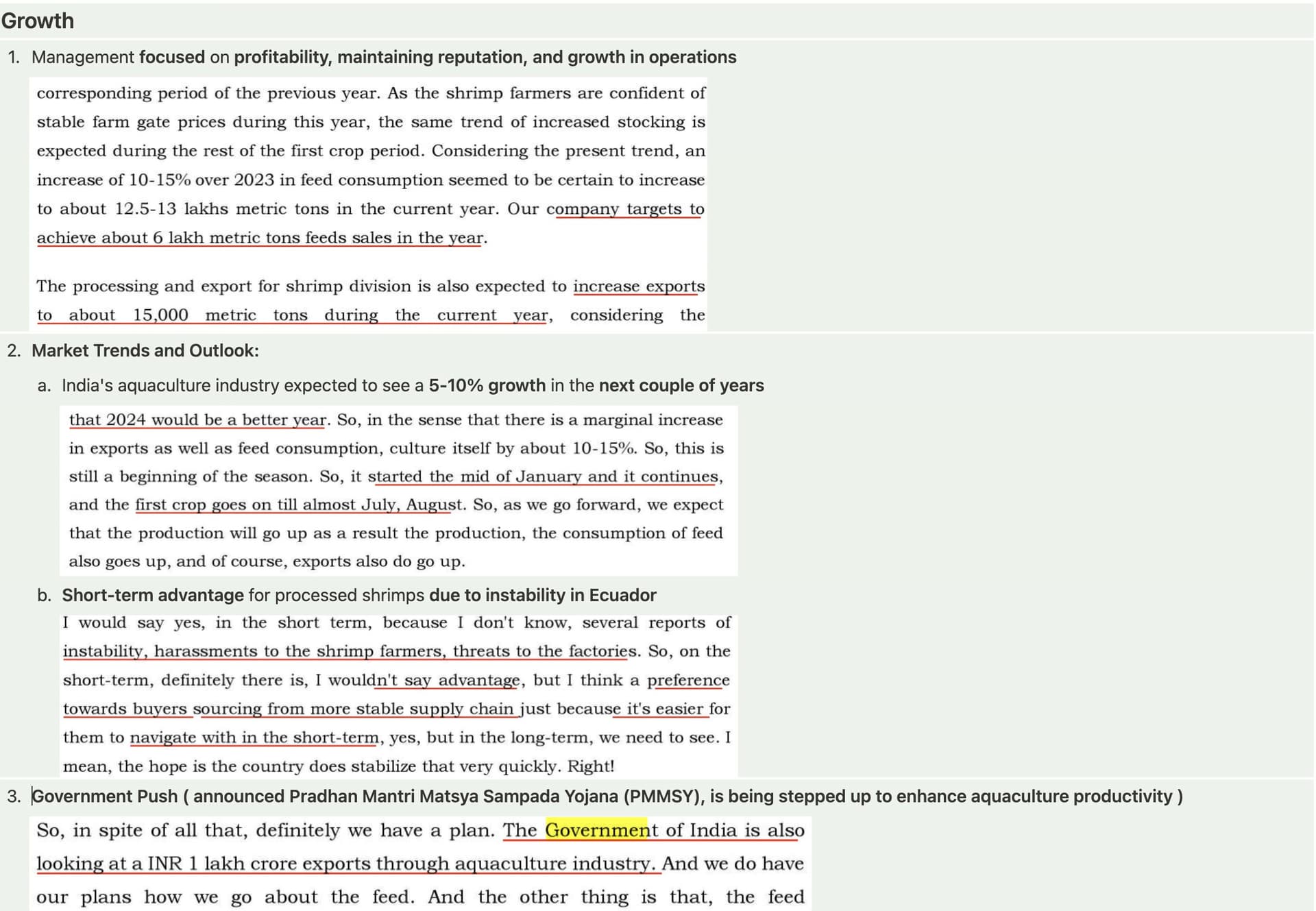

I have Gone through Many Article and thread To Understand Better Shrimp Industries

Here is My Take

Feed and Shrimp Processing Industries: India

“What Went Wrong in the Feed Processing and Shrimp Industries”

The world’s two major shrimp exporters—Ecuador and India

Increase in the capacity of Ecuador leads to oversupply and spiralling prices impacted Indian Shrimp Industry Badly Below chart shows how last 2-3 Years export of India Compared to Ecuador

How They able to Do This

Ecuador’s farmers have been increasing their output by using post-larvae that are tolerant to disease and grow increasingly fast; by using nursery ponds to shorten production cycles; by adding aeration systems and auto feeders to their grow-out ponds, which enable higher stocking densities

Ecuador supply at $7.42/kg where India Supply at $9.1/kg which leads to decrease the market share of India from 43% to 36% in 2-3 Years now again back to 36% in US

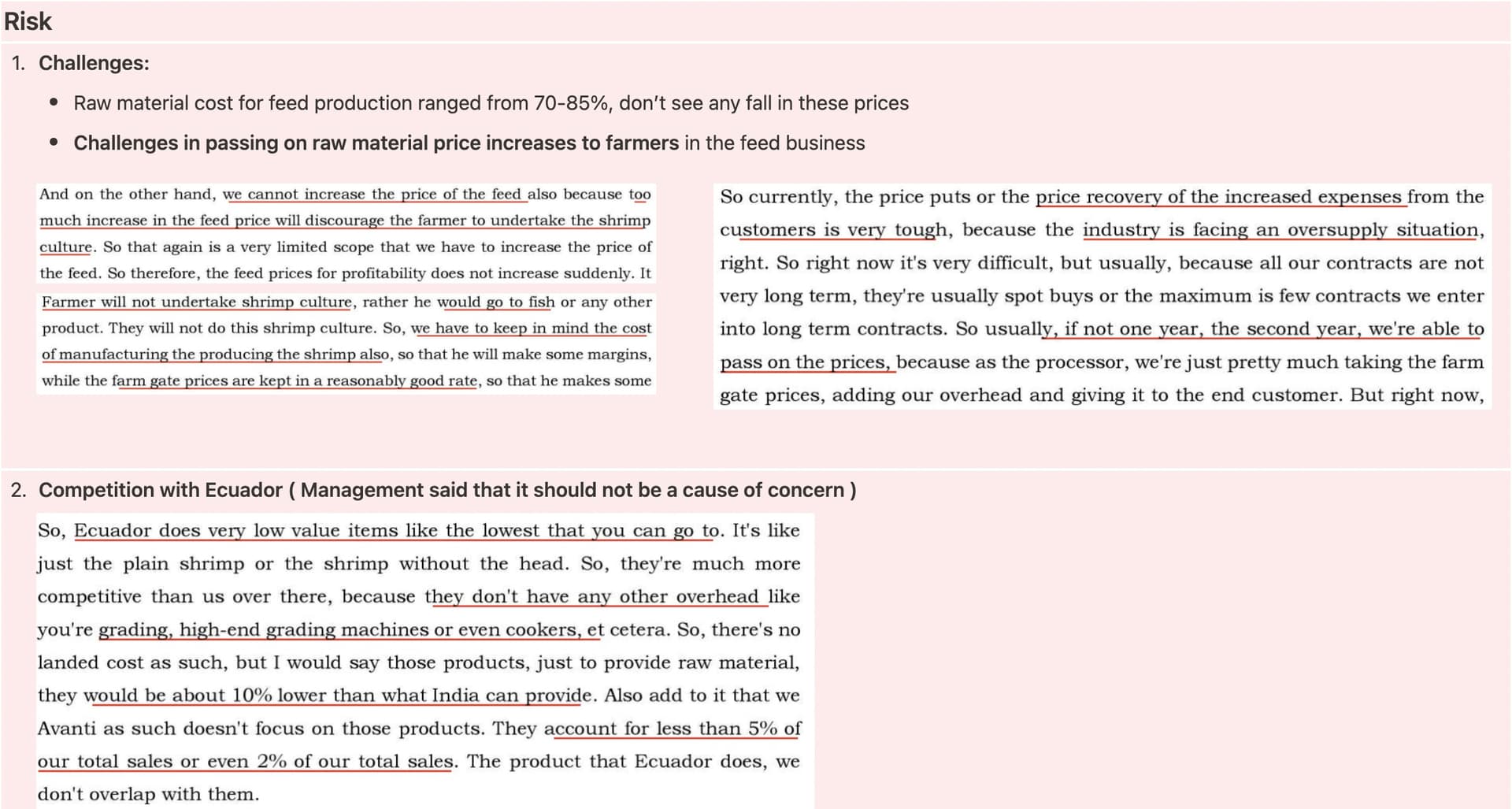

Ecuador has a lower cost of production of processed shrimp as processors there are large vertically integrated companies. Additionally, they have become the biggest producer of shrimp in past 2 years (from production of 600 mn to 1.5bn now).

Ecuador focuses on commodity products like headless shell on or head on, shell on shrimp

Raw Material Cost Increased for fishmeal, soyabean, wheat impacted the overall Indian shrimp Industries

Market expansion

Nearly 75% of China was made up of Ecuador shrimp market but covid restriction led to Aggressively focus product in US Market proximity to US coast reduced the Shipment transit time, faciliting Ecuador to dump its product in US Market leads to stiff competition to India where Shipment from India to US it takes Nearly 40 Days leads Further increase in fright and landing cost

What’s Happening Now

· Most of the Indian company under CAPEX and may commissioning of new plant will yield good topline growth and better ROCE

· US shrimp import market has seen improvement in past 3 months after 13 consecutive months of YOY decrease. However, realizations are lower by 10-15%

· In Indonesia and Ecuador, there might even be Antidumping Duty by US Countervailing Duty

· Company To Watch out: Avanti Feeds, Sharat Industries, Apex Frozen, Coastal Corporation

· Avanti a Market Leader Needs to closely monitor, company at bottom price, cyclical benefit may play out ,the PE at Lowest as compared to Mean PE of 5 Years