How do you look at businesses like these w.r.t returns? Price has been in consolidating for 4-6 years. Would you not think too much in cases like these, if you had made big returns, so even if the non-performing years are added to the holding period, the overall return is satisfactory for you, and your focus lies elsewhere? Or you have a certain threshold w.r.t time, after which you exit, not to mention the fact that you know about the businesses very well? Or 4-6 years of time is not that long for businesses which will be existence for decades, and assuming, as you would have fairly large positions, you will hold for longer periods?

I have not particularly read many of your comments, one reason being, you are a very experienced investor, who manage several portfolios, but it will help to know.

And is holding for years a combination of availability of capital for other ventures, affordability of opportunity cost, and temperament or is it an advantage limited to few?

I don’t have a good answer. I run a very diversified portfolio and I’m very comfortable to hold a company like Avanti. i try to increase allocation when I feel this offers more value vs other ideas.

But yes, last 3-5 years have been a drag. Since last 2 years I have been expecting things to change for the industry to happen but that is not playing out…but with more time I feel that my respect for the underlying business/leadership of Avanti have only increased.

I don’t agree its a good business as in it isn’t a good industry, look at the performance of any of the other listed players. There is no pricing power, RM cost is highly variable and volatile but governments are on your back all the time to not pass on price increases, working capital management is extremely challenging because of the kind of customers (look at Jain irrigation or any of the pipes players who largely cater to rural areas to understand what I mean).

Nevertheless there is a huge gap between how Avanti has done and how the its compatriots have performed. It may be management quality or it may be books not being pristine or a bit of both, I am simply unable to tell. Better to track and sit out till there are signs of cyclical turnaround which at the moment there are none.

The company has guided of ending the year with 6 Lac MT Shrimp Feed Sales (9M figures are around 4.2Lac MT) and 15000 MT for processed Shrimp. The available Capacity is around 7,75,000 TPA for Shrimp Feed and for Shrimp Processing , it is around 29,000 TPA so capacity wise , they do not need any Capex as of now.

What I want to understand is How Big the Market is…? At what levels , these sales can go up in say next 5-6 Years. Though Company is planning to make Fish Feed and can also go into other verticals in similar line of business but do you have any idea of Market of Shrimp Feed and Processed Shrimp.

Avanti is no doubt the Market leader which has consistently performed well. I only want to understand how Big it can Grow…! If you have any idea or figures which you may have read or heard in any concall or discussions…

I don’t think its a very scalable business as Avanti already has a large market share. The problem is Avanti is a big fish in a small pond. It will be wrong to expect high growth rates from here. Yet, on the positive side - govt keeps talking about growing exports from India…and over last 5 years nothing much has happened in the industry…hence at some point there should be some growth.

Have zero clue why my earlier message was deleted. Nevertheless, there were some serious allegations on the Indian shrimp industry as a whole in the articles posted earlier in this thread. It was one-sided as the responses were completely missing!

Here are a couple:

Choice Canning, the Indian company accused of re-exporting shrimps that were rejected earlier due to FDA detecting pesticides in their shipments - they have rejected the allegation that their shipments were ever rejected.

Nekkanti - accused of HR violations - was never enquired by the AP journalist if Nekkanti even ran that factory before publishing the story! And the journalist has been avoiding them even after publishing the story.

All that my now-deleted comment was raise doubt on the authenticity of these reports. Haven’t been a shareholder of any shrimp companies from a few years. Don’t have any cash in this game currently.

Not sure if the companies response is true or not. But pretty sure that deleting a post that questions the intentions of targeted news reporting against the Indian shrimp industry, that too in an Indian discussion forum is pathetic!

With La Niña conditions being predicted this year , how will the Indian shrimp industry be affected with respect to good fishing season expected during La nina in South America .All seniors request your views on the same .

Have been tracking the sector for a few months and I believe that the ADD and CVD court case is the primary trigger in this sector.

Lot of factors which are outside the control of shrimp manufacturers:

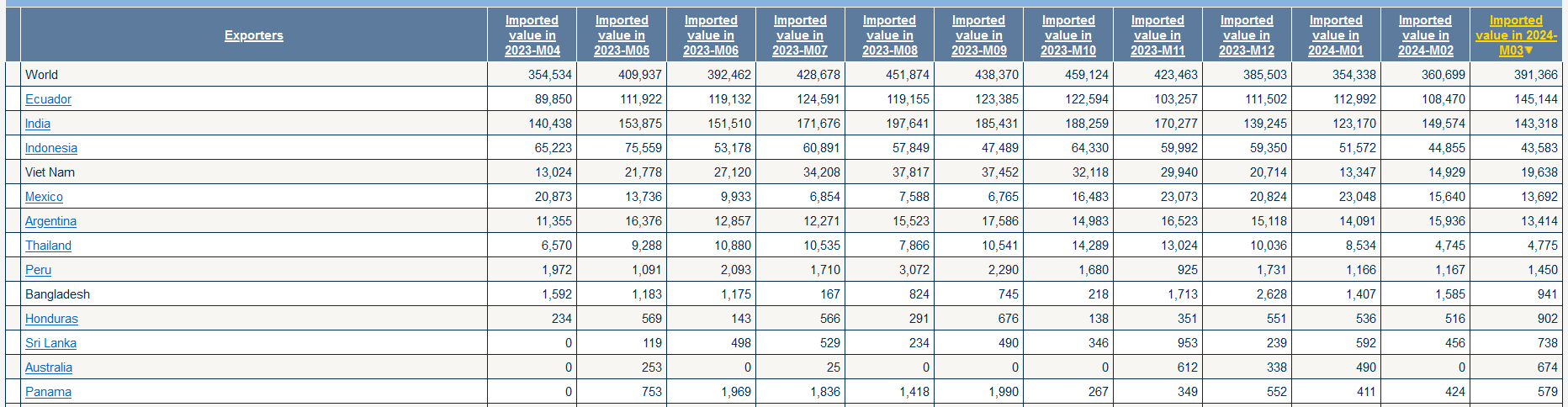

US shrimp consumption growth is slow (market size remains stagnant). Imports to US are also decreasing

Chart: Value of shrimps Imported by US (in USD '000)

Environmental factors that impact shrimp production and feed demand (demand fluctuates)

Raw material (fish meal, basically salt water sardines) prices keep going up as fish landing has decreased due to climate change (supplier side challenges)

Competition from a bunch of countries even aside from Ecuador (whose costs are significantly lower, both for production and freight), like Vietnam and Indonesia

US is the only large market for value added shrimp products where the margins are. China and Japan primarily import frozen shrimps only

Discl: small position. trimmed down and missed out on recent gains

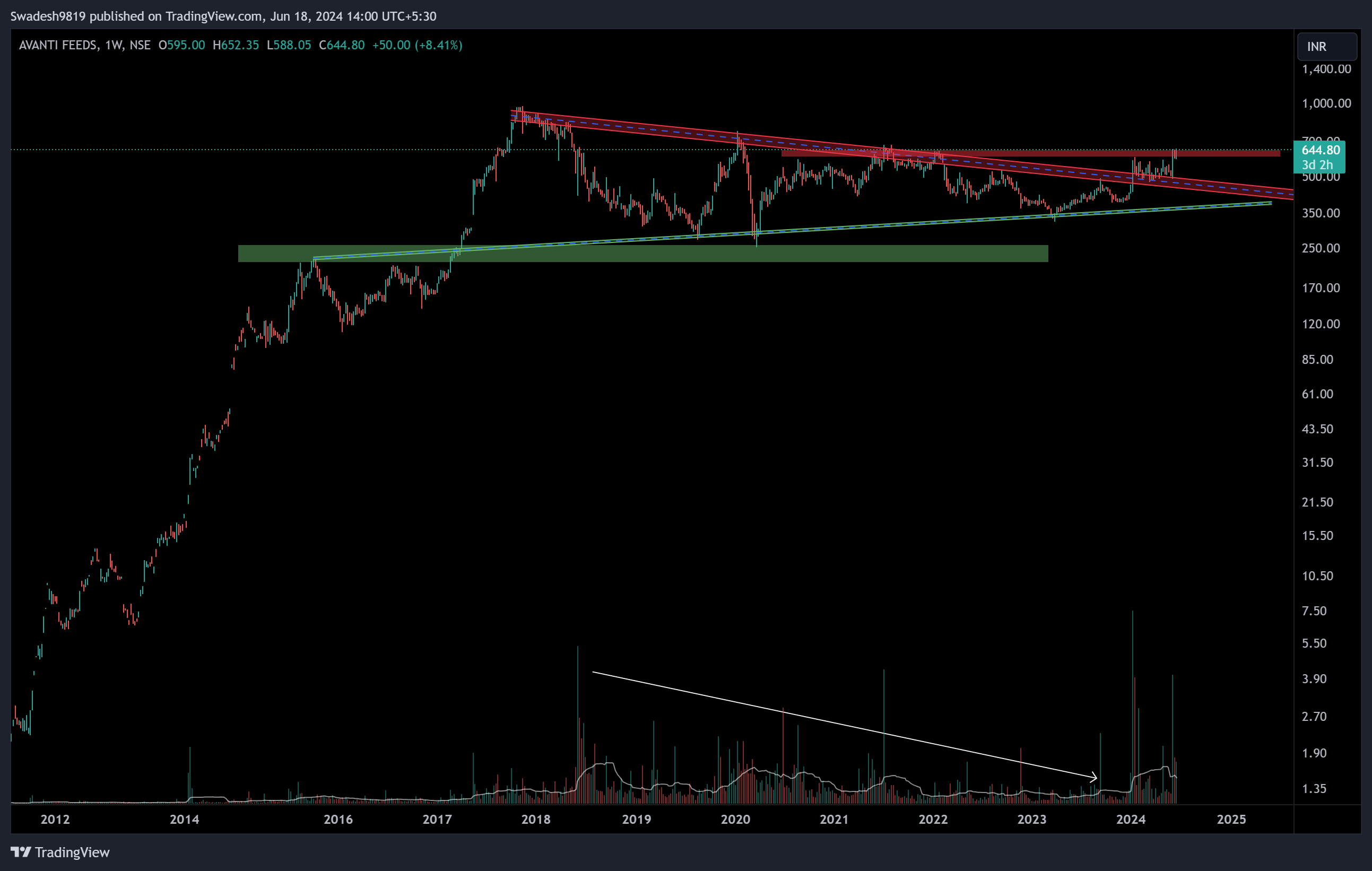

Is it not the data we see now has been discounted long ago? Since the chart looks super bullish and had broke out multi year consolidation in the form of symmetrical traingle pattern and consolidated just above the trendline.

I’ve the right to be wrong and I think it is entering into Stage 2.

The only fundamental trigger I can see is from the recent elections, which we know is most probably not going to impact the company’s operations much considering it’s already at 50-60% and commands ~10-20% more price for its feed (my rough estimate) compared to competitors.

Regarding the US case, it keeps getting postponed with probably next update in Oct (if I’m remembering correctly).

So, if all else has remained the same, then how will the company’s fortunes change? Also, they’re venturing into pet food because even they have realized the same but that is a very long-term bet with branded competition

Company is in Stage-2 but my fundamental knowledge of this sector has left me unconvinced.

IMO at the moment the stock rally seems to be taking place because of the political scenario rather than internal or external factor that affect the co.

To what extent can that push the stock with change in internals? Or are we anticipating the political situation will be a catalyst for the change in the company performance?

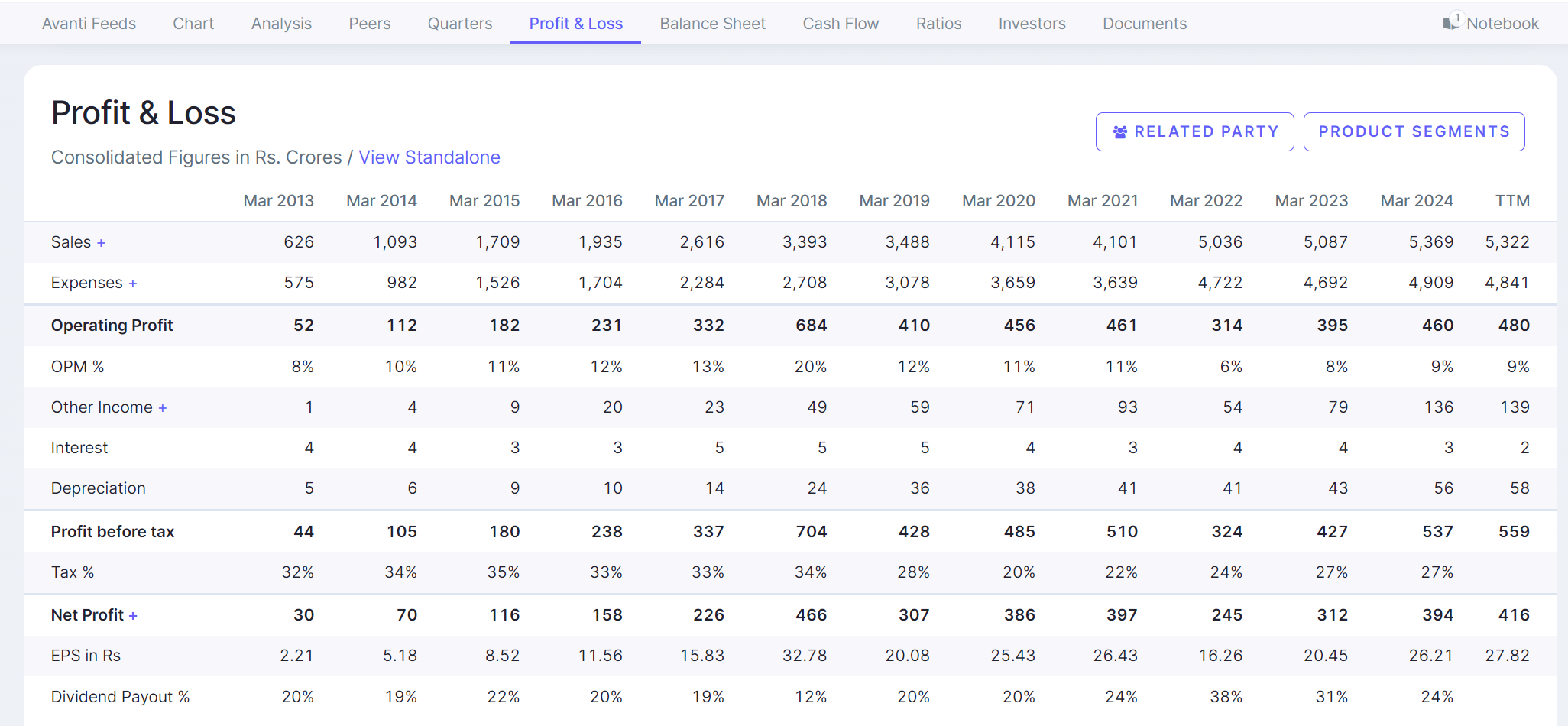

Avanti has been able to grow vs the peak in 2018. While every other company in the feed business has de-grown a lot. Infact if one goes deeper, one will see that others are bleeding and everyone is making losses or just breaking even…while Avanti continues to generate superb cash flows!!

This is the quality and brand power of the feed business of Avanti. They have added more capacity over last 2 years.

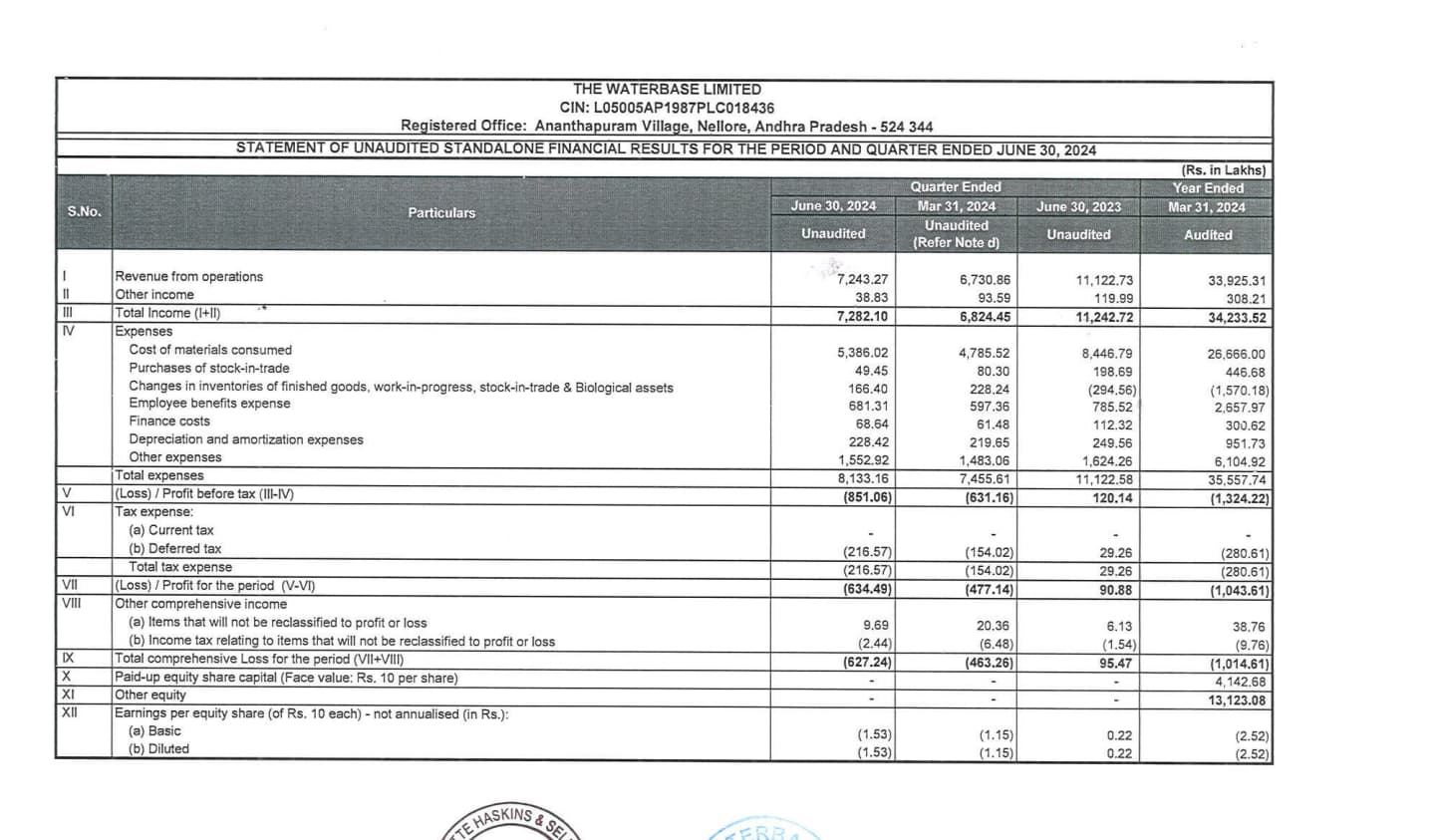

Just read the credit rating report of CP feeds and one will realise that they are making big losses.

Similar story here. Avanti is perhaps the only one which has grown and making money. Others have de-grown and are either making losses or just breaking even.

When one talks to people in the industry then everyone says, don’t compare us to Avanti, they are way ahead and leaders in what they do!

I think in Avanti, the business quality is superb but this has become a problem for them…lol. They don’t know what to do with the free cash flows they keep generating. And this has impacted the wonderful ratios we used to see earlier.

Last 5 years have been really bad for the industry and this highlights the difference in business quality of various cos.

I had high hopes from the management atleast on the quality front. This changed when Avanti saw salmonella issue in its products and had to recall due to FDA regulations.

I wanted to know if this is common in the industry (India and abroad). Are there any hidden implications (customer avoiding a brand due to this)? Perhaps you could add some colour?

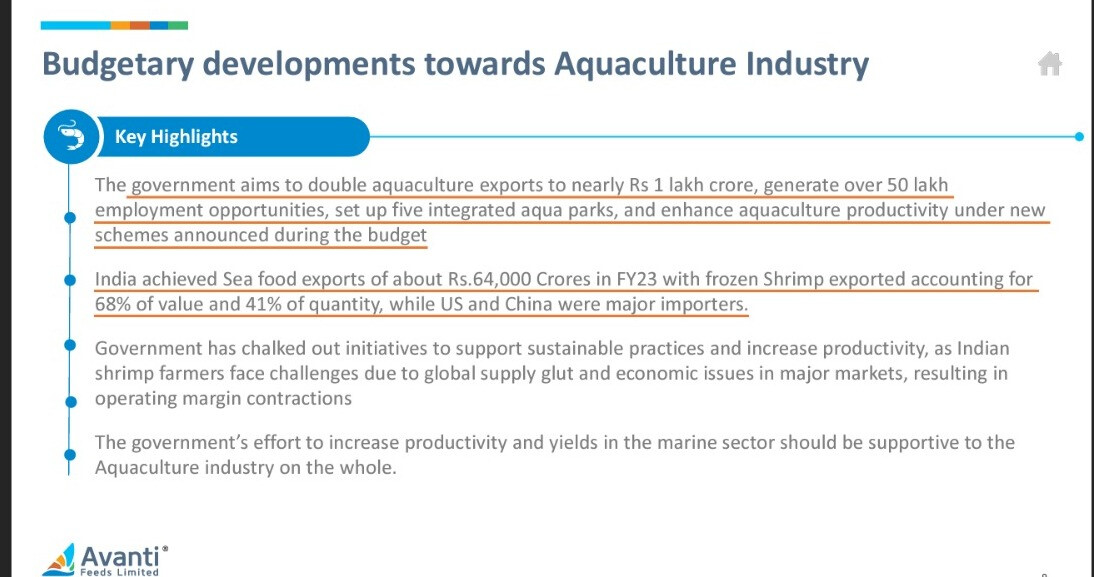

In the Budget speech, FM has announced that a network of Nucleus Breeding Centres for Shrimp Broodstocks will be setup. Additionally, financing for shrimp farming, processing, and export will be facilitated through the National Bank for Agriculture and Rural Development (NABARD).

In a recent report, CareEdge highlighted India’s position as the world’s second-largest aquaculture producer after China and one of the largest exporters of seafood globally. Over the past decade, shrimp production in India has seen an impressive growth of 255 percent, with production reaching 11.6 lakh MT in FY23 compared to 3.3 lakh MT in FY14.

Shrimp exports, which constitute approximately 70 percent of India’s marine exports, have also experienced remarkable growth. From FY14 to FY23, shrimp export volumes increased by 136 percent, and their value in INR terms grew by 122 percent. However, FY24 saw a deviation from this trend, with a 10 percent moderation in exports in INR terms, primarily due to international pricing pressures.

A simple analysis of this qtr result will show how beautiful/strong business model of Avanti is. The whole industry has been in shambles and most of the players are making losses and de-growing while Avanti continues to grow and is making all time high profits now:

U hit nail on the head , i was also scraching my head how come waterbase in the same sector is posting losses, yes avanti is having great execution skills,