Hi @lakshay_agarwal: What do you understand by these two data Points:

Shrimp exports decreased from last year by 30% however gross income from shrimp processing and exports division increased 30%, specially as they clearly mention its due to increase in sales quantity by 35%

I guess you misread the export numbers, what the export numbers state is :

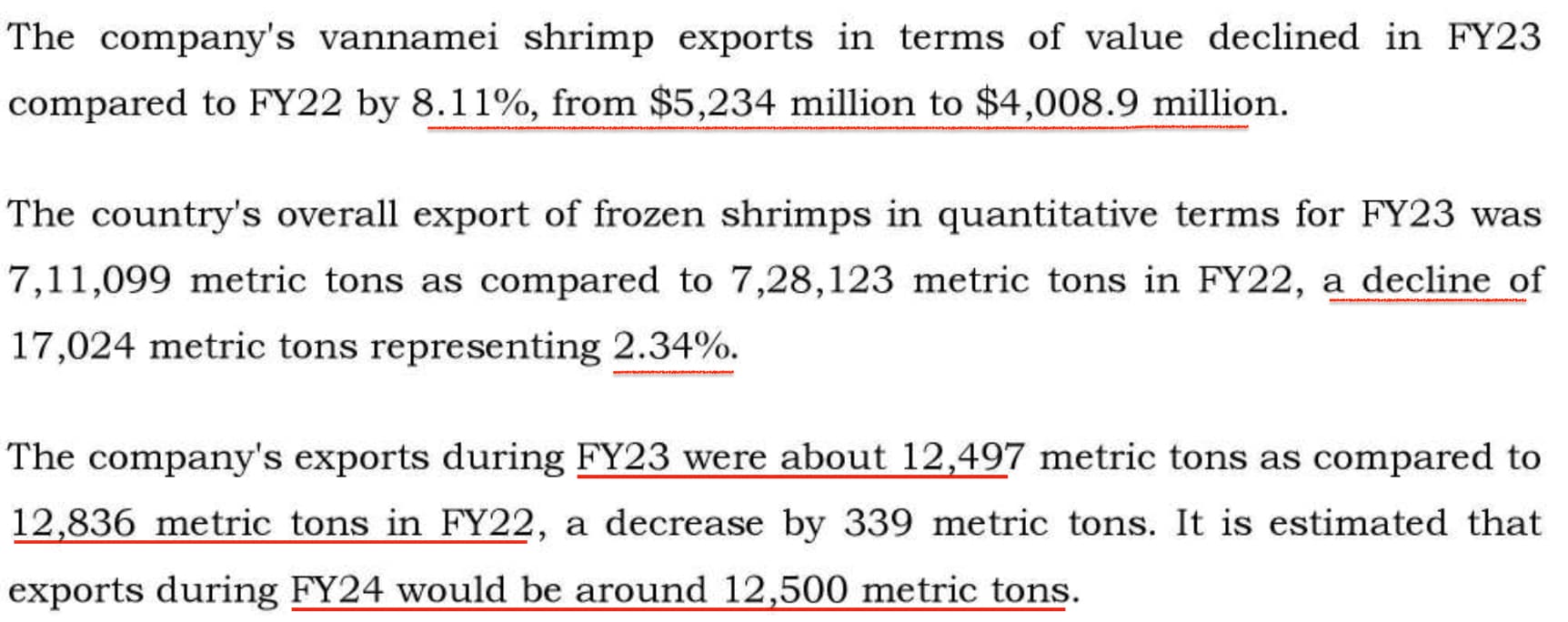

So the country’s overall exports were down by somewhat 2.4% , and the company’s exports were also somewhat down by 2.6%, but in the specific Q3 comparison we saw an increase in gross income by 29% which was mainly attributed to sales volume increase of approx 39% as shown below from 2865 mt to 3990 mt

Rest if you still have doubts, then you can directly message me ![]()

A decline from $5234 million to $4008 million is 23%. How is it 8.11%

1 Like

I think rather than taking management comments at absolute face value (promoters are very conservative), one must try to understand what is happening in the industry. Look at nos of Avanti vs its peers and there is a contrasting difference in the performance over the last 3 years. Most of the players despite being small have not grown and are working on wafer-thin margins or making losses. It’s rare to see a market leader having 45-50% market share continuing to maintain/grow its sales when the industry is in bad shape and other players are bleeding.

Interestingly after a gap of almost a year, Avanti recent commentary seems a bit positive.

Disc: Invested in family and client acs

41 Likes

totally agree with you . Avanti is only co which has maintained market share , profitability at this scale and has the unique advantage of size to take advantage of tailwinds in sector.

1 Like

Near term triggers:

Ecuador as country is going through an emergency, nobody wants to stay exposed to vulnerable supply chains any more. The country is also in a catch 22 situation where it had to cancel some arms deal with US because Russia threatened to import bananas from India. US are also looking at imposing duties on cheaper shrimp imports.

Fin Min has announced for a package with more details post election for the aquaculture sector as a whole, should be interesting.

Avanti is also diversifying. So like in the feeds segment they are gaining technical know how from Thai union, now they have signed a similar agreement with another Thai co for developing own pet food biz and shall also enter into fish feeds vertical. All of this should help as they have a very strong reputation/brand recall (synergies playing out potentially).

For me this might not be a buy and forget bet, more like a situation where trying to time the industry cycle bottom and then see how it plays.

Also attaching a chart with Nifty500 rel strength.

13 Likes

Another good set of nos from Avanti, with sales growing by 14% and EPS by 16%. Management seemed quite bullish on demand in 2024 and are targeting 17% volume growth in feeds segment and 20% in processed shrimp segment. Concall notes below.

FY24Q3

-

Present RM price: 129/kg (vs 138/kg last quarter), 53/kg soyabean (vs 54/kg last quarter), 30/kg wheat flour (29/kg last quarter)

-

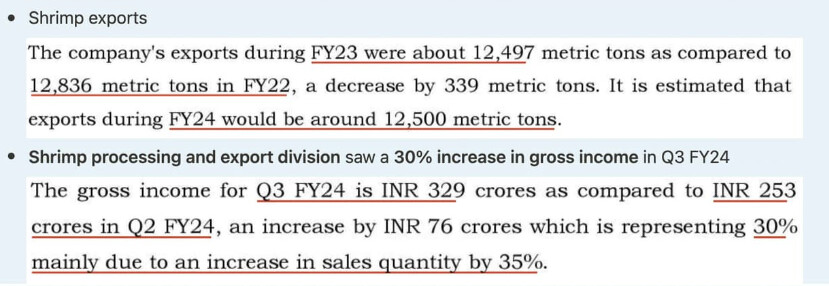

Processed shrimp sales grew 30% YOY (35% volume growth)

-

2024 feed volume: Expect 10-15% growth to 12.5-13 lakh MT – Avanti’s target is 6 lakh MT (vs 5.13 lakh MT in 2023)

-

2024 shrimp sales: Expect 15,000 MT (vs 12,478 MT in 2023) . Strengthening exports to USA and Canada, and venturing into new markets of Japan and Korea

-

Seeing short term benefits from geopolitical problems in Ecuador

Disclosure: Invested (position size here, no transactions in last-30 days)

21 Likes

How should we view this report?

https://twitter.com/NDTVProfitIndia/status/1770733334475215096

6 Likes

The senator move is after this whistleblower report

5 Likes

Is it bad for indian shrimp companies, or favourable as it makes attempt to make level playing ground for India against Eucador due to higher CVD on Eucador. @harsh.beria93 @Tar @Chins

2 Likes

2 Likes

Reality of Indian shrimp industry whistle blower issue https://youtu.be/N0eXL3s3r9I?si=7f9bS0ZmZqKTcOj9

1 Like

How does intention even matter ? Even if it is political and if the industry is export driven, any such action means a significant headwind for the firms. From investment perspective, this could be a big drag.

However, even with intention, it is being done by almost every nation. Nothing to do with US or West. India is also protective about a lot of industries. And, every country is within their rights to define the quality check. Indian pharma is a shining example of how the industry has grown in generics in US even though its such a highly regulated place.

3 Likes

Not a non-vegetarian so curious to know if a situation like Bird-flu increase the consumption of other meat sources. Is there a possibility to see a spike in prawn/seafood consumption?

Hi Ayush - I have been following this company for a long time though i am not an investor since many years. Think many investors including you, (if i remember the concall transcripts correctly) have raised the issue of the high cash holdings for which the management has been giving explanations which seem ludicrous (in one call they said it is so difficult to get 100 cr loans from banks or something to that effect). If they were some crank guys one could understand but in all other aspects of their business they are the most efficient guys in the industry. As an investor, smart people doing seemingly dumb things is a bigger worry than simple dumb management.

Since you have followed them so closely (unless Im mistaken you are among the initial lot for whom it was a 80-100 bagger), what gives you the confidence that published numbers are what the management says they are because the Occam’s razor explanation for the cash (along with the presence of small time auditors) is that things aren’t actually what they are shown to be.

What do you mean, why do you doubt? It seems they have audited Suven Pharma a few years ago.

Not invested.

1 Like

What I could understand is that all these options we give to management for cash payout etc involve taxation. For an entrepreneur all these things are a hit. What will they do with cash payouts at their end…they are already getting funds by way of salaries and dividend and don’t have avenues to deploy.

4 Likes

They increased salaries by a good amount sometime in 2023. And unless I’m very wrong this factor has depressed both return ratios and share price reducing returns for management…

But thanks for the response. It’s quite frustrating. They’ve been gaining market share and have seemingly avoided many pitfalls better than competition (my company works with other players in theindustry so have some general idea of what’s going on), but this fact I’ve not been able to fathom.

I mean the general quality of confidence is lower with smaller auditors. Not a capability point more related to intent and checks and balances. Especially when management description of accounts is questionable as in this case…

1 Like

I agree that the company has been doing several good things on the business front…despite such challenging scenario in the industry…they have been able to grow and build capacities for future. Just that the business is so good that it throws out cash flows and they don’t have avenues to deploy

9 Likes