredients that are seen in very small stores in Bangalore were not present. E.g. Brown sugar. However, they had certain brands of imported pasta on which they were giving extremely good offers. This was a little surprising.

-

I could not find fresh vegetables? Do they not stock the same.

-

It was decently crowded on a weekday (3 PM) and I can understand the reason people visit D-Mart (obviously discounts).

My two cents - a very good bargain store specifically for those looking to buy in bulk. I saw three dudes emptying an entire shelf of Ragi Mix (probably 50 of those .5 kg bags). They would obviously do well as long as they are able to provide the humongous discounts. As long as they can maintain the same I suppose they will grow. I will still prefer a Big Basket or a nearby store like More because of the variety and since I do not buy in bulk but that is just me.

Note: Not invested nor tracking

6 Likes