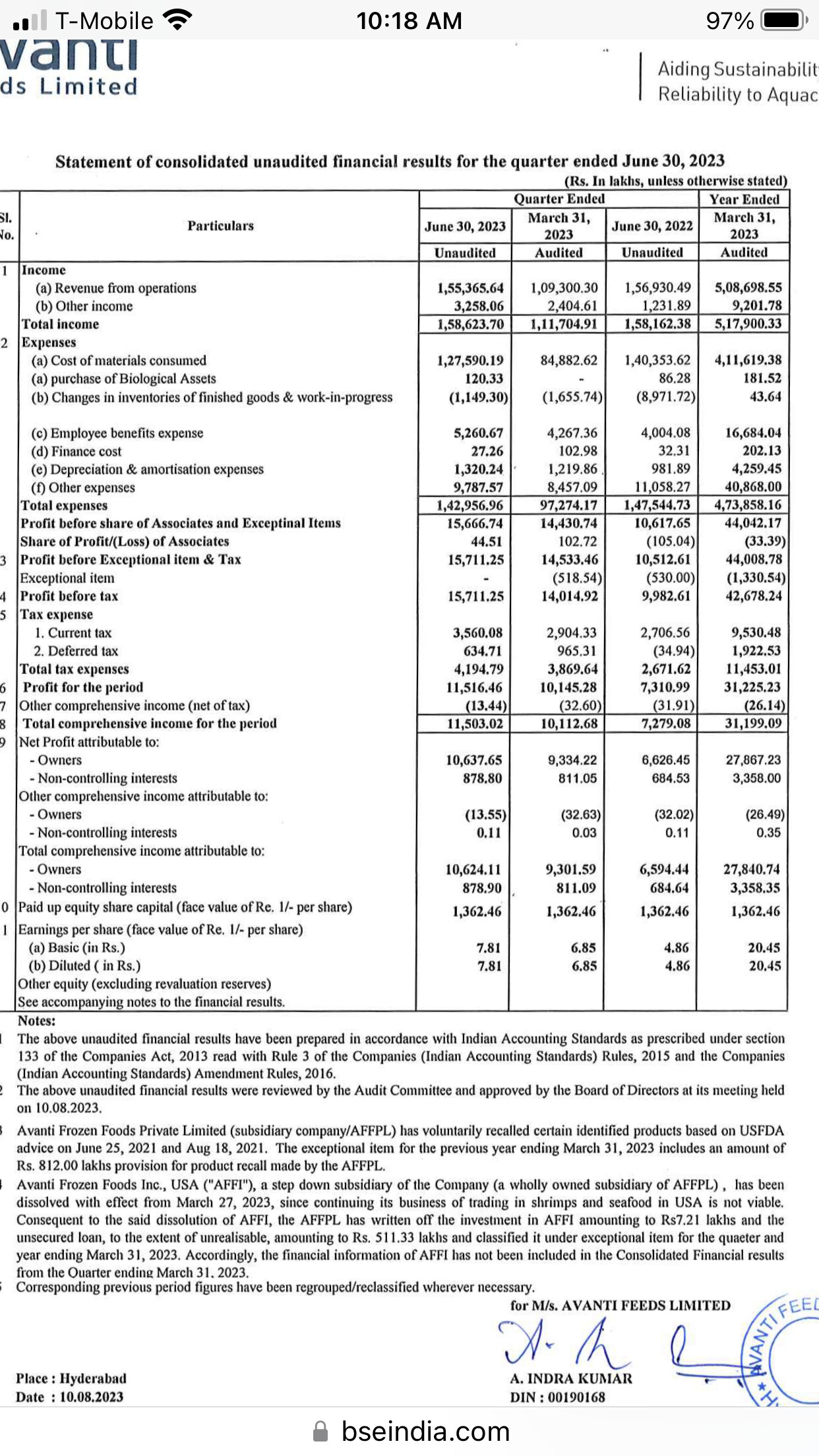

Q1 Results

5 Likes

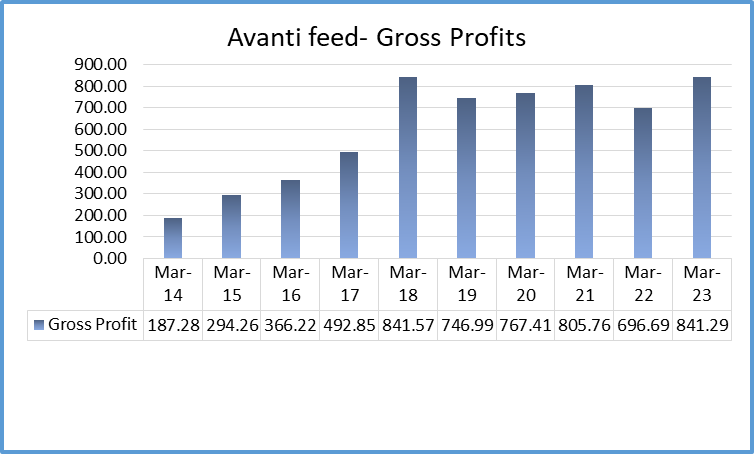

Avanti’s gross profitability hit all time high !

Though the company grew its revenue in last few years, its gross profits were all over the place.

3 Likes

Some highlights from Q1 FY24 earnings call

Input cost outlook

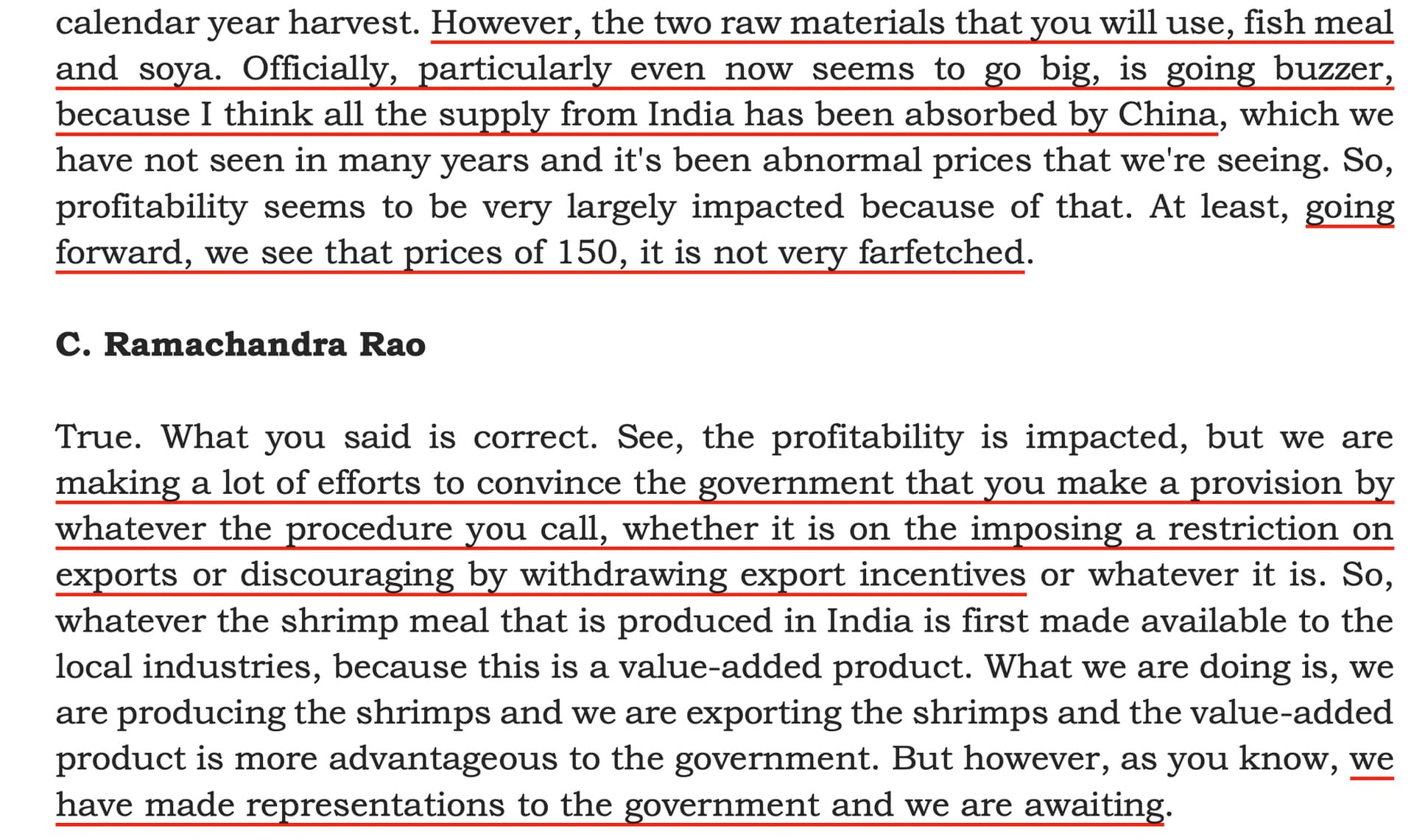

The raw material costs are still high. It is expected to be high in Q2 and possibly rest of FY24.

The freight costs have come down, which helps a bit.

Revenue growth prospects

Management commented that the outlook of shrimp culture industry is a bit bleak. The import of brood stock fell by as much as 40% in Dec-Mar 2023. This means that the demand will be severely impacted.

Demand outlook

Previous year demand was dampened due to inflation. China is also suffering from economic woes resulting in drop in demand.

The company is trying to diversify into different market and into value added products. Though the demand is expected to recover, it is still very early to say when it will happen. The management did mention that things are not playing out as what they had predicted earlier.

Margin sustainability and Profitability

The industry is suffering from high cost and an oversupply issue that puts pressure on margins.

CapEx items

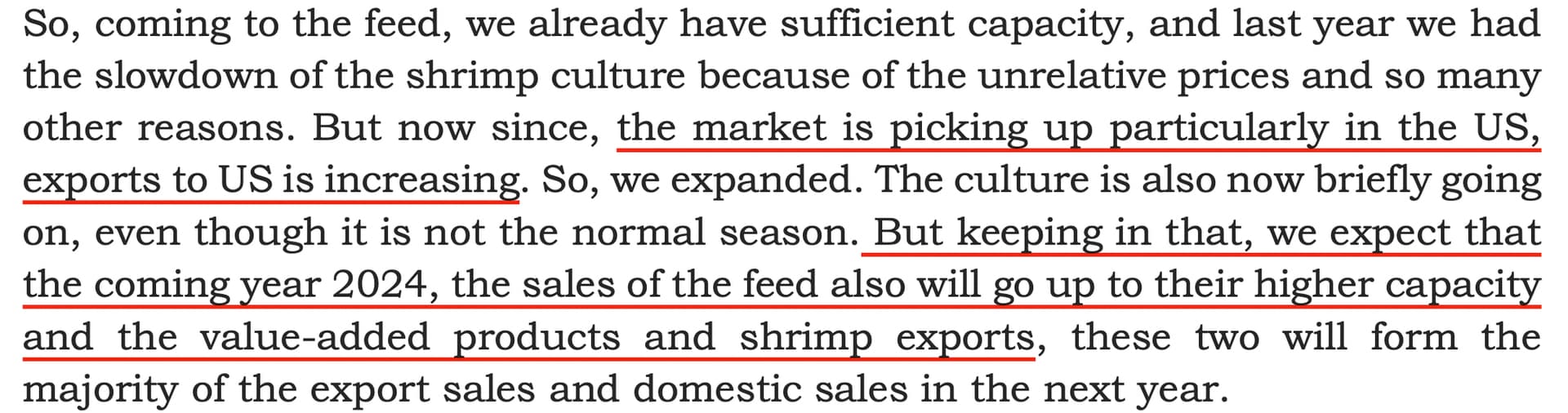

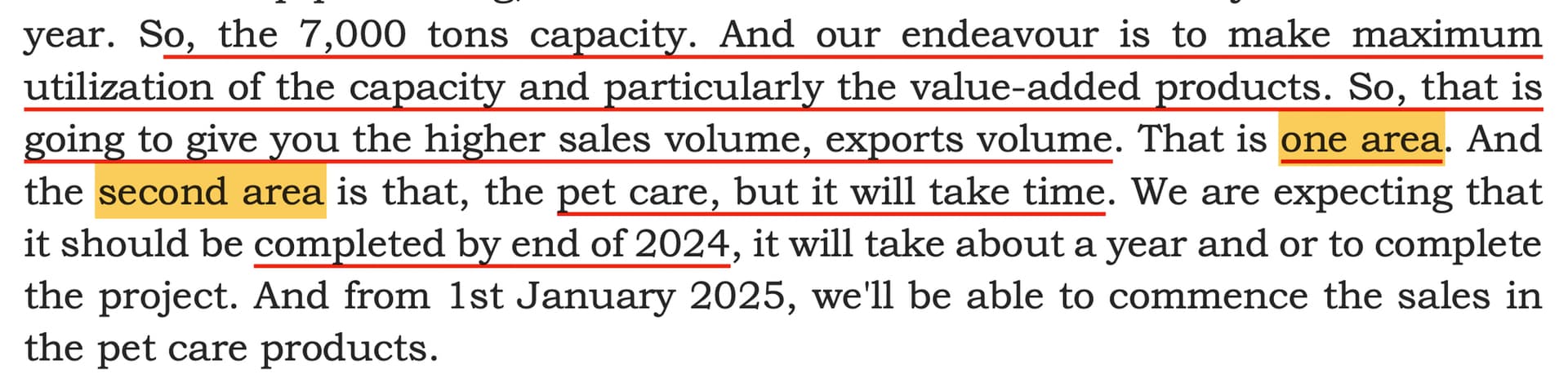

The additional shrimp processing facility will be online in Mar 2024. Besides that, they are also investing on fish feed plant to venture into the fish industry which will be in collaboration with Thai Union. However, the capacity utilization will still be low in next 2 years.

Cyclicality

It looks like there will be a bit more downside in FY23. Yet to reach cyclical bottom as the worst is still to come. Nikhilesh mentioned that the shrimp price is probably at lowest point and we might witness some consolidation in next 16 to 24 months. But, the management lacks confidence in foreseeing any improvements in FY24.

Meanwhile, the company has invested on capex, which would provide it enough flexibility in capitalising recovery when the cycle turns.

Outlook

The company for sure will be under continuing tremendous pressure in FY24. However, they have enough gun powder to navigate this cycle and are still profitable.

Some core hypothesis

- Input cost would gradually decrease going ahead

- Demand will start to pick up from Christmas season.

- Shrimp price will increase slowly as we are probably at lowest point (Q3 onwards)

- CapEx would help to slingshot during cyclical recovery from FY25 onwards

Disc: Invested and having a SIP to accumulate

15 Likes

2 Likes

Seems like encouraging signs for the sector.

9 Likes

Avanti Feeds has disclosed the setup of Avanti Pet Care Pvt Ltd to the exchanges. Good to see the management finally walking the talk. They had brought this up few years ago and were at the time hesitant due to market conditions not being suitable.

5 Likes

Seems to be a PVT LTD tho!

2 Likes

Q2FY24 Results

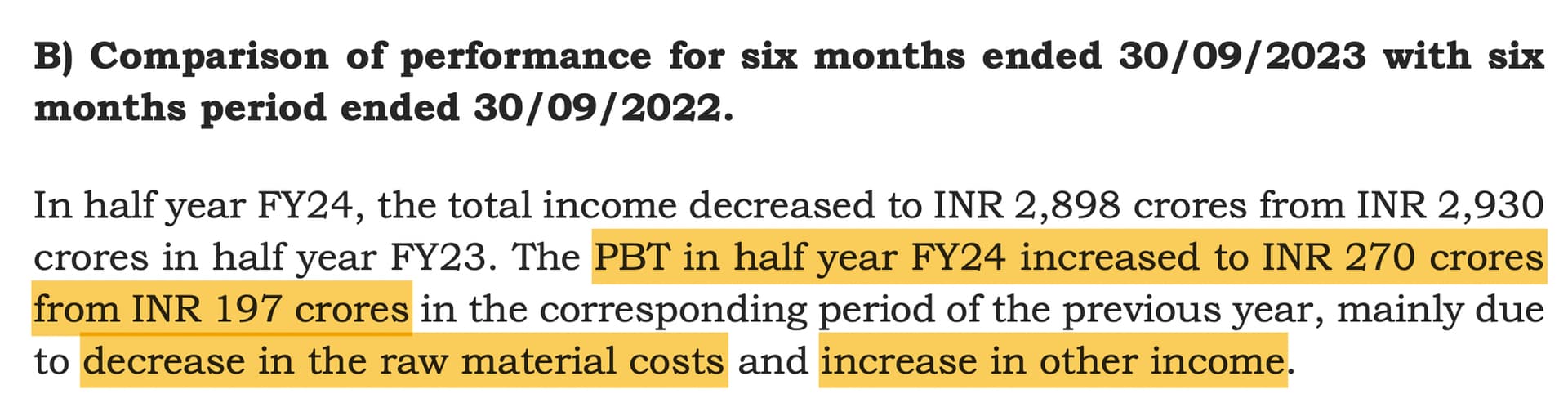

Comparison of performance for six months ended 30/09/2023 with six months period ended 30/09/2022

Revenue (Consolidated)

- The total income decreased to INR 2,898 crores from INR 2,930

- The PBT increased to INR 270 crores from INR 197 crores (mainly due to decrease in the raw material costs and increase in other income)

Standalone Results

FEED DIVISION

- The total income increased to INR 2,415 crores from INR 2,352 crores in half-year ended FY23 due to increase in feed sales and other income.

- The PBT in HY FY22 increased to INR 212 crores from INR 130 crores in the corresponding period of the previous year, mainly due to decrease in raw material costs and increase in other income

SHRIMP PROCESSING DIVISION

The gross income for six months during FY24 was INR 491 crores as compared to INR 583 crores in corresponding six months’ period of the previous year. A decrease of INR 92 crores in the gross income during first six months of the FY24 is mainly decrease in quantity of sales by 1,144 metric tons

The PBT in six months FY24 is INR 63.60 crores as compared to INR 63.10 crores in the six months ended in FY23. The marginal increase in PBT is due to decrease in cost of raw materials consumed at ocean freight rates.

- No additional provision made to compensate for recall of the products (all the earlier provisioning is used up, 0.99 cr left )

Note : As regards the product liability claims for bodily injury caused by consuming company’s contaminated product under the recall, the company has submitted a revised claim for the claims received and settled by the company to the insurance company. The surveyor has confirmed that the claim will be processed by insurance company on or before 30th November 2023. Since the liability has been covered under the commercial general liability insurance policy, no provision has been made in the financial statements of the company.

Projections for the rest of the year

Feed :

On the basis of estimated shrimp production in 2023, the estimated feed consumption is about 10.5-11 lakh metric tons. The company’s feed sales during the previous year FY22 was about 5.41 lakh metric tons as compared to 4.73 lakh metric tons in FY21, an increase by 68,000 metric tons. However, the company’s estimated shrimp feed sales were 4.97 lakhs metric tons in FY23, down by 44,000 metric tons when compared with FY22. The company’s estimated production in sale of shrimp feed in the calendar year 2023 is about 4.9 lakh metric tons at the same level as in the previous year, when

the total Indian feed consumption is down by 15%. The company has been able to maintain its production and sales, though there was overall decrease in the country.

SHRIMP PROCESSING & EXPORT:

The countries vannamei shrimp exports in terms of value declined in FY23

compared to FY22 by 8.11% from $5,234.36 million to $4,809.99 million. The country’s overall exports of frozen shrimp in quantitative tons for FY23 was 7,11,099 metric tons as compared to 7,28,123 metric tons in FY22, a decline of 17,024 metric tons representing 2.34%. The company’s shrimp exports during the FY23 was about 12,497 metric tons as compared to 12,836 metric tons in the FY22, a decrease by 339 metric tons. It is estimated that the export during the FY24 would be around 12,000 metric tons.

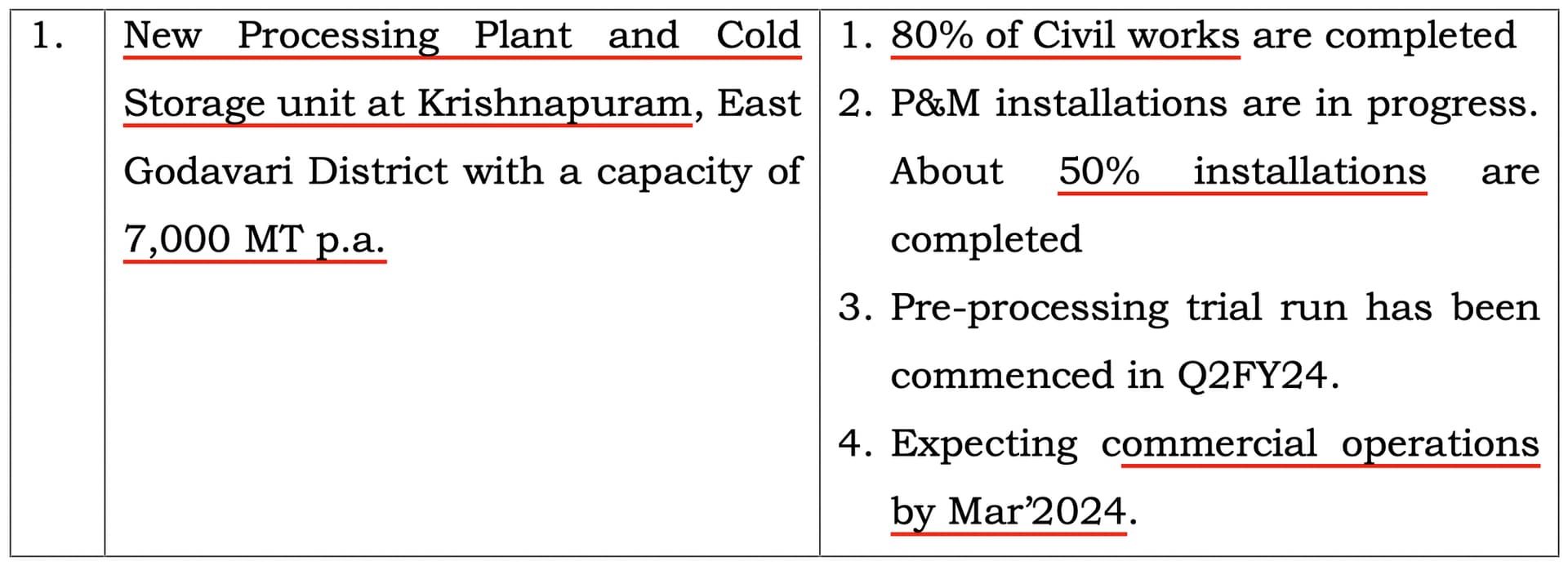

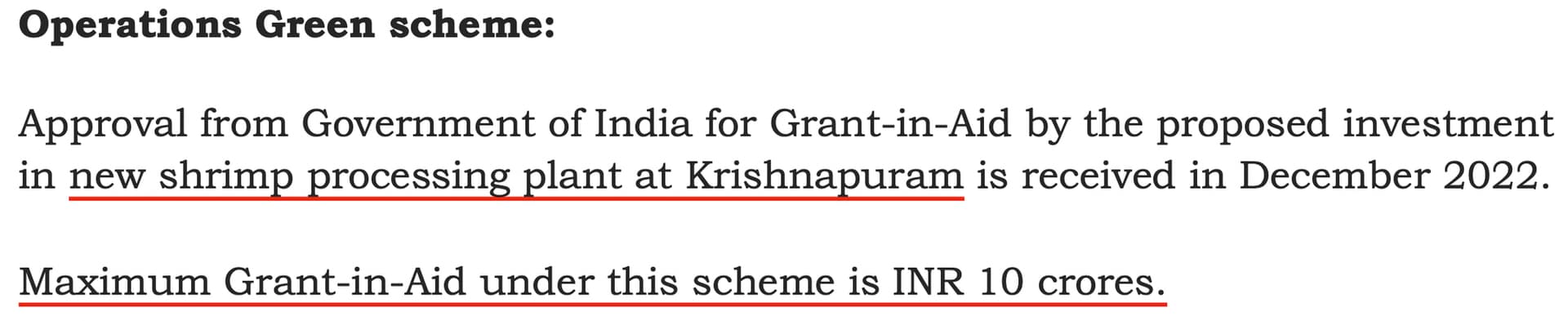

- New Processing Plant and Cold Storage unit at Krishnapuram, East Godavari District with a capacity of 7,000 MT p.a. (Expecting commercial operations by Mar’2024 )

New Initiatives

- PET FOOD : Entering into JV with Bluefalo Pet Care Company Limited Thailand (51% by Avanti and 49% Bluefalo) - Market research is in progress about the demand for Pet products in Indian market (Aiming to launch to market by 1st Jan 2025)

- FISH FEED : Huge shortage in the domestic market , most of it is being exported to address this issue working on initiatiative to make it locally for captive consumption and sell in export markets, market research is in progress, an agreement is signed for tech. transfer with Thai Union Feedmill

Raw Material prices are stable , may go down in coming months due to new crop is coming into the markets

7 Likes

A lot of competition from shrimp in Ecuador…I dont think this will go up for some time

1 Like

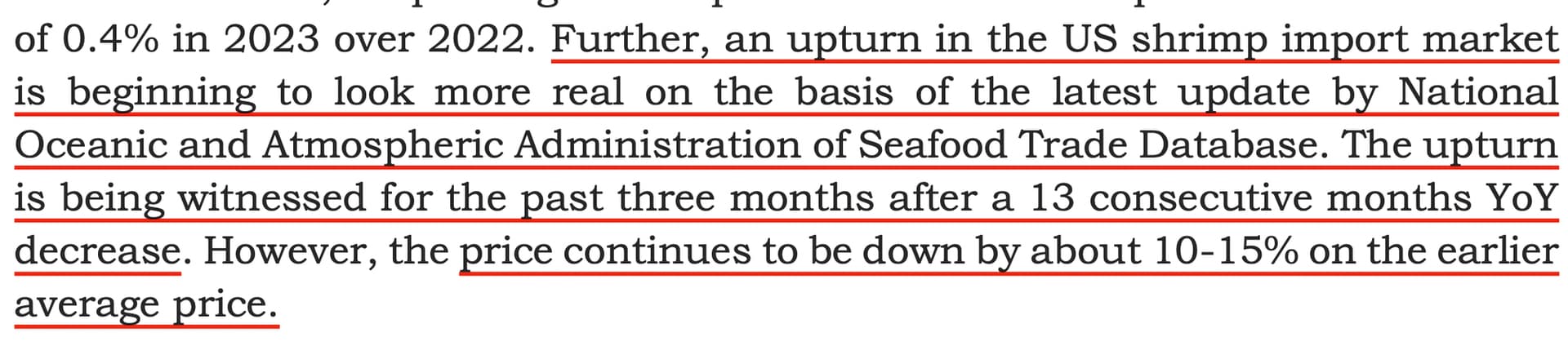

US shrimp market seems to be reviving in last 3 months, although realizations continue to be on the lower side. It looks like shrimp sector has bottomed out. Concall notes below.

FY24Q2

- Present RM price: 138/kg fish meal (vs 127/kg last quarter), 54/kg soyabean (vs 54/kg last quarter), 29/kg wheat flour (33/kg last quarter)

- Shrimp processing capex (will get 10 cr. state government support in this capex)

- US shrimp import market has seen improvement in past 3 months after 13 consecutive months of YOY decrease. However, realizations are lower by 10-15%

- Petcare: technical know-how will come from Bluefalo Pet Care Thailand, Avanti will hold 51% in this JV. Expect commercialization in by Jan 2025

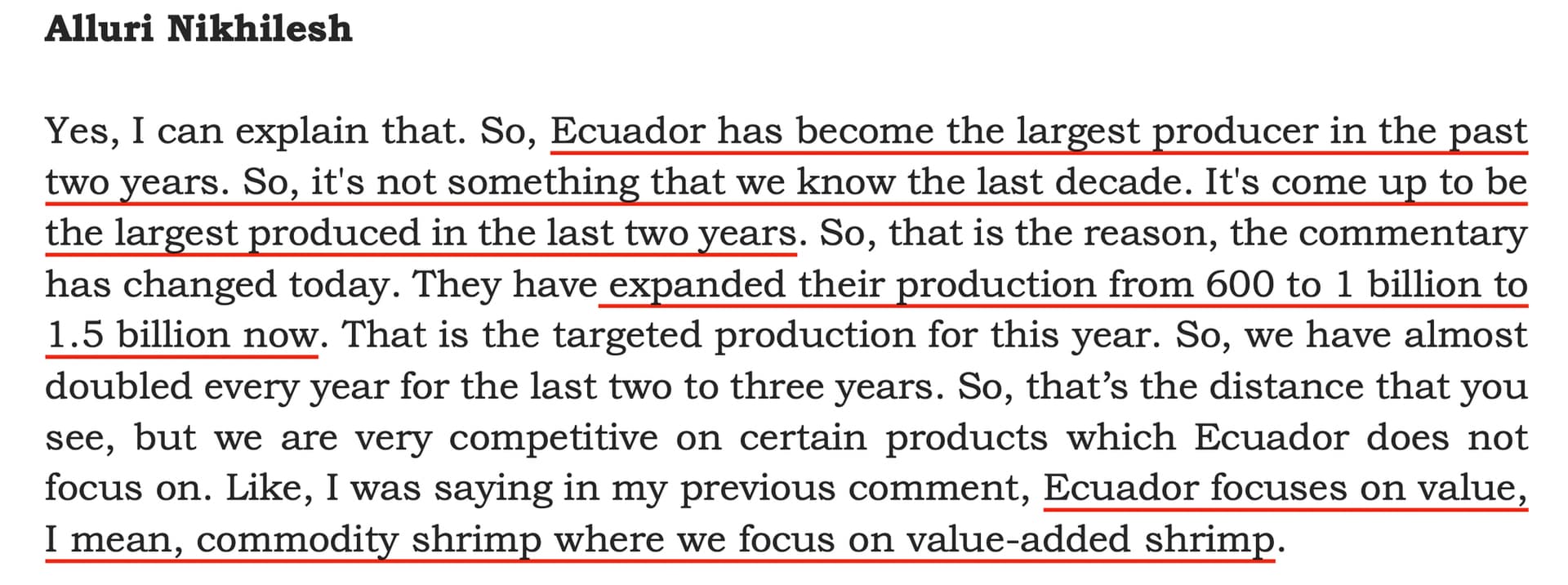

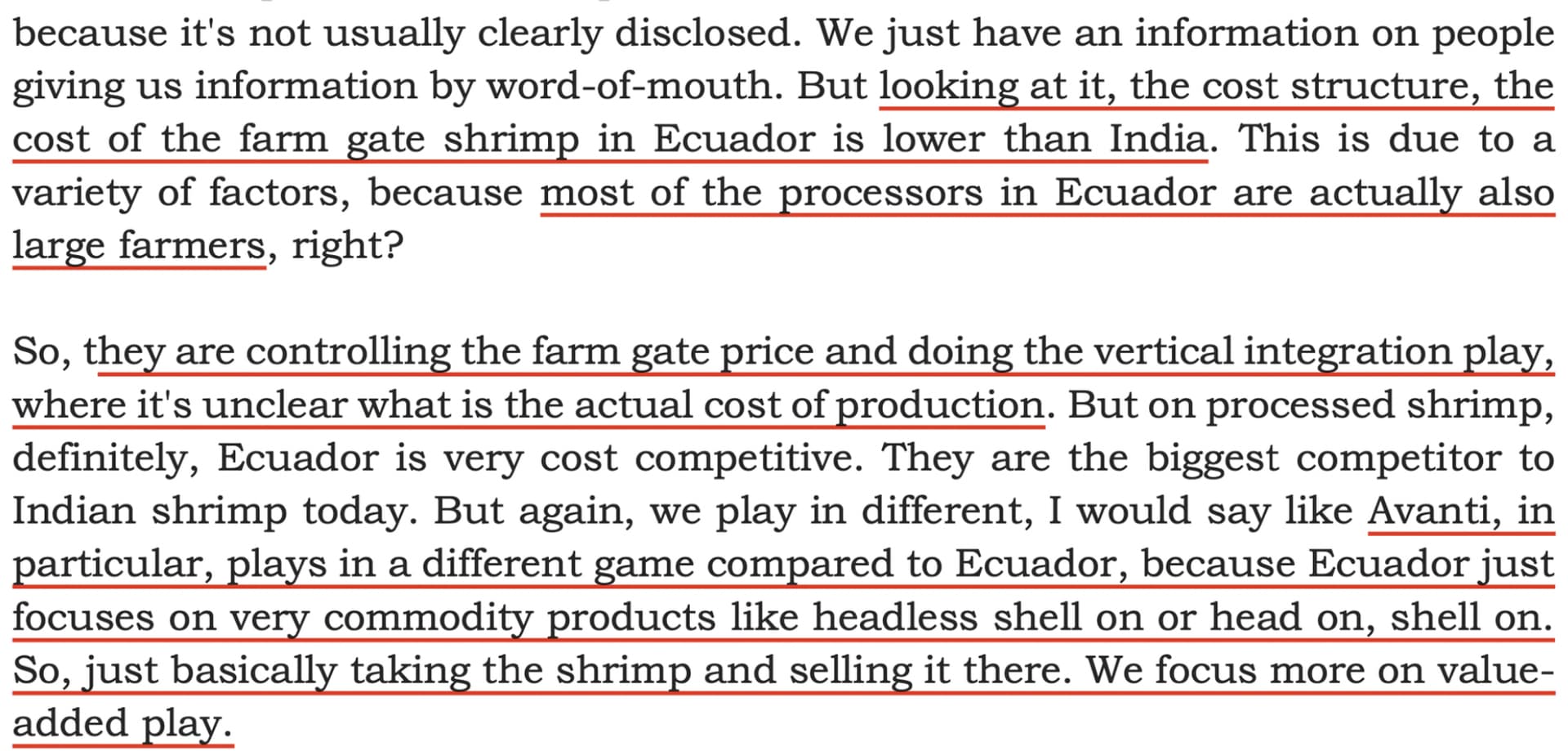

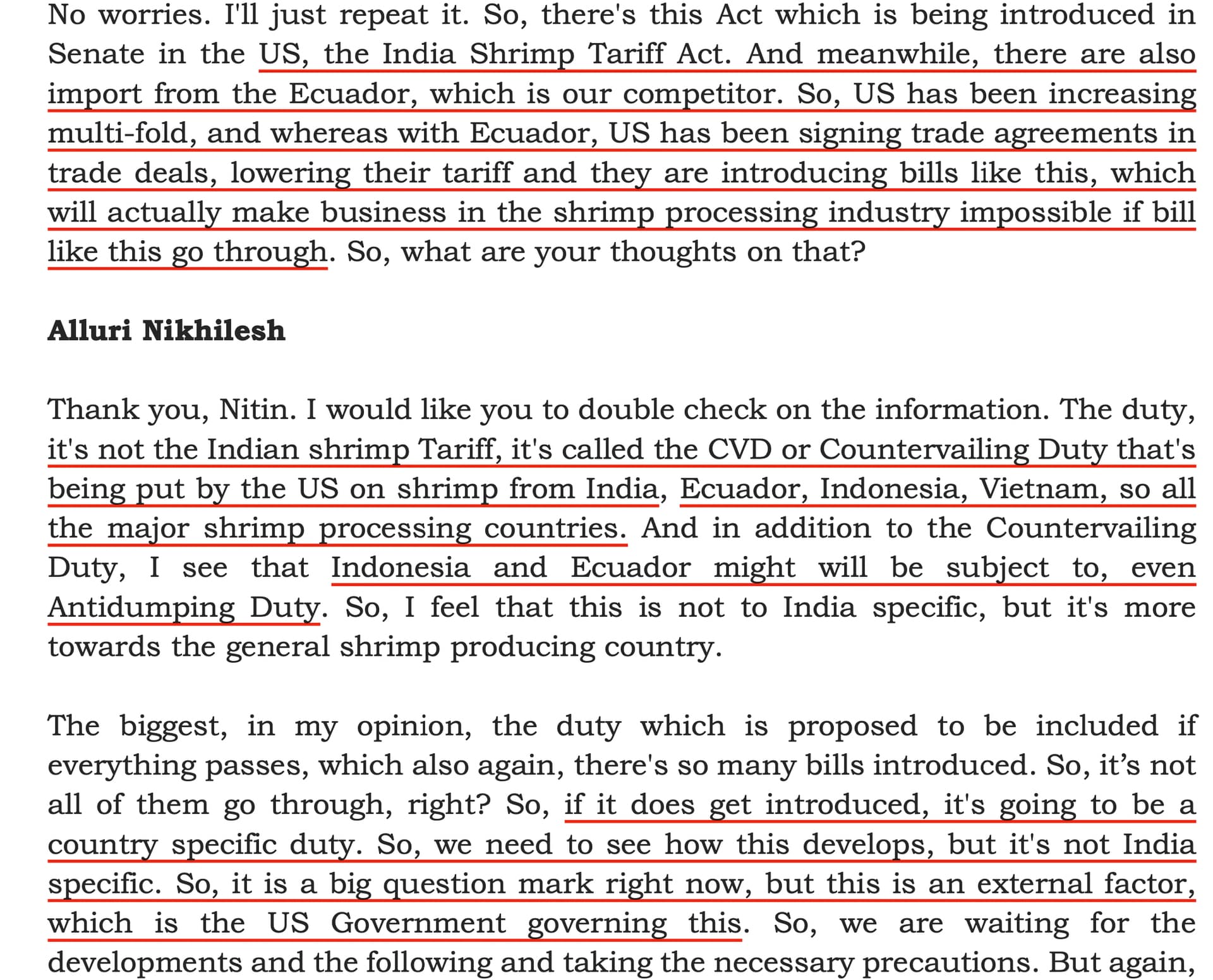

- US Countervailing Duty: Being proposed on shrimp exporers from India, Ecuador, Indonesia, Vietnam. In Indonesia and Ecuador, there might even be Antidumping Duty

- Ecuador has a lower cost of production of processed shrimp as processors there are large vertically integrated companies. Additionally, they have become the biggest producer of shrimp in past 2 years (from production of 600 mn to 1.5bn now). Ecuador focuses on commodity products like headless shell on or head on, shell on shrimp

Disclosure: Invested (position size here, no transactions in last-30 days)

9 Likes

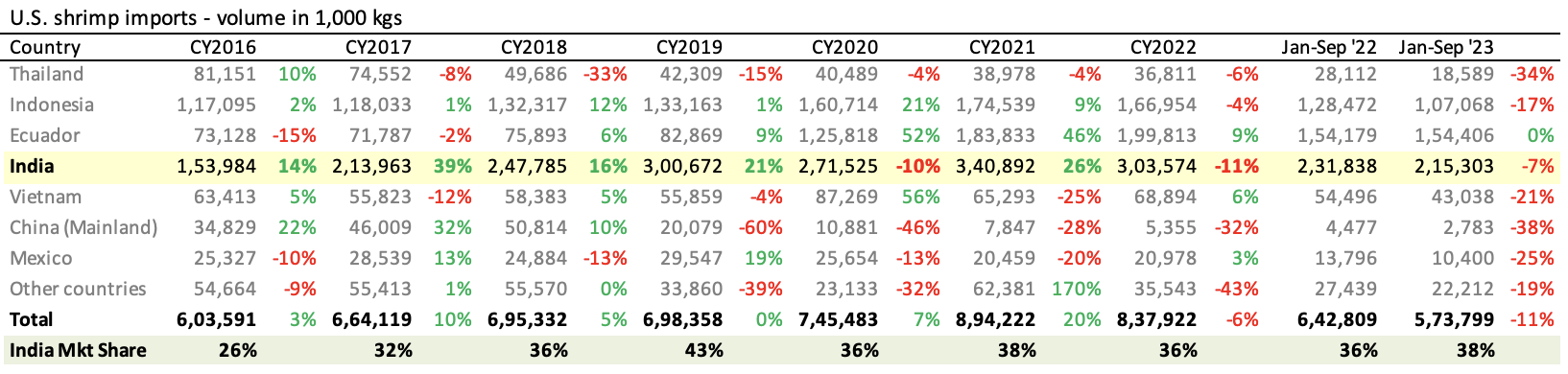

Encouraging. Some data to chew -

The table illustrates the volume of U.S. shrimp imports from various countries over the years.

Key takeaways:

- U.S. shrimp imports have shown consistent growth over the years till CY21; degrowth in CY22 and YTD!

- India has seen a substantial increase in its market share of U.S. shrimp imports till CY19; peaked at 43%. De-growth to 36% by CY22. YTD has rebound to 38%

- Ecuador has seen stunning growth in CY20 and CY21; growth rate has tapered since then

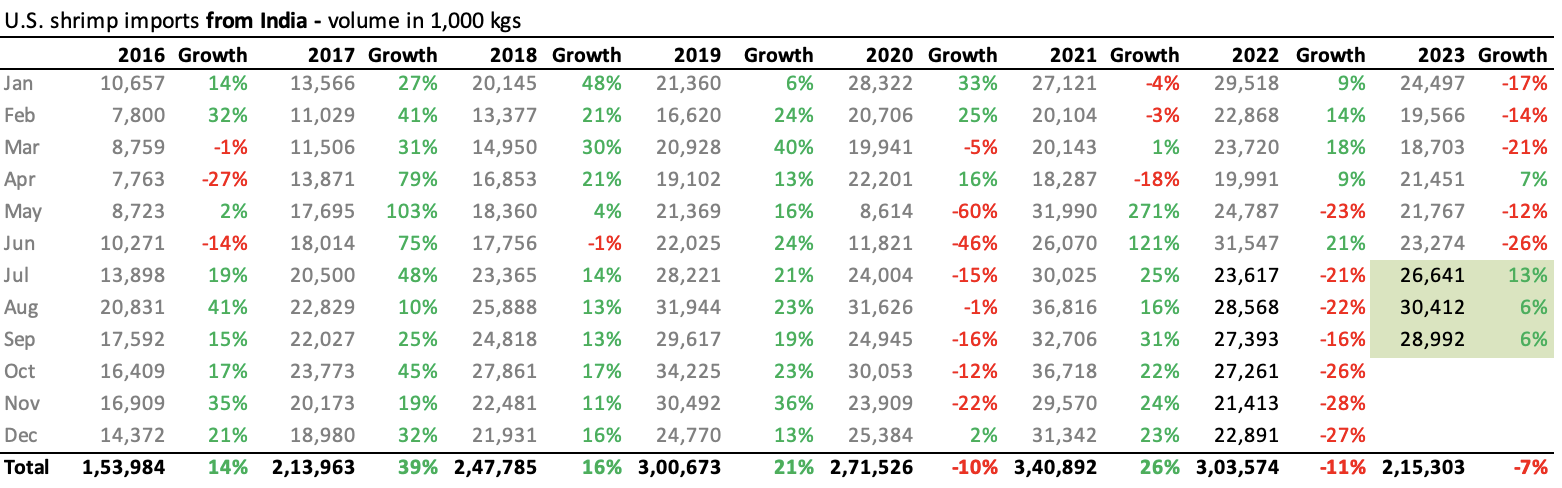

Key takeaways:

- India has seen YoY growth in Jul-Aug-Sep '23 of U.S. shrimp imports after nearly 14 consecutive months of YoY degrowth

Source: https://www.fisheries.noaa.gov/foss/f?p=215:20:9994685233348:::::

18 Likes

Hi Harsh,

Among Avanti and Apex Frozen which should benefit most with revival in sector?

Thanks

Some General pointers for basic understanding of the cyclicality in the shrimp business and mapping the points discussed in the Q2FY24 with the company:

- Normally, the shrimp culture season starts in end of January or February

- Shrimp Feed Consumption :

- Raw Material pricing : Major component of expenses

Ecuador Vs India explained :

Cost Structure Comparison :

Financials

- Sales have not seen any improvement in the last couple of years due to fall in shrimp prices and Ecuador chipping in market share.

- But we have to see what has led to the fall in expenses which seems like to be the reason for a growth in profit?

- Snippet from con-call

- Seeing the Operating Profit Margin trend, single digit has been seen only in 2013 which was a decade back, from there on the margins had improved.

- Also there has been other income increase

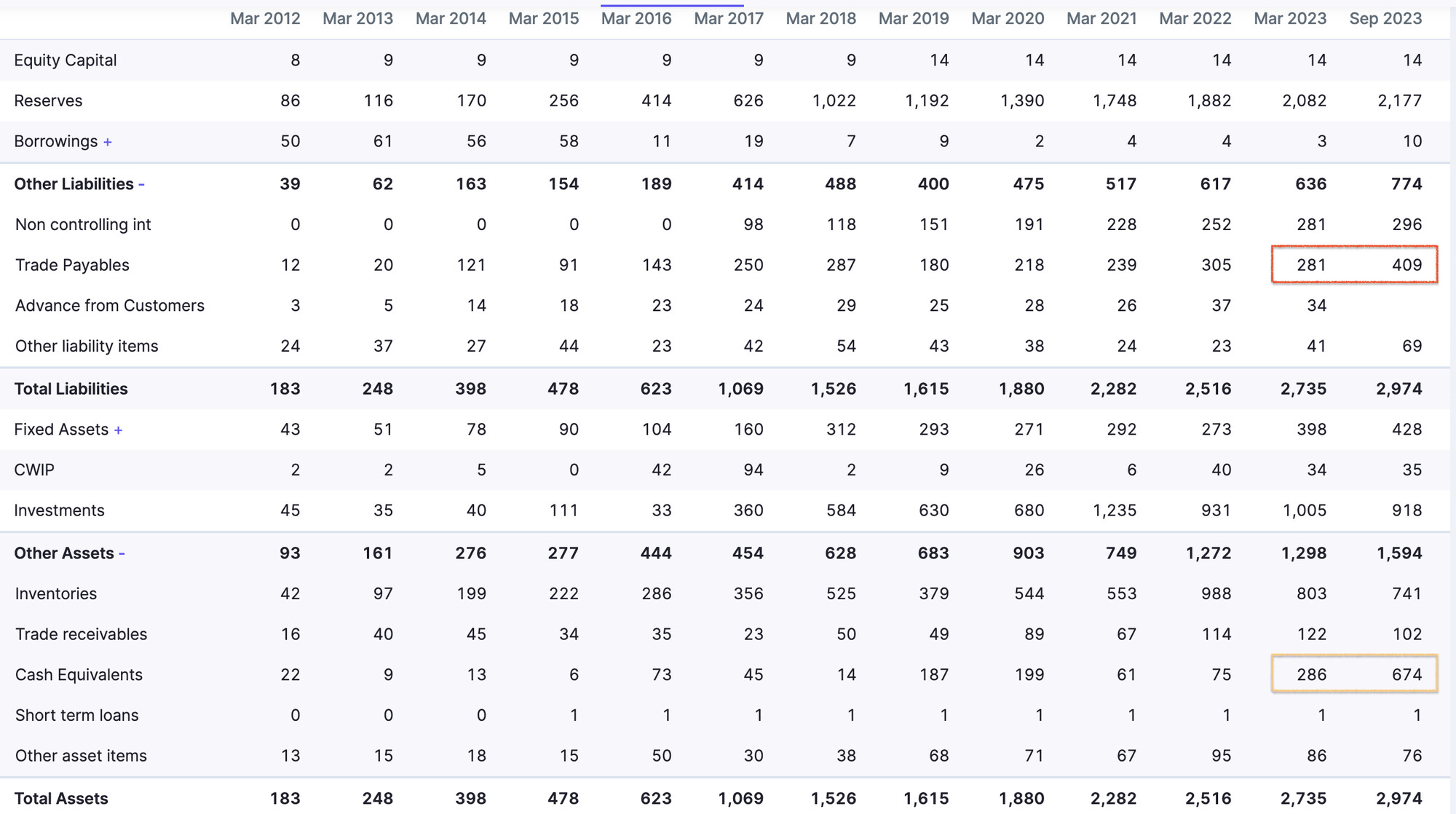

BALANCE SHEET

-

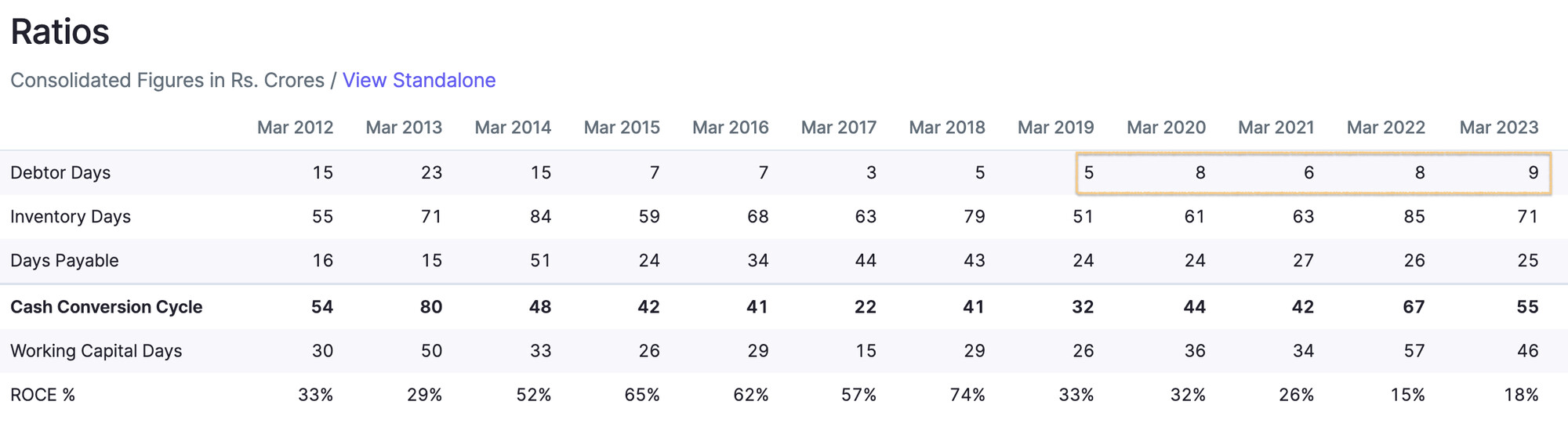

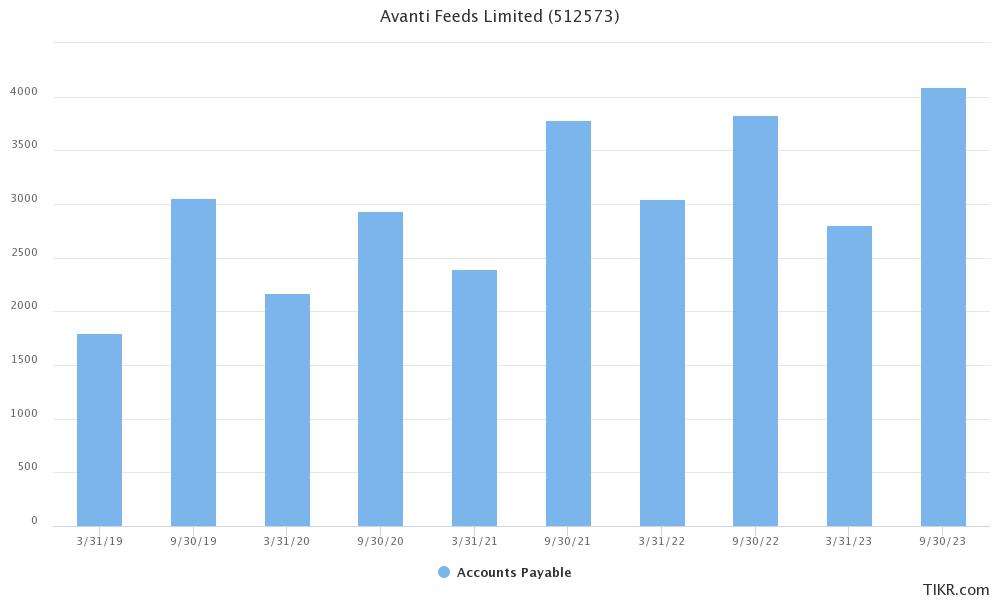

Why have the trade payables increased so much, it is a liability after all so need to be looked at because due to this the profits would have an upward bias

-

They are holding extra cash than what they used to

- Not much investment opportunities ?

- Not sure about the near future ?

Answer : Received from con-call

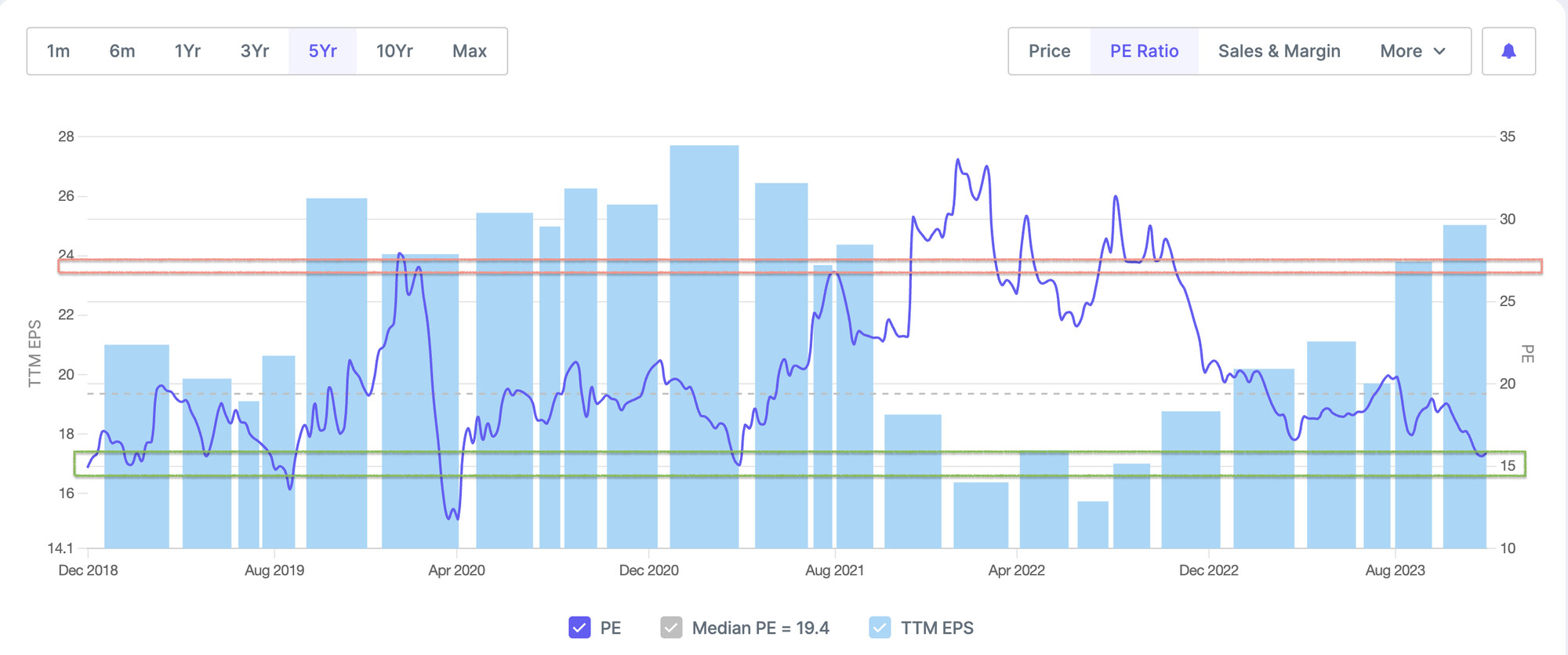

Ratio Analysis

- Seeing the last 5 years PE ratio, 15 times has provided a value comfort and as the margins improve we can see it go 22-24 times i.e. 50%+

- The increase in debtors is a seasonal play and would be in single digits only as mentioned by the management

Growth Triggers :

- Optimistic outlook for an increase in sales in the second half of FY24

- ************************First Area : New plant coming up which would start contributing to sales

- More on Second Area - Pet Care :

************************************Additional Benefits :************************************

Risks :

- Possibility of an imposition Tariffs/Quotas by US to regulate import prices

- Possibility of a further increase in raw material prices like Soya & Fish Meal

Technical Analysis :

With an intermediate support of 375( No reco, do your own due diligence)

I have summarised the point in this thread too - https://twitter.com/Lakshayy_99/status/1728689844136943949.

Do let me know your thoughts, and correct me if there’s any thing incorrect. Hope you gained some insight from this :)

19 Likes

This is a normal H1 phenomena, please look at payables at end of each H1 during past few years, this year its not abnormal.

9 Likes

Export of shrimp meals by indian manufacturers to china is biggest problem faced by indian shrimp industries. Indian manufacturers prefer to export china market as ther are getting very good rate by exporting to china. Government is also not regulating the export by indian manufacturers because it is getting valuable foreign exchange. I think Avanti needs to fully backward integrated in terms of shrimp feed rather than going for new expansion in pet care.

@harsh.beria93

Disc: Not holding, just reading out of curiosity. Correct me if l am wrong in understanding of prevailing market conditions.

1 Like

I hope you know that fishmeals are harvested out of the sea, do you want Avanti to start fishing now? While making shrimp feed, Avanti also consumes soyabean and wheat flour. If prices of soya and wheat increase, should they start farming soya and wheat as well? There is a limit to backward integration!

26 Likes

Hi Harsh, I have read about your views about Avanti, Sharath, but not about Apex Frozen. Do you find any major issues with Apex?

1 Like

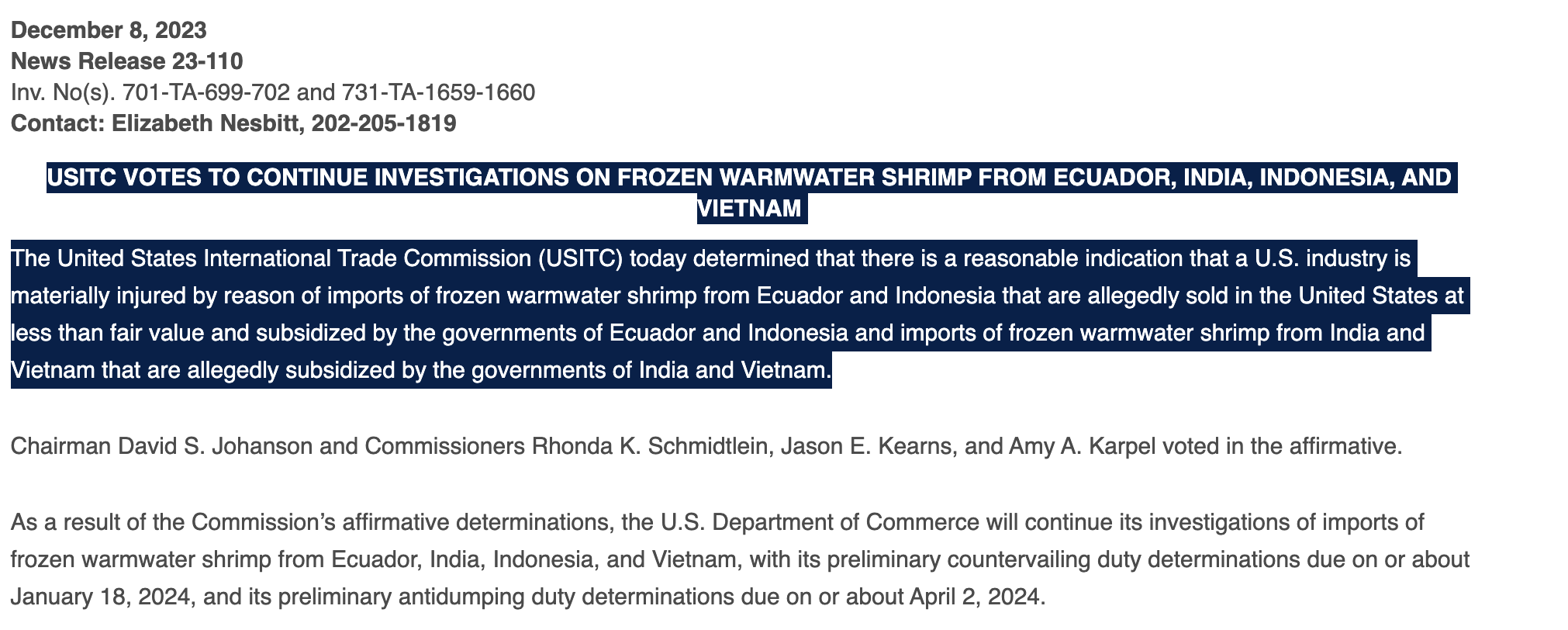

Latest update on ADD and CVD from US

US ITC (International Trade Commission) has voted to continue investigations for AD and CVD. [source]

So far proceedings seems to be going as per expected timelines. Next steps regarding investigations to be conducted by US DOC (Department of Commerce) are the time consuming parts, especially for ADD related investigations.

Expected timeline is as below [source] -

PS: Alleged dumping margins on Ecuador is 9.55% to 25.82% and Indonesia is 26.13% to 33.95%. CVD on Ecuador, India, Indonesia and Vietnam seems to be a non-event with <2% impact.

17 Likes

What are the chances that anti dumping duty is imposed on India along with Eucador and Indonesia? Near term uncertainity is hanging on business model of Avanti feeds in my opinion. what are the signs to look out for revival in shrimp industries till anti dumping duty is imposed on Eucador and Indonesia?

4 Likes

Hi @tpatel

Thanks for the super useful information and case source…!!

We should keep a close tab of the developments here.

Overall I feel the industry has consolidated for last couple of years and if the recent trends are to sustain then there could be some recovery and then going forward if the judgement on duties is favourable then it all could finally play out…and Avanti has been a good performer even during the difficult phase of Industry.

Also, one thing that I want to bring to your notice…

My interpretation is that the subsidies that these countries are offering is more than 2% which is higher than the limit allowed by US for imports coming from developing nations…and the final CVD & ADD will be decided and levied based on the case proceedings.

Regards,

Yogansh Jeswani

Disclosure: Invested

4 Likes