What is their logic behind dismissing Ecuador as a concern?

11 Likes

Hello Harsh,

I went through the annual report and have the below query on their declining operating profit.

26,427.74 in FY21-22 against 40,419.30 in FY20-21

This is despite an increase in the revenue. Can we attribute to the lower profit only to increase in raw-material cost (feed, packaging, logistics) which they are not able to completely transfer it to the farmers who are their main customers?

Also I could see a huge negative inventory affecting its operating cash flow. This is contradictory to their statement that despite COVID challenges, the sales has increased. If so, why this unsold inventory?

(40,133.52) in FY21-22 against 5,702.52 in FY20-21

Disc: have a small tracking position and planning to add more once the price bottoms out and start an upward trend

4 Likes

1 Like

The increase in inventory in FY21-22 was due to the firm acquiring a lot of the RMs uupfront, anticipating the significant inflation thorugh most of CY22.

Also, most of the margin pressure is attributable to the RM headwinds, which should subside from here (already improving sequentially basis management commentary).

4 Likes

Flattish sales from Avanti with revival in margins. Q4FY23 looks ominous, with 25% decline in shrimp seed sales in the first 45 days of the quarter. Concall notes below.

FY23Q3

- Expect CY23 shrimp production at 8.5 lakh MT (vs 9 lakh MT in CY22)

- Present RM price: 110/kg fish meal (export prices are 150/kg causing hike in domestic pries), 57/kg soyabean, 36/kg wheat (expect price softening)

- Annual fishmeal production is 3.75 – 4 lakh MT and Shrimp Feed Industry consumes 3 lakhs MT

- Until mid-February’23, shrimp seed stocking was 5700 Mn vs 7800 Mn Seed during last year

- Lost 50,000 MT of feed sales due to delay in commissioning of new plant

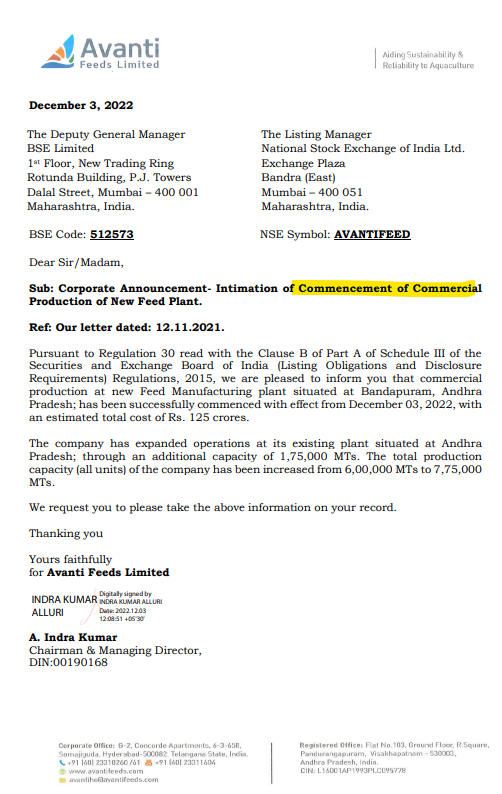

- Feed Capex: Completed expansion of 175’000 MT in December 2022 which will contribute 25% more sales at full utilization

- Shrimp processing capex

- Focusing on value-added products shrimps, where margins are higher. Started 2-3 categories of value-added products (current share of value added products is 25% of sales)

- In value added shrimps, can only operate at 60-65% utilization as it requires more manual work

- Peak season working capital requirement is 800-900 cr. Despite that, they still have 1000 cr.+ cash

Disclosure: Invested (position size here, no transactions in last-30 days)

5 Likes

Avanti Feeds might be at or reaching cyclical bottom. There could be a bit more pain and re-rating could be slow due to macro conditions. But, from a 2 year horizon, this seems to be a good time to accumulate.

Some of my rationale for identifying this as cyclical bottom:

- Input costs for Avanti has increased due to increase in prices of fishmeal, Soybean, Wheat and Cereals. This is also affecting the poultry sector (you can check margins of Venky’s India as well). As a result, EBIDT & OPM margins are at 10 year lows for Avanti.

- US FDA restriction on cooked shrimp is also lifted. But, it hasn’t resulted in export growth yet. Also, China is just opening up and consumption is expected to revive.

- Freight costs might be coming down, adding some cost savings.

- COVID has been a terrible period for the shrimp industry with demand faltering and production constrained. This has forced many farmers out of business and many going for a crop holiday till April 2023.

- Industry is still grappling with negative sentiments from farmers (demand side). The problems got worse to the extent that government needed to step in to mediate pricing on feed as well as offtake.

- This resulted in Avanti not being able to increase feed price and at the same time forced to absorb high raw material cost.

- There is severe lack of automation and technology use in shrimp farming. 60% of farmers are small and marginal.

- Indian domestic consumption has not been tapped well. Given that Indian diet largely misses animal protein (with poultry as the primary source), there is a good scope for shrimps to fill in the gap

- Meanwhile, Ecuador is proving to be a tough competitor recently, capturing India’s export market share. To me, this is a significant reason for the downcycle to be a bit more prolonged.

- Lastly, the frequency of posts in this thread is also at bottom

, indicating negative investor sentiment.

, indicating negative investor sentiment.

Positives going ahead

- On a long term aspect, India has huge land availability for shrimp farming. Coupled with increased domestic consumption, I am optimistic on sustainable growth rate of above 10% (might take a while to dig out of current cycle)

- Govt has reduced duties on fish feed and is trying to support the industry through policies

- CAPEX and commissioning of new plant will yield good topline growth and better ROCE

- Potential to look into fish feed market which would be another leg of growth

- Potential for margin expansion from value added products

- Stock price is reaching attractive levels now (PE<20) compared to the potential earnings going ahead

- Company has enough cash to survive and exploit the cyclical nature of industry. They are also rightfully holding the cash for working capital purpose than just to reduce cash in balance sheet

Not sure if Avanti is applying waste management processes. For example, shrimp heads can be reused in feed, shrimp shells can be used to extract chemicals for pharma and paper industry.

Reference

A good overview on Indian Shrimp industry and recommendations to govt and industry

Disc: Started nibbling with SIP

18 Likes

I think no one is considering the investments of Avanti Feeds in NCDs and how it will react to the interest rise.

1 Like

As long as ANDHRA pradesh current govt is in power it’s difficult for Avanti feeds to make money. farmers are grappling with huge losses in ANDHRA PRADESH the election is due next year.once the election is over they may provide a slight breather for avanti feeds.caste equations are also at play here.

5 Likes

Spoke with two farmers from AP state to understand current situation:

Andhra Pradesh shrimp farming was not doing well. Things were really bad during September,October,and November of 2022. Disease impact was high during last season. Even if the crop was good, shrimp prices were low which affected farmers. Even the offtake of shrimp from ponds was delayed by companies. When things were good everything use to happen within a day. During last season farmers have to wait for 2-3 days for the buyer to come take shrimp. Sept-October period farmers barely made any money.

Due to such bad conditions around 20% of farmers have moved to fish farming and some have just stopped further shrimp farming.

Feed cost was also continuously increased by companies. This has been stabilized during the last 2-3 months without further hike. Presently a 25kg bag costs around Rs.2000.

Cost of probiotics, vitamins used in shrimp farming also has increased.(probiotics are supplied by sanizymes, intas, ?avanti. etc…)

AP government is not giving electricity subsidy to farmers which is adding to the farmers burden. Power cost which used to be Rs.1.75 per unit is now at Rs.4 per unit. At present running cost of electricity is around 7k to 8k per acre( at Rs. 4 /unit). In general power cost is less during the first month of shrimp farming as all aerators need not run but increases from second month. Finally subsidy may be given in the next 1-2 months as the Govt has started collecting documents from farmers.

If the initial infrastructure is in place the present running cost per acre is around 5 to 6 lac per acre which used to be 4 to 5 lac 3 years back. This cost included seed, probiotics, power, labor ,etc…)

In general Avanti and CP food is preferred. There are few more players. One farmer mentioned Sandhya feed is doing well.

Currently things have started improving and farmers are happy with the present shrimp price.

Current price;

30 count: ~Rs.475

40 count: ~Rs.370

50 count: ~Rs.350

60 count~Rs.320

70 count~Rs.300

(this is last one week price)

Present season is better as the disease burden is less during summer.

Farmers who have stopped shrimp farming during last season have started again. Those who have shifted to fish farming will take another 7-8 months to come back. Once they start fish farming they have to wait for 8-12 months to get good fish output. Ultimately they will come back to shrimp farming if the current shrimp price is maintained or improves. In general fish farming is not as lucrative as shrimp farming for farmers and they have to do it at least 10-15 acres to get a decent amount. Shrimp farming can be done by small farmers with limited land.

(I am trying to speak with an employee of a company involved in processed shrimp export. Will update if I get any usefull information)

Discl: tracking

41 Likes

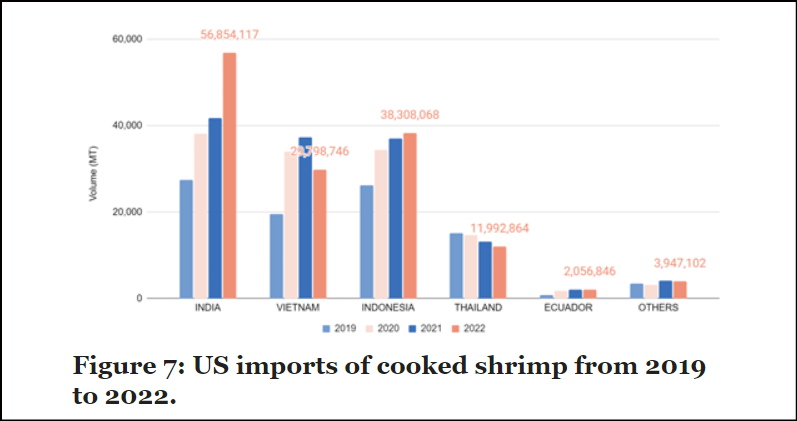

Good insights on Shrimp exports of India & Equador.

Increasing supply from equador and perception that equador shrimp is better quality than Indian seems to be problem that currently being faced by Shrimp exports from india.

11 Likes

From Godrej Agrovet concall

Am expecting margin pressure in current quarter as well. Let see what Avanti will tell us.

Disc: Invested. Might add bits at corrections with a 2 year view.

5 Likes

Want to share the highest value add article I’ve read on shrimp. It’s a long read on the shrimp space in India and Ecuador.

Some excerpts:

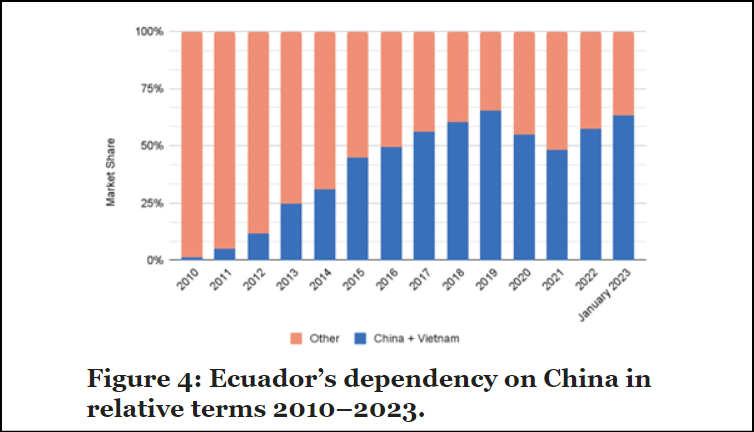

- How China has been Ecuador’s major market in the last decade:

- The case for how value add shrimp is the way to beat Ecuador:

In general, the key question for commodity shrimp is whether Ecuador has enough production volumes to service both Chinese + US demand. If most of their shrimp heads to China after the fall in 2020-2022, then a normalisation in US inventories this summer could start a revival.

Here’s another read on US inventories:

The blog I’ve linked to also has two fantastic reports on Ecuador and India.

23 Likes

Analyst report from Geojit is out.

IMHO, the business cycle is slowly starting to turn positive. The business momentum will pick up only by Q3-Q4 FY24. But, as expected the margin improvements come much earlier as input cost softens (takes a little bit of lag to process inventories though)

Disc: Invested

5 Likes

India investing on indigenous shrimp variety. Shows the increasing focus of government to support shrimp industry.

2 Likes

Announcement on BSE website that Avanti Feeds has incorporated a new subsidiary called Avanti Pet Care pvt ltd. Does any one on this forum know the business plan or intentions behind this?

1 Like

The management had announced plans to get into pet food industry some time back, could be inline with that.

3 Likes